|

市場調查報告書

商品編碼

1766283

靈活模組化包裝系統市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Flexible and Modular Packaging Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

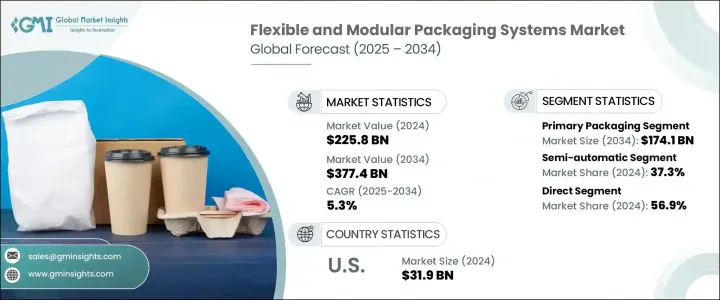

2024年,全球軟性及模組化包裝系統市場規模達2,258億美元,預計2034年將以5.3%的複合年成長率成長,達到3,774億美元。自動化技術的快速發展正在徹底改變製造業,高度適應性的包裝系統能夠在各種包裝形式、尺寸和產品類型之間快速切換。這種靈活性對於食品、化妝品和藥品等行業至關重要,這些行業通常面臨著頻繁的產品重新設計和種類繁多的產品組合。精簡營運以快速回應不斷變化的消費者偏好和更短的產品生命週期已成為至關重要的競爭優勢。小批量生產能力與無縫流程操作相結合,可提高效率和靈活性。環保意識的增強、支持性研發政策以及對社會治理的重視,正在推動企業尋求永續的包裝解決方案。

這些環保措施不僅提升了公司的品牌形象,也能開拓注重永續發展的新市場,最終提升顧客忠誠度和長期獲利能力。採用綠色實踐可以幫助企業透過有效利用資源和減少浪費來降低營運成本,從而實現環境責任與更佳財務業績相輔相成的雙贏局面。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 2258億美元 |

| 預測值 | 3774億美元 |

| 複合年成長率 | 5.3% |

半自動包裝系統在2024年佔據37.3%的市場佔有率,預計2025年至2034年期間的複合年成長率為6.1%。半自動包裝系統因其成本效益和適合中小型企業的特點,將繼續受到青睞。這些系統實現了人工和自動化的平衡組合,幫助企業在保持營運靈活性的同時降低資本支出。

2024年,直接分銷通路佔比56.9%。製造商更青睞直銷,因為這種方式能夠促進與客戶的密切聯繫,從而提供量身定做的解決方案和全面的售後支持,包括維護和技術援助。直接接觸能夠深入了解客戶的生產需求,使供應商能夠提供客製化的系統設計、培訓和服務合約。

2024年,美國軟性和模組化包裝系統市場價值達319億美元,預計到2034年將以5.9%的複合年成長率成長。自動化技術的進步以及包裝食品、藥品和個人護理等行業日益成長的需求,支撐了美國在全球市場的地位。北美擁有成熟的包裝機械產業和強大的消費者基礎,被公認為消費品製造業的領導者。州際安全、衛生和永續性相關法規的實施,正鼓勵企業將老舊設備升級為更有效率、更精簡的系統。

全球軟性和模組化包裝系統市場的關鍵公司包括 Barry-Wehmiller Companies、Coesia Group、Fuji Machinery Co., Ltd.、Haver & Boecker、IMA Group、Ishida Co., Ltd.、KHS GmbH、Marchesini Group、Multivac Group、ProMach Inc.、Serac Group、Sidelma、Schesibini Group、Multivac。為加強市場影響力,軟性和模組化包裝系統領域的公司專注於多項策略措施。他們投入大量資金進行研發,以創新先進、適應性強的包裝解決方案,滿足不斷變化的消費者需求。與技術提供者的策略夥伴關係和協作增強了他們的自動化能力,而收購有助於擴大產品組合和地理覆蓋範圍。公司強調永續性,正在開發符合全球環境法規的環保系統,吸引客戶優先考慮綠色包裝。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商概況

- 利潤率

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 機會

- 成長潛力分析

- 未來市場趨勢

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按包裝類型

- 監理框架

- 標準和認證

- 環境法規

- 進出口法規

- 貿易統計(HS 編碼-3921)

