|

市場調查報告書

商品編碼

1936052

全球國防噴射燃料啟動器 (JFS) 市場 (2026-2036)Global Defense Engine Oil Cooling Systems Market 2026-2036 |

||||||

全球國防噴射燃料啟動器 (JFS) 市場預計在 2026 年達到 1.9 億美元,預計到 2036 年將達到 2.7 億美元,2026 年至 2036 年的複合年增長率 (CAGR) 為 3.30%。

引言

全球國防噴射燃料啟動器 (JFS) 市場使用獨立的燃氣發生器,透過渦輪壓縮機組件燃燒噴射燃料 A,從而驅動主引擎點火。單軸JFS將核心引擎從零轉速加速至自推進轉速,然後透過離合器與輔助驅動裝置分離。

市場正朝著 "更電氣化" 的架構發展,這需要與混合動力推進系統相容的輕型啟動器。核心技術包括氣浮式渦輪、可變進氣導葉以及與FADEC聯動的順序控制,以實現無縫切換。模組化大修支援現場維護。

地緣政治緊急需求正在推動發展,優先考慮能夠耐受污染燃料和極端氣候的JFS。開放式架構支援跨引擎系列的整合。供應鏈專注於高溫密封件和單晶葉片。競爭對手包括霍尼韋爾、普惠和賽峰集團,它們在電動輔助版本方面處於領先地位。

國防噴射燃料啟動器 (JFS) 技術的影響

電助力 JFS 啟動器在熱啟動時,透過高扭力馬達在初始轉速提升後直接切換至燃料燃燒,顯著縮短了啟動時間。可變幾何壓縮機可防止在各種環境條件下(從極寒到沙漠環境)出現喘振。

陶瓷軸承完全取代了油路系統,無需掃氣幫浦即可實現乾式馬達運轉。內建的健康監測系統分析排氣溫度和振動特性,可在渦輪葉片失效前預測其損壞情況。增材製造的葉輪優化了氣流,同時最大限度地減少了慣性質量。

全權限數位引擎控制 (FADEC) 融合控制系統協調啟動器分離與主引擎點火,防止熱氣回流。混合動力設計整合了啟動發電機,可實現無縫模式切換。與雙軸設計相比,單軸簡化設計減少了零件數量。

