|

市場調查報告書

商品編碼

2071375

2026 年至 2035 年電氣金屬管材的市場機會、成長要素、產業趨勢分析與預測。Electrical Metal Tubing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

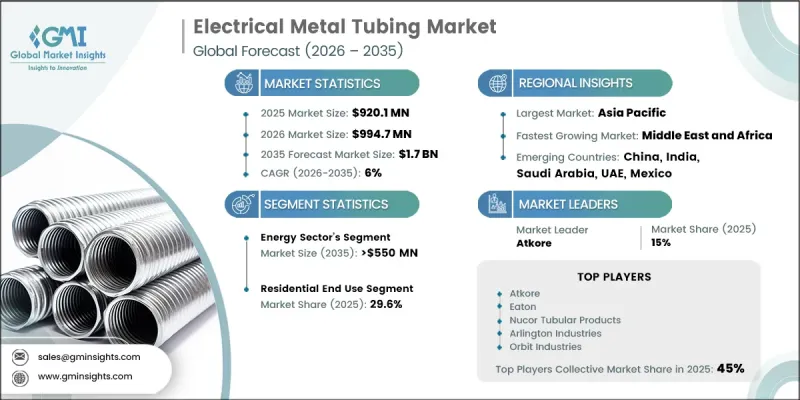

全球電氣金屬管市場預計到 2025 年將達到 9.201 億美元,年複合成長率為 6%,到 2035 年將達到 17 億美元。

市場擴張的驅動力主要來自建築方法的不斷變化、基礎設施的快速現代化以及主要經濟體日益嚴格的電氣安全法規。新興市場加速的都市化和工業發展帶來了強勁的需求,大規模的建設活動也持續擴大了對電氣裝置的需求。電氣金屬導管因其輕質、耐腐蝕、耐用且易於安裝等優點而日益普及,使其適用於多個終端用戶領域的現代電氣佈線系統。能源基礎設施建設的活性化活躍,特別是可再生能源設施和電網現代化項目的推進,進一步刺激了產品需求。製造商正日益注重先進的防護塗層和表面處理技術,以提高產品的耐久性和環境適應性。同時,對永續建築方法和智慧電網整合的日益重視,也推動了電氣金屬導管在節能型和技術先進的電氣系統中得到更廣泛的應用。這些因素共同為全球電氣金屬導管市場創造了穩定且長期的成長環境。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 9.201億美元 |

| 預計金額 | 17億美元 |

| 複合年成長率 | 6% |

預計到2035年,能源產業規模將達到5.5億美元。這一成長主要得益於可再生能源基礎設施投資的增加、輸配電網路的升級改造以及全球向更節能的電力系統轉型。此外,工業應用中日益嚴格的安全要求和不斷發展的電氣標準也進一步推動了電氣金屬管在安全合規安裝中的應用。

預計到2025年,住宅領域將佔市場佔有率的29.6%,到2035年將達到4.8億美元。該領域的成長主要得益於建設活動的活性化、對電氣安全標準合規性的日益重視以及對耐用型線路保護解決方案需求的不斷成長。由於使用壽命長、耐腐蝕,且適用於公共設施和建築基礎設施的安裝,電氣金屬導管在住宅應用中被廣泛使用。

美國電氣金屬管市場預計到2025年將達到1.354億美元,到2035年將達到2.2億美元。該國市場成長的主要驅動力是基礎設施現代化方面的大量投資,尤其是在配電系統和可再生能源項目方面。住宅、商業和工業領域對可靠、安全的電氣佈線解決方案的需求不斷成長,進一步推動了電氣金屬管的普及。此外,嚴格的建築規範和電氣安全法規也促進了電氣金屬管的使用。智慧電網技術的推廣和電動車充電基礎設施的日益普及也為美國電氣金屬管市場的長期成長做出了貢獻。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 監理情勢

