|

市場調查報告書

商品編碼

1876653

清真認證蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Halal-Certified Protein Hydrolysates Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

2024 年全球清真認證蛋白質水解物市場價值為 8 億美元,預計到 2034 年將以 5.6% 的複合年成長率成長至 14 億美元。

由於健康意識的提高和對清潔標籤、功能性成分需求的成長,市場正在蓬勃發展。消費者越來越關注蛋白質消化率、肌肉恢復和腸道健康,這推動了運動營養、膳食補充劑和臨床營養領域的成長。酶水解技術的進步透過提高製程效率和產品品質重塑了市場格局。現代酵素法系統能夠實現對胜肽的精確分解,從而生產出生物利用度更高、異味更少的水解物。全球食品配料生產商正在調整其酶水解工藝,以滿足清真認證的要求,從而實現精準營養和更清潔的生產。清真認證水解物在嬰幼兒營養和臨床營養領域的應用日益廣泛,因為它們可以降低致敏性並提高營養吸收率,這也推動了市場對這類產品的接受度。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 8億美元 |

| 預測值 | 14億美元 |

| 複合年成長率 | 5.6% |

由於消費者對永續、符合倫理且不含過敏原的蛋白質來源的需求日益成長,預計到2024年,植物蛋白水解物的市場規模將達到3.6億美元。乳糖不耐症、素食主義和環保意識的提升促使生產商用大豆、豌豆和米水解物取代動物性蛋白質。植物蛋白水解物易於獲得清真認證、原料供應充足且生產流程簡單,使其成為飲料、功能性食品和運動營養品領域的理想選擇。

2024年,酶水解市場規模預計將達到4.816億美元,這主要歸功於其特異性以及在不損害營養完整性的前提下生產高品質、具有生物活性的蛋白質水解物的能力。此方法使生產商能夠控制肽鏈的長度和組成,從而提高膳食補充劑、臨床食品和運動營養品的消化率和功能性。此外,由於酵素水解無需使用化學催化劑,因此符合清真標準,適用於清真認證的生產線。

預計到2024年,北美清真認證蛋白水解物市場規模將達到1.2億美元,佔全球市佔率的15%。其中,美國貢獻了1.008億美元,這主要得益於其成熟的食品加工業、消費者對功能性和清潔標籤成分的高需求以及不斷成長的穆斯林人口。此外,注重健身的消費者對清真認證營養補充品的認知度不斷提高,也是推動該地區市場成長的重要因素。

全球清真認證蛋白水解物市場的主要參與者包括Arla Foods Ingredients、ADM(Archer Daniels Midland)、嘉吉公司、Actus Nutrition、恆天然合作集團、格蘭比亞公司、菲仕蘭公司、雅培公司、羅蓋特公司、帝斯曼-菲美意公司、凱瑞集團和Agropur合作社。為了鞏固市場地位,清真認證蛋白水解物領域的企業正致力於研發,以提高酵素解效率、胜肽生物利用度和清潔標籤配方。與食品製造商、營養品牌和臨床營養供應商的策略合作有助於拓展分銷網路。此外,各公司還在清真認證流程、區域生產設施和原料採購方面進行投資,以確保合規性和規模化生產。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 健康意識的提高和對清潔標籤產品的需求

- 酶水解技術進步

- 在嬰幼兒及臨床營養領域的應用不斷拓展

- 產業陷阱與挑戰

- 生產成本上升和價格溢價

- 清真認證原料供應有限

- 市場機遇

- 植物蛋白水解物生長潛力

- 數位溯源與區塊鏈整合

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 產品

- 未來市場趨勢

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 專利格局

- 貿易統計(HS編碼)(註:僅提供重點國家的貿易統計資料)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依來源類型分類,2021-2034年

- 主要趨勢

- 植物性蛋白質水解物

- 豌豆蛋白水解物

- 大豆蛋白水解物

- 米蛋白水解物

- 大麻蛋白水解物

- 其他植物來源

- 動物性蛋白質水解物

- 乳清蛋白水解物

- 酪蛋白水解物

- 牛蛋白水解物

- 禽肉蛋白質水解物

- 海洋蛋白水解物

- 魚蛋白水解物

- 蝦子和甲殼類水解物

- 其他海洋來源

- 微生物蛋白水解物

第6章:市場估算與預測:依加工技術分類,2021-2034年

- 主要趨勢

- 酵素水解

- 微生物酵素系統

- 植物來源的酵素系統

- 固定化酵素技術

- 酸水解

- 鹼性水解

- 其他

第7章:市場估計與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 嬰兒營養

- 深度水解配方

- 部分水解配方

- 低過敏性產品

- 運動營養

- 運動前補充劑

- 運動後恢復產品

- 蛋白質粉和蛋白質奶昔

- 臨床/醫學營養

- 腸內營養產品

- 醫用食品

- 專業膳食管理

- 膳食補充品和營養保健品

- 膠囊和片劑

- 粉狀補充劑

- 功能性食品

- 食品飲料原料

- 增味劑

- 蛋白質強化

- 乳化劑和穩定劑

- 化妝品及個人護理

- 抗衰老產品

- 護髮產品

- 護膚應用

第8章:市場估算與預測:依最終用途產業分類,2021-2034年

- 主要趨勢

- 食品飲料製造商

- 製藥

- 營養保健品和膳食補充品生產商

- 化妝品及個人護理

- 動物飼料和寵物食品

第9章:市場估計與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第10章:公司簡介

- Arla Foods Ingredients

- Fonterra Co-operative Group

- Cargill Incorporated

- Kerry Group

- DSM-Firmenich

- ADM (Archer Daniels Midland)

