|

市場調查報告書

商品編碼

2073631

半導體物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Semiconductor Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

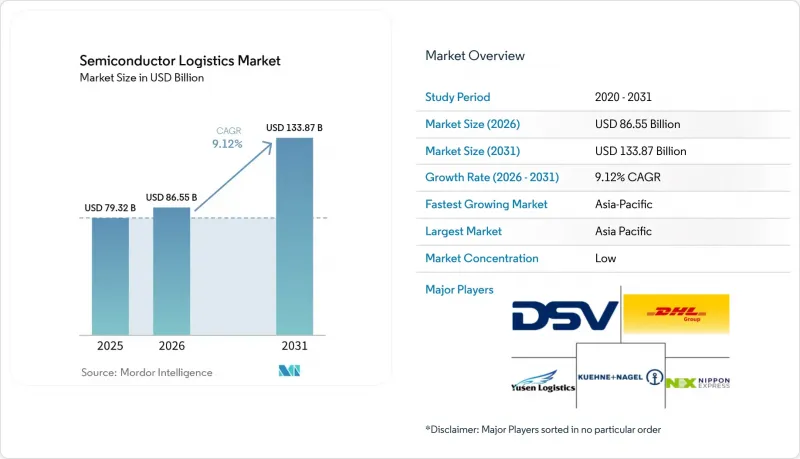

據 Mordor Intelligence 稱,2025 年半導體物流市場價值為 793.2 億美元,預計到 2031 年將達到 1338.7 億美元,而 2026 年為 865.5 億美元,預測期(2026-2031 年)的複合年成長率為 9.12%。

本報告按功能(運輸、倉儲配送及其他)、營運模式(低溫運輸物流、非低溫運輸物流)、目的地(國內、國際)、產品類型(原料及化學品及其他)及地區(北美、南美、亞太、歐洲、中東和非洲)進行細分。市場預測以美元計價。

全球半導體物流市場趨勢與洞察

美國和歐洲製造業加速擴張

2025年至2026年間,美洲、日本和歐洲計畫新建18座晶圓廠,這些計畫正在重塑全球物流格局。例如,台積電位於亞利桑那州的園區和英特爾在多個州的產能擴張項目,都需要一個無污染的卡車運輸網路,以嚴格的準時交付計劃運送超高純度氣體、光阻劑和晶圓盒。除了傳統的長途運輸路線外,連接晶圓廠、供應商物流中心和專用轉運設施的區域性「牛奶配送」路線也正在湧現。物流業者正在投資符合ISO 5級標準的拖車和車載顆粒物感測器,以滿足這些服務水準。房地產開發商正在鳳凰城、哥倫布和德勒斯登附近打造新的物流中心,以整合半導體級倉庫,縮短前置作業時間,並減少對空運的依賴。因此,對A級卡車和認證司機的需求激增,推動了半導體物流市場的蓬勃發展。

東南亞地區晶圓層次電子構裝外包業務正在迅速成長。

先進封裝技術的快速外包正在拓展連接馬來西亞、越南和菲律賓的點對點運輸路線。日月光半導體(ASE Technology)位於檳城的工廠已擴建至340萬平方英尺,目前擁有6,000名員工,使其溫度敏感基板的出口量增加了兩倍。安靠(Amkor)投資16億美元在北寧省的工廠新增了20萬平方米的無塵室空間,專門用於系統級封裝(SiP)模組的生產,從而增加了導線架、層壓板和底部填充劑等化學品的供應量。這些項目需要保稅倉庫、符合ISO 14001標準的地面運輸車輛以及全天候的報關服務,以管理區域退貨和部分出貨。東南亞各國政府正在簡化自由貿易區的監管,並在機場投資建造雙視角X光掃描儀,以加速半導體貨物的清關速度,進一步刺激半導體物流市場的發展。

A級無塵室所需的卡車和貨櫃供應緊張。

不斷湧現的製造項目公告已經超過了專用車輛的供應速度。配備無塵室的拖車製造商報告稱,訂單已超過18個月,而承運商則面臨ISO 5級內襯價格兩位數的上漲。一些托運人正在租用安裝在標準拖車內的可移動軟壁潔淨室作為臨時措施,但這種方案會使裝載作業複雜化並降低裝載效率。隨著新型先進製程節點的推出,顆粒濃度容差要求越來越嚴格,專用車輛的供需失衡持續限制半導體物流市場的發展。