數位孿生技術驗證了在戰鬥損傷進氣條件下的啟動範圍。燃料霧化環形燃燒器能夠可靠地點燃合成燃料混合物。這些進步使得從前沿跑道自主起飛成為可能。

國防噴射燃料啟動器 (JFS) 的關鍵驅動因素

"更電氣化" 引擎的普及推動了對整合式啟動發電機的需求,以取代外部 JFS,從而促進了混合動力設計的發展。第六代無人平台需要具備無需地面支援的空中啟動能力。

永續性強調模組化轉子,允許互換燃料盒。出口項目要求對各種煤油燃料具有廣泛的耐受性。緊急發射要求在冷浸狀態下也能在一分鐘內啟動。

預算考量傾向於採用具有軍用級硬化性能的商用衍生產品。供應的穩定性可以彌補渦輪葉片材料的限制。互通性使得聯盟引擎可以使用通用的驅動底座。

定向能武器需要兆瓦級的啟動能力,因此噴射燃料啟動器(JFS)是一種能夠獨立運作的啟動裝置。

本報告分析了全球國防噴射燃料啟動器(JFS)市場,深入探討了影響該市場的技術、未來十年的預測以及區域趨勢。

目錄

國防噴射燃料啟動器 (JFS) 市場報告定義

國防噴射燃料啟動器 (JFS) 市場區隔

依平台

依啟動器類型

依點火方式

未來十年國防噴射燃料啟動器 (JFS) 市場分析

國防噴射燃料啟動器 (JFS) 市場技術

全球國防噴射燃料啟動器 (JFS) 市場預測

區域國防噴射燃料啟動器 (JFS) 市場趨勢及預測

北美

驅動因素、限制因素及挑戰

PEST分析

市場預測與情境分析

主要公司

供應商層級概覽

公司標竿分析

歐洲

中東

亞太地區

南美洲

國防噴射燃料啟動器 (JFS) 市場國家分析

美國

國防項目

最新資訊

專利

當前市場技術成熟度

市場預測與情境分析

加拿大

義大利

法國

德國

荷蘭

比利時

西班牙

瑞典

希臘

澳洲

南非

印度

中國

俄羅斯

韓國

日本

馬來西亞

新加坡

巴西

國防噴射燃料啟動器 (JFS) 市場機會矩陣

國防噴射燃料啟動器 (JFS) 市場專家意見

結論

關於航空與國防市場報告

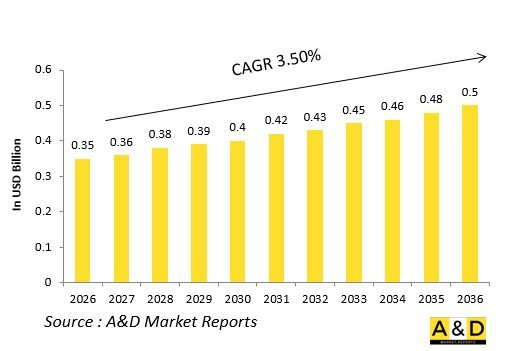

The Global Defense Engine Oil Cooling Systems Market is estimated at USD 0.35 billion in 2026, projected to grow to USD 0.5 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 3.50% over the forecast period 2026-2036.

Introduction

The global Defense Engine Oil Cooling Systems market regulates lubricant temperatures to protect bearings and gears under extreme thermal loads from combat maneuvers and weapons bay openings. Air-oil coolers exchange heat with bypass air, while fuel-oil exchangers leverage kerosene's capacity during cruise.

Market evolution tracks sixth-generation engines with ceramic turbines generating unprecedented sump temperatures. Core technologies include surface-air coolers, fuel-cooled oil coolers, and thermostatic bypass valves maintaining oil viscosity across flight envelopes. Modular heat exchanger cores enable rapid field swaps.

Geopolitical air superiority campaigns drive development, prioritizing systems compatible with directed-energy weapons and synthetic lubricants. Open architectures support technology insertion without engine redesigns. Supply chains focus on titanium brazing and corrosion-resistant coatings. Competition features Honeywell, Collins Aerospace, and Safran pioneering ram-air recovery designs.

Technology Impact in Defense Engine Oil Cooling Systems

Microchannel heat exchangers multiply surface area within existing envelopes, doubling heat rejection via laminar flow optimization. Phase-change materials in secondary loops absorb transient loads during afterburner lighting, stabilizing primary oil temperatures.

Electrochromic variable-geometry louvers modulate ram-air intake autonomously, maximizing recovery during climbs while minimizing drag in loiter. Fuel-cooled oil coolers with vortex generators enhance kerosene-side convection, rejecting heat without auxiliary blowers.

Embedded fiber-optic distributed temperature sensors feed FADEC closed-loop control, preempting coking during sustained max power. Additively manufactured lattice fins boost air-side effectiveness while slashing weight. Synthetic ester lubricants with doubled thermal capacity enable hotter sumps.

Predictive algorithms analyze delta-T signatures across cores, cueing filter swaps before bypass activation. Hybrid electric architectures demand dual-loop cooling for motor oils alongside turbine lubricants. Digital twins validate exchanger performance under battle-damaged inlet flows. These ensure continuous lubrication throughout mission profiles.

Key Drivers in Defense Engine Oil Cooling Systems

Adaptive cycle engines generate sump temperatures exceeding legacy limits, mandating advanced exchangers beyond current fuel-cooled capacity. Sixth-generation unmanned platforms require autonomous thermal management without pilot override.