- Actus Nutrition

- FrieslandCampina

- Agropur Cooperative

- Roquette Freres

- Abbott Laboratories

- Glanbia PLC

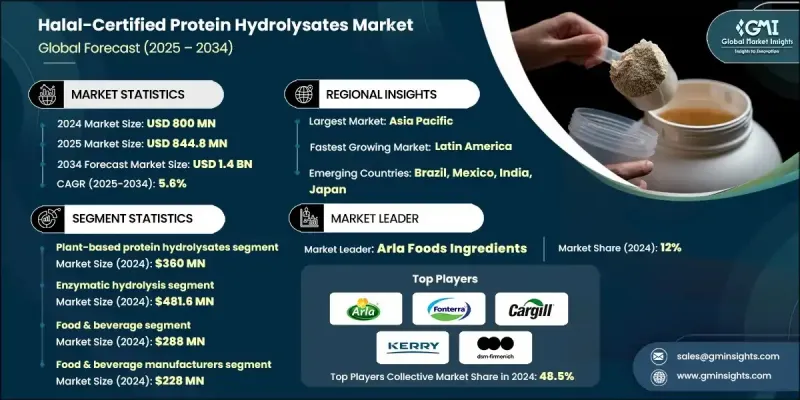

The Global Halal-Certified Protein Hydrolysates Market was valued at USD 800 million in 2024 and is estimated to grow at a CAGR of 5.6% to reach USD 1.4 billion by 2034.

The market is witnessing expansion due to rising health awareness and the increasing demand for clean-label, functional ingredients. Consumers are becoming more conscious of protein digestibility, muscle recovery, and gut health, which is fueling growth across sports nutrition, dietary supplements, and clinical nutrition sectors. Advances in enzymatic hydrolysis are reshaping the market by enhancing process efficiency and product quality. Modern enzyme-based systems allow controlled peptide breakdown, producing hydrolysates with higher bioavailability and reduced off-flavors. Global food ingredient manufacturers are adapting their enzymatic hydrolysis processes to meet halal compliance, enabling precision nutrition and cleaner production. The growing use of halal-certified hydrolysates in infant and clinical nutrition, where they reduce allergenicity and improve nutrient absorption, is also driving market adoption.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $800 Million |

| Forecast Value | $1.4 Billion |

| CAGR | 5.6% |

The plant-based protein hydrolysates accounted for USD 360 million in 2024, owing to rising consumer preference for sustainable, ethical, and allergen-free protein sources. Lactose intolerance, veganism, and environmental awareness have encouraged manufacturers to replace animal-derived proteins with soy, pea, and rice hydrolysates. Their ease of halal certification, availability of raw materials, and simplified production processes make plant-based hydrolysates ideal for beverages, functional foods, and sports nutrition applications.

The enzymatic hydrolysis segment reached USD 481.6 million in 2024, attributed to its specificity and ability to produce high-quality, bioactive protein hydrolysates without compromising nutritional integrity. This method allows manufacturers to control peptide chain length and composition, improving digestibility and functionality for dietary supplements, clinical foods, and sports nutrition. Additionally, enzymatic hydrolysis aligns with halal standards since it avoids chemical catalysts, making it suitable for halal-certified production lines.

North America Halal-Certified Protein Hydrolysates Market captured USD 120 million in 2024, representing 15% share. The U.S. contributed USD 100.8 million due to its mature food processing industry, high consumer demand for functional and clean-label ingredients, and growing Muslim population. Increasing awareness of halal-certified nutritional supplements among fitness-focused consumers is also driving market growth in the region.

