|

市場調查報告書

商品編碼

1876643

抗菌(酵素法)蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Antimicrobial (Enzymatic) Protein Hydrolysates Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

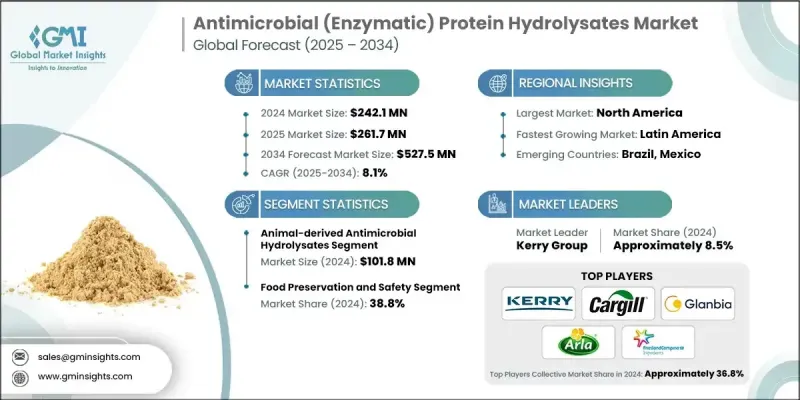

2024 年全球抗菌(酵素法)蛋白水解物市值為 2.421 億美元,預計到 2034 年將以 8.1% 的複合年成長率成長至 5.275 億美元。

隨著食品生產商和消費者轉向符合「清潔標籤」理念的天然保鮮方案,市場動能日益強勁。酵素改質水解物因其有助於保持產品新鮮度且不損害營養完整性,正擴大被選為合成防腐劑的替代品。全球對抗生素抗藥性的日益關注也推動了這一趨勢,促使人們更加需要不會導致抗生素濫用的抗菌工具。這些水解物在食品和健康相關應用中能夠有效控制微生物,使其完美契合不斷變化的監管和安全要求。人們對健康和保健的日益關注也推動了市場需求,因為如今的消費者尋求兼具功能性和生物活性的成分,使其用途超越了基本的保鮮功能。隨著業界重心轉向能夠提升產品安全性和品質的天然來源解決方案,抗菌蛋白水解物有望在食品、營養及相關領域中廣泛應用。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 2.421億美元 |

| 預測值 | 5.275億美元 |

| 複合年成長率 | 8.1% |

2024年,動物源抗菌水解物市場規模達1.018億美元,預計2025年至2034年將以7.8%的複合年成長率成長。由於其強大的胜肽活性和良好的監管認可,這類產品在食品保鮮、臨床營養和膳食補充劑配方中的應用持續成長。這些水解物通常由牛奶、肉類或雞蛋等蛋白質來源製成,因其抗菌潛力而備受青睞,尤其適用於需要兼顧安全性和增強生物活性的高蛋白即食產品。

2024年,食品保鮮和安全應用領域創造了9,370萬美元的市場規模,預計到2034年將以7.4%的複合年成長率成長。該領域主要利用蛋白質水解物來抑制乳製品、加工食品、飲料和簡便食品中的微生物生長。由於製造商用天然來源的胜肽替代品取代了合成防腐劑,因此蛋白質水解物的使用符合清潔標籤的要求,有助於延長保存期限並保持成分清單的透明度。

2024年,北美抗菌(酵素法)蛋白水解物市場規模達8,470萬美元。由於消費者日益重視清潔標籤的食品保鮮理念和嚴格的食品安全合規要求,該地區對酵素法蛋白水解物的應用正在不斷成長。該地區擁有眾多功能性食品和營養保健品生產商,這有利於兼具抗菌和營養特性的生物活性胜肽的廣泛應用。減少化學防腐劑使用的監管壓力也促使食品公司採用酶法蛋白水解物,同時,對生物技術和蛋白質加工的投資不斷提升產品質量,提高成分分析的準確性,並增強食品和醫療保健行業的規模化生產能力。

