|

市場調查報告書

商品編碼

2073649

綠色物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Green Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

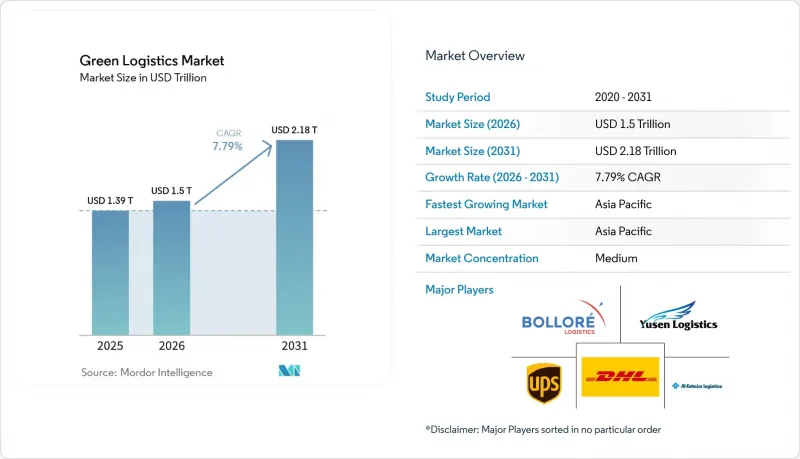

據 Mordor Intelligence 稱,2025 年綠色物流市場價值 1.39 兆美元,預計到 2031 年將達到 2.18 兆美元,而 2026 年為 1.5 兆美元,預測期(2026-2031 年)複合年成長率為 7.79%。

本報告按最終用戶(零售及電商、製造及工業、汽車、醫療保健及製藥、食品飲料等)、服務類型(倉儲、運輸、附加價值服務)和地區(北美、南美、亞太、歐洲、中東和非洲)對行業進行分類。市場預測以美元計價。

全球綠色物流市場趨勢與洞察

整個供應鏈的淨零排放強制性要求正在嚴格執行。

歐盟永續性報告指令和加州先進清潔卡車法規等資訊揭露要求,迫使貨運公司將碳排放標準納入競標,加速了對經認證的低排放服務的需求。 DHL的目標是到2030年實現30%的永續航空燃料(SAF)摻混比例,而UPS計劃在2050年實現其整個機隊的碳中和。採購負責人現在將高達3%的物流預算分配給與合規相關的脫碳項目,而排放績效正成為贏得合約的關鍵因素。能夠提供可審計數據的供應商在獲得路線合約方面享有先發優勢,尤其是在歐盟和美國的貿易路線上。無法提供可靠藍圖的承運商最快可能在2027年就被從首選供應商名單中移除。

電子商務的快速發展正在加速低碳最後一公里解決方案的開發。

小包裹量的激增導致排放集中在人口稠密的都市區,促使市政當局實施零排放區和堵塞收費。人工智慧驅動的電動貨車路線最佳化技術已在歐洲主要城市將配送時間縮短了15%至20%,同時二氧化碳排放降低了高達40%。像Maas這樣的零售商與Einride合作,資助部署300輛8級電動卡車,目標是到2030年每年減少2萬噸排放。儘管消費者支付溢價的意願仍然較低,但監管獎勵和品牌舉措正使「綠色配送」成為綠色物流市場的標準選項。

對零排放車輛和基礎設施進行大量初期投資。

雖然純電動卡車的購置溢價在每輛7萬至11.3萬美元之間,但專用電動公路項目若配備兆瓦級充電樁,每公里成本可能超過310萬美元。小規模運輸公司面臨資金籌措難題,殘值的不確定性也持續阻礙以二手車轉售為基礎的資金籌措模式。儘管營運成本降低的效益會隨著時間的推移而累積,但短期現金流壓力阻礙了綠色融資機制尚未完善的新興經濟體大規模採用電動卡車。

細分市場分析

到2025年,製造業和工業貨運商將佔綠色物流市場26.20%的佔有率,這反映了他們數十年來形成的合規文化和可預測的運輸模式,從而簡化了排放審計。這些公司已建立的供應商評估體系進一步鞏固了其市場佔有率優勢,因為貨運預算會分配給那些擁有基於資產的脫碳藍圖的供應商。高能耗工廠正擴大協商結合再生能源和電動卡車的綜合方案,並承諾多年減少碳排放。目前規模較小的零售和電子商務產業正以17.35%的複合年成長率快速成長,這主要得益於都市區微型倉配中心和大都會圈強制性零排放配送時段的推動。隨著退貨量的增加以及企業將「免費」配送的成本內部化,電子商務貨運的綠色物流市場預計將迅速擴張。同時,汽車製造商正在試行電動車運輸,以期將每輛車的物流排放減少40%。此外,醫療保健相關企業正在共同投資永續航空燃料 (SAF) 走廊,以確保低溫運輸的完整性,同時不增加碳排放強度。

