|

市場調查報告書

商品編碼

2066742

歐洲LED照明:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)Europe LED Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

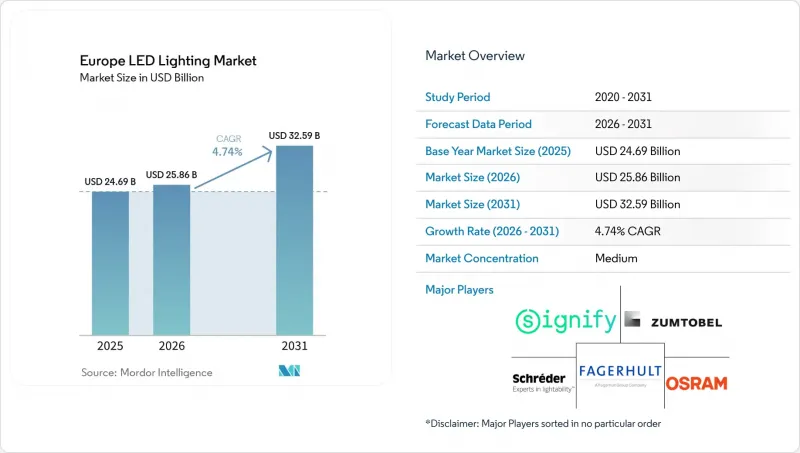

據 Mordor Intelligence 稱,2025 年歐洲 LED 照明市值為 246.9 億美元,預計將從 2026 年的 258.6 億美元成長到 2031 年的 325.9 億美元,2026 年至 2031 年的複合年成長率為 4.74%。

本報告按產品類型(燈具、照明設備)、分銷管道(直銷、批發/零售等)、安裝類型(新安裝、維修安裝)、應用領域(商業辦公室、零售商店、酒店、工業等)、最終用戶(室內、室外等)和國家/地區進行細分。市場預測以美元計價。

歐洲LED照明市場趨勢與洞察

歐盟嚴格的能源效率法規正在推動基本需求。

歐洲LED照明市場目前受益於法律規範,該框架不僅關注能源效率,更著眼於產品結構、文件和生命週期性能。歐盟2019/2020號法規規定了LED燈的最低發光效率標準,而更新的永續產品生態設計法規則進一步擴大了合規範圍,將耐用性、可維修性和回收材料含量揭露納入其中。這增加了不合規的成本,尤其是在歐洲區域能源性能認證(EPREL)註冊和數據檢驗已成全部區域日益重要的執法措施的情況下。歐盟委員會也表示,目前的生態設計和能源標籤計畫將在2023年使歐盟最終能源消耗量減少12%,避免1.45億噸二氧化碳排放,並創造34.6萬個就業崗位,顯示政策支持並非曇花一現,而是持續強勁。從2026年起,新增的「數位產品護照」要求將繼續有利於那些能夠大規模管理工程、可追溯性和監管報告的歐洲LED照明市場製造商。此外,即使在以規格主導的項目中,對高階品牌的支持也在不斷成長。這是因為針對閃爍和頻閃效果的更嚴格的性能標準,使得在採購階段檢驗技術品質變得更加容易。

鹵素燈和螢光的快速淘汰正在催生對替代品的結構性需求。

歐盟於2023年禁止銷售T5和T8螢光管後,歐洲LED照明市場需求持續成長。這是因為更換工作通常會落後於法規的實施幾個維護週期。這種時間滯後影響顯著,因為許多辦公室、零售商店、醫院和公共設施仍在繼續使用禁令生效後未立即更換的過時設備。以斯洛伐克一家醫院的維修為例,其年能耗降低了52%,從93,728千瓦時降至45,063千瓦時,每年節省成本超過23,000歐元(約25,070美元)。這為公共機構和機構負責人提供了清晰的投資回報前景。此外,將許多T8燈管更換為LED燈需要更新控制設備和試運行工作,因此其升級週期比簡單地更換燈管要大規模多。因此,許多專案正從簡單的基礎維護支出轉向系統化的維修。公開競標進一步推動了這一趨勢,波蘭塞穆德公社的計畫就是一個例證。作為該市現代化計劃的一部分,該項目已簽訂契約,將在2026年前更換436個LED燈。這繼續支撐著歐洲LED照明市場,該市場目前仍受到該地區非住宅和公共基礎設施更新浪潮的推動,而這一浪潮尚未完全實現。

