|

市場調查報告書

商品編碼

2073545

印度LED照明:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)India LED Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

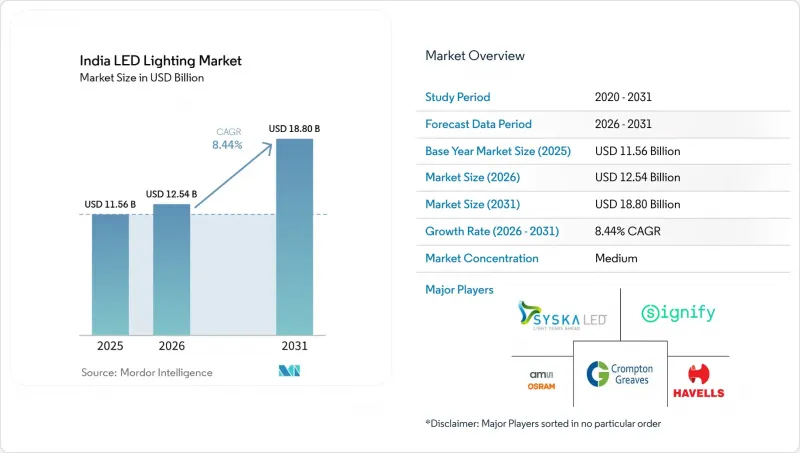

據 Mordor Intelligence 稱,印度 LED 照明市場預計到 2026 年價值將達到 125.4 億美元,高於 2025 年的 115.6 億美元,預計到 2031 年將達到 188 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 8.44%。

本報告按產品類型(燈具、照明設備)、分銷管道(直銷、批發/零售、電子商務)、安裝類型(新安裝、維修)、應用領域(商業辦公室、零售商店、酒店、工業等)和最終用戶(室內、室外、汽車)進行細分。市場預測以美元計價。

印度LED照明市場趨勢與洞察

政府對路燈更換為LED燈的補貼計畫正在迅速增加。

印度能源效率服務有限公司 (EESL) 已製定後續採購輪次的藍圖,目標是在 2024 年前在全國安裝 1,270 萬盞 LED 路燈,從而將市政能源消耗降低 50% 至 60%。 UJALA 框架下的批量競標模式匯集了需求,與供應商協商大幅折扣,並納入了基於結果的服務契約,以保證流明輸出。各邦政府正透過專案預算撥款來強化這一模式,僅奧里薩邦就批准了 20 萬印度盧比(約 2,400 萬美元)用於制定多年維修計畫。這項示範計畫正在推動私人城鎮和工業園區採用 LED 路燈,使下游需求翻倍。隨著印度智慧城市計畫繼續優先發展自適應道路照明,公共部門的需求發揮了需求保障機制的作用,確保供應商獲得可預測的訂單量。

新建商業不動產專案的強制性能源效率標準

節能建築標準 (ECBC) 對照明功率密度設定了限制,如果不使用 LED 燈,幾乎不可能達到這些限制,這促使 LED 技術在所有大型新建商業項目中廣泛應用。安得拉邦於 2025 年初實施了自身的 ECBC 法規,目前已有多個邦正在效倣此政策模式。這項強制性規定將 LED 燈從可選配置提升為法律強制要求,從而創造了一個不受短期價格波動影響的永續市場。該規範與 LEED 和 IGBC 等綠色建築認證的一致性,進一步加速了開發商(旨在獲得高租金)和重視租戶永續性的公司對 LED 燈的採用。維修工程也受益匪淺,因為業主在升級現有物業以符合修訂後的 ECBC 標準時,通常會更換整個照明系統,而不僅僅是單一燈具。

傳統燈泡的高額消費稅

LED燈泡適用12%的商品及服務稅(GST)稅率,但由於其出廠價格較高,低收入消費者的稅負仍然相當沉重,削弱了稅收優惠的實際效果。在電網覆蓋不到的偏遠村莊,這種差距尤其明顯,因為電網的收費系統和零售利潤推高了售價,導致燈泡的終身節能效果難以確定。此外,微企業也面臨合規的挑戰,因為GST申報需要電子發票,而許多非正規企業缺乏這方面的能力。這些因素綜合起來,可能導致補貼計畫實施不充分的地區更換週期延長。因此,能源效率的提升可能會被延緩,進而可能減緩印度LED照明市場的銷售成長。

