|

市場調查報告書

商品編碼

1715448

航空航太和國防工程服務市場:全2025-2035年Global Aerospace & Defense Engineering Services Market 2025-2035 |

||||||

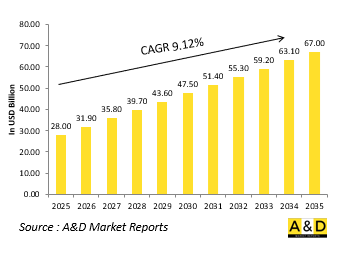

全球航空航太和國防工程服務市場預計在 2025 年價值 280 億美元,預計到 2035 年將成長到 670 億美元,複合年增長率為 9.12%。

航空航太與國防工程服務市場簡介

軍事航空航太和國防工程服務在設計、開發、整合和維持空中、陸地、海洋和太空領域的先進防禦系統方面發揮著至關重要的作用。這些服務涵蓋廣泛的技術專長,包括系統工程、軟體開發、結構分析、推進優化、網路安全和數位轉型。隨著國防平台變得越來越先進和互聯,工程服務對於確保新舊系統保持有效運作並符合不斷發展的軍事標準至關重要。對多域作戰、無人系統和天基防禦資產的日益關注,進一步擴大了航空航天和國防工程服務的範圍。政府和國防承包商越來越依賴專業工程公司來提供創新解決方案,以提高平台性能、延長系統生命週期並降低維護成本。從原型開發到在役支持,這些服務彌合了技術進步與實際營運需求之間的差距。隨著全球國防現代化進程的加快,工程服務提供者在塑造下一代軍事能力、確保任務準備和支援全球盟友防禦計畫方面發揮著比以往任何時候都更具戰略性的作用。

科技對航太與國防工程服務市場的影響:

技術發展正在改變軍事航空航太和國防工程服務,實現更有效率的開發週期、增強的性能分析和改進的維持策略。基於模型的系統工程 (MBSE) 和數位孿生等數位工程工具正在徹底改變國防平台的設計、測試和維護方式,降低原型成本並加快部署時間。人工智慧和機器學習透過分析大量的營運數據來增強預測性維護、優化物流並改善戰場決策。積層製造和先進材料科學使得生產更輕、更堅固的零件成為可能,從而使軍用飛機和地面車輛更加耐用、更省油。網路安全也是一個重點,工程團隊整合了先進的加密、入侵偵測和安全軟體開發技術,以保護關鍵任務系統免受網路威脅。自主技術和人機協作的興起將需要專業的工程專業知識,將人工智慧驅動的決策融入作戰系統,同時確保營運安全和合規性。這些技術進步不僅提高了軍事平台的效力,也改變了國防部隊在快速發展的作戰環境中規劃、執行和維持任務的方式。

航空航太與國防工程服務市場的主要驅動力:

軍事航空航太和國防工程服務的需求受到戰略、營運和技術因素的共同驅動。主要推動因素之一是全球國防現代化的推動,各國都在升級舊系統並開發下一代能力以應對新出現的威脅。高超音速武器、隱形平台和定向能系統等航空航天技術的快速發展需要不斷創新以確保軍事競爭優勢。不斷加劇的地緣政治緊張局勢和不斷變化的國防重點也促使各國政府投資更具彈性和適應性的國防系統,進一步增加了對專業工程技能的需求。將無人平台和自主系統整合到軍事行動中需要新的工程方法來確保與現有資產的無縫互通性。此外,成本效益和永續性問題正在推動國防組織採用先進的生命週期管理策略,包括預測性維護和模組化平台設計。隨著軍隊尋求在管理預算限制的同時優化性能,將工程服務外包給專業公司正成為一個有吸引力的選擇。多領域作戰(陸、空、海、太空和網路戰的交叉)的日益複雜化進一步凸顯了工程服務在製定現代國防戰略中的關鍵作用。

航空航太與國防工程服務市場的區域趨勢:

軍事航空航太和國防工程服務的區域趨勢會根據國防優先事項、工業能力和地緣政治動態而變化。在北美,尤其是美國,強大的國防預算和強大的國防工業基礎正在推動對先進工程服務的大規模投資。重點是下一代戰鬥機、飛彈防禦系統、太空軍事資產和人工智慧驅動的戰爭解決方案。歐洲優先考慮未來作戰航空系統 (FCAS) 和暴風戰鬥機計劃等聯合防禦計劃,這促使對航空電子、推進和隱形技術等工程專業知識的需求增加。亞太地區正經歷快速發展,中國、印度、日本和韓國大力投資自主防禦能力,包括高超音速武器、先進的海軍平台和自主系統。這些國家越來越依賴當地的工程專業知識來開發和維持其軍事資產。在中東,透過戰略合作夥伴關係和對當地製造和維持能力的投資,繼續擴大的航空航太和國防工程足跡。國防工程服務透過技術轉移和國際合作在拉丁美洲和非洲逐漸擴大,支持了該地區航空航太工業的發展並提高了軍事自給自足能力。

領先的航空航太和國防工程服務項目

歐盟委員會宣佈為 EDIRPA 計劃(透過聯合採購加強歐洲國防工業)下的通用裝甲車系統 (CAVS) 項目提供 6000 萬歐元的資金。這項雄心勃勃的計畫旨在開發現代化、標準化的裝甲車,以增強芬蘭、拉脫維亞、瑞典和德國軍隊的作戰能力。 CAVS計畫旨在滿足日益增長的部隊機動性和防護需求,同時促進歐洲國家之間的國防合作和裝備標準化。

本報告研究了全球航空航太和國防工程服務市場,並按細分市場、技術趨勢、機會分析、公司概況和國家數據提供了 10 年市場預測。

目錄

全球航空航太與國防工程服務市場 – 目錄

全球航空航太與國防工程服務市場 - 報告定義

全球航空航太與國防工程服務市場細分

按地區

按類型

按平台

依用途

未來 10 年全球航太與國防工程服務市場分析

對全球航空航太和國防工程服務市場長達十年的分析提供了全球航空航太和國防工程服務市場成長、變化趨勢、技術採用概況和整體市場吸引力的詳細概述。

全球航空航太與國防工程服務市場技術

本部分涵蓋預計將影響該市場的十大技術以及這些技術可能對整個市場產生的影響。

全球航空航太與國防工程服務市場預測

針對該市場未來十年的全球航空航太和國防工程服務市場預測,已在上述各個細分市場進行了詳細解釋。

區域航空航太和國防工程服務市場趨勢與預測

本部分涵蓋全球航空航太和國防工程服務市場的區域趨勢、推動因素、阻礙因素、課題以及政治、經濟、社會和技術方面。它還提供了詳細的區域市場預測和情境分析。區域分析包括主要公司概況、供應商格局和公司基準測試。目前市場規模是根據正常業務情境估算的。

北美

促進因素、阻礙因素與課題

害蟲

市場預測與情境分析

主要公司

供應商層級結構

企業基準

歐洲

中東

亞太地區

南美洲

市場國家分析

本章重點介紹該市場的主要防禦計劃,並介紹該市場的最新新聞和專利。它還提供國家級的 10 年市場預測和情境分析。

美國

國防計畫

最新消息

專利

目前該市場的技術成熟度

市場預測與情境分析

加拿大

義大利

法國

德國

荷蘭

比利時

西班牙

瑞典

希臘

澳洲

南非

印度

中國

俄羅斯

韓國

日本

馬來西亞

新加坡

巴西

全球航空航太與國防工程服務市場機會矩陣

全球航空航太與國防工程服務市場報告專家意見

結論

關於航空和國防市場報告

The Global Aerospace & Defense Engineering Services market is estimated at USD 28.00 billion in 2025, projected to grow to USD 67.00 billion by 2035 at a Compound Annual Growth Rate (CAGR) of 9.12% over the forecast period 2025-2035.