Sustainment prioritizes core modularization eliminating scheduled engine removals. Export programs demand wide-cut fuel compatibility across kerosene blends. Supercruise-afterburner cycling stresses conventional coolers beyond margins.

Budget favors commercial derivatives with mil-spec hardening. Supply resilience counters titanium constraints via 3D-printed alternatives. Interoperability enables common cores across coalition engines.

Directed-energy extraction creates megawatt thermal loads requiring parallel cooling paths. These position oil cooling as thermodynamic enablers.

Regional Trends in Defense Engine Oil Cooling Systems

North America leads F-35 sustainment, pioneering fuel-cooled architectures for STOVL profiles.

Europe upgrades Rafale/Typhoon exchangers for synthetic lubricants in dispersed basing.

Asia-Pacific surges with indigenous programs-India's Kaveri, China's WS-15-prioritizing high-altitude heat rejection.

Middle East adapts coatings for sand-contaminated oils.

Russia hardens exchangers for Su-57 sustained afterburner.

South Korea integrates KF-21 exports with common cores.

Trends favor microchannel designs; Asia-Pacific captures manufacturing growth.

Key Defense Engine Oil Cooling Systems Programs

F135 fuel-oil cooler sustains STOVL transitions and afterburner via vortex-enhanced kerosene flow.

NGAD adaptive exchangers schedule cooling with third-stream modulation.

EJ200 upgrades reject supercruise heat through variable-geometry air-oil cores.

Kaveri equips Tejas with indigenous ram-air recovery.

F119 exchangers enable stealth missions with minimized drag louvers.

Rafale M88 integrates carrier catapult thermal surge protection.

Su-57 AL-41F1 handles thrust-vectoring oil heating.

T-50 FADEC-controlled bypass prevents sump overtemperature.

Table of Contents

Defense Engine Oil Cooling Systems Market - Table of Contents

Defense Engine Oil Cooling Systems Market Report Definition

Defense Engine Oil Cooling Systems Market Segmentation

By Platform

By Cooling Method

By System Integration

Defense Engine Oil Cooling Systems Market Analysis for next 10 Years

The 10-year Defense Engine Oil Cooling Systems market analysis would give a detailed overview of Defense Engine Oil Cooling Systems market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense Engine Oil Cooling Systems Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense Engine Oil Cooling Systems Market Forecast

The 10-year Defense Engine Oil Cooling Systems market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense Engine Oil Cooling Systems Market Trends & Forecast

The regional counter drone market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Defense Engine Oil Cooling Systems Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense Engine Oil Cooling Systems Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense Engine Oil Cooling Systems Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2026-2036

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By System Integration, 2026-2036

- Table 18: Scenario Analysis, Scenario 1, By Platform, 2026-2036

- Table 19: Scenario Analysis, Scenario 1, By Cooling Method, 2026-2036

- Table 20: Scenario Analysis, Scenario 2, By System Integration, 2026-2036

- Table 21: Scenario Analysis, Scenario 2, By Platform, 2026-2036

- Table 22: Scenario Analysis, Scenario 2, By Cooling Method, 2026-2036

List of Figures

- Figure 1: Global Defense Engine Oil Cooling Systems Market Forecast, 2026-2036

- Figure 2: Global Defense Engine Oil Cooling Systems Market Forecast, By System Integration, 2026-2036

- Figure 3: Global Defense Engine Oil Cooling Systems Market Forecast, By Platform, 2026-2036

- Figure 4: Global Defense Engine Oil Cooling Systems Market Forecast, By Cooling Method, 2026-2036

- Figure 5: North America, Defense Engine Oil Cooling Systems Market, Forecast, 2026-2036

- Figure 6: Europe, Defense Engine Oil Cooling Systems Market, Forecast, 2026-2036

- Figure 7: Middle East, Defense Engine Oil Cooling Systems Market, Forecast, 2026-2036

- Figure 8: APAC, Defense Engine Oil Cooling Systems Market, Forecast, 2026-2036

- Figure 9: South America, Defense Engine Oil Cooling Systems Market, Forecast, 2026-2036