細分市場分析

至2025年,運輸服務將佔半導體物流市場的58.93%。這是因為晶圓廠、OSAT(外包半導體加工測試)和OEM(原始設備製造商)都依賴及時、無污染地運輸高價值貨物。對於需要將交貨時間控制在一小時以內的區域航線,地面運輸佔據主導地位,以滿足工廠的即時補貨需求。同時,對於光掩模、EUV(極紫外光微影)設備和關鍵備件,專用貨機和包機航班確保了全球運輸能力。光是大韓航空就營運23架專用於半導體運輸的寬體貨機,佔該產業全球運輸能力的6%。這一細分市場的規模賦予了航空公司與機場和地面服務商就優先起降時刻和安全停機位進行談判的議價能力,進一步鞏固了其在半導體物流市場的主導地位。

附加價值服務呈現最高成長率,預計到2031年將以4.08%的複合年成長率成長,這主要得益於價值鏈日益複雜化,對清關、保稅倉儲和出口管制諮詢的需求不斷成長。提供包裝套件、靜電放電防護審核服務和廠外MRO(維修、維修和大修)補貨服務的供應商正與希望減少供應商數量的代工廠簽訂長期合約。隨著代工廠擴大非核心業務的外包,物流公司透過在現場部署技術人員並協調設備調配,獲得了高利潤的收入來源,並擺脫了低利潤的純運輸業務,實現了業務多元化。

至2025年,非低溫運輸服務將佔半導體物流市場規模的76.70%,涵蓋成品晶片、製造設備以及常溫儲存的主流材料。多模態樞紐整合了保稅倉庫和防靜電集散區,將運往不同地區的貨物集中起來,從而最佳化幹線運輸的經濟效益。同時,由於極紫外光光阻劑、特種氣體和先進聚合物對溫度控制有嚴格的要求,低溫運輸運輸的需求正以4.78%的複合年成長率快速成長。 DHL已投資20億歐元(約22億美元)建造符合GDP標準的樞紐,使其能夠抓住這一特殊領域的成長機遇,並緩解可能拖累半導體物流市場發展的重大運力瓶頸。

區域分析

預計到2025年,亞太地區將維持43.10%的市場佔有率,並在2031年之前以4.85%的複合年成長率引領區域成長,這主要得益於一體化的半導體生態系統和策略性的供應鏈多元化舉措。台積電在台灣晶圓代工產業中佔據主導地位,擁有54%的全球市場佔有率,並佔先進晶片產量的近90%,由此產生了大規模的物流流動,包括用於運輸極光刻(EUV)化學品的專用潔淨室運輸和溫控處理。韓國在記憶體領域的主導地位,由三星和SK海力士主導,隨著兩家公司擴大其HBM產能,也產生了龐大的物流量。三星計劃在2024年將產量提高2.5倍,而SK海力士正在高階儲存產品領域投資10兆韓元。在東南亞市場,隨著半導體公司業務多元化,成長正在加速,其中馬來西亞每年從半導體出口中獲得約1300億美元的收入。同時,越南正吸引大規模的封裝投資,其中包括安高集團在北寧省投資16億美元的工廠。預計該地區的物流基礎設施將面臨600億美元的投資缺口,以滿足未來的貿易需求。各國正努力改善交通基礎設施,並建立半導體物流中心,以維持競爭優勢。

北美正經歷強勁成長,這得益於政府前所未有的投資以及根據《晶片產業戰略法案》(CHIPS Act)527億美元的預算撥款推動的戰略性回流舉措。台積電在亞利桑那州的650億美元投資是美國歷史上最大的海外製造項目,三座晶圓廠創造了約6000個高科技就業崗位,並為先進半導體生產建立了一條新的國內物流走廊。英特爾在北美約900億美元的投資(其中85億美元來自《晶片產業戰略法案》)橫跨多個州,建構了一個服務於汽車、國防和人工智慧市場的綜合物流網路。儘管該地區受惠於完善的物流基礎設施和法律規範,但其營運成本高昂,建設成本比亞洲工廠高出約10%,營運成本則高出35%。英特爾致力於人才培養,包括利用《晶片產業戰略法案》撥款6500萬美元用於其培訓項目,這不僅有助於解決嚴重的技能短缺問題,同時也為半導體物流運營建立了一條永續的人才儲備庫。