維修對成本的敏感度較高,投資回收期較長,限制了中小企業採用翻新改造方案。

在歐洲LED照明市場,中小企業(SME)的採用率差距依然顯著。這是因為全面互聯維修需要一筆初始投資,而許多中小企業無法在一個預算週期內承擔這筆費用。光是在愛爾蘭,就有24.8萬家中小企業使用著10.9萬棟建築,但到2025年,只有4%的企業能夠完成全面維修。這清楚地表明,即使長期能源效率優勢顯而易見,小規模用戶的行動依然緩慢。在南歐和東歐,這種限制更為突出,因為這些地區電價低廉且資本預算緊張,難以指望基礎維修計畫在短期內獲得投資回報。雖然資金籌措模式有所幫助,但它們通常需要進行能源審計、信用審查和簽訂契約,這對許多小規模企業來說既複雜又耗時。 Whitecroft Lighting為Currys設計的循環照明昇級項目,展示了透過大規模措施所能取得的成就。透過維修77家門市並重新利用6500多盞燈具,我們減少了40%的能源消耗和溫室氣體排放。問題在於,獨立經營的中小型企業很少有這樣的購買力,而且在投資決策週期短、融資極為敏感的情況下,歐洲LED照明市場仍然錯失了一些轉折點。

細分市場分析

到2025年,燈具和照明裝置將佔歐洲LED照明市場57.63%的佔有率,以金額為準將顯著超過燈泡。這一領先優勢反映出市場需求正從簡單地更換光源轉向升級到整合式照明裝置,後者將合規性、控制和使用壽命作為一個整體產品進行評估。因此,歐洲LED照明市場的大部分價值正向完整的照明系統轉移,尤其是在商業和公共專案中,規格、安裝時間和文件都至關重要。 Zumtberg的模組化連續陣列系統「TECTON II」表明,供應商之間的競爭不僅體現在產量上,也體現在工作效率上,該系統聲稱與傳統配置相比,安裝時間縮短了71%。在這樣一個市場中,承包商的確定、合規性相關文件以及因維修造成的運作往往與單價一樣影響採購決策,因此,這是一個至關重要的因素。

儘管燈具市場規模相對較小,但預計到2031年將以5.02%的複合年成長率成長,成為歐洲LED照明市場成長最快的產品類型。這一成長與市場對禁用螢光的替代需求以及市政部門持續淘汰公共設施中老舊鈉燈和傳統照明燈具的項目密切相關。在尚未需要全面更換照明燈具,或操作員希望逐步過渡以減少短期資本投入的情況下,燈具仍然發揮著至關重要的作用。此外,歐盟2019/2020號法規維持了高耐用性標準,包括光通量維持率要求。這不僅杜絕了不合格產品,也為公共部門採購中的認證供應商提供了支援。目前,已有超過50萬種光源型號在EPREL註冊,歐洲LED照明產業依然保持著強勁的發展勢頭,同時,監管機構的品質檢驗也變得更加便捷,採購商的透明度也更高。

到2025年,批發和零售將佔46.12%的市場佔有率,這意味著分銷網路仍將是歐洲LED照明市場活動的重要組成部分。電氣設備批發商仍然至關重要,因為他們連接製造商與承包商、安裝商和維護團隊,這些客戶仍然傾向於本地庫存支援和技術指導。直銷在歐洲LED照明市場也仍然很重要,因為大規模的規格製定者是設施經理、顧問或建築師,而不是購買現成產品的普通消費者。這些銷售管道依然穩健,因為複雜的專案需要設計協助、試運行建議和售後服務,而這些服務並非總是能透過廣泛的線上管道獲得。儘管如此,跨品牌產品數據比較的便利性正使採購行為更加透明和標準化。

預計到2031年,電子商務將以5.45%的複合年成長率成長,成為歐洲LED照明市場成長最快的銷售管道。 EPREL基於QR碼的產品資訊正在推動這一轉變,因為它允許買家自行驗證效能並查看數據,而無需完全依賴分銷商的解讀。另一方面,線上產品比較能力的提升使得非聯網LED產品更容易趨於同質化,這可能會給主要競爭優勢在於基礎硬體的供應商帶來價格壓力。對於連網照明燈具而言,尚未完全消除中間商,因為設定、控制功能整合和試運行軟體通常需要經銷商的支援以及製造商主導的工作流程。隨著數位產品護照法規的臨近,預計歐洲LED照明市場將更加清晰地區分透過透明數位比較銷售的簡單產品和仍依賴規格和支援的系統主導產品。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 歐盟嚴格的能源效率法規