- Figure 10: United States, Defense Engine Oil Cooling Systems Market, Technology Maturation, 2026-2036

- Figure 11: United States, Defense Engine Oil Cooling Systems Market, Forecast, 2026-2036

- Figure 12: Canada, Defense Engine Oil Cooling Systems Market, Technology Maturation, 2026-2036

- Figure 13: Canada, Defense Engine Oil Cooling Systems Market, Forecast, 2026-2036

- Figure 14: Italy, Defense Engine Oil Cooling Systems Market, Technology Maturation, 2026-2036

- Figure 15: Italy, Defense Engine Oil Cooling Systems Market, Market Forecast, 2026-2036

- Figure 16: France, Defense Engine Oil Cooling Systems Market, Technology Maturation, 2026-2036

- Figure 17: France, Defense Engine Oil Cooling Systems Market, Market Forecast, 2026-2036

- Figure 18: Germany, Defense Engine Oil Cooling Systems Market, Technology Maturation, 2026-2036

- Figure 19: Germany, Defense Engine Oil Cooling Systems Market, Market Forecast, 2026-2036

- Figure 20: Netherlands, Defense Engine Oil Cooling Systems Market, Technology Maturation, 2026-2036

- Figure 21: Netherlands, Defense Engine Oil Cooling Systems Market, Market Forecast, 2026-2036

- Figure 22: Belgium, Defense Engine Oil Cooling Systems Market, Technology Maturation, 2026-2036

- Figure 23: Belgium, Defense Engine Oil Cooling Systems Market, Market Forecast, 2026-2036

- Figure 24: Spain, Defense Engine Oil Cooling Systems Market, Technology Maturation, 2026-2036

- Figure 25: Spain, Defense Engine Oil Cooling Systems Market, Market Forecast, 2026-2036

- Figure 26: Sweden, Defense Engine Oil Cooling Systems Market, Technology Maturation, 2026-2036

- Figure 27: Sweden, Defense Engine Oil Cooling Systems Market, Market Forecast, 2026-2036

- Figure 28: Brazil, Defense Engine Oil Cooling Systems Market, Technology Maturation, 2026-2036

- Figure 29: Brazil, Defense Engine Oil Cooling Systems Market, Market Forecast, 2026-2036

- Figure 30: Australia, Defense Engine Oil Cooling Systems Market, Technology Maturation, 2026-2036

- Figure 31: Australia, Defense Engine Oil Cooling Systems Market, Market Forecast, 2026-2036

- Figure 32: India, Defense Engine Oil Cooling Systems Market, Technology Maturation, 2026-2036

- Figure 33: India, Defense Engine Oil Cooling Systems Market, Market Forecast, 2026-2036

- Figure 34: China, Defense Engine Oil Cooling Systems Market, Technology Maturation, 2026-2036

- Figure 35: China, Defense Engine Oil Cooling Systems Market, Market Forecast, 2026-2036

- Figure 36: Saudi Arabia, Defense Engine Oil Cooling Systems Market, Technology Maturation, 2026-2036

- Figure 37: Saudi Arabia, Defense Engine Oil Cooling Systems Market, Market Forecast, 2026-2036

- Figure 38: South Korea, Defense Engine Oil Cooling Systems Market, Technology Maturation, 2026-2036

- Figure 39: South Korea, Defense Engine Oil Cooling Systems Market, Market Forecast, 2026-2036

- Figure 40: Japan, Defense Engine Oil Cooling Systems Market, Technology Maturation, 2026-2036

- Figure 41: Japan, Defense Engine Oil Cooling Systems Market, Market Forecast, 2026-2036

- Figure 42: Malaysia, Defense Engine Oil Cooling Systems Market, Technology Maturation, 2026-2036

- Figure 43: Malaysia, Defense Engine Oil Cooling Systems Market, Market Forecast, 2026-2036