電動車、標準化托盤和數位化載貨證券系統的日益普及,使製造商能夠可視化其「從生產到工廠」的碳足跡,從而實現持續最佳化。同時,電子商務企業正利用人工智慧整合宅配櫃、自行車宅配和暗店網路,以消除配送失敗。這兩種模式都依賴以數據為中心的績效儀表板,將排放排放轉化為具有競爭力的採購指標,展現了多元化的終端用戶如何加速綠色物流市場的成長。

區域分析

預計到2025年,亞太地區將以36.65%的銷售額佔有率引領綠色物流市場,並有望以8.62%的複合年成長率(CAGR)實現最快成長,直至2031年。在中國,由於全國綠色貨運走廊的建設和對8級電動卡車的補貼,車輛現代化正在加速。同時,印度正充分利用新建的工業園區,從一開始就將屋頂太陽能發電和電動車充電設施納入其中。日本正持續推動貨運鐵路現代化,並擴大模式轉換計劃,以緩解公路擁塞並減少物流領域的二氧化碳排放。東南亞國家正利用技術轉讓,透過將電池更換和微電網解決方案整合到港口擴建計畫中,大幅提升現有基礎設施。

北美仍是全球第二大貢獻地區,這得益於美國聯邦政府設定的目標:到2040年實現卡車銷售100%為零排放車輛(ZEV),以及大幅降低7級和8級電動卡車購買成本的稅額扣抵。加州的「先進清潔卡車」規則已強制要求汽車製造商逐步提高零排放車輛的銷售配額,並正在加快在I-5和I-10沿線部署充電站。在加拿大,將於2024年6月生效的《綠色清洗法案》將對誤導性的環境聲明處以最高1000萬加元的罰款,迫使運輸商披露可審計的資訊。同時,墨西哥正在推動「綠色邊境」計劃,以統一南北貿易路線的排放標準。

歐洲擁有世界上最完善的政策組合之一,包括碳定價、電動公路試點計畫以及2030年重型卡車二氧化碳排放強制性減少43%的規定,這使得零排放貨運成為一項監管確定性目標。瑞典的電動公路網路到2025年將擴展到50多公里,其營運績效數據指南德國在全國的推廣。物流公司正在採用低碳車輛,以此作為業務永續營運的必要條件。 CEVA公司新增的23輛電動卡車使其每年二氧化碳排放減少了38,300噸,而整合的充電網路則確保了運作。儘管東歐的運輸路線在基礎設施方面較為落後,但在歐盟用於綠色走廊建設的凝聚基金的支持下,預計到本世紀末,這些路線將實現一體化。

中東和非洲地區雖然仍處於發展初期,但正快速推進。阿拉伯聯合大公國的「2050年淨零排放策略」正在支持傑貝阿里建設一座太陽能物流園區;沙烏地阿拉伯則將綠氫能試點計畫與利雅德-吉達走廊的貨運試驗結合。南非的碳排放稅鼓勵運輸公司轉向生質柴油混合燃料,但電網可靠性方面的挑戰正在減緩車輛電氣化的普及。整體而言,各地區的情況不盡相同,當地的政策獎勵、基礎建設和產業基礎將決定綠色物流的普及速度,但目前每個地區都在推進一些關鍵項目,這些項目正展現出綠色物流市場不可逆轉的發展勢頭。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 全球供應鏈正在加強淨零排放義務。

- 電子商務的快速發展正在加速對低碳最後一公里解決方案的需求。

- 電池電動卡車和燃料電池卡車的成本迅速下降。

- 利用人工智慧最佳化路線和負載容量,從而減少排放。

- 在重型貨運路線上引入電動道路系統

- 一種將碳減排效果貨幣化的新型「綠色即服務」合約模式。

- 市場限制因素

- 對零排放車輛和基礎設施的高額初始資本投資

- 全球碳排放報告和綠色燃料標準有差異

- 除主要路線外,其他路線缺乏充電和環保燃料基礎設施。

- 與ESG「綠色清洗」指控相關的訴訟和處罰案件增加

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按最終用戶分類(價值,十億美元)