- 主要進口國

- 主要出口國

- 產品採購分析

- 波特五力分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:按類型,2021 - 2034 年

- 主要趨勢

- 軟包裝

- 電影

- 袋子和包包

- 收縮膜

- 拉伸膜

- 包裝紙和箔紙

- 模組化包裝

- 模組化裝盒系統

- 模組化裝箱機

- 模組化灌裝機

- 模組化堆疊系統

- 模組化標籤系統

第6章:市場估計與預測:依包裝類型,2021 - 2034 年

- 主要趨勢

- 基本的

- 次要

- 第三

第7章:市場估計與預測:按自動化,2021 - 2034 年

- 主要趨勢

- 手動的

- 半自動

- 全自動

第8章:市場估計與預測:按材料,2021 - 2034 年

- 主要趨勢

- 塑膠

- 紙和紙板

- 金屬

- 玻璃

- 生物基和可堆肥材料

- 其他

第9章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 食品和飲料

- 烘焙和糖果

- 乳製品

- 製藥

- 電子商務與物流

- 其他(農產品等)

第 10 章:市場估計與預測:按配銷通路,2021 年至 2034 年

- 主要趨勢

- 直接的

- 間接

第 11 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- MEA

- 南非

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

第12章:公司簡介

- Barry-Wehmiller Companies

- Coesia Group

- Fuji Machinery Co., Ltd.

- Haver & Boecker

- IMA Group

- Ishida Co., Ltd.

- KHS GmbH

- Marchesini Group

- Multivac Group

- ProMach Inc.

- Serac Group

- Sidel Group

- SIG Combibloc Group

- Syntegon Technology (Bosch Packaging)

- Tetra Pak

The Global Flexible and Modular Packaging Systems Market was valued at USD 225.8 billion in 2024 and is estimated to grow at a CAGR of 5.3% to reach USD 377.4 billion by 2034. The rapid advancement in automation technology is revolutionizing manufacturing with highly adaptable packaging systems capable of switching between various packaging formats, sizes, and product types swiftly. This flexibility is essential across industries like food, cosmetics, and pharmaceuticals, which often face frequent product redesigns and a broad portfolio of items. Streamlining operations to quickly respond to shifting consumer preferences and shorter product life cycles has become a vital competitive edge. Small batch production capabilities, combined with seamless process operation, offer enhanced efficiency and agility. Increased environmental awareness, supportive research and development policies, and emphasis on social governance are pushing companies toward sustainable packaging solutions.

These eco-friendly initiatives not only enhance a company's brand image but also open doors to new market segments that prioritize sustainability, ultimately driving increased customer loyalty and long-term profitability. Embracing green practices allows businesses to reduce operational costs through efficient resource use and waste minimization, creating a win-win scenario where environmental responsibility aligns with stronger financial performance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $225.8 Billion |

| Forecast Value | $377.4 Billion |

| CAGR | 5.3% |

The semi-automatic segment held a 37.3% share in 2024 and is projected to grow at a CAGR of 6.1% between 2025 and 2034. Semi-automatic packaging systems continue to be favored for their cost-effectiveness and suitability for small to medium-sized operations. These systems provide a balanced combination of manual effort and automation, helping businesses reduce capital expenditures while maintaining operational flexibility.

Direct distribution channels accounted for a 56.9% share in 2024. Manufacturers prefer direct sales because this approach fosters close relationships with customers, allowing for tailored solutions and comprehensive after-sales support, including maintenance and technical assistance. Direct engagement provides valuable insights into customer production needs, enabling suppliers to offer customized system designs, training, and service contracts.

U.S. Flexible and Modular Packaging Systems Market was valued at USD 31.9 billion in 2024 and is expected to grow at a CAGR of 5.9% through 2034. The country's stronghold in the global market is supported by advancements in automation technology and growing demand from sectors like packaged foods, pharmaceuticals, and personal care. With a well-established packaging machinery industry and a robust consumer base, North America is recognized as a leader in consumer goods manufacturing. The implementation of interstate regulations concerning safety, hygiene, and sustainability is encouraging companies to upgrade outdated equipment to more efficient, streamlined systems.