細分市場分析

2025年,照明燈具和照明設備佔總銷售額的61.25%。這主要歸功於大規模基礎設施升級和商業建築室內裝修中對具有卓越光控性能和防塵/防水性能的整合解決方案的青睞。在印度LED照明市場,政府高速公路計畫和企業園區指定使用IP66防護等級的道路照明燈具和模組化辦公燈具,推動了該細分市場規模的成長,並推高了平均售價。製造商利用嚴格的競標流程,積極提升銷售智慧驅動器和鋁製外殼,即使晶片平均售價下降,也能維持穩健的利潤率。同時,由於仍有77億個傳統白熾燈泡和螢光燈(CFL)燈座未得到支持,燈泡細分市場的銷量實現了兩位數成長,凸顯了印度LED照明市場「雙軌部署模式」的特點。

燈具品類預計年複合成長率為10.32%,此預測基於一般家庭的購買力以及「Gram Ujala」代金券計畫持續推進農村地區的銷售。該計劃為貧困線以下家庭提供燈泡補貼。 SMD封裝生產線的規模經濟效應已降低9瓦燈泡的價格,在電網發達的地區,投資回收期縮短至不到一年。同時,路燈和建築照明燈具的普及預計將帶來更高的毛利率,促使供應商建造新的內部擠出和粉末塗裝設施。在大批量生產、低利潤的燈具與小批量生產、高利潤的照明燈具並存的市場環境下,供應鏈的柔軟性至關重要,許多知名品牌正被鼓勵建立多元化的產品組合。

電氣承包商重視信用條款、現場技術指導和批量採購折扣,而這些優惠很少透過線上平台提供,因此預計到2025年,傳統批發管道仍將佔銷售額的53.15%。大型零售商和機構買家也依賴批發總代理來協調承包工程中多家供應商的交貨,而交鑰匙工程正是印度LED照明市場的特色。然而,在消費性電子產品市場和製造商經營的Shopify店舖的推動下,電子商務佔有率正以8.88%的複合年成長率快速成長,這些店鋪吸引了尋求快速補貨的都市區DIY消費者和小規模建築商。

對於許多品牌而言,直銷 (D2C) 物流透過簡化分銷管道和揭示即時需求訊號,加速了 SKU 精簡週期。然而,由於電子商務的退貨和逆向物流成本不斷擠壓淨利率,一些企業正在採用混合經營模式,在線銷售較為簡單的 SKU,同時透過認證的增值轉售商供應專業照明設備。為了應對這一變化,現有批發商正透過基於應用程式的訂購系統、動態信用評分和全通路忠誠度計畫來反擊。隨著金融科技驅動的營運資金解決方案的擴展,小規模經銷商將能夠獲得所需的流動資金,從而儲備高階智慧照明 SKU,並維持其在印度 LED 照明市場的地位。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 政府加大了路燈維修的補貼力道。

- 新建商業不動產專案的強制性能源效率標準

- LED元件價格大幅下降和國內生產規模擴大。

- 透過有組織的零售和電子商務拓展照明銷售管道

- 印度主要城市物聯網智慧照明試點項目

- 保護性栽培叢集中園藝LED的本地化

- 市場限制因素

- 高稅率(18%)消費稅與傳統燈具的比較

- 郊區售後服務網的去中心化

- 本地組裝廠商之間的價格競爭給利潤率帶來了壓力。

- 創新外形規格的BIS認證進度延遲

- 產業價值鏈分析

- 宏觀經濟因素的影響

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 依產品類型

- 燈

- 照明設備/固定設備

- 透過分銷管道

- 直銷

- 批發和零售

- 電子商務

- 按安裝類型

- 新安裝

- 改裝安裝

- 透過使用

- 商業辦公

- 零售店

- 飯店業

- 產業

- 高速公路和普通公路

- 大樓

- 公共場所

- 醫院

- 園藝和花園

- 住宅

- 車

- 其他(化工、石油天然氣、農業)

- 最終用戶

- 室內的

- 戶外的

- 車

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Signify Innovations India Ltd.

- Havells India Ltd.

- Crompton Greaves Consumer Electricals Ltd.

- Bajaj Electricals Ltd.

- Syska LED Lights Pvt. Ltd.

- Wipro Lighting-Wipro Enterprises Pvt. Ltd.

- Surya Roshni Ltd.

- Orient Electric Ltd.

- Panasonic Life Solutions India Pvt. Ltd.

- Osram Lighting Pvt. Ltd.(LEDVANCE India)

- Eveready Industries India Ltd.