Introduction to Aerospace & Defense Engineering Services Market

Military aerospace and defense engineering services play a crucial role in the design, development, integration, and sustainment of advanced defense systems across air, land, sea, and space domains. These services encompass a broad range of technical expertise, including systems engineering, software development, structural analysis, propulsion optimization, cybersecurity, and digital transformation. With defense platforms becoming more sophisticated and interconnected, engineering services are vital in ensuring that new and legacy systems remain operationally effective and compliant with evolving military standards. The growing emphasis on multi-domain operations, unmanned systems, and space-based defense assets has further expanded the scope of aerospace and defense engineering services. Governments and defense contractors increasingly rely on specialized engineering firms to provide innovative solutions that enhance platform performance, extend system lifecycles, and reduce maintenance costs. From prototype development to in-service support, these services bridge the gap between technological advancements and real-world operational requirements. As global defense modernization efforts accelerate, engineering service providers are playing an ever-more strategic role in shaping next-generation military capabilities, ensuring mission readiness, and supporting allied defense initiatives worldwide.

Technology Impact in Aerospace & Defense Engineering Services Market:

Advancements in technology are reshaping military aerospace and defense engineering services, enabling more efficient development cycles, enhanced performance analysis, and improved sustainment strategies. Digital engineering tools, such as model-based systems engineering (MBSE) and digital twins, have revolutionized how defense platforms are designed, tested, and maintained, reducing prototyping costs and accelerating time-to-deployment. Artificial intelligence and machine learning are enhancing predictive maintenance, optimizing logistics, and improving battlefield decision-making by analyzing vast amounts of operational data. Additive manufacturing and advanced materials science are enabling the production of lightweight, high-strength components that enhance durability and fuel efficiency in military aircraft and ground vehicles. Cybersecurity has also become a central focus, with engineering teams integrating advanced encryption, intrusion detection, and secure software development practices to protect mission-critical systems from cyber threats. The rise of autonomous technologies and human-machine teaming requires specialized engineering expertise to integrate AI-driven decision-making into combat systems while ensuring operational safety and compliance. These innovations are not only increasing the effectiveness of military platforms but also transforming how defense forces plan, execute, and sustain missions in rapidly evolving operational environments.

Key Drivers in Aerospace & Defense Engineering Services Market:

The demand for military aerospace and defense engineering services is driven by a combination of strategic, operational, and technological factors. One of the primary drivers is the global push for defense modernization, where nations are upgrading legacy systems and developing next-generation capabilities to address emerging threats. The rapid evolution of aerospace technologies, including hypersonic weapons, stealth platforms, and directed energy systems, requires continuous engineering innovation to ensure competitive military advantage. Increasing geopolitical tensions and shifting defense priorities are also prompting governments to invest in more resilient and adaptable defense systems, further boosting the need for specialized engineering expertise. The integration of unmanned platforms and autonomous systems into military operations demands new engineering approaches to ensure seamless interoperability with existing assets. Additionally, cost efficiency and sustainability concerns are pushing defense organizations to adopt advanced lifecycle management strategies, including predictive maintenance and modular platform designs. As military forces seek to optimize performance while managing budget constraints, outsourcing engineering services to specialized firms is becoming an attractive option. The growing complexity of multi-domain operations, where land, air, sea, space, and cyber warfare intersect, further underscores the critical role of engineering services in shaping modern defense strategies.

