|

市場調查報告書

商品編碼

1773330

眼鏡包裝市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Eyewear Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

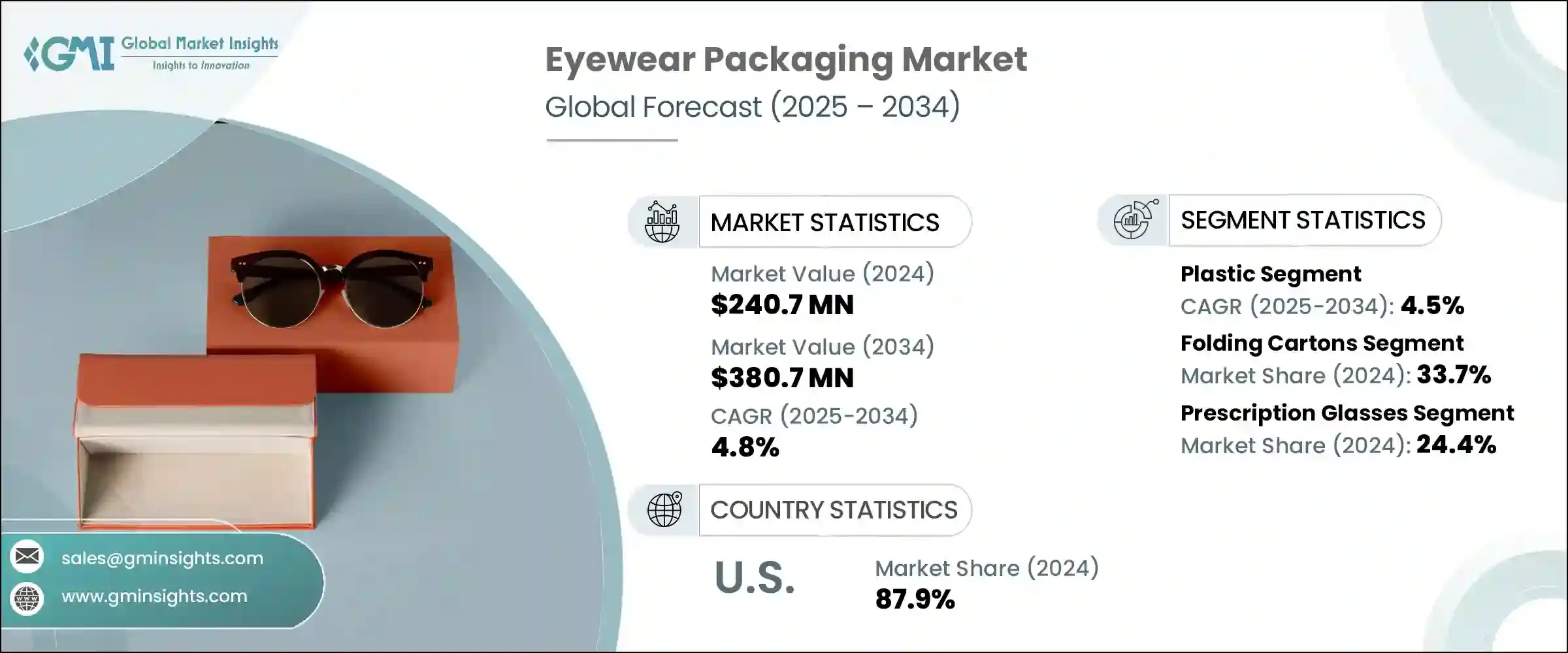

2024 年全球眼鏡包裝市場價值為 2.407 億美元,預計到 2034 年將以 4.8% 的複合年成長率成長至 3.807 億美元。這一成長主要得益於對時尚眼鏡和處方眼鏡需求的不斷成長,以及電子商務作為主要銷售管道的迅速崛起。由於螢幕使用率的提高、視力矯正需求以及眼鏡逐漸成為時尚配件等因素,越來越多的人群依賴眼鏡。因此,對能夠體現品牌形象、提升產品外觀並保護高階產品的高品質包裝的需求顯著成長。各品牌正專注於將視覺吸引力與結構完整性相結合的包裝,以滿足這些不斷變化的期望,並在競爭激烈的市場環境中鞏固客戶忠誠度。

線上零售日益佔據主導地位,重塑了眼鏡產品的銷售方式,對耐用且外觀精美的包裝的需求也隨之增加。如今,在直銷通路中,保護性、以品牌為中心的設計對於減少產品損壞和提升開箱體驗至關重要。此外,消費者對環保解決方案的偏好也日益成長,這推動了包裝向可回收和永續材料的轉變。極簡主義美學與負責任採購材料的整合反映了全球消費者偏好和合規要求的變化。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 2.407億美元 |

| 預測值 | 3.807億美元 |

| 複合年成長率 | 4.8% |

預計到2034年,紙和紙板市場規模將達到1.043億美元。隨著可回收性、輕量化和永續採購成為人們優先考慮的因素,紙質包裝正日益受到歡迎。這些材料廣泛用於外包裝和店內展示,幫助品牌迎合日益成長的環保意識消費者群體。越來越多的企業採用FSC認證的紙板和簡潔的設計,在增強環保責任感的同時,保持產品的外觀吸引力。