歐洲正透過協調一致的產業政策和對半導體製造能力的大量公共投資,崛起為策略性成長市場。德國的「矽谷薩克森」地區是一體化生態系統的典範,而《歐洲晶片法案》旨在透過對國內製造業的戰略投資,到2030年將該地區的生產佔有率從少於10%提升至20%(德勤美國)。安森美半導體(ON Semiconductor,簡稱onsemi)在捷克共和國投資20億美元建造碳化矽(SiC)製造工廠就是一個重要的投資案例。該工廠將專注於生產用於電動車和可再生能源應用的節能半導體,預計每年可為捷克共和國創造超過2.7億美元的GDP(onsemi)。該地區的物流基礎設施受益於成熟的汽車供應鍊和法律規範,包括GDPR和環境認證。此外,DHL在醫療保健物流領域投資20億歐元(約22億美元),正在增強其在半導體化學品和材料運輸方面的專業能力。歐洲半導體物流的成長符合永續性要求和循環經濟原則,為綠色物流解決方案和碳中和運輸網路創造了機會。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 美國和歐洲製造業加速擴張

- 東南亞晶圓層次電子構裝業務激增

- 向鑄造廠附近的「牛奶配送」式物流模式過渡

- EUV微影術化學品的低溫運輸合規性

- 政府透過可信賴的合作夥伴為供應鏈提供補貼

- 基於人工智慧的動態路線規劃和預計到達時間(ETA)視覺化平台

- 市場限制因素

- A級無塵室所需的卡車和貨櫃供應緊張。

- 包租貨船噴射機燃料額外費用的波動

- 經認證的危險物品/靜電放電防護訓練畢業生長期短缺

- 出口中國設備的許可證審核延誤

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 新冠疫情和地緣政治動盪的影響

第5章 市場規模與成長預測

- 按功能

- 運輸

- 路

- 鐵路

- 水路和海路

- 航路

- 倉儲/物流

- 附加價值服務(包裝、清關、經紀等)

- 運輸

- 透過操作模式

- 低溫運輸物流

- 非低溫運輸物流

- 目的地

- 國內的

- 國際的

- 依產品類型

- 原料和化學品

- 晶圓(未加工和已加工)

- 包裝材料

- 成品半導體產品

- 其他物品(光罩和分劃板、特殊耗材等)

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 秘魯

- 智利

- 阿根廷

- 其他南美國家

- 亞太地區

- 印度

- 中國

- 日本

- 澳洲

- 韓國

- 東南亞(新加坡、馬來西亞、泰國、印尼、越南、菲律賓)

- 其他亞太國家

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 比荷盧經濟聯盟(比利時、荷蘭、盧森堡)

- 北歐國家(丹麥、芬蘭、冰島、挪威、瑞典)

- 其他歐洲國家

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- DHL Supply Chain and Global Forwarding

- Kuehne+Nagel

- Nippon Express

- DSV

- Yusen Logistics

- UPS Supply Chain Solutions

- FedEx Logistics

- CEVA Logistics

- Omni Logistics

- Dimerco

- NNR Global Logistics

- MOL Logistics

- AIT Worldwide Logistics

- Kintetsu World Express, Inc.

- Logistics Plus Inc.

- CCS-Express

- Buske Logistics

- K Line Logistics

- Javelin Logistics Company, Inc.

- Three Way Logistics

第7章 市場機會與未來展望

According to Mordor Intelligence, the semiconductor logistics market size was valued at USD 79.32 billion in 2025 and estimated to grow from USD 86.55 billion in 2026 to reach USD 133.87 billion by 2031, at a CAGR of 9.12% during the forecast period (2026-2031).

This report is Segmented by Function (Transportation, Warehousing & Distribution, and More), Mode of Operation (Cold-Chain Logistics, Non-Cold-Chain Logistics), Destination (Domestic, International), Product Type (Raw Materials & Chemicals, and More), and Geography (North America, South America, Asia-Pacific, Europe, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Semiconductor Logistics Market Trends and Insights

Accelerated Fab Expansion in the United States and Europe

Eighteen new fabs slated for 2025-2026 in the Americas, Japan, and Europe are reshaping global logistics corridors. Projects such as TSMC's Arizona campus and Intel's multi-state capacity expansions require contamination-free trucking networks to deliver ultra-high-purity gases, photoresists, and wafer pods on strict just-in-time schedules. Traditional long-haul routes are being supplemented by regional "milk-run" circuits that loop among fabs, supplier distribution centers, and specialized trans-load facilities. Logistics providers are investing in ISO Class 5-compatible trailers and on-board particulate sensing to meet these service levels. Real-estate developers are co-locating semiconductor-grade warehouses near Phoenix, Columbus, and Dresden, creating new nodes that shorten lead times and reduce air-freight reliance. The resulting demand surge for Class A trucks and certified drivers underpins a measurable uplift in the semiconductor logistics market.