Regional Trends in Aerospace & Defense Engineering Services Market:

Regional trends in military aerospace and defense engineering services vary based on defense priorities, industrial capabilities, and geopolitical dynamics. In North America, particularly the United States, strong defense budgets and a robust defense industrial base drive significant investments in advanced engineering services. The focus is on next-generation fighter aircraft, missile defense systems, space-based military assets, and AI-driven warfare solutions. Europe is prioritizing collaborative defense programs, such as the Future Combat Air System (FCAS) and the Tempest fighter program, leading to increased demand for engineering expertise in avionics, propulsion, and stealth technology. The Asia-Pacific region is experiencing rapid growth, with China, India, Japan, and South Korea investing heavily in indigenous defense capabilities, including hypersonic weapons, advanced naval platforms, and autonomous systems. These nations are increasingly relying on local engineering expertise to develop and sustain their military assets. The Middle East continues to expand its aerospace and defense engineering footprint through strategic partnerships and investments in local manufacturing and sustainment capabilities. In Latin America and Africa, defense engineering services are gradually expanding through technology transfers and international collaborations, supporting the development of regional aerospace industries and improving the self-sufficiency of military forces.

Key Aerospace & Defense Engineering Services Program:

The European Commission has announced €60 million in funding for the Common Armoured Vehicle System (CAVS) project under the EDIRPA program (European Defense Industry Reinforcement Instrument through Joint Procurement). This ambitious initiative seeks to develop a modern, standardized armored vehicle to strengthen the operational capabilities of the armed forces in Finland, Latvia, Sweden, and Germany. The CAVS project aims to meet increasing demands for troop mobility and protection, while promoting defense collaboration and equipment standardization among European nations.

Table of Contents

Global Aerospace & Defense Engineering Services Market - Table of Contents

Global Aerospace & Defense Engineering Services market Report Definition

Global Aerospace & Defense Engineering Services market Segmentation

By Region

By Type

By Platform

By Application

Global Aerospace & Defense Engineering Services market Analysis for next 10 Years

The 10-year Global Aerospace & Defense Engineering Services market analysis would give a detailed overview of Global Aerospace & Defense Engineering Services market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Global Aerospace & Defense Engineering Services

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Aerospace & Defense Engineering Services market Forecast

The 10-year Global Aerospace & Defense Engineering Services market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Aerospace & Defense Engineering Services market Trends & Forecast

The regional Global Aerospace & Defense Engineering Services market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Access Control Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Global Aerospace & Defense Engineering Services market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Global Aerospace & Defense Engineering Services market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2025-2035

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2025-2035

- Table 18: Scenario Analysis, Scenario 1, By Type, 2025-2035

- Table 19: Scenario Analysis, Scenario 1, By Application, 2025-2035

- Table 20: Scenario Analysis, Scenario 1, By Platform, 2025-2035

- Table 21: Scenario Analysis, Scenario 2, By Region, 2025-2035

- Table 22: Scenario Analysis, Scenario 2, By Type, 2025-2035

- Table 23: Scenario Analysis, Scenario 2, By Application, 2025-2035

- Table 24: Scenario Analysis, Scenario 2, By Platform, 2025-2035

List of Figures

- Figure 1: Global Aerospace & Defense Engineering Services Market Forecast, 2025-2035

- Figure 2: Global Aerospace & Defense Engineering Services Market Forecast, By Region, 2025-2035

- Figure 3: Global Aerospace & Defense Engineering Services Market Forecast, By Type, 2025-2035

- Figure 4: Global Aerospace & Defense Engineering Services Market Forecast, By Application, 2025-2035

- Figure 5: Global Aerospace & Defense Engineering Services Market Forecast, By Platform, 2025-2035

- Figure 6: North America, Aerospace & Defense Engineering Services Market, Market Forecast, 2025-2035

- Figure 7: Europe, Aerospace & Defense Engineering Services Market, Market Forecast, 2025-2035

- Figure 8: Middle East, Aerospace & Defense Engineering Services Market, Market Forecast, 2025-2035

- Figure 9: APAC, Aerospace & Defense Engineering Services Market, Market Forecast, 2025-2035

- Figure 10: South America, Aerospace & Defense Engineering Services Market, Market Forecast, 2025-2035

- Figure 11: United States, Aerospace & Defense Engineering Services Market, Technology Maturation, 2025-2035

