|

市場調查報告書

商品編碼

1822633

植物蛋白水解物市場機會、成長動力、產業趨勢分析及2025-2034年預測Plant Protein Hydrolysate Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

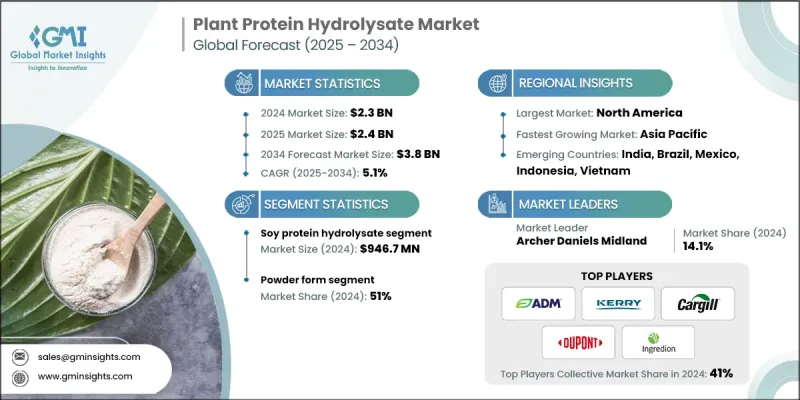

根據 Global Market Insights Inc. 發布的最新報告,全球植物蛋白水解物市場規模預計在 2024 年為 23 億美元,預計將從 2025 年的 24 億美元成長到 2034 年的 38 億美元,複合年成長率為 5.1%。

消費者日益轉向植物性飲食和清潔標籤產品,是植物蛋白水解物市場的主要驅動力。越來越多的人在選擇飲食時優先考慮健康、永續性和道德方面的考量,這導致對植物源性成分的需求激增。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 23億美元 |

| 預測值 | 38億美元 |

| 複合年成長率 | 5.1% |

大豆蛋白水解物的採用率不斷上升

2024年,大豆蛋白水解物市場佔據了顯著佔有率,這得益於大豆豐富的氨基酸成分和廣泛的可用性。作為一種用途廣泛且經濟高效的來源,大豆水解物廣泛應用於運動營養、嬰兒配方奶粉和功能性食品。其卓越的消化率和抗過敏特性使其在動物性替代品中佔據絕對優勢。市場參與者正在充分利用大豆蛋白的營養價值,同時投資於加工技術以減少苦味並提升風味,從而使大豆水解物對注重健康的消費者更具吸引力。

粉末獲得牽引力

2024年,粉狀產品佔據了相當大的市場佔有率,這得益於其便利性、更長的保存期限以及易於添加到各種食品和飲料產品中的優勢。粉末為製造商提供了靈活性,使其能夠配製從蛋白奶昔到烘焙食品的各種產品,而不會影響口感或營養成分。消費者也更青睞粉狀水解物,因為它們便於攜帶,並且在日常飲食中可以直接使用。各公司正致力於改善粉狀植物蛋白水解物的溶解度和口感,以拓寬其應用範圍,並提高全球消費者的接受度。

北美將成為推動力地區

到2034年,北美植物蛋白水解物市場將迎來強勁成長,這得益於消費者對植物性營養和健康趨勢的日益關注。製造商正利用與食品和飲料品牌的合作,創新並擴展符合北美口味和監管標準的產品組合。在研發方面的投資以及強調永續性和健康益處的行銷策略,正在進一步增強其在該地區的市場影響力。

植物蛋白水解物市場的主要參與者有 Ingredion Incorporated、杜邦、阿徹丹尼爾斯米德蘭公司 (ADM)、凱裡集團和嘉吉。

為了鞏固市場地位,植物蛋白水解物市場的企業正專注於產品創新,專注於改善風味和提高生物利用度。與食品製造商和營養品牌的策略合作,使其應用範圍更廣,市場滲透速度更快。擴大產能和採購永續原料有助於滿足日益成長的需求,同時契合消費者的價值觀。此外,企業也投資於教育行銷活動,以提高人們對植物蛋白水解物益處的認知,從而在競爭日益激烈的市場中推動其普及和客戶忠誠度。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 市場機會

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 價格趨勢

- 按地區

- 未來市場趨勢

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 專利格局

- 貿易統計資料(HS 編碼)(註:僅提供重點國家的貿易統計資料)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物的策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考慮

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場規模與預測:依來源,2021-2034

- 主要趨勢

- 大豆蛋白水解物

- 小麥蛋白水解物

- 豌豆蛋白水解物

- 米蛋白水解物

- 大麻蛋白水解物

- 葵花蛋白水解物

- 其他

第6章:市場規模及預測:依形式,2021-2034

- 主要趨勢

- 液體

- 粉末

第7章:市場規模與預測:按應用,2021-2034

- 主要趨勢

- 食品和飲料

- 營養補充品

- 動物飼料

- 其他

第 8 章:市場規模與預測:按地區,2021-2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第9章:公司簡介

- Archer Daniels Midland Company

- Kerry Group

- DuPont

- Ingredion Incorporated

- Cargill

- Evonik Industries

- Koninklijke DSM

- Glanbia

- Tate & Lyle

- Bunge Limited

- Roquette Freres

- Brenntag

- Associated British Foods

- Novozymes

- Givaudan

The global plant protein hydrolysate market was estimated at USD 2.3 billion in 2024 and is expected to grow from USD 2.4 billion in 2025 to USD 3.8 billion by 2034, at a CAGR of 5.1%, according to the latest report published by Global Market Insights Inc.