- NTL Lemnis India Pvt. Ltd.

- Goldmedal Electricals Pvt. Ltd.

- HPL Electric and Power Ltd.

- Fiem Industries Ltd.

- Polycab India Ltd.(Lighting division)

- IKEA India Pvt. Ltd.(Smart-home LEDs)

- Halonix Technologies Pvt. Ltd.

- Sturlite Electric Pvt. Ltd.

- Kwality Photonics Pvt. Ltd.(LED chips)

- MIC Electronics Ltd.

- Luker Electric Technologies Pvt. Ltd.

- Opple Lighting India Pvt. Ltd.

- RR Kabel Ltd.(Lighting division)

- Vihan Electric Pvt. Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the india LED lighting market size in 2026 is estimated at USD 12.54 billion, growing from 2025 value of USD 11.56 billion with 2031 projections showing USD 18.8 billion, growing at 8.44% CAGR over 2026-2031.

This report is Segmented by Product Type (Lamps, and Luminaires/Fixtures), Distribution Channel (Direct Sales, Wholesale/Retail, and E-Commerce), Installation Type (New Installation, and Retrofit Installation), Application (Commercial Offices, Retail Stores, Hospitality, Industrial, and More), and End User (Indoor, Outdoor, and Automotive). The Market Forecasts are Provided in Terms of Value (USD).

India LED Lighting Market Trends and Insights

Surging Government Subsidy Programs for Street-Light Retrofits

Energy Efficiency Services Limited (EESL) had installed 12.7 million LED streetlights nationally by 2024, delivering municipal energy savings of 50-60% and setting a blueprint for subsequent procurement rounds. Bulk-tender models under the UJALA umbrella aggregate demand, negotiate steep supplier discounts, and incorporate performance-based service contracts that guarantee lumen output. State governments reinforce the model with dedicated budget outlays Odisha alone sanctioned INR 200 crore (USD 24 million) in 2024 creating a multiyear retrofit pipeline. Demonstration effects spur private townships and industrial parks to replicate street-lighting conversions, multiplying downstream demand. As Smart Cities Mission funds continue to prioritize adaptive roadway lighting in India, public-sector demand acts as a demand-certification mechanism, assuring suppliers of predictable order volumes.

Mandatory Energy-Efficiency Norms for New Commercial Real-Estate Projects

The Energy Conservation Building Code (ECBC) enforces lighting power-density ceilings that are practically unattainable without the use of LEDs, thereby embedding technology adoption in every major green-field commercial project. Andhra Pradesh operationalized state-specific ECBC rules in early 2025, providing a policy template that is now being replicated across multiple states. Mandatory compliance elevates LEDs from a discretionary specification to a statutory line item, thereby creating an enduring offtake channel irrespective of short-term price fluctuations. The code's alignment with LEED and IGBC green-building certifications further increases LED penetration among developers chasing premium lease rates and corporate tenants' sustainability commitments. Retrofits also benefit because landlords upgrading legacy properties to meet revised ECBC thresholds typically replace full lighting systems rather than selectively swap lamps.

High GST Slab Versus Conventional Lamps

Although LED bulbs fall under a 12% GST tier, their higher ex-factory price means the absolute tax burden remains sizable for low-income customers, diluting the headline fiscal incentive. The differential is sharper in off-grid villages where grid tariffs make lifetime savings nebulous and where retail markups inflate ticket prices. Micro-enterprises also face compliance headaches because GST filings demand digitized invoicing, a capability many informal traders lack. Combined, these factors can slow the replacement cycle in regions where subsidy programs are not fully implemented, postponing energy-efficiency gains and dampening volume growth in the Indian LED lighting market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Fall in LED Component Pricing and Domestic Manufacturing Scale-Up

- Growth of Organized Retail and E-Commerce Lighting Channels

- Fragmented After-Sales Service Network in Semi-Urban Areas

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Luminaires and fixtures accounted for 61.25% of 2025 revenue, as large-format infrastructure upgrades and commercial interiors favored integrated solutions that offered superior optical control and ingress protection. Within the Indian LED lighting market, the size of this segment is driven by government highway projects and corporate campuses specifying IP66-rated roadway fixtures and modular office troffers, which elevates average selling prices. Manufacturers exploited the specification-heavy tender process to upsell smart drivers and aluminum housings, improving margin resilience even as chip ASPs dropped. Concurrently, the lamps segment recorded double-digit unit expansion, as 7.7 billion legacy incandescent and CFL sockets remained unaddressed, illustrating the dual-track adoption pattern that defines the Indian LED lighting market.

