|

市場調查報告書

商品編碼

2038678

2026-2035年新鮮蔬菜市場機會、成長要素、產業趨勢分析及預測Fresh Vegetable Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

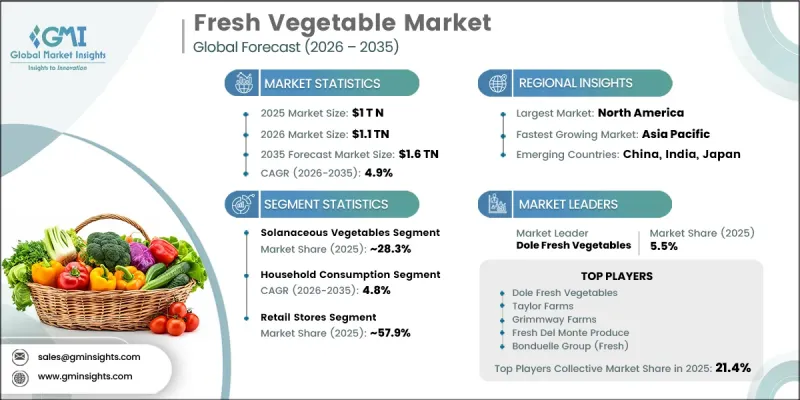

預計到 2025 年,全球新鮮蔬菜市場價值將達到 1 兆美元,並有望以 4.9% 的複合年成長率成長,到 2035 年達到 1.6 兆美元。

消費者對健康食品日益成長的偏好、不斷增強的永續性意識以及農業技術的進步正在推動市場擴張。隨著越來越多的人關注營養膳食並尋求更新鮮、無化學添加的食品,市場需求不斷成長。永續的農業實踐和環保意識強的消費習慣正在改變生產和分銷模式。精簡的供應鏈,以及農業技術和倉儲解決方案的進步,確保了全年穩定的供應。

| 市場規模 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 1兆美元 |

| 預測金額 | 1.6兆美元 |

| 複合年成長率 | 4.9% |

按用途分類,該市場包括家庭消費、食品加工、餐飲服務業及其他領域。家庭消費仍佔據主導地位,佔總需求的60.4%,因為消費者傾向於在日常飲食中優先選擇新鮮、加工較少的食品。人們對營養益處的認知不斷提高,加上推廣新鮮農產品的行銷宣傳活動,正在影響消費者的購買模式。向植物來源飲食習慣的轉變也是推動這一成長的因素,越來越多的消費者選擇營養豐富、加工較少的食品。

零售業佔57.9%的市場佔有率,預計到2035年將以4.9%的複合年成長率成長。隨著消費者越來越重視便利性、透明的產品資訊和穩定的品質標準,分銷管道正在迅速發展。超級市場和大賣場等傳統零售業態憑藉其豐富的商品選擇、具有競爭力的價格和全面的店內購物體驗,繼續發揮核心作用。同時,受數位化購物行為的轉變以及消費者對宅配服務和精準數位促銷的日益偏好的推動,線上零售業務顯著擴張,尤其是在疫情之後。電商平台提供詳細的產品訊息,方便消費者購買有機和特色蔬菜,並幫助企業接觸到更廣泛的消費群體。同時,農夫市集也越來越受到注重健康的消費者的歡迎,他們重視新鮮的本地農產品和透明的耕作方式,從而支持了當地農業經濟的發展。

預計到2025年,北美新鮮蔬菜市佔率將達到13.8%。該地區的需求成長主要得益於消費者對採用永續和在地化耕作方式生產的有機蔬菜日益成長的偏好。美國和加拿大的消費者正逐漸轉向更健康的飲食,包括植物來源食品。包括超級市場、零售店和線上平台在內的分銷網路正在擴大產品供應範圍,並透過標籤和認證標準提高透明度。此外,餐飲服務業也擴大採用新鮮蔬菜來提升營養價值和整體食品品質。人們對食品安全、環境永續性和負責任的耕作方式的日益關注,進一步推動了市場的長期成長。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 市場機遇

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 按類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利趨勢

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲(MEA)