Key companies in the Global Flexible and Modular Packaging Systems Market include Barry-Wehmiller Companies, Coesia Group, Fuji Machinery Co., Ltd., Haver & Boecker, IMA Group, Ishida Co., Ltd., KHS GmbH, Marchesini Group, Multivac Group, ProMach Inc., Serac Group, Sidel Group, SIG Combibloc Group, Syntegon Technology (Bosch Packaging), and Tetra Pak. To strengthen their market presence, companies in the flexible and modular packaging systems sector focus on several strategic initiatives. They invest heavily in research and development to innovate advanced, adaptable packaging solutions that meet evolving consumer demands. Strategic partnerships and collaborations with technology providers enhance their automation capabilities, while acquisitions help expand product portfolios and geographic reach. Emphasizing sustainability, firms are developing eco-friendly systems that comply with global environmental regulations, which in turn attracts customers to prioritize green packaging.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Packaging type

- 2.2.4 Automation

- 2.2.5 Material

- 2.2.6 End use

- 2.2.7 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and Innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By packaging type

- 3.7 Regulatory framework

- 3.7.1 Standards and certifications

- 3.7.2 Environmental regulations

- 3.7.3 Import export regulations

- 3.8 Trade statistics (HS code-3921)

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Product procurement analysis

- 3.10 Porter's five forces analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Flexible packaging

- 5.2.1 Films

- 5.2.2 Pouches & bags

- 5.2.3 Shrink films

- 5.2.4 Stretch films

- 5.2.5 Wraps & foils

- 5.3 Modular packaging

- 5.3.1 Modular cartoning systems

- 5.3.2 Modular case packers

- 5.3.3 Modular filling machines

- 5.3.4 Modular palletizing systems

- 5.3.5 Modular labeling systems

Chapter 6 Market Estimates & Forecast, By Packaging Type, 2021 - 2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Primary

- 6.3 Secondary

- 6.4 Tertiary

Chapter 7 Market Estimates & Forecast, By Automation, 2021 - 2034 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Manual

- 7.3 Semi-automatic

- 7.4 Fully automatic

Chapter 8 Market Estimates & Forecast, By Material, 2021 - 2034 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Plastic

- 8.3 Paper and paperboard

- 8.4 Metal

- 8.5 Glass

- 8.6 Bio-based and compostable materials

- 8.7 Other

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Food and beverages

- 9.3 Bakery and confectionery

- 9.4 Dairy

- 9.5 Pharmaceuticals

- 9.6 E-commerce and logistics

- 9.7 Others (agricultural products, etc.)

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Direct

- 10.3 Indirect

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 UAE

- 11.6.3 Saudi Arabia

Chapter 12 Company Profiles

- 12.1 Barry-Wehmiller Companies

- 12.2 Coesia Group

- 12.3 Fuji Machinery Co., Ltd.

- 12.4 Haver & Boecker

- 12.5 IMA Group

- 12.6 Ishida Co., Ltd.

- 12.7 KHS GmbH

- 12.8 Marchesini Group

- 12.9 Multivac Group

- 12.10 ProMach Inc.

- 12.11 Serac Group

- 12.12 Sidel Group

- 12.13 SIG Combibloc Group

- 12.14 Syntegon Technology (Bosch Packaging)

- 12.15 Tetra Pak

全球軟性紙包裝市場:預測(至2032年)-按包裝類型、材料類型、通路、技術、應用和地區進行分析

全球軟性紙包裝市場:預測(至2032年)-按包裝類型、材料類型、通路、技術、應用和地區進行分析 軟質包裝市場按材料、包裝類型、印刷技術、應用和地區分類-預測至2030年

軟質包裝市場按材料、包裝類型、印刷技術、應用和地區分類-預測至2030年 包裝貼合機機:全球市佔率及排名、總收入及需求預測(2025-2031年)

包裝貼合機機:全球市佔率及排名、總收入及需求預測(2025-2031年) 軟質包裝的全球市場的未來(~2030年)2032 年軟包裝市場預測:按包裝類型、結構、印刷、封口、密封、最終用戶和地區進行的全球分析

軟質包裝的全球市場的未來(~2030年)2032 年軟包裝市場預測:按包裝類型、結構、印刷、封口、密封、最終用戶和地區進行的全球分析 按材料、產品類型、包裝形式、最終用途和分銷管道分類的軟性工業包裝市場 - 2025-2030 年全球預測軟包裝市場按產品類型、材料類型、技術、封蓋類型、最終用戶和分銷管道分類 - 2025-2030 年全球預測

按材料、產品類型、包裝形式、最終用途和分銷管道分類的軟性工業包裝市場 - 2025-2030 年全球預測軟包裝市場按產品類型、材料類型、技術、封蓋類型、最終用戶和分銷管道分類 - 2025-2030 年全球預測 全球軟包裝市場研究報告-產業分析、規模、佔有率、成長、趨勢及2025年至2033年預測

全球軟包裝市場研究報告-產業分析、規模、佔有率、成長、趨勢及2025年至2033年預測 歐洲軟包裝:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)軟包裝產業:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)

歐洲軟包裝:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)軟包裝產業:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)