2024年,折疊紙盒在眼鏡包裝市場的佔有率為33.7%。折疊紙盒以其經濟高效和用途廣泛而聞名,在零售和線上管道仍然是首選的二次包裝。這些紙盒提供了充足的品牌展示空間,易於客製化,並且由於其可折疊和輕質的特性,支持永續物流。由於其在運輸和貨架展示方面效率更高,折疊紙盒在大批量銷售中的應用尤為突出。

2024年,美國眼鏡包裝市場佔據了87.9%的市場。美國市場趨勢正受到消費者對高階包裝、永續性和增強型網購體驗的偏好的影響。隨著電子商務的持續蓬勃發展,對功能性、時尚性包裝的需求日益成長,這些包裝不僅能確保配送過程中的保護,還能提供引人入勝的客戶互動體驗。包裝創新正成為成熟且要求嚴苛的市場中實現差異化的關鍵。

活躍於眼鏡包裝市場的關鍵公司包括 Giorgio Fedon and Figli、Kling、King Home Printing、Ibex Packaging、Box Muse、Gatto Astucci 和 Classic Packaging。為了確保在眼鏡包裝行業的競爭地位,領先的參與者正在投資永續性、客製化和先進的設計技術。許多公司正在轉向可生物分解和可回收的包裝材料,以滿足環境法規和消費者期望。品牌差異化是透過反映產品身分的個人化和奢華風格的包裝來實現的。公司正在增強結構設計能力,以確保運輸過程中的耐用性,尤其是對於線上訂單。與眼鏡製造商和直接面對消費者的品牌的合作有助於加強他們的客戶群。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率

- 成本結構

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 對永續和環保包裝的需求不斷成長

- 時尚和處方眼鏡領域的眼鏡銷售成長

- 拓展電子商務分銷管道

- 奢侈品和設計師眼鏡包裝的客製化趨勢

- 更重視高階化與品牌差異化

- 產業陷阱與挑戰

- 永續和客製化包裝解決方案成本高

- 跨多個市場的監管合規挑戰

- 市場機會

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 科技與創新格局

- 當前的技術趨勢

- 新興技術

- 價格趨勢

- 歷史價格分析(2021-2024)

- 價格趨勢促進因素

- 區域價格差異

- 價格預測(2025-2034年)

- 定價策略

- 新興商業模式

- 合規性要求

- 永續性措施

- 永續材料評估

- 碳足跡分析

- 循環經濟實施

- 永續性認證和標準

- 永續性投資報酬率分析

- 全球消費者情緒分析

- 專利分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 市場集中度分析

- 按地區

- 關鍵參與者的競爭基準

- 財務績效比較

- 收入

- 利潤率

- 研發

- 產品組合比較

- 產品範圍廣度

- 科技

- 創新

- 地理位置比較

- 全球足跡分析

- 服務網路覆蓋

- 各區域市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 利基市場參與者

- 戰略展望矩陣

- 財務績效比較

- 2021-2024 年關鍵發展

- 併購

- 夥伴關係和合作

- 技術進步

- 擴張和投資策略

- 永續發展舉措

- 數位轉型舉措

- 新興/新創企業競爭對手格局

第5章:市場估計與預測:按材料,2021-2034

- 主要趨勢

- 塑膠

- 紙和紙板

- 金屬

- 皮革

- 其他

第6章:市場估計與預測:依產品類型,2021-2034

- 主要趨勢

- 折疊紙盒

- 硬盒/箱

- 袋裝

- 其他

第7章:市場估計與預測:依眼鏡分類,2021-2034

- 主要趨勢

- 處方眼鏡

- 太陽眼鏡

- 運動眼鏡

- 安全/工業眼鏡

第8章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第9章:公司簡介

- Box Muse

- Classic Packaging

- Gatto Astucci

- Giorgio Fedon and Figli

- Ibex Packaging

- King Home Printing

- Kling

- Lsuny Company

- Marber

- Packman Packaging

- Packtek

- Processo Plast Enterprise

- Rongyu Packing

- Salazar Packaging

The Global Eyewear Packaging Market was valued at USD 240.7 million in 2024 and is estimated to grow at a CAGR of 4.8% to reach USD 380.7 million by 2034. This growth is being propelled by increasing demand for both fashion and prescription eyewear, alongside the rapid rise of e-commerce as a dominant sales channel. A wider demographic now relies on eyewear due to factors like increased screen usage, vision correction needs, and the evolution of eyewear into a fashion-forward accessory. As a result, the need for high-quality packaging that reflects brand identity, elevates presentation, and protects premium products has grown significantly. Brands are focusing on packaging that merges visual appeal with structural integrity to meet these shifting expectations and reinforce customer loyalty in a competitive market landscape.