- Figure 44: Singapore, Defense Engine Oil Cooling Systems Market, Technology Maturation, 2026-2036

- Figure 45: Singapore, Defense Engine Oil Cooling Systems Market, Market Forecast, 2026-2036

- Figure 46: United Kingdom, Defense Engine Oil Cooling Systems Market, Technology Maturation, 2026-2036

- Figure 47: United Kingdom, Defense Engine Oil Cooling Systems Market, Market Forecast, 2026-2036

- Figure 48: Opportunity Analysis, Defense Engine Oil Cooling Systems Market, By System Integration (Cumulative Market), 2026-2036

- Figure 49: Opportunity Analysis, Defense Engine Oil Cooling Systems Market, By System Integration (CAGR), 2026-2036

- Figure 50: Opportunity Analysis, Defense Engine Oil Cooling Systems Market, By (Cumulative Market), 2026-2036

- Figure 51: Opportunity Analysis, Defense Engine Oil Cooling Systems Market, By Platform(CAGR), 2026-2036

- Figure 52: Opportunity Analysis, Defense Engine Oil Cooling Systems Market, By Cooling Method (Cumulative Market), 2026-2036

- Figure 53: Opportunity Analysis, Defense Engine Oil Cooling Systems Market, By Cooling Method (CAGR), 2026-2036

- Figure 54: Scenario Analysis, Defense Engine Oil Cooling Systems Market, Cumulative Market, 2026-2036

- Figure 55: Scenario Analysis, Defense Engine Oil Cooling Systems Market, Global Market, 2026-2036

- Figure 56: Scenario 1, Defense Engine Oil Cooling Systems Market, Total Market, 2026-2036

- Figure 57: Scenario 1, Defense Engine Oil Cooling Systems Market, By System Integration, 2026-2036

- Figure 58: Scenario 1, Defense Engine Oil Cooling Systems Market, By Platform, 2026-2036

- Figure 59: Scenario 1, Defense Engine Oil Cooling Systems Market, By Cooling Method, 2026-2036

- Figure 60: Scenario 2, Defense Engine Oil Cooling Systems Market, Total Market, 2026-2036

- Figure 61: Scenario 2, Defense Engine Oil Cooling Systems Market, By System Integration, 2026-2036

- Figure 62: Scenario 2, Defense Engine Oil Cooling Systems Market, By Platform, 2026-2036

- Figure 63: Scenario 2, Defense Engine Oil Cooling Systems Market, By Cooling Method, 2026-2036

- Figure 64: Company Benchmark, Defense Engine Oil Cooling Systems Market, 2026-2036

2026年航太與國防印刷電路基板(PCB)市場報告

2026年航太與國防印刷電路基板(PCB)市場報告 2025-2029年全球航太和國防領域的人工智慧(AI)和機器人技術

2025-2029年全球航太和國防領域的人工智慧(AI)和機器人技術 GMIPulse -航太與國防市場情報訂閱2025年航太和國防無損檢測(NDT)全球市場報告

GMIPulse -航太與國防市場情報訂閱2025年航太和國防無損檢測(NDT)全球市場報告 航太和國防市場:按產業和地區分類2025年全球航太與國防市場報告

航太和國防市場:按產業和地區分類2025年全球航太與國防市場報告 航空航太和國防工程服務市場:全2025-2035年2025-2035年全球航空航太與國防部門工程與研發

航空航太和國防工程服務市場:全2025-2035年2025-2035年全球航空航太與國防部門工程與研發 航太和國防熱管理系統市場機會、成長動力、產業趨勢分析和 2025 - 2034 年預測

航太和國防熱管理系統市場機會、成長動力、產業趨勢分析和 2025 - 2034 年預測 航太和國防諮詢市場按服務類型、應用和最終用戶分類 - 2025-2030 年全球預測

航太和國防諮詢市場按服務類型、應用和最終用戶分類 - 2025-2030 年全球預測