- 快速淘汰鹵素燈和螢光

- 企業對零排放的承諾正在加速維修工作。

- LED每流明成本更低

- 競標專案。

- 部署現場可再生能源和直流微電網

- 市場限制因素

- 中小企業維修的投資回收期受價格影響。

- 稀土元素磷光體供應鏈的變異性

- 歐盟生態設計與WEEE合規性的複雜性

- 智慧照明安裝人員短缺

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 依產品類型

- 燈

- 照明燈具/燈具

- 透過分銷管道

- 直銷

- 批發/零售

- 電子商務

- 按安裝類型

- 新推出

- 改裝安裝

- 透過使用

- 商業辦公

- 零售店

- 飯店業

- 產業

- 高速公路和普通公路

- 大樓

- 公共場所

- 醫院

- 花園

- 住宅

- 車

- 其他用途(化學品、石油和天然氣、農業)

- 最終用戶

- 室內的

- 戶外的

- 車

- 國家

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 瑞典

- 波蘭

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Signify NV

- Zumtobel Group AG

- Osram Licht AG(ams-Osram)

- Schreder SA

- Fagerhult Group

- Acuity Brands Lighting Inc.

- Havells Sylvania Europe Ltd.

- Legrand SA

- Eaton Corporation plc(Cooper Lighting)

- TRILUX GmbH and Co. KG

- Thorn Lighting Ltd.

- FW Thorpe Plc

- LEDVANCE GmbH

- Helvar Oy Ab

- iGuzzini illuminazione SpA

- Glamox AS

- Cree Lighting Europe SpA

- ITECH LED Lighting

- Hella GmbH and Co. KGaA

- Nichia Europe GmbH

- Siteco GmbH

- Disano Illuminazione SpA

- Tridonic GmbH and Co KG

- Opple Lighting Europe BV

第7章 市場機會與未來展望

According to Mordor Intelligence, the europe lED lighting market size was valued at USD 24.69 billion in 2025 and is forecasted to grow from USD 25.86 billion in 2026 to USD 32.59 billion by 2031, growing at a CAGR of 4.74% from 2026 to 2031.

This report is Segmented by Product Type (Lamps, and Luminaires/Fixtures), Distribution Channel (Direct Sales, Wholesale/Retail, and More), Installation Type (New Installation, and Retrofit Installation), Application (Commercial Offices, Retail Stores, Hospitality, Industrial, and More), End User (Indoor, Outdoor, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

Europe LED Lighting Market Trends and Insights

Stringent EU Energy-Efficiency Regulations Drive Baseline Demand

The Europe LED lighting market is benefiting from a regulatory framework that now reaches beyond efficiency and into product structure, documentation, and lifecycle performance. Regulation (EU) 2019/2020 set minimum efficacy thresholds for LED lamps, and the newer Ecodesign for Sustainable Products Regulation extended the compliance burden into durability, reparability, and recycled-content disclosure. This has raised the cost of non-compliance, especially as EPREL registration and data validation have become more visible enforcement tools across the region. The European Commission also stated that the current ecodesign and energy-labelling program helped cut final EU energy consumption by 12% in 2023, while avoiding 145 million tonnes of CO2 emissions and supporting 346,000 jobs, which shows why policy support remains firm rather than temporary. The Digital Product Passport will add another layer from 2026 onward, which means the Europe LED lighting market will continue to reward manufacturers that can manage engineering, traceability, and regulatory reporting at scale. Premium brands are also gaining support in specification-led projects because requirements such as stricter flicker and stroboscopic performance have made technical quality easier to verify during procurement.

Rapid Phase-Out of Halogen and Fluorescent Lamps Creates a Structural Replacement Pipeline

The Europe LED lighting market continues to draw demand from the 2023 EU phase-out of T5 and T8 fluorescent tubes because replacement behavior typically trails regulation by several maintenance cycles. That lag matters because many offices, retail sites, hospitals, and municipal facilities are still working through old installed bases that were not replaced immediately after the sales ban. A hospital retrofit in Slovakia showed a 52% reduction in annual energy use, falling from 93,728 kWh to 45,063 kWh, while yearly cost savings exceeded EUR 23,000 (USD 25,070), which keeps the payback case visible for public and institutional buyers. The replacement cycle is also larger than a simple lamp swap because many T8 conversions require control-gear updates and commissioning work, which pushes more projects toward connected retrofits instead of basic maintenance spend. Public tenders continue to reinforce that pipeline, as seen in the Szemud Commune project in Poland, where 436 LED replacements were contracted through 2026 under a municipal modernization program. This keeps the Europe LED lighting market supported by a replacement wave that has not yet fully worked through the region's non-residential and public infrastructure stock.