The lamps category's 10.32% CAGR outlook is based on household affordability and the continued rural push of Gram Ujala vouchers, which subsidize bulbs for families living below the poverty line. Economies of scale on SMD package lines are already compressing the prices of 9-watt bulbs, narrowing the payback window to under one year in grid-connected regions. Conversely, luminaire penetration in street and architectural lighting is expected to unlock higher gross profit pools, prompting suppliers to add in-house extrusion and powder-coating units. The coexistence of high-volume low-margin lamps and lower-volume high-margin fixtures requires supply-chain agility, encouraging multiproduct portfolios across most frontline brands.

Traditional wholesale channels still accounted for 53.15% of 2025 billings as electrical contractors value credit terms, on-site technical guidance, and bulk discounts that online portals rarely extend. Big-box retailers and institutional buyers also rely on wholesale master dealers to coordinate multi-vendor deliveries for turnkey projects that define the India LED lighting market. Yet the e-commerce slice is expanding at 8.88% CAGR, propelled by electronics marketplaces and manufacturer-hosted Shopify storefronts that appeal to urban DIY consumers and small builders seeking quick replenishment.

For many brands, direct-to-consumer logistics have streamlined distribution channels and revealed real-time demand signals, thereby accelerating SKU rationalization cycles. However, e-commerce returns and reverse-logistics costs dilute net margins, driving some players to hybridize by listing low-complexity SKUs online while routing professional-grade luminaires through authorized value-added resellers. Wholesale incumbents are answering back with app-based ordering, dynamic credit scoring, and omnichannel loyalty programs. As fintech-enabled working-capital solutions scale, smaller dealers will gain the liquidity needed to stock premium smart-lighting SKUs, preserving their relevance in the India LED lighting market.

Complete Report Scope:

- By Product Type

- Lamps

- Luminaires / Fixtures

- By Distribution Channel

- Direct Sales

- Wholesale Retail

- E-commerce

- By Installation Type

- New Installation

- Retrofit Installation

- By Application

- Commercial Offices

- Retail Stores

- Hospitality

- Industrial

- Highway and Roadway

- Architectural

- Public Places

- Hospitals

- Horticulture Gardens

- Residential

- Automotive

- Others (Chemicals, Oil and Gas, Agriculture)

- By End-User

- Indoor

- Outdoor

- Automotive

List of Companies Covered in this Report:

- Signify Innovations India Ltd.

- Havells India Ltd.

- Crompton Greaves Consumer Electricals Ltd.

- Bajaj Electricals Ltd.

- Syska LED Lights Pvt. Ltd.

- Wipro Lighting - Wipro Enterprises Pvt. Ltd.

- Surya Roshni Ltd.

- Orient Electric Ltd.

- Panasonic Life Solutions India Pvt. Ltd.

- Osram Lighting Pvt. Ltd. (LEDVANCE India)

- Eveready Industries India Ltd.

- NTL Lemnis India Pvt. Ltd.

- Goldmedal Electricals Pvt. Ltd.

- HPL Electric and Power Ltd.

- Fiem Industries Ltd.

- Polycab India Ltd. (Lighting division)

- IKEA India Pvt. Ltd. (Smart-home LEDs)

- Halonix Technologies Pvt. Ltd.

- Sturlite Electric Pvt. Ltd.

- Kwality Photonics Pvt. Ltd. (LED chips)

- MIC Electronics Ltd.

- Luker Electric Technologies Pvt. Ltd.

- Opple Lighting India Pvt. Ltd.

- RR Kabel Ltd. (Lighting division)

- Vihan Electric Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging government subsidy programmes for street-light retrofits

- 4.2.2 Mandatory energy-efficiency norms for new commercial real-estate projects