參與抗菌(酵素法)蛋白水解物市場的主要公司包括嘉吉公司、格蘭比亞公司、菲仕蘭配料公司、阿拉食品配料公司、凱瑞集團等。這些公司正致力於透過多種策略來鞏固其市場地位。許多公司正加大對先進酵素法加工技術的投資,以提高胜肽的純度、效力和穩定性。各公司正拓展與食品製造商、營養保健品品牌和生技合作夥伴的合作,以加速跨多個領域的應用開發。提供清潔標籤配方支援、客製化抗菌解決方案和增強功能特性仍然是其核心優先事項。此外,各公司也正在增加研發投入,以尋找具有卓越抗菌性能的新型生物活性胜肽。擴大生產規模、改善監管合規性以及加強全球分銷網路有助於提升競爭力。

目錄

第1章:方法論

- 市場範圍和定義

- 研究設計

- 研究方法

- 資料收集方法

- 資料探勘來源

- 全球的

- 地區/國家

- 基準估算和計算

- 基準年計算

- 市場估算的關鍵趨勢

- 初步研究和驗證

- 原始資料

- 預測模型

- 研究假設和局限性

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 天然食品防腐劑需求不斷成長

- 日益嚴重的抗生素抗藥性問題

- 提高健康和保健意識

- 在功能性食品領域不斷拓展的應用

- 產業陷阱與挑戰

- 高昂的生產和加工成本

- 監理複雜性和核准挑戰

- 保存期限有限和穩定性問題

- 市場機遇

- 乳製品廢水資源化利用

- 人工智慧驅動的胜肽發現

- 化妝品領域的新興應用

- 植物性蛋白質來源的擴張

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 依產品

- 未來市場趨勢

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 專利格局

- 貿易統計(註:僅提供重點國家的貿易統計)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依產品類型分類,2021-2034年

- 主要趨勢

- 動物源性抗菌水解物

- 乳蛋白水解物

- 乳清蛋白水解物

- 酪蛋白水解物

- 魚蛋白水解物

- 肉類蛋白水解物

- 蛋清蛋白水解物

- 植物源抗菌水解物

- 大豆蛋白水解物

- 小麥蛋白水解物

- 豆類蛋白質水解物

- 穀物蛋白水解物

- 種子蛋白質水解物

- 海洋來源的抗菌水解物

- 魚類副產品水解物

- 藻類蛋白水解物

- 海藻蛋白水解物

- 甲殼類動物殼水解物

- 微生物來源的抗菌水解物

- 細菌發酵產物

- 真菌水解物

- 酵母衍生胜肽

第6章:市場估算與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 食品保藏與安全

- 天然防腐劑

- 抗菌塗層

- 活性包裝解決方案

- 延長保存期限

- 營養補充品

- 運動營養

- 臨床營養

- 嬰兒配方奶粉

- 膳食補充劑

- 功能性食品

- 動物飼料和寵物食品

- 生長促進劑

- 抗生素替代品

- 消化系統健康支持

- 增強免疫系統

- 醫藥和醫療保健

- 治療性胜肽

- 傷口護理產品

- 口腔護理應用

- 局部抗菌劑

- 化妝品和個人護理

- 抗菌製劑

- 保養品

- 護髮應用

- 抗衰老解決方案

第7章:市場估計與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第8章:公司簡介

- Kerry Group

- Cargill Inc.

- Glanbia plc

- Arla Foods Ingredients

- FrieslandCampina Ingredients

- DSM-Firmenich

- ADM (Archer Daniels Midland)

- AMCO Proteins

- Kemin Industries

- Titan Biotech

- BRF Ingredients

- Constantino & C Spa

- Crescent Biotech

- Aker Biomarine

- Biomega Group

- Essentia Protein Solutions

The Global Antimicrobial (Enzymatic) Protein Hydrolysates Market was valued at USD 242.1 million in 2024 and is estimated to grow at a CAGR of 8.1% to reach USD 527.5 million by 2034.