The growing dominance of online retail has reshaped how eyewear products are sold, increasing the demand for durable and visually appealing packaging. Protective, brand-focused designs are now essential to reduce product damage and boost unboxing experiences in direct-to-consumer channels. There is also a rising preference for eco-conscious solutions, which is driving a shift toward recyclable and sustainable materials in packaging. The integration of minimalist aesthetics and responsibly sourced materials reflects changing global preferences and compliance requirements.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $240.7 Million |

| Forecast Value | $380.7 Million |

| CAGR | 4.8% |

The paper and paperboard segment is expected to reach USD 104.3 million by 2034. With recyclability, lightweight, and sustainable sourcing becoming priorities, paper-based packaging is gaining popularity. These materials are used widely for exterior packaging and in-store displays, helping brands align with the growing eco-conscious consumer segment. Companies are increasingly incorporating FSC-certified boards and clean designs to enhance environmental responsibility while keeping their products visually appealing.

The folding cartons segment in the eyewear packaging market held a 33.7% share in 2024. Known for their cost-effectiveness and versatility, folding cartons remain a preferred secondary packaging choice in both retail and online settings. These cartons offer substantial space for branding, are easy to customize, and support sustainable logistics due to their collapsible and lightweight nature. Their use is particularly prominent in high-volume sales due to the efficiency they bring in shipping and shelf display.

United States Eyewear Packaging Market captured an 87.9% share in 2024. Market trends in the U.S. are being shaped by consumer preferences for premium packaging, sustainability, and enhanced online shopping experiences. As e-commerce continues to thrive, the need for functional and stylish packaging ensures protection during delivery, while offering an engaging customer interaction is growing steadily. Packaging innovation is becoming a tool for differentiation in a mature and demanding marketplace.

Key companies active in the Eyewear Packaging Market include Giorgio Fedon and Figli, Kling, King Home Printing, Ibex Packaging, Box Muse, Gatto Astucci, and Classic Packaging. To secure a competitive position in the eyewear packaging industry, leading players are investing in sustainability, customization, and advanced design technologies. Many companies are shifting toward biodegradable and recyclable packaging materials to meet environmental regulations and consumer expectations. Brand differentiation is achieved through personalized and luxury-inspired packaging that reflects the product's identity. Firms are enhancing structural design capabilities to ensure durability during shipping, especially for online orders. Partnerships with eyewear manufacturers and direct-to-consumer brands help strengthen their client base.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Material trends

- 2.2.2 Product Type trends

- 2.2.3 Eyewear trends

- 2.2.4 Regional trends

- 2.3 TAM analysis, 2025-2034 (USD Billion)

- 2.4 CXO perspectives: strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and strategic recommendations

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for sustainable and eco-friendly packaging

- 3.2.1.2 Growth in eyewear sales across fashion and prescription segments

- 3.2.1.3 Expansion of e-commerce distribution channels

- 3.2.1.4 Customization trends in luxury and designer eyewear packaging

- 3.2.1.5 Increasing focus on premiumization and brand differentiation

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of sustainable and custom packaging solutions

- 3.2.2.2 Regulatory compliance challenges across multiple markets

- 3.2.3 Market opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 Historical price analysis (2021-2024)

- 3.8.2 Price trend drivers

- 3.8.3 Regional price variations

- 3.8.4 Price forecast (2025-2034)

- 3.9 Pricing strategies

- 3.10 Emerging business models

- 3.11 Compliance requirements

- 3.12 Sustainability measures

- 3.12.1 Sustainable materials assessment

- 3.12.2 Carbon footprint analysis

- 3.12.3 Circular economy implementation

- 3.12.4 Sustainability certifications and standards

- 3.12.5 Sustainability roi analysis

- 3.13 Global consumer sentiment analysis

- 3.14 Patent analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia pacific

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&d

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ Startup Competitors Landscape

Chapter 5 Market Estimates & Forecast, By Material,2021-2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Plastic

- 5.3 Paper & paperboard

- 5.4 Metal

- 5.5 Leather

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Folding cartons

- 6.3 Rigid boxes/cases

- 6.4 Pouches

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Eyewear, 2021-2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Prescription glasses

- 7.3 Sunglasses

- 7.4 Sports eyewear

- 7.5 Safety/industrial glasses

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Box Muse

- 9.2 Classic Packaging

- 9.3 Gatto Astucci

- 9.4 Giorgio Fedon and Figli

- 9.5 Ibex Packaging

- 9.6 King Home Printing

- 9.7 Kling

- 9.8 Lsuny Company

- 9.9 Marber

- 9.10 Packman Packaging

- 9.11 Packtek

- 9.12 Processo Plast Enterprise

- 9.13 Rongyu Packing

- 9.14 Salazar Packaging