- 零售與電子商務

- 製造業和工業

- 車

- 醫療和藥品

- 食品/飲料

- 化學品和危險物質

- 其他

- 按服務類型

- 倉庫/存儲

- 運輸

- 路

- 鐵路

- 海路和內河航道

- 航空

- 附加價值服務(包裝、套件組裝、貼標)

- 地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 秘魯

- 智利

- 阿根廷

- 其他南美國家

- 亞太地區

- 印度

- 中國

- 日本

- 澳洲

- 韓國

- 東南亞(新加坡、馬來西亞、泰國、印尼、越南、菲律賓)

- 其他亞太國家

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 比荷盧經濟聯盟(比利時、荷蘭、盧森堡)

- 北歐國家(丹麥、芬蘭、冰島、挪威、瑞典)

- 其他歐洲國家

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- DHL Group

- United Parcel Service(UPS)

- FedEx Corporation

- GEODIS

- Hellmann Worldwide Logistics

- Kuehne+Nagel International AG

- Nippon Express

- CEVA Logistics

- XPO Logistics

- DSV A/S

- Yusen Logistics Co., Ltd.

- Bollore Logistics

- Al-Futtaim Logistics

- Mahindra Logistics Ltd.

- Americold Logistics

- GXO Logistics

- CH Robinson Worldwide, Inc.

- Lineage Logistics

- JD Logistics

- Ryder System, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the green logistics market size was valued at USD 1.39 trillion in 2025 and estimated to grow from USD 1.5 trillion in 2026 to reach USD 2.18 trillion by 2031, at a CAGR of 7.79% during the forecast period (2026-2031).

This report Segments the Industry Into by End User (Retail and E-Commerce, Manufacturing & Industrial, Automotive, Healthcare & Pharmaceuticals, Food & Beverages, and More), by Service Type (Warehousing & Storage, Transportation, and Value-Added Services), and by Geography (North America, South America, Asia-Pacific, Europe, and Middle East & Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Green Logistics Market Trends and Insights

Net-zero mandates tightening across supply chains

Mandatory disclosure rules such as the EU Corporate Sustainability Reporting Directive and California's Advanced Clean Truck regulation are forcing shippers to embed carbon criteria into bids, accelerating demand for certified low-emission services. DHL already targets 30% sustainable aviation fuel (SAF) blending by 2030, while UPS plans fleet-wide carbon neutrality by 2050. Procurement leaders now allocate up to 3% of logistics budgets to compliance-linked decarbonization projects, turning emissions performance into a contract-winning differentiator. Providers showing audit-ready data enjoy first-mover advantages in lane awards, especially on EU-US trade flows. Absent credible roadmaps, carriers risk exclusion from preferred supplier lists as early as 2027.

E-commerce boom accelerating low-carbon last-mile solutions

Spiking parcel volumes concentrate emissions in dense urban nodes, where municipalities deploy zero-emission zones and congestion pricing. AI-guided routing of electric vans has cut delivery times by 15-20% while lowering CO2 by as much as 40% in large European capitals. Retailers such as Mars are co-funding 300 electric Class 8 trucks with Einride, targeting 20,000 t annual reductions by 2030. Although consumer willingness to pay premiums remains muted, regulatory incentives and brand commitments are pushing "green delivery" toward default status in the green logistics market.

High upfront capex for zero-emission fleets & infrastructure

Purchase premiums on battery-electric trucks range from USD 70,000-113,000 per unit, while megawatt chargers can exceed USD 3.1 million per kilometer on dedicated electric-road projects. Smaller carriers struggle to secure financing, and uncertainty over residual values still dampens resale-based funding models. Although operating savings accumulate over time, near-term cash-flow strain hinders scale adoption in emerging economies lacking green credit facilities.

Other drivers and restraints analyzed in the detailed report include:

- Rapid cost declines in battery-electric & fuel-cell trucks

- AI-enabled route & load optimization, cutting emissions

- Limited charging & green-fuel infrastructure outside Tier-1 routes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Manufacturing & industrial shippers accounted for 26.20% of the green logistics market in 2025, reflecting decades-long compliance cultures and predictable shipping patterns that simplify emissions auditing. Their embedded supplier scorecards channel freight budgets toward providers with asset-based decarbonization roadmaps, reinforcing share dominance. Energy-intensive plants increasingly negotiate integrated renewable power and electric truck packages that lock in multiyear carbon reductions. Retail & e-commerce, though smaller today, is advancing at an 17.35% CAGR, propelled by urban micro-fulfilment centers and mandated zero-emission delivery windows in metropolitan zones. The green logistics market size for e-commerce shipments is set to climb sharply as returns volumes swell and merchants internalize the cost of "free" delivery. Automotive OEMs, meanwhile, trial electric car carriers to cut distribution emissions by 40% per unit, while healthcare brands co-invest in SAF corridors to safeguard cold-chain integrity without raising carbon intensity.