Price-Sensitive Retrofit Payback Periods Constrain SME Adoption

The Europe LED lighting market still faces a clear adoption gap among smaller businesses because full connected retrofits require higher upfront spending than many SMEs can absorb in one budget cycle. In Ireland alone, 248,000 SMEs occupied 109,000 buildings, yet only 4% had undergone deep retrofitting by 2025, which illustrates how slowly smaller occupiers move even when the long-term efficiency case is positive. This constraint is more visible in Southern and Eastern Europe, where lower electricity prices and tighter capital budgets weaken the near-term return case for basic retrofits. Financing models can help, but they often require energy audits, credit screening, and contract structures that many smaller operators see as complex or time-consuming. Whitecroft Lighting's circular relight program for Currys showed what scale can achieve, refurbishing 77 stores, reusing more than 6,500 luminaires, and reducing energy use and greenhouse gas emissions by 40%. The problem is that individually owned SMEs rarely have that purchasing leverage, so the Europe LED lighting market still loses some conversion volume where investment decisions remain short-cycle and highly cash sensitive.

Other drivers and restraints analyzed in the detailed report include:

- Falling LED Cost Per Lumen Expands The Addressable Market

- Corporate Net-Zero Commitments Accelerate Commercial Retrofits Beyond Minimum Compliance

- Supply-Chain Volatility for Rare-Earth Phosphors Introduces Margin and Availability Risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Luminaires and fixtures held 57.63% of the Europe LED lighting market share in 2025, which kept this category firmly ahead of lamps in value terms. This lead reflects the shift from lamp-only replacement toward integrated fixture upgrades, where compliance, controls, and service life are assessed at the full-product level rather than through a simple source swap. The Europe LED lighting market has therefore moved more of its value into complete luminaire systems, especially in commercial and public projects where specification, installation time, and documentation all matter. Zumtobel's TECTON II modular continuous-row system showed how suppliers are competing on labor efficiency as much as on output, with a stated 71% saving in installation time compared with conventional configurations.That matters in a market where contractor availability, compliance paperwork, and retrofit downtime often shape procurement decisions as much as unit cost.

The lamps segment is smaller, but it is still forecasted to grow at a 5.02% CAGR through 2031, which makes it the fastest-moving product category in the Europe LED lighting market. This growth is tied to the replacement of banned fluorescent formats and to municipal programs that continue to remove older sodium and conventional lighting points from public estates. The lamp category remains relevant where full fixture replacement is not yet necessary, or where operators want a staged conversion that limits immediate capital spend. Regulation (EU) 2019/2020 also keeps durability standards high, including lumen-maintenance requirements that screen out weaker products and support certified suppliers in public-sector buying. With more than 500,000 light-source models registered in EPREL, the Europe LED lighting industry remains deep and active, but quality verification has become easier for surveillance authorities and more visible for buyers.

Wholesale and retail held 46.12% share in 2025, which shows that distributor networks still anchor a large part of Europe LED lighting market activity. Electrical wholesalers remain important because they connect manufacturers with contractors, installers, and maintenance teams that still prefer local inventory support and technical guidance. Direct sales also remained important in the Europe LED lighting market, where large commercial, healthcare, airport, and municipal projects are specified by facility managers, consultants, or architects instead of off-the-shelf buyers. Those routes stay resilient because complex projects need design support, commissioning input, and after-sales accountability that broad online channels do not always provide. Even so, purchasing behavior is becoming more transparent and more standardized as product data has become easier to compare across brands.

E-commerce is forecasted to expand at a 5.45% CAGR through 2031, making it the fastest-growing route to market in the Europe LED lighting market size mix by channel. EPREL's QR-based product information has helped this shift because buyers can verify performance and labeling data without relying only on distributor interpretation. The downside is that online comparison makes non-connected LED products easier to commoditize, which can compress pricing for suppliers that compete mainly on basic hardware. Connected luminaires still resist full disintermediation because configuration, controls integration, and commissioning software often require dealer-backed or manufacturer-led workflows. As Digital Product Passport rules move closer, the Europe LED lighting market is likely to sort itself more clearly between simple products that sell on transparent digital comparison and system-led products that still depend on specification and support.

List of Companies Covered in this Report:

- Signify N.V.

- Zumtobel Group AG

- Osram Licht AG (ams-Osram)

- Schreder SA

- Fagerhult Group

- Acuity Brands Lighting Inc.