The increasing consumer shift toward plant-based diets and clean-label products is a major driver for the plant protein hydrolysate market. More people are prioritizing health, sustainability, and ethical considerations when choosing what to eat, leading to a surge in demand for plant-derived ingredients.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.3 Billion |

| Forecast Value | $3.8 Billion |

| CAGR | 5.1% |

Rising Adoption of Soy Protein Hydrolysate

The soy protein hydrolysate segment held a notable share in 2024, driven by soy's rich amino acid profile and widespread availability. As a versatile and cost-effective source, soy hydrolysates are extensively used in sports nutrition, infant formulas, and functional foods. Their superior digestibility and allergen-friendly nature position them well against animal-based alternatives. Market players are capitalizing on soy protein's nutritional benefits while investing in processing technologies to reduce bitterness and enhance flavor, making soy hydrolysates more appealing to health-conscious consumers.

Powder To Gain Traction

The powder form segment held a significant share in 2024, driven by its convenience, longer shelf life, and ease of incorporation into various food and beverage products. Powders provide manufacturers with the flexibility to formulate everything from protein shakes to bakery items without compromising texture or nutritional content. Consumers also prefer powdered hydrolysates for their portability and straightforward usage in daily diets. Companies are focusing on improving the solubility and taste profiles of powdered plant protein hydrolysates to broaden their application scope and increase consumer acceptance globally.

North America to Emerge as a Propelling Region

North America plant protein hydrolysate market will witness robust growth through 2034, fueled by increasing consumer awareness of plant-based nutrition and health trends. Manufacturers are leveraging partnerships with food and beverage brands to innovate and expand product portfolios tailored to North American tastes and regulatory standards. Investments in R&D and marketing strategies emphasizing sustainability and health benefits are further strengthening the market presence across the region.

Major players involved in the plant protein hydrolysate market are Ingredion Incorporated, DuPont, Archer Daniels Midland Company (ADM), Kerry Group, and Cargill.

To solidify their market foothold, companies in the plant protein hydrolysate market are emphasizing product innovation, focusing on flavor improvement and enhanced bioavailability. Strategic collaborations with food manufacturers and nutrition brands enable wider application and faster market penetration. Expanding production capacities and sourcing sustainable raw materials help meet rising demand while aligning with consumer values. Additionally, companies invest in educational marketing campaigns to raise awareness about the benefits of plant protein hydrolysates, thereby driving adoption and customer loyalty in an increasingly competitive landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Source

- 2.2.2 Form

- 2.2.3 Application

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Size and Forecast, By Source, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Soy protein hydrolysate

- 5.3 Wheat protein hydrolysate

- 5.4 Pea protein hydrolysate

- 5.5 Rice protein hydrolysate

- 5.6 Hemp protein hydrolysate

- 5.7 Sunflower protein hydrolysate

- 5.8 Others

Chapter 6 Market Size and Forecast, By Form, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Liquid

- 6.3 Powder

Chapter 7 Market Size and Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Food & beverages

- 7.3 Nutritional supplements

- 7.4 Animal feed

- 7.5 Others

Chapter 8 Market Size and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East & Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

- 8.6.4 Rest of Middle East & Africa

Chapter 9 Company Profiles

- 9.1 Archer Daniels Midland Company

- 9.2 Kerry Group

- 9.3 DuPont

- 9.4 Ingredion Incorporated

- 9.5 Cargill

- 9.6 Evonik Industries

- 9.7 Koninklijke DSM

- 9.8 Glanbia

- 9.9 Tate & Lyle

- 9.10 Bunge Limited

- 9.11 Roquette Freres

- 9.12 Brenntag

- 9.13 Associated British Foods

- 9.14 Novozymes

- 9.15 Givaudan

蛋白質水解物市場規模、佔有率及成長分析(依產品類型、形態類型、應用類型及地區分類)-2026-2033年產業預測

蛋白質水解物市場規模、佔有率及成長分析(依產品類型、形態類型、應用類型及地區分類)-2026-2033年產業預測 全球蛋白質水解物市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球蛋白質水解物市場規模、佔有率、趨勢和成長分析報告(2026-2034) 有機蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)單細胞蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)精準發酵法製備蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)老年營養蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)下一代蛋白質水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034)

有機蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)單細胞蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)精準發酵法製備蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)老年營養蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)下一代蛋白質水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034) 蛋白質水解物市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、來源、形態、製程、應用、地區和競爭格局分類,2020-2030年預測非基因改造蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)食品廢棄物衍生蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)

蛋白質水解物市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、來源、形態、製程、應用、地區和競爭格局分類,2020-2030年預測非基因改造蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)食品廢棄物衍生蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)