Key players in the Global Halal-Certified Protein Hydrolysates Market include Arla Foods Ingredients, ADM (Archer Daniels Midland), Cargill Incorporated, Actus Nutrition, Fonterra Co-operative Group, Glanbia PLC, FrieslandCampina, Abbott Laboratories, Roquette Freres, DSM-Firmenich, Kerry Group, and Agropur Cooperative. To strengthen their presence, companies in the halal-certified protein hydrolysates sector are focusing on research and development to improve enzymatic hydrolysis efficiency, peptide bioavailability, and clean-label formulations. Strategic collaborations with food manufacturers, nutrition brands, and clinical nutrition providers help expand distribution networks. Firms are also investing in halal certification processes, regional production facilities, and raw material sourcing to ensure compliance and scalability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Source type

- 2.2.3 Processing Technology

- 2.2.4 Application

- 2.2.5 End Use Industry

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising health consciousness & clean label demand

- 3.2.1.2 Technological advancements in enzymatic hydrolysis

- 3.2.1.3 Expanding applications in infant & clinical nutrition

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Higher production costs & price premiums

- 3.2.2.2 Limited availability of halal-certified raw materials

- 3.2.3 Market opportunities

- 3.2.3.1 Plant-based protein hydrolysates growth potential

- 3.2.3.2 Digital traceability & blockchain integration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 Product

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Source Type, 2021 - 2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Plant-based protein hydrolysates

- 5.2.1 Pea protein hydrolysates

- 5.2.2 Soy protein hydrolysates

- 5.2.3 Rice protein hydrolysates

- 5.2.4 Hemp protein hydrolysates

- 5.2.5 Other plant sources

- 5.3 Animal-based protein hydrolysates

- 5.3.1 Whey protein hydrolysates

- 5.3.2 Casein hydrolysates

- 5.3.3 Bovine protein hydrolysates

- 5.3.4 Poultry protein hydrolysates

- 5.4 Marine protein hydrolysates

- 5.4.1 Fish protein hydrolysates

- 5.4.2 Shrimp & crustacean hydrolysates

- 5.4.3 Other marine sources

- 5.5 Microbial protein hydrolysates

Chapter 6 Market Estimates and Forecast, By Processing Technology, 2021 - 2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Enzymatic hydrolysis

- 6.2.1 Microbial enzyme systems

- 6.2.2 Plant-derived enzyme systems

- 6.2.3 Immobilized enzyme technology

- 6.3 Acid hydrolysis

- 6.4 Alkaline hydrolysis

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Infant nutrition

- 7.2.1 Extensively hydrolyzed formulas

- 7.2.2 Partially hydrolyzed formulas

- 7.2.3 Hypoallergenic products

- 7.3 Sports nutrition

- 7.3.1 Pre-workout supplements

- 7.3.2 Post-workout recovery products

- 7.3.3 Protein powders & shakes

- 7.4 Clinical/medical nutrition

- 7.4.1 Enteral nutrition products

- 7.4.2 Medical foods

- 7.4.3 Specialized dietary management

- 7.5 Dietary supplements & nutraceuticals

- 7.5.1 Capsules & tablets

- 7.5.2 Powder supplements

- 7.5.3 Functional foods

- 7.6 Food & beverage ingredients

- 7.6.1 Flavor enhancers

- 7.6.2 Protein fortification

- 7.6.3 Emulsifiers & stabilizers

- 7.7 Cosmetics & personal care

- 7.7.1 Anti-aging products

- 7.7.2 Hair care products

- 7.7.3 Skin care applications

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Food & beverage manufacturers

- 8.3 Pharmaceuticals

- 8.4 Nutraceuticals & Dietary supplement producers

- 8.5 Cosmetics & personal care

- 8.6 Animal feed & pet food

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Arla Foods Ingredients

- 10.2 Fonterra Co-operative Group

- 10.3 Cargill Incorporated

- 10.4 Kerry Group

- 10.5 DSM-Firmenich

- 10.6 ADM (Archer Daniels Midland)

- 10.7 Actus Nutrition

- 10.8 FrieslandCampina

- 10.9 Agropur Cooperative

- 10.10 Roquette Freres

- 10.11 Abbott Laboratories

- 10.12 Glanbia PLC

蛋白質水解物市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、來源、形態、製程、應用、地區和競爭格局分類,2020-2030年預測

蛋白質水解物市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、來源、形態、製程、應用、地區和競爭格局分類,2020-2030年預測 嬰兒配方奶粉蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)免疫調節蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)抗菌(酵素法)蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)植物蛋白水解物市場機會、成長動力、產業趨勢分析及2025-2034年預測海洋蛋白水解物市場機會、成長動力、產業趨勢分析及2025-2034年預測蛋白質水解物市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

嬰兒配方奶粉蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)免疫調節蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)抗菌(酵素法)蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)植物蛋白水解物市場機會、成長動力、產業趨勢分析及2025-2034年預測海洋蛋白水解物市場機會、成長動力、產業趨勢分析及2025-2034年預測蛋白質水解物市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 全球蛋白質水解物市場研究報告 - 產業分析、規模、佔有率、成長、趨勢及 2025 年至 2033 年預測抗菌(酵素)蛋白水解物市場機會、成長動力、產業趨勢分析與預測 2025 - 2034蛋白質水解物的全球市場

全球蛋白質水解物市場研究報告 - 產業分析、規模、佔有率、成長、趨勢及 2025 年至 2033 年預測抗菌(酵素)蛋白水解物市場機會、成長動力、產業趨勢分析與預測 2025 - 2034蛋白質水解物的全球市場