Market momentum is growing as food manufacturers and consumers shift toward natural preservation solutions that align with clean-label expectations. Enzyme-modified hydrolysates are being chosen more frequently as alternatives to synthetic preservatives because they help maintain product freshness without compromising nutritional integrity. This trend is supported by rising global concern surrounding antibiotic resistance, which has elevated the need for antimicrobial tools that do not contribute to antibiotic overuse. These hydrolysates provide effective microbial control in food and health-related applications, making them a strong fit for evolving regulatory and safety requirements. Increasing interest in health and wellness is also boosting demand, as today's consumers seek ingredients that offer both functional and bioactive benefits, expanding their relevance beyond basic preservation. With industry emphasis shifting toward naturally derived solutions that enhance product safety and quality, antimicrobial protein hydrolysates are poised for strong adoption across food, nutrition, and allied sectors.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $242.1 Million |

| Forecast Value | $527.5 Million |

| CAGR | 8.1% |

The animal-derived antimicrobial hydrolysates segment was valued at USD 101.8 million in 2024 and is expected to grow at a 7.8% CAGR from 2025 to 2034. Their uptake continues to increase across food preservation, clinical nutrition, and supplement formulations due to strong peptide activity and favorable regulatory acceptance. These hydrolysates are commonly produced from protein sources such as milk, meat, or eggs and are valued for their antimicrobial potential in high-protein and ready-to-eat products requiring both safety and enhanced bioactivity.

The food preservation and safety application segment generated USD 93.7 million in 2024 and will grow at a 7.4% CAGR through 2034. This segment relies on protein hydrolysates to help inhibit microbial growth in dairy items, processed foods, beverages, and convenience meals. Their use supports clean-label requirements as manufacturers replace synthetic preservatives with naturally sourced peptide-based alternatives that help extend shelf life and maintain transparency in ingredient listings.

North America Antimicrobial (Enzymatic) Protein Hydrolysates Market generated USD 84.7 million in 2024. Adoption is increasing in the region due to heightened emphasis on clean-label preservation and strict food safety compliance. The area benefits from a strong presence of functional food and nutraceutical producers, supporting expanded use of bioactive peptides that offer combined antimicrobial and nutritional properties. Regulatory pressure to reduce chemical preservative use is also prompting food companies to incorporate enzymatic hydrolysates, while investments in biotechnology and protein processing continue to refine product quality, improve profiling accuracy, and enhance scalability across food and healthcare industries.

Major companies participating in the Antimicrobial (Enzymatic) Protein Hydrolysates Market include Cargill Inc., Glanbia plc, FrieslandCampina Ingredients, Arla Foods Ingredients, Kerry Group, and others. Companies in the Antimicrobial (Enzymatic) Protein Hydrolysates Market are focusing on several strategies to strengthen their presence. Many are channeling investments into advanced enzymatic processing technologies to improve peptide purity, potency, and consistency. Firms are expanding collaborations with food manufacturers, nutraceutical brands, and biotechnology partners to accelerate application development across multiple sectors. Emphasis on clean-label formulation support, tailored antimicrobial solutions, and enhanced functional profiles remains a core priority. Companies are also increasing R&D spending to identify novel bioactive peptides with superior antimicrobial properties. Scaling production capabilities, improving regulatory alignment, and enhancing global distribution networks help reinforce competitiveness.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for natural food preservatives

- 3.2.1.2 Growing antibiotic resistance concerns

- 3.2.1.3 Increasing health and wellness awareness

- 3.2.1.4 Expanding applications in functional foods

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production and processing costs

- 3.2.2.2 Regulatory complexity and approval challenges

- 3.2.2.3 Limited shelf life and stability issues

- 3.2.3 Market opportunities

- 3.2.3.1 Dairy wastewater valorization

- 3.2.3.2 AI-driven peptide discovery

- 3.2.3.3 Emerging applications in cosmetics

- 3.2.3.4 Plant-based protein sources expansion

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Million, Kilo Tons)