Electric-vehicle density, standardized pallets, and digitized bill-of-lading systems grant manufacturers visibility into cradle-to-gate footprints, enabling continuous optimization. In contrast, e-commerce operators leverage AI to orchestrate parcel lockers, bike couriers, and dark-store networks that eliminate failed delivery attempts. Both archetypes converge on data-centric performance dashboards that convert emissions tracking into a competitive procurement variable, illustrating how diverse end users amplify growth in the green logistics market.

Complete Report Scope:

- By End User (Value, USD Bn)

- Retail & E-commerce

- Manufacturing & Industrial

- Automotive

- Healthcare & Pharmaceuticals

- Food & Beverages

- Chemicals & Hazardous Materials

- Others

- By Service Type (Value)

- Warehousing and Storage

- Transportation

- Road

- Rail

- Sea and Inland Waterways

- Air

- Value-Added Services (Packaging, Kitting, Labelling)

- Geography (Value)

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

- Middle East And Africa

- United Arab of Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East And Africa

- North America

Geography Analysis

APAC led the green logistics market with a 36.65% revenue share in 2025 and is growing fastest at 8.62% CAGR through 2031. China's nationwide green-freight corridors and subsidies for electric Class 8 trucks accelerate fleet turnover, while India leverages new-build industrial parks to embed rooftop PV and EV charging from inception . Japan continues to modernize freight rail, expanding its modal shift program to lower highway congestion and cut logistics CO2. Southeast Asian nations capitalize on technology transfer, integrating battery swapping and microgrid solutions into port expansions to leapfrog legacy infrastructure.

North America remains the second-largest regional contributor, buoyed by the US federal target for 100% zero-emission truck sales by 2040 and tax credits that slash acquisition costs on Class 7-8 electrics. California's Advanced Clean Truck rule already compels OEMs to meet escalating ZEV sales quotas, driving early deployment of charging hubs across I-5 and I-10 corridors. Canada's anti-greenwashing legislation, effective June 2024, imposes fines up to CAD 10 million for misleading environmental claims, pushing carriers toward audit-ready disclosures, while Mexico promotes green-border programs that synchronize emissions standards on North-South trade routes.

Europe enjoys the world's most sophisticated policy mix-carbon pricing, eHighway pilots, and 43% CO2 cut mandates for heavy trucks by 2030-making zero-emission freight a regulatory certainty. Sweden's electric road classes expanded to over 50 km in 2025, generating performance data that informs Germany's national rollout. Logistics firms deploy low-carbon fleets as a licence-to-operate; CEVA's addition of 23 electric trucks curbs 38,300 t of CO2 annually, while integrated charging networks protect uptime. Eastern European lanes, though lagging infrastructure, attract EU cohesion funds earmarked for green corridors, promising convergence by the end of the decade.

The Middle East and Africa are nascent but rapidly mobilizing. The UAE's Net Zero 2050 Strategy backs solar-powered logistics parks at Jebel Ali, and Saudi Arabia links green hydrogen pilots to freight trials on the Riyadh-Jeddah corridor. South Africa's carbon tax nudges carriers toward biodiesel blends, yet grid reliability challenges slow widespread fleet electrification. Overall, regional heterogeneity ensures that localized policy incentives, infrastructure readiness, and industrial baselines dictate adoption speed, but each geography now features anchor projects that signal irreversible momentum in the green logistics market.

- DHL Group

- United Parcel Service (UPS)

- FedEx Corporation

- GEODIS

- Hellmann Worldwide Logistics

- Kuehne + Nagel International AG

- Nippon Express

- CEVA Logistics

- XPO Logistics

- DSV A/S

- Yusen Logistics Co., Ltd.

- Bollore Logistics

- Al-Futtaim Logistics

- Mahindra Logistics Ltd.

- Americold Logistics

- GXO Logistics

- C.H. Robinson Worldwide, Inc.