- Figure 12: United States, Aerospace & Defense Engineering Services Market, Market Forecast, 2025-2035

- Figure 13: Canada, Aerospace & Defense Engineering Services Market, Technology Maturation, 2025-2035

- Figure 14: Canada, Aerospace & Defense Engineering Services Market, Market Forecast, 2025-2035

- Figure 15: Italy, Aerospace & Defense Engineering Services Market, Technology Maturation, 2025-2035

- Figure 16: Italy, Aerospace & Defense Engineering Services Market, Market Forecast, 2025-2035

- Figure 17: France, Aerospace & Defense Engineering Services Market, Technology Maturation, 2025-2035

- Figure 18: France, Aerospace & Defense Engineering Services Market, Market Forecast, 2025-2035

- Figure 19: Germany, Aerospace & Defense Engineering Services Market, Technology Maturation, 2025-2035

- Figure 20: Germany, Aerospace & Defense Engineering Services Market, Market Forecast, 2025-2035

- Figure 21: Netherlands, Aerospace & Defense Engineering Services Market, Technology Maturation, 2025-2035

- Figure 22: Netherlands, Aerospace & Defense Engineering Services Market, Market Forecast, 2025-2035

- Figure 23: Belgium, Aerospace & Defense Engineering Services Market, Technology Maturation, 2025-2035

- Figure 24: Belgium, Aerospace & Defense Engineering Services Market, Market Forecast, 2025-2035

- Figure 25: Spain, Aerospace & Defense Engineering Services Market, Technology Maturation, 2025-2035

- Figure 26: Spain, Aerospace & Defense Engineering Services Market, Market Forecast, 2025-2035

- Figure 27: Sweden, Aerospace & Defense Engineering Services Market, Technology Maturation, 2025-2035

- Figure 28: Sweden, Aerospace & Defense Engineering Services Market, Market Forecast, 2025-2035

- Figure 29: Brazil, Aerospace & Defense Engineering Services Market, Technology Maturation, 2025-2035

- Figure 30: Brazil, Aerospace & Defense Engineering Services Market, Market Forecast, 2025-2035

- Figure 31: Australia, Aerospace & Defense Engineering Services Market, Technology Maturation, 2025-2035

- Figure 32: Australia, Aerospace & Defense Engineering Services Market, Market Forecast, 2025-2035

- Figure 33: India, Aerospace & Defense Engineering Services Market, Technology Maturation, 2025-2035

- Figure 34: India, Aerospace & Defense Engineering Services Market, Market Forecast, 2025-2035

- Figure 35: China, Aerospace & Defense Engineering Services Market, Technology Maturation, 2025-2035

- Figure 36: China, Aerospace & Defense Engineering Services Market, Market Forecast, 2025-2035

- Figure 37: Saudi Arabia, Aerospace & Defense Engineering Services Market, Technology Maturation, 2025-2035

- Figure 38: Saudi Arabia, Aerospace & Defense Engineering Services Market, Market Forecast, 2025-2035

- Figure 39: South Korea, Aerospace & Defense Engineering Services Market, Technology Maturation, 2025-2035

- Figure 40: South Korea, Aerospace & Defense Engineering Services Market, Market Forecast, 2025-2035

- Figure 41: Japan, Aerospace & Defense Engineering Services Market, Technology Maturation, 2025-2035

- Figure 42: Japan, Aerospace & Defense Engineering Services Market, Market Forecast, 2025-2035

- Figure 43: Malaysia, Aerospace & Defense Engineering Services Market, Technology Maturation, 2025-2035

- Figure 44: Malaysia, Aerospace & Defense Engineering Services Market, Market Forecast, 2025-2035

- Figure 45: Singapore, Aerospace & Defense Engineering Services Market, Technology Maturation, 2025-2035

- Figure 46: Singapore, Aerospace & Defense Engineering Services Market, Market Forecast, 2025-2035