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依蔬菜類型分類,2022-2035年

- 綠葉蔬菜

- 萵苣

- 菠菜

- 羽衣甘藍

- 瑞士甜菜

- 其他

- 十字花科蔬菜

- 綠色花椰菜

- 花椰菜

- 高麗菜

- 抱子甘藍

- 其他

- 根莖類

- 紅蘿蔔

- 馬鈴薯

- 甜菜

- 蘿蔔

- 其他

- 洋蔥和韭菜

- 洋蔥

- 蒜

- 青蔥

- 蔥

- 其他

- 茄科蔬菜

- 番茄

- 青椒

- 茄子

- 其他

- 豆子

- 豌豆

- 豆子

- 扁豆

- 其他

- 葫蘆科蔬菜

- 黃瓜

- 西葫蘆

- 南瓜

- 瓜

- 其他

- 其他

- 玉米

- 蘆筍

- 朝鮮薊

- 其他

第6章 市場估算與預測:依最終用途分類,2022-2035年

- 家庭消費

- 食品加工

- 食品服務業

- 其他用途

第7章 市場估價與預測:依通路分類,2022-2035年

- 零售店

- 線上零售

- 農夫市集

- 專賣店

- 食品服務業

- 批發市場

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第9章:公司簡介

- Baloian Farms

- Bonduelle Group

- BrightFarms

- Church Brothers Farms

- Dole Fresh Vegetables

- Earthbound Farm

- Fresh Del Monte Produce

- Grimmway Farms

- Lipman Family Farms

- Mann Packing Company

- Mastronardi Produce(SUNSET Grown)

- Ocean Mist Farms

- SunFed

- Tanimura &Antle

- Taylor Farms

The Global Fresh Vegetable Market was valued at USD 1 trillion in 2025 and is estimated to grow at a CAGR of 4.9% to reach USD 1.6 trillion by 2035.

Rising consumer preference for healthier food options, increasing sustainability awareness, and advancements in agricultural technology are fueling market expansion. There is an increasing demand as many people focus on nutrient-rich diets and seek out fresher, chemical-free options. Sustainable farming practices and eco-conscious purchasing habits are driving shifts in production and distribution. Enhanced supply chain efficiency, supported by technological improvements in farming techniques and storage solutions, ensures year-round availability.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1 Trillion |

| Forecast Value | $1.6 Trillion |

| CAGR | 4.9% |

Segmented by application, the market includes household consumption, food processing, food service, and others. Household consumption remains dominant, contributing 60.4% of total demand as consumers prioritize fresh, whole foods in their daily meals. Increased awareness of nutritional benefits, combined with marketing campaigns promoting fresh produce, is influencing purchasing patterns. The ongoing shift toward plant-based eating habits reinforces this growth, as more consumers opt for minimally processed foods with high nutrient content.

The retail stores segment held a 57.9% share and is projected to grow at a CAGR of 4.9% through 2035. Distribution channels are evolving quickly as consumers increasingly prioritize easy access, transparent product information, and consistent quality standards. Conventional retail formats such as supermarkets and hypermarkets continue to play a central role by offering a wide assortment of products, competitive pricing, and a comprehensive shopping experience under one roof. At the same time, online retailing has expanded significantly, supported by the shift toward digital purchasing behavior, especially following the pandemic, along with growing preference for doorstep delivery and targeted digital promotions. E-commerce platforms also enable access to organic and specialty vegetables while providing detailed product insights, allowing companies to reach broader consumer segments. In parallel, farmers markets are gaining popularity among health-conscious consumers who value fresh, locally sourced produce and transparent farming practices, while also supporting regional agricultural economies.

North America Fresh Vegetable Market accounted for 13.8% share in 2025. Demand in the region is strongly influenced by the growing preference for organically produced vegetables sourced through sustainable and local farming practices. Consumers in both the United States and Canada are increasingly shifting toward healthier diets, including plant-based food choices. Distribution networks such as supermarkets, retail outlets, and online platforms are ensuring wider product availability while improving transparency through labeling and certification standards. Additionally, the foodservice sector is increasingly incorporating fresh vegetables to enhance nutritional value and overall food quality. Rising awareness regarding food safety, environmental sustainability, and responsible agricultural practices is further supporting long-term market growth.

Major companies operating in the Global Fresh Vegetable Market include Fresh Del Monte Produce, Taylor Farms, Dole Fresh Vegetables, Bonduelle Group, Grimmway Farms, BrightFarms, Earthbound Farm, Tanimura & Antle, Mann Packing Company, Mastronardi Produce (SUNSET Grown), Church Brothers Farms, Baloian Farms, Ocean Mist Farms, Lipman Family Farms, and SunFed. Key strategies to strengthen growth in the fresh vegetable market include expanding contract farming and direct sourcing partnerships to ensure consistent supply and quality control. Companies are investing in cold chain logistics and advanced storage systems to reduce post-harvest losses and maintain freshness across long distribution routes. Strengthening organic certification and transparent labeling practices is helping build consumer trust and brand loyalty. Market players are also focusing on digital transformation through e-commerce platforms and mobile applications to improve accessibility and customer engagement. Product diversification, including ready-to-eat and pre-cut vegetable offerings, is supporting convenience-driven demand. Additionally, investments in sustainable farming techniques and water-efficient cultivation methods are enhancing long-term productivity while aligning with environmental expectations.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vegetable type

- 2.2.3 End use

- 2.2.4 Distribution channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Vegetable Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Leafy Greens