- 4.2.3 Rapid fall in LED component pricing and domestic manufacturing scale-up

- 4.2.4 Growth of organised retail and e-commerce lighting channels

- 4.2.5 IoT-enabled smart-lighting pilots in tier-1 Indian cities

- 4.2.6 Localization of horticulture LEDs for protected farming clusters

- 4.3 Market Restraints

- 4.3.1 High GST slab (18%) versus conventional lamps

- 4.3.2 Fragmented after-sales service network in semi-urban areas

- 4.3.3 Price-war margin squeeze among local assemblers

- 4.3.4 Delayed BIS certification timelines for innovative form-factors

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Lamps

- 5.1.2 Luminaires / Fixtures

- 5.2 By Distribution Channel

- 5.2.1 Direct Sales

- 5.2.2 Wholesale Retail

- 5.2.3 E-commerce

- 5.3 By Installation Type

- 5.3.1 New Installation

- 5.3.2 Retrofit Installation

- 5.4 By Application

- 5.4.1 Commercial Offices

- 5.4.2 Retail Stores

- 5.4.3 Hospitality

- 5.4.4 Industrial

- 5.4.5 Highway and Roadway

- 5.4.6 Architectural

- 5.4.7 Public Places

- 5.4.8 Hospitals

- 5.4.9 Horticulture Gardens

- 5.4.10 Residential

- 5.4.11 Automotive

- 5.4.12 Others (Chemicals, Oil and Gas, Agriculture)

- 5.5 By End-User

- 5.5.1 Indoor

- 5.5.2 Outdoor

- 5.5.3 Automotive

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Signify Innovations India Ltd.

- 6.4.2 Havells India Ltd.

- 6.4.3 Crompton Greaves Consumer Electricals Ltd.

- 6.4.4 Bajaj Electricals Ltd.

- 6.4.5 Syska LED Lights Pvt. Ltd.

- 6.4.6 Wipro Lighting - Wipro Enterprises Pvt. Ltd.

- 6.4.7 Surya Roshni Ltd.

- 6.4.8 Orient Electric Ltd.

- 6.4.9 Panasonic Life Solutions India Pvt. Ltd.

- 6.4.10 Osram Lighting Pvt. Ltd. (LEDVANCE India)

- 6.4.11 Eveready Industries India Ltd.

- 6.4.12 NTL Lemnis India Pvt. Ltd.

- 6.4.13 Goldmedal Electricals Pvt. Ltd.

- 6.4.14 HPL Electric and Power Ltd.

- 6.4.15 Fiem Industries Ltd.

- 6.4.16 Polycab India Ltd. (Lighting division)

- 6.4.17 IKEA India Pvt. Ltd. (Smart-home LEDs)

- 6.4.18 Halonix Technologies Pvt. Ltd.

- 6.4.19 Sturlite Electric Pvt. Ltd.

- 6.4.20 Kwality Photonics Pvt. Ltd. (LED chips)

- 6.4.21 MIC Electronics Ltd.

- 6.4.22 Luker Electric Technologies Pvt. Ltd.

- 6.4.23 Opple Lighting India Pvt. Ltd.

- 6.4.24 RR Kabel Ltd. (Lighting division)

- 6.4.25 Vihan Electric Pvt. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

亞太地區LED照明:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

亞太地區LED照明:市佔率分析、產業趨勢與統計及成長預測(2026-2031年) LED霓虹燈市場規模、佔有率和成長分析:按產品類型、安裝類型、電壓類型、應用、顏色類型、分銷管道、最終用戶和地區分類-2026-2033年產業預測

LED霓虹燈市場規模、佔有率和成長分析:按產品類型、安裝類型、電壓類型、應用、顏色類型、分銷管道、最終用戶和地區分類-2026-2033年產業預測 LED 照明和 OLED 照明:市場分析和製造趨勢

LED 照明和 OLED 照明:市場分析和製造趨勢 LED面板燈市場報告:按應用和地區分類(2026-2034)歐洲LED照明:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)

LED面板燈市場報告:按應用和地區分類(2026-2034)歐洲LED照明:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年) LED照明市場規模、佔有率和成長分析:按產品類型、安裝類型、流明、應用、銷售管道和地區分類-2026-2033年產業預測

LED照明市場規模、佔有率和成長分析:按產品類型、安裝類型、流明、應用、銷售管道和地區分類-2026-2033年產業預測 LED環形燈市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測

LED環形燈市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測 LED照明系統市場預測至2034年-按產品、通路、技術、應用、最終用戶和地區分類的全球分析LED嵌燈市場報告:按應用和地區分類(2026-2034年)LED照明市場規模、佔有率、趨勢和預測:按應用和地區分類,2026-2034年

LED照明系統市場預測至2034年-按產品、通路、技術、應用、最終用戶和地區分類的全球分析LED嵌燈市場報告:按應用和地區分類(2026-2034年)LED照明市場規模、佔有率、趨勢和預測:按應用和地區分類,2026-2034年