- Havells Sylvania Europe Ltd.

- Legrand S.A.

- Eaton Corporation plc (Cooper Lighting)

- TRILUX GmbH and Co. KG

- Thorn Lighting Ltd.

- FW Thorpe Plc

- LEDVANCE GmbH

- Helvar Oy Ab

- iGuzzini illuminazione S.p.A.

- Glamox AS

- Cree Lighting Europe S.p.A.

- ITECH LED Lighting

- Hella GmbH and Co. KGaA

- Nichia Europe GmbH

- Siteco GmbH

- Disano Illuminazione S.p.A.

- Tridonic GmbH and Co KG

- Opple Lighting Europe B.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent EU Energy-Efficiency Regulations

- 4.2.2 Rapid Phase-Out of Halogen and Fluorescent Lamps

- 4.2.3 Corporate Net-Zero Commitments Accelerating Retrofits

- 4.2.4 Falling LED Cost per Lumen

- 4.2.5 Smart-City Tenders Bundling IoT Sensors

- 4.2.6 On-Site Renewable and DC Micro-Grids Adoption

- 4.3 Market Restraints

- 4.3.1 Price-Sensitive Retrofit Payback Period in SMEs

- 4.3.2 Supply-Chain Volatility for Rare-Earth Phosphors

- 4.3.3 Complexity of EU Eco-design and WEEE Compliance

- 4.3.4 Shortage of Skilled Installers for Connected Lighting

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Lamps

- 5.1.2 Luminaires / Fixtures

- 5.2 By Distribution Channel

- 5.2.1 Direct Sales

- 5.2.2 Wholesale / Retail

- 5.2.3 E-Commerce

- 5.3 By Installation Type

- 5.3.1 New Installation

- 5.3.2 Retrofit Installation

- 5.4 By Application

- 5.4.1 Commercial Offices

- 5.4.2 Retail Stores

- 5.4.3 Hospitality

- 5.4.4 Industrial

- 5.4.5 Highway and Roadway

- 5.4.6 Architectural

- 5.4.7 Public Places

- 5.4.8 Hospitals

- 5.4.9 Horticulture Gardens

- 5.4.10 Residential

- 5.4.11 Automotive

- 5.4.12 Other Applications (Chemicals, Oil and Gas, Agriculture)

- 5.5 By End User

- 5.5.1 Indoor

- 5.5.2 Outdoor

- 5.5.3 Automotive

- 5.6 By Country

- 5.6.1 Germany

- 5.6.2 United Kingdom

- 5.6.3 France

- 5.6.4 Italy

- 5.6.5 Spain

- 5.6.6 Netherlands

- 5.6.7 Sweden

- 5.6.8 Poland

- 5.6.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Signify N.V.

- 6.4.2 Zumtobel Group AG

- 6.4.3 Osram Licht AG (ams-Osram)

- 6.4.4 Schreder SA

- 6.4.5 Fagerhult Group

- 6.4.6 Acuity Brands Lighting Inc.

- 6.4.7 Havells Sylvania Europe Ltd.

- 6.4.8 Legrand S.A.

- 6.4.9 Eaton Corporation plc (Cooper Lighting)

- 6.4.10 TRILUX GmbH and Co. KG

- 6.4.11 Thorn Lighting Ltd.

- 6.4.12 FW Thorpe Plc

- 6.4.13 LEDVANCE GmbH

- 6.4.14 Helvar Oy Ab

- 6.4.15 iGuzzini illuminazione S.p.A.

- 6.4.16 Glamox AS

- 6.4.17 Cree Lighting Europe S.p.A.

- 6.4.18 ITECH LED Lighting

- 6.4.19 Hella GmbH and Co. KGaA

- 6.4.20 Nichia Europe GmbH

- 6.4.21 Siteco GmbH

- 6.4.22 Disano Illuminazione S.p.A.

- 6.4.23 Tridonic GmbH and Co KG

- 6.4.24 Opple Lighting Europe B.V.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

印度LED照明:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區LED照明:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

印度LED照明:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區LED照明:市佔率分析、產業趨勢與統計及成長預測(2026-2031年) LED霓虹燈市場規模、佔有率和成長分析:按產品類型、安裝類型、電壓類型、應用、顏色類型、分銷管道、最終用戶和地區分類-2026-2033年產業預測

LED霓虹燈市場規模、佔有率和成長分析:按產品類型、安裝類型、電壓類型、應用、顏色類型、分銷管道、最終用戶和地區分類-2026-2033