- 5.2.1 Lettuce

- 5.2.2 Spinach

- 5.2.3 Kale

- 5.2.4 Swiss Chard

- 5.2.5 Others

- 5.3 Cruciferous Vegetables

- 5.3.1 Broccoli

- 5.3.2 Cauliflower

- 5.3.3 Cabbage

- 5.3.4 Brussels Sprouts

- 5.3.5 Others

- 5.4 Root Vegetables

- 5.4.1 Carrots

- 5.4.2 Potatoes

- 5.4.3 Beets

- 5.4.4 Radishes

- 5.4.5 Others

- 5.5 Allium Vegetables

- 5.5.1 Onions

- 5.5.2 Garlic

- 5.5.3 Leeks

- 5.5.4 Shallots

- 5.5.5 Others

- 5.6 Solanaceous Vegetables

- 5.6.1 Tomatoes

- 5.6.2 Peppers

- 5.6.3 Eggplants

- 5.6.4 Others

- 5.7 Legumes

- 5.7.1 Peas

- 5.7.2 Beans

- 5.7.3 Lentils

- 5.7.4 Others

- 5.8 Cucurbitaceous Vegetables

- 5.8.1 Cucumbers

- 5.8.2 Zucchinis

- 5.8.3 Pumpkins

- 5.8.4 Melons

- 5.8.5 Others

- 5.9 Other

- 5.9.1 Corn

- 5.9.2 Asparagus

- 5.9.3 Artichokes

- 5.9.4 Others

Chapter 6 Market Estimates and Forecast, By End Use, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Household consumption

- 6.3 Food processing

- 6.4 Foodservice

- 6.5 Other end-uses

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Retail stores

- 7.3 Online retailing

- 7.4 Farmers' markets

- 7.5 Specialty stores

- 7.6 Foodservice providers

- 7.7 Wholesale markets

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Baloian Farms

- 9.2 Bonduelle Group

- 9.3 BrightFarms

- 9.4 Church Brothers Farms

- 9.5 Dole Fresh Vegetables

- 9.6 Earthbound Farm

- 9.7 Fresh Del Monte Produce

- 9.8 Grimmway Farms

- 9.9 Lipman Family Farms

- 9.10 Mann Packing Company

- 9.11 Mastronardi Produce (SUNSET Grown)

- 9.12 Ocean Mist Farms

- 9.13 SunFed

- 9.14 Tanimura & Antle

- 9.15 Taylor Farms

2034年農業低溫運輸市場預測-按解決方案類型、組件、技術、應用、最終用戶和地區分類的全球分析從農場到餐桌市場預測至2034年-全球分析(按產品、來源、經營模式、餐廳類型、菜系類型、服務類型、最終用戶和地區分類)微型農業市場預測至2034年—全球耕作方式、農場類型、生長介質、生長環境、作物類型、技術、應用、最終用戶和區域分析

2034年農業低溫運輸市場預測-按解決方案類型、組件、技術、應用、最終用戶和地區分類的全球分析從農場到餐桌市場預測至2034年-全球分析(按產品、來源、經營模式、餐廳類型、菜系類型、服務類型、最終用戶和地區分類)微型農業市場預測至2034年—全球耕作方式、農場類型、生長介質、生長環境、作物類型、技術、應用、最終用戶和區域分析 新鮮蔬菜市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年

新鮮蔬菜市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年 生鮮食品市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、通路、地區及競爭格局分類,2021-2031年)

生鮮食品市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、通路、地區及競爭格局分類,2021-2031年) 新鮮水果和蔬菜市場規模、佔有率和成長分析(按類型、類別、品質、水果類型、蔬菜類型、通路、最終用戶、包裝和地區分類)—2026-2033年產業預測

新鮮水果和蔬菜市場規模、佔有率和成長分析(按類型、類別、品質、水果類型、蔬菜類型、通路、最終用戶、包裝和地區分類)—2026-2033年產業預測 新鮮水果市場規模、佔有率及成長分析(按產品類型、通路、新鮮度、天然狀態、包裝類型和地區分類)-產業預測(2026-2033年)

新鮮水果市場規模、佔有率及成長分析(按產品類型、通路、新鮮度、天然狀態、包裝類型和地區分類)-產業預測(2026-2033年) 新鮮蔬菜市場規模、佔有率及成長分析(按產品、通路、最終用途、種植方法及地區分類)-2026-2033年產業預測新鮮水果和蔬菜市場-全球產業規模、佔有率、趨勢、機會和預測,按產品、性質、最終用戶、地區和競爭細分,2020-2030 年

新鮮蔬菜市場規模、佔有率及成長分析(按產品、通路、最終用途、種植方法及地區分類)-2026-2033年產業預測新鮮水果和蔬菜市場-全球產業規模、佔有率、趨勢、機會和預測,按產品、性質、最終用戶、地區和競爭細分,2020-2030 年 全球有機生鮮食品市場

全球有機生鮮食品市場