- 5.1 Key trends

- 5.2 Animal-derived antimicrobial hydrolysates

- 5.2.1 Milk protein hydrolysates

- 5.2.2 Whey protein hydrolysates

- 5.2.3 Casein hydrolysates

- 5.2.4 Fish protein hydrolysates

- 5.2.5 Meat protein hydrolysates

- 5.2.6 Egg protein hydrolysates

- 5.3 Plant-derived antimicrobial hydrolysates

- 5.3.1 Soy protein hydrolysates

- 5.3.2 Wheat protein hydrolysates

- 5.3.3 Legume protein hydrolysates

- 5.3.4 Cereal protein hydrolysates

- 5.3.5 Seed protein hydrolysates

- 5.4 Marine-derived antimicrobial hydrolysates

- 5.4.1 Fish by-product hydrolysates

- 5.4.2 Algae protein hydrolysates

- 5.4.3 Seaweed protein hydrolysates

- 5.4.4 Crustacean shell hydrolysates

- 5.5 Microbial-derived antimicrobial hydrolysates

- 5.5.1 Bacterial fermentation products

- 5.5.2 Fungal hydrolysates

- 5.5.3 Yeast-derived peptides

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million, Kilo Tons)

- 6.1 Key trends

- 6.2 Food preservation and safety

- 6.2.1 Natural preservatives

- 6.2.2 Antimicrobial coatings

- 6.2.3 Active packaging solutions

- 6.2.4 Shelf-life extension

- 6.3 Nutritional supplements

- 6.3.1 Sports nutrition

- 6.3.2 Clinical nutrition

- 6.3.3 Infant formula

- 6.3.4 Dietary supplements

- 6.3.5 Functional foods

- 6.4 Animal feed and pet food

- 6.4.1 Growth promoters

- 6.4.2 Antibiotic alternatives

- 6.4.3 Digestive health support

- 6.4.4 Immune system enhancement

- 6.5 Pharmaceutical and healthcare

- 6.5.1 Therapeutic peptides

- 6.5.2 Wound care products

- 6.5.3 Oral care applications

- 6.5.4 Topical antimicrobials

- 6.6 Cosmetics and personal care

- 6.6.1 Antimicrobial formulations

- 6.6.2 Skin care products

- 6.6.3 Hair care applications

- 6.6.4 Anti-aging solutions

Chapter 7 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million, Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.5.4 Rest of Latin America

- 7.6 Middle East & Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

- 7.6.4 Rest of Middle East & Africa

Chapter 8 Company Profiles

- 8.1 Kerry Group

- 8.2 Cargill Inc.

- 8.3 Glanbia plc

- 8.4 Arla Foods Ingredients

- 8.5 FrieslandCampina Ingredients

- 8.6 DSM-Firmenich

- 8.7 ADM (Archer Daniels Midland)

- 8.8 AMCO Proteins

- 8.9 Kemin Industries

- 8.10 Titan Biotech

- 8.11 BRF Ingredients

- 8.12 Constantino & C Spa

- 8.13 Crescent Biotech

- 8.14 Aker Biomarine

- 8.15 Biomega Group

- 8.16 Essentia Protein Solutions

蛋白質水解物市場規模、佔有率及成長分析(依產品類型、形態類型、應用類型及地區分類)-2026-2033年產業預測

蛋白質水解物市場規模、佔有率及成長分析(依產品類型、形態類型、應用類型及地區分類)-2026-2033年產業預測 全球蛋白質水解物市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球蛋白質水解物市場規模、佔有率、趨勢和成長分析報告(2026-2034) 有機蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)單細胞蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)精準發酵法製備蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)老年營養蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)下一代蛋白質水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034)

有機蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)單細胞蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)精準發酵法製備蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)老年營養蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)下一代蛋白質水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034) 蛋白質水解物市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、來源、形態、製程、應用、地區和競爭格局分類,2020-2030年預測非基因改造蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)食品廢棄物衍生蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)

蛋白質水解物市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、來源、形態、製程、應用、地區和競爭格局分類,2020-2030年預測非基因改造蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)食品廢棄物衍生蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)