- Lineage Logistics

- JD Logistics

- Ryder System, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Net-zero mandates tightening across global supply chains

- 4.2.2 E-commerce boom accelerating demand for low-carbon last-mile solutions

- 4.2.3 Rapid cost declines in battery-electric & fuel-cell trucks

- 4.2.4 AI-enabled route & load optimisation cutting emissions

- 4.2.5 Roll-out of electric road systems on heavy-freight corridors

- 4.2.6 Emerging "Green-as-a-Service" contractual models monetising carbon savings

- 4.3 Market Restraints

- 4.3.1 High upfront capex for zero-emission fleets & infrastructure

- 4.3.2 Fragmented global standards for carbon reporting & green fuels

- 4.3.3 Limited charging & green-fuel infrastructure outside Tier-1 routes

- 4.3.4 Rising litigation/penalties linked to ESG-greenwashing claims

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By End User (Value, USD Bn)

- 5.1.1 Retail & E-commerce

- 5.1.2 Manufacturing & Industrial

- 5.1.3 Automotive

- 5.1.4 Healthcare & Pharmaceuticals

- 5.1.5 Food & Beverages

- 5.1.6 Chemicals & Hazardous Materials

- 5.1.7 Others

- 5.2 By Service Type (Value)

- 5.2.1 Warehousing and Storage

- 5.2.2 Transportation

- 5.2.2.1 Road

- 5.2.2.2 Rail

- 5.2.2.3 Sea and Inland Waterways

- 5.2.2.4 Air

- 5.2.3 Value-Added Services (Packaging, Kitting, Labelling)

- 5.3 Geography (Value)

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 South America

- 5.3.2.1 Brazil

- 5.3.2.2 Peru

- 5.3.2.3 Chile

- 5.3.2.4 Argentina

- 5.3.2.5 Rest of South America

- 5.3.3 Asia-Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.3.3.7 Rest of Asia-Pacific

- 5.3.4 Europe

- 5.3.4.1 United Kingdom

- 5.3.4.2 Germany

- 5.3.4.3 France

- 5.3.4.4 Spain

- 5.3.4.5 Italy

- 5.3.4.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.3.4.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.3.4.8 Rest of Europe

- 5.3.5 Middle East And Africa

- 5.3.5.1 United Arab of Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 South Africa

- 5.3.5.4 Nigeria

- 5.3.5.5 Rest of Middle East And Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 United Parcel Service (UPS)

- 6.4.3 FedEx Corporation

- 6.4.4 GEODIS

- 6.4.5 Hellmann Worldwide Logistics

- 6.4.6 Kuehne + Nagel International AG

- 6.4.7 Nippon Express

- 6.4.8 CEVA Logistics

- 6.4.9 XPO Logistics

- 6.4.10 DSV A/S

- 6.4.11 Yusen Logistics Co., Ltd.

- 6.4.12 Bollore Logistics

- 6.4.13 Al-Futtaim Logistics

- 6.4.14 Mahindra Logistics Ltd.

- 6.4.15 Americold Logistics

- 6.4.16 GXO Logistics

- 6.4.17 C.H. Robinson Worldwide, Inc.

- 6.4.18 Lineage Logistics

- 6.4.19 JD Logistics

- 6.4.20 Ryder System, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

美國綠色物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

美國綠色物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 綠色物流市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、部署、最終用戶及解決方案分類

綠色物流市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、部署、最終用戶及解決方案分類 2026年全球綠色物流市場報告

2026年全球綠色物流市場報告 2034年全球電動貨運和綠色物流走廊市場預測-按商業模式、運輸方式、走廊基礎設施、技術、最終用戶和區域分類的全球分析

2034年全球電動貨運和綠色物流走廊市場預測-按商業模式、運輸方式、走廊基礎設施、技術、最終用戶和區域分類的全球分析 綠色物流市場:按車隊遠端資訊處理、電動車充電基礎設施、類型和最終用途分類-全球預測,2026-2032年

綠色物流市場:按車隊遠端資訊處理、電動車充電基礎設施、類型和最終用途分類-全球預測,2026-2032年 2026-2030年全球綠色物流認證服務市場綠色物流市場預測至2032年:按組件、運輸方式、業務類型、最終用戶和地區分類的全球分析

2026-2030年全球綠色物流認證服務市場綠色物流市場預測至2032年:按組件、運輸方式、業務類型、最終用戶和地區分類的全球分析 全球綠色物流市場

全球綠色物流市場 印度綠色物流市場:依營運模式、業務類型、最終用途、地區、機會及預測,2019-2033日本的綠色物流市場:運用形態·業務類型·終端用戶·各地區的機會及預測 (2019-2033年)

印度綠色物流市場:依營運模式、業務類型、最終用途、地區、機會及預測,2019-2033日本的綠色物流市場:運用形態·業務類型·終端用戶·各地區的機會及預測 (2019-2033年)