- Figure 47: United Kingdom, Aerospace & Defense Engineering Services Market, Technology Maturation, 2025-2035

- Figure 48: United Kingdom, Aerospace & Defense Engineering Services Market, Market Forecast, 2025-2035

- Figure 49: Opportunity Analysis, Aerospace & Defense Engineering Services Market, By Region (Cumulative Market), 2025-2035

- Figure 50: Opportunity Analysis, Aerospace & Defense Engineering Services Market, By Region (CAGR), 2025-2035

- Figure 51: Opportunity Analysis, Aerospace & Defense Engineering Services Market, By Type (Cumulative Market), 2025-2035

- Figure 52: Opportunity Analysis, Aerospace & Defense Engineering Services Market, By Type (CAGR), 2025-2035

- Figure 53: Opportunity Analysis, Aerospace & Defense Engineering Services Market, By Application (Cumulative Market), 2025-2035

- Figure 54: Opportunity Analysis, Aerospace & Defense Engineering Services Market, By Application (CAGR), 2025-2035

- Figure 55: Opportunity Analysis, Aerospace & Defense Engineering Services Market, By Platform (Cumulative Market), 2025-2035

- Figure 56: Opportunity Analysis, Aerospace & Defense Engineering Services Market, By Platform (CAGR), 2025-2035

- Figure 57: Scenario Analysis, Aerospace & Defense Engineering Services Market, Cumulative Market, 2025-2035

- Figure 58: Scenario Analysis, Aerospace & Defense Engineering Services Market, Global Market, 2025-2035

- Figure 59: Scenario 1, Aerospace & Defense Engineering Services Market, Total Market, 2025-2035

- Figure 60: Scenario 1, Aerospace & Defense Engineering Services Market, By Region, 2025-2035

- Figure 61: Scenario 1, Aerospace & Defense Engineering Services Market, By Type, 2025-2035

- Figure 62: Scenario 1, Aerospace & Defense Engineering Services Market, By Application, 2025-2035

- Figure 63: Scenario 1, Aerospace & Defense Engineering Services Market, By Platform, 2025-2035

- Figure 64: Scenario 2, Aerospace & Defense Engineering Services Market, Total Market, 2025-2035

- Figure 65: Scenario 2, Aerospace & Defense Engineering Services Market, By Region, 2025-2035

- Figure 66: Scenario 2, Aerospace & Defense Engineering Services Market, By Type, 2025-2035

- Figure 67: Scenario 2, Aerospace & Defense Engineering Services Market, By Application, 2025-2035

- Figure 68: Scenario 2, Aerospace & Defense Engineering Services Market, By Platform, 2025-2035

- Figure 69: Company Benchmark, Aerospace & Defense Engineering Services Market, 2025-2035

全球國防機油冷卻系統市場:2026-2036年

全球國防機油冷卻系統市場:2026-2036年 2026年全球航太和國防領域無損檢測(NDT)市場報告2026年全球航太與國防市場報告2026年航太和國防領域量子運算全球市場報告2026年全球航太和國防溫度控管系統市場報告

2026年全球航太和國防領域無損檢測(NDT)市場報告2026年全球航太與國防市場報告2026年航太和國防領域量子運算全球市場報告2026年全球航太和國防溫度控管系統市場報告 航太與國防領域虛擬實境(VR)市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034年預測全球航太與國防市場規模、佔有率、趨勢及成長分析報告(2026-2034)

航太與國防領域虛擬實境(VR)市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034年預測全球航太與國防市場規模、佔有率、趨勢及成長分析報告(2026-2034) 2025-2029年全球航太和國防領域的人工智慧(AI)和機器人技術

2025-2029年全球航太和國防領域的人工智慧(AI)和機器人技術 GMIPulse -航太與國防市場情報訂閱

GMIPulse -航太與國防市場情報訂閱 航太和國防市場:按產業和地區分類

航太和國防市場:按產業和地區分類