Surging Wafer-Level Packaging Outsourcing in Southeast Asia

Rapid outsourcing of advanced packaging drives point-to-point lanes across Malaysia, Vietnam, and the Philippines. ASE Technology's Penang expansion to 3.4 million ft2 and 6,000 staff has tripled outbound shipments of temperature-sensitive substrates. Amkor's USD 1.6 billion Bac Ninh facility adds 200,000 m2 of clean-room space dedicated to system-in-package modules, amplifying inbound flows of lead frames, laminate, and under-fill chemicals. These projects demand bonded consolidation warehouses, ISO 14001-compliant road fleets, and 24/7 customs-broker desks to manage zone returns and partial shipments. Southeast Asian governments are streamlining free-trade-zone rules and investing in dual-view X-ray scanners at airports to accelerate clearance of semiconductor cargo, further stimulating the semiconductor logistics market.

Tight Capacity for Class A Clean-Room Trucks & Containers

Back-to-back fab announcements have outpaced specialty-fleet growth. Clean-room-equipped trailer builders report order backlogs exceeding 18 months, while operators face double-digit price inflation for ISO Class 5 liners. Some shippers charter mobile soft-wall clean rooms inside standard trailers as stop-gap measures, yet these solutions add loading complexity and reduce cube utilization. With every new advanced node requiring tighter particle thresholds, the supply-demand imbalance for specialty vehicles continues to constrain the semiconductor logistics market.

Other drivers and restraints analyzed in the detailed report include:

- AI-Enabled Dynamic Routing and ETA Visibility Platforms

- Government Subsidies for Trusted-Partner Supply Chains

- Persistent Shortage of Certified DG/ESD-Trained Manpower

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation services held 58.93% of the semiconductor logistics market in 2025 as fabs, OSATs, and OEMs depend on time-definite, contamination-free movement of high-value cargo. Road fleets dominate intra-regional lanes where just-in-time plant replenishment requires sub-hour transit precision, while dedicated freighters and charter flights secure global capacity for masks, EUV machines, and critical spares. Korean Air alone operates 23 wide-body freighters dedicated to semiconductors, equal to a 6% share of global capacity for this vertical. The segment's scale gives carriers bargaining power with airports and ground handlers for priority slots and secure-tarmac clearance, reinforcing its primacy within the semiconductor logistics market size.

Value-added services posted the fastest segmental CAGR of 4.08% through 2031 as supply-chain complexity raises demand for customs brokerage, bonded warehousing, and export-control consulting. Providers that offer packaging kitting, ESD audit services, and sub-fab MRO replenishment win long-term contracts from foundries keen to minimize vendor count. As fabs outsource more non-core activities, logistics firms embed technicians on-site to manage tool-move coordination, enabling higher-margin revenue streams and diversifying away from low-yield pure transportation.

Non-cold-chain services accounted for 76.70% of the semiconductor logistics market size in 2025, covering finished chips, tooling, and mainstream materials that tolerate ambient conditions. Multi-modal hubs integrate bonded warehouses with ESD-safe staging areas to aggregate loads bound for diverse geographies, optimizing line-haul economics. Yet demand for cold-chain lanes is rising swiftly at a 4.78% CAGR as EUV photoresists, specialty gases, and advanced polymers impose tight thermal envelopes. DHL's EUR 2 billion (USD 2.20 billion) investment in GDP-compliant hubs positions the firm to capture this specialized growth, easing a key capacity bottleneck that threatened to slow the semiconductor logistics market.

Complete Report Scope:

- By Function

- Transportation

- Roadways

- Railways

- Water and Seaways

- Airways

- Warehousing and Distribution

- Value-Added Services (Packaging, Customs, Brokerage, Others)

- Transportation

- By Mode of Operation

- Cold-Chain Logistics

- Non-Cold-Chain Logistics

- By Destination

- Domestic

- International

- By Product type

- Raw Materials and Chemicals

- Wafers (Bare and Processed)

- Packaging Materials

- Finished Semiconductor Products

- Others (Photo masks and reticles, Specialty consumables, etc.)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

- Middle East and Africa

- United Arab of Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East And Africa

- North America

Geography Analysis

Asia-Pacific maintains its dominant position with 43.10% market share in 2025 and leads regional growth at 4.85% CAGR through 2031, driven by its integrated semiconductor ecosystem and strategic supply chain diversification initiatives. Taiwan's foundry leadership, anchored by TSMC's 54% global market share and nearly 90% of advanced chip production, drives significant logistics flows that require specialized clean-room transportation and temperature-controlled handling for EUV chemicals. South Korea's memory dominance, led by Samsung and SK Hynix, is generating substantial logistics volumes as both expand HBM production, with Samsung increasing output 2.5 times in 2024 and SK Hynix investing KRW 10 trillion in high-end storage products. Southeast Asian markets are experiencing accelerated growth as semiconductor companies diversify operations, with Malaysia generating approximately USD 130 billion annually from semiconductor exports while Vietnam attracts major packaging investments like Amkor's USD 1.6 billion facility in Bac Ninh. The region's logistics infrastructure faces a projected USD 60 billion investment gap to meet future trade demands, with countries enhancing transport infrastructure and establishing specialized semiconductor logistics hubs to maintain competitive advantages.

North America demonstrates robust growth momentum driven by unprecedented government investment and strategic reshoring initiatives under the CHIPS Act's USD 52.7 billion allocation. TSMC's USD 65 billion Arizona investment represents the largest foreign manufacturing project in U.S. history, with three fabs creating approximately 6,000 high-tech jobs and establishing new domestic logistics corridors for advanced semiconductor production. Intel's nearly USD 90 billion domestic investment spans multiple states, supported by USD 8.5 billion in CHIPS funding, and is creating integrated logistics networks that serve automotive, defense, and AI markets. The region benefits from established logistics infrastructure and regulatory frameworks, though faces higher operational costs with U.S. facilities costing approximately 10% more to build and up to 35% higher operating costs compared to Asian counterparts. Workforce development initiatives, including Intel's USD 65 million CHIPS funding for training programs, address critical skills shortages while establishing sustainable talent pipelines for semiconductor logistics operations.

Europe emerges as a strategic growth market through coordinated industrial policy and substantial public investment in semiconductor manufacturing capabilities. Germany's Silicon Saxony region serves as a model integrated ecosystem, while the European Chips Act targets increasing regional production from sub-10% to 20% by 2030 through strategic investments in domestic manufacturing Deloitte US. Major investments include onsemi's USD 2 billion silicon carbide facility in the Czech Republic, targeting energy-efficient semiconductors for electric vehicles and renewable energy applications, with potential to generate over USD 270 million annually for Czech GDP onsemi. The region's logistics infrastructure benefits from established automotive supply chains and regulatory frameworks including GDPR and environmental certifications, while DHL's EUR 2 billion (USD 2.20 billion) health logistics investment enhances specialized transportation capabilities for semiconductor chemicals and materials. European semiconductor logistics growth aligns with sustainability mandates and circular economy principles, creating opportunities for green logistics solutions and carbon-neutral transportation networks.

List of Companies Covered in this Report:

- DHL Supply Chain and Global Forwarding

- Kuehne + Nagel

- Nippon Express

- DSV

- Yusen Logistics

- UPS Supply Chain Solutions

- FedEx Logistics

- CEVA Logistics

- Omni Logistics

- Dimerco

- NNR Global Logistics

- MOL Logistics

- AIT Worldwide Logistics

- Kintetsu World Express, Inc.

- Logistics Plus Inc.

- CCS-Express

- Buske Logistics

- K Line Logistics

- Javelin Logistics Company, Inc.

- Three Way Logistics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated fab expansion in the United States and Europe

- 4.2.2 Surging wafer-level packaging outsourcing in Southeast Asia

- 4.2.3 Shift toward near-foundry "milk-run" logistics models

- 4.2.4 Cold-chain compliance for EUV photolithography chemicals

- 4.2.5 Government subsidies for trusted-partner supply chains

- 4.2.6 AI-enabled dynamic routing and ETA visibility platforms

- 4.3 Market Restraints

- 4.3.1 Tight capacity for Class A clean-room trucks and containers

- 4.3.2 Volatile jet-fuel surcharges on chartered freighters

- 4.3.3 Persistent shortage of certified DG/ESD-trained manpower

- 4.3.4 Export-control licensing delays for China-bound tools

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of COVID-19 and Geopolitical Disruptions

5 Market Size and Growth Forecasts (Value)

- 5.1 By Function

- 5.1.1 Transportation

- 5.1.1.1 Roadways

- 5.1.1.2 Railways

- 5.1.1.3 Water and Seaways

- 5.1.1.4 Airways

- 5.1.2 Warehousing and Distribution

- 5.1.3 Value-Added Services (Packaging, Customs, Brokerage, Others)

- 5.1.1 Transportation

- 5.2 By Mode of Operation

- 5.2.1 Cold-Chain Logistics

- 5.2.2 Non-Cold-Chain Logistics

- 5.3 By Destination

- 5.3.1 Domestic

- 5.3.2 International

- 5.4 By Product type

- 5.4.1 Raw Materials and Chemicals

- 5.4.2 Wafers (Bare and Processed)

- 5.4.3 Packaging Materials

- 5.4.4 Finished Semiconductor Products

- 5.4.5 Others (Photo masks and reticles, Specialty consumables, etc.)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Peru

- 5.5.2.3 Chile

- 5.5.2.4 Argentina

- 5.5.2.5 Rest of South America

- 5.5.3 Asia-Pacific

- 5.5.3.1 India

- 5.5.3.2 China

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.5.3.7 Rest of Asia-Pacific

- 5.5.4 Europe

- 5.5.4.1 United Kingdom

- 5.5.4.2 Germany

- 5.5.4.3 France

- 5.5.4.4 Spain

- 5.5.4.5 Italy

- 5.5.4.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.5.4.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.5.4.8 Rest of Europe

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab of Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East And Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 DHL Supply Chain and Global Forwarding

- 6.4.2 Kuehne + Nagel

- 6.4.3 Nippon Express

- 6.4.4 DSV

- 6.4.5 Yusen Logistics

- 6.4.6 UPS Supply Chain Solutions

- 6.4.7 FedEx Logistics

- 6.4.8 CEVA Logistics

- 6.4.9 Omni Logistics

- 6.4.10 Dimerco

- 6.4.11 NNR Global Logistics

- 6.4.12 MOL Logistics

- 6.4.13 AIT Worldwide Logistics

- 6.4.14 Kintetsu World Express, Inc.

- 6.4.15 Logistics Plus Inc.

- 6.4.16 CCS-Express

- 6.4.17 Buske Logistics

- 6.4.18 K Line Logistics

- 6.4.19 Javelin Logistics Company, Inc.

- 6.4.20 Three Way Logistics

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

半導體元件清洗市場:依清潔劑、清洗設備、產業、清洗製程、材料類型、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測半導體及電路製造市場:依產品類型、應用、組件、晶圓尺寸、材料、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測

半導體元件清洗市場:依清潔劑、清洗設備、產業、清洗製程、材料類型、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測半導體及電路製造市場:依產品類型、應用、組件、晶圓尺寸、材料、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測 全球半導體晶片生態系統市場:機會與策略展望(至2035年)

全球半導體晶片生態系統市場:機會與策略展望(至2035年) 半導體產業:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

半導體產業:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026 年至 2035 年電氣金屬管材的市場機會、成長要素、產業趨勢分析與預測。半導體及相關裝置市場:全球產業分析、市場規模、市場佔有率及預測(2026-2033 年),依半導體類型、裝置類型、材料類型、技術、應用、國家及地區分類半導體智慧電網市場:按組件、功能、應用、最終用戶、國家和地區分類-行業分析、市場規模、市場佔有率和預測(2026-2033 年)

2026 年至 2035 年電氣金屬管材的市場機會、成長要素、產業趨勢分析與預測。半導體及相關裝置市場:全球產業分析、市場規模、市場佔有率及預測(2026-2033 年),依半導體類型、裝置類型、材料類型、技術、應用、國家及地區分類半導體智慧電網市場:按組件、功能、應用、最終用戶、國家和地區分類-行業分析、市場規模、市場佔有率和預測(2026-2033 年) 2026-2030年全球半導體市場

2026-2030年全球半導體市場 用於替代能源技術的半導體:機會和市場

用於替代能源技術的半導體:機會和市場 有機半導體市場:全球產業規模、市場佔有率、趨勢、機會和預測(按材料類型、應用和地區分類)、競爭格局(2021-2031 年)

有機半導體市場:全球產業規模、市場佔有率、趨勢、機會和預測(按材料類型、應用和地區分類)、競爭格局(2021-2031 年)