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 成長潛力分析

- 波特的分析

- PESTLE分析

- 成本結構分析:電氣應用金屬管

- 貿易數據分析

- 進出口額趨勢

- 主要貿易路線及關稅的影響

- 生產能力和運轉率

- 各地區的生產能力

- 運轉率和擴張計劃

- 新機會和趨勢

- 投資分析及未來展望

第4章 競爭情勢

- 介紹

- 企業市佔率分析:按地區分類

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場規模及預測:以交易量計算,2022-2035年

- 1/2 到 1 英寸

- 1 1/4 至 2 英寸

- 2 1/2 至 3 英寸

- 3-4英寸

- 5-6英寸

- 其他

第6章 市場規模與預測:依應用領域分類,2022-2035年

- 鐵路基礎設施

- 製造工廠

- 造船和海上設施

- 加工廠

- 能源

- 其他

第7章 市場規模及預測:依最終用途分類,2022-2035年

- 住宅

- 商業

- 產業

- 公用事業

第8章 市場規模及預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 法國

- 德國

- 義大利

- 英國

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 中東和非洲

- 沙烏地阿拉伯

- UAE

- 卡達

- 南非

- 拉丁美洲

- 巴西

- 阿根廷

第9章:公司簡介

- American Fittings

- Arlington Industries

- Atkore

- Bridgeport

- Eaton

- EVT Electrical

- GERPAAS

- Hangzhou Francis Conduit Industries

- Nucor Tubular Products

- Orbit Industries

- Producto Electric

- Quality Tube

- Representative Materials Company

- RYMCO USA

- Topaz Lighting

- Topele Enterprise

- Western Tube

- Wheatland Tube

- Yuyao Hengxing Pipe

- Ammo International

The Global Electrical Metal Tubing Market was valued at USD 920.1 million in 2025 and is estimated to grow at a CAGR of 6% to reach USD 1.7 billion by 2035.

Market expansion is shaped by ongoing shifts in construction methodologies, rapid infrastructure modernization initiatives, and the tightening of electrical safety regulations across major economies. Strong demand is being generated by accelerating urbanization and industrial development in emerging markets, where large-scale construction activity continues to expand electrical installation requirements. The adoption of electrical metal tubing is also increasing due to its lightweight structure, corrosion resistance, durability, and ease of installation, making it suitable for modern electrical wiring systems across multiple end-use sectors. Rising activity in energy infrastructure, particularly renewable energy installations and grid modernization projects, is further reinforcing product demand. Manufacturers are increasingly focusing on advanced protective coatings and surface treatments to enhance durability and environmental resistance. At the same time, growing emphasis on sustainable construction practices and smart grid integration is supporting wider adoption of electrical metal tubing in energy-efficient and technologically advanced electrical systems. These combined factors are creating a stable long-term growth environment for the global electrical metal tubing market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $920.1 Million |

| Forecast Value | $1.7 Billion |

| CAGR | 6% |

The energy segment is expected to reach USD 550 million by 2035. Expansion in this segment is being driven by increasing investment in renewable energy infrastructure, upgrades to power transmission and distribution networks, and the global shift toward energy-efficient electrical systems. In addition, more stringent safety requirements and evolving electrical standards in industrial applications are further increasing the adoption of electrical metal tubing for secure and compliant installations.

The residential segment accounted for 29.6% share in 2025 and is projected to reach USD 480 million by 2035. Growth in this segment is supported by rising construction activity, increasing focus on electrical safety compliance, and growing demand for durable wiring protection solutions. Electrical metal tubing is widely used in residential applications due to its long service life, corrosion resistance, and suitability for utility and building infrastructure installations.

U.S. Electrical Metal Tubing Market was valued at USD 135.4 million in 2025 and is expected to reach USD 220 million by 2035. Market growth in the country is driven by significant investments in infrastructure modernization, particularly across power distribution systems and renewable energy projects. Increasing demand for reliable and safe electrical wiring solutions across residential, commercial, and industrial sectors is further supporting adoption. In addition, stringent building codes and electrical safety regulations are encouraging wider use of electrical metal tubing. The expansion of smart grid technologies and the growing deployment of EV charging infrastructure are also contributing to long-term market growth in the United States.

Major companies operating in the global electrical metal tubing market include Atkore, Eaton, Wheatland Tube, Western Tube, Orbit Industries, Arlington Industries, Bridgeport, Nucor Tubular Products, Topaz Lighting, Hangzhou Francis Conduit Industries, Yuyao Hengxing Pipe, Quality Tube, Topele Enterprise, American Fittings, GERPAAS, EVT Electrical, Producto Electric, Representative Materials Company, RYMCO USA, and Ammo International. Companies operating in the electrical metal tubing market are focusing on strengthening their market position through product innovation, operational efficiency, and geographic expansion. A key strategy involves developing corrosion-resistant and high-durability tubing solutions with advanced protective coatings to meet evolving infrastructure requirements. Manufacturers are also investing in automated production technologies to improve cost efficiency and product consistency. Strategic partnerships with construction firms, electrical contractors, and infrastructure developers are helping expand market reach. Companies are increasingly targeting renewable energy and smart grid projects to align with long-term energy transition trends.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.8.3.1 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Trade size trends

- 2.4 Application trends

- 2.5 End use trends

- 2.6 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.7 Cost structure analysis of electrical metal tubing

- 3.8 Trade data analysis (Driven by Primary Research)

- 3.8.1 Import/export value trends (Driven by Primary Research)

- 3.8.2 Key trade corridors & tariff impact (Driven by Primary Research)

- 3.9 Production capacity & utilization (Driven by Primary Research)

- 3.9.1 Production capacity by region (Driven by Primary Research)

- 3.9.2 Utilization rates and expansion pipeline (Driven by Primary Research)

- 3.10 Emerging opportunities & trends

- 3.11 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Competitive positioning matrix

- 4.4 Key Developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans and funding

Chapter 5 Market Size and Forecast, By Trade Size, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 1/2 to 1 inch

- 5.3 1 1/4 to 2 inches

- 5.4 2 1/2 to 3 inches

- 5.5 3 to 4 inches

- 5.6 5 to 6 inches

- 5.7 Others

Chapter 6 Market Size and Forecast, By Application, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Rail infrastructure

- 6.3 Manufacturing facilities

- 6.4 Shipbuilding & offshore facilities

- 6.5 Process plants

- 6.6 Energy

- 6.7 Others

Chapter 7 Market Size and Forecast, By End Use, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Residential

- 7.3 Commercial

- 7.4 Industrial

- 7.5 Utility

Chapter 8 Market Size and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 France

- 8.3.2 Germany

- 8.3.3 Italy

- 8.3.4 UK

- 8.3.5 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 Qatar

- 8.5.4 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

Chapter 9 Company Profiles

- 9.1 American Fittings

- 9.2 Arlington Industries

- 9.3 Atkore

- 9.4 Bridgeport

- 9.5 Eaton

- 9.6 EVT Electrical

- 9.7 GERPAAS

- 9.8 Hangzhou Francis Conduit Industries

- 9.9 Nucor Tubular Products

- 9.10 Orbit Industries

- 9.11 Producto Electric

- 9.12 Quality Tube

- 9.13 Representative Materials Company

- 9.14 RYMCO USA

- 9.15 Topaz Lighting

- 9.16 Topele Enterprise

- 9.17 Western Tube

- 9.18 Wheatland Tube

- 9.19 Yuyao Hengxing Pipe

- 9.20 Ammo International

半導體元件清洗市場:依清潔劑、清洗設備、產業、清洗製程、材料類型、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測半導體及電路製造市場:依產品類型、應用、組件、晶圓尺寸、材料、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測

半導體元件清洗市場:依清潔劑、清洗設備、產業、清洗製程、材料類型、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測半導體及電路製造市場:依產品類型、應用、組件、晶圓尺寸、材料、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測 全球半導體晶片生態系統市場:機會與策略展望(至2035年)

全球半導體晶片生態系統市場:機會與策略展望(至2035年) 半導體產業:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)半導體及相關裝置市場:全球產業分析、市場規模、市場佔有率及預測(2026-2033 年),依半導體類型、裝置類型、材料類型、技術、應用、國家及地區分類半導體智慧電網市場:按組件、功能、應用、最終用戶、國家和地區分類-行業分析、市場規模、市場佔有率和預測(2026-2033 年)

半導體產業:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)半導體及相關裝置市場:全球產業分析、市場規模、市場佔有率及預測(2026-2033 年),依半導體類型、裝置類型、材料類型、技術、應用、國家及地區分類半導體智慧電網市場:按組件、功能、應用、最終用戶、國家和地區分類-行業分析、市場規模、市場佔有率和預測(2026-2033 年) 2026-2030年全球半導體市場

2026-2030年全球半導體市場 用於替代能源技術的半導體:機會和市場

用於替代能源技術的半導體:機會和市場 有機半導體市場:全球產業規模、市場佔有率、趨勢、機會和預測(按材料類型、應用和地區分類)、競爭格局(2021-2031 年)

有機半導體市場:全球產業規模、市場佔有率、趨勢、機會和預測(按材料類型、應用和地區分類)、競爭格局(2021-2031 年) 智慧電網半導體元件市場預測至2034年:按元件、應用、最終用戶和地區分類的全球分析

智慧電網半導體元件市場預測至2034年:按元件、應用、最終用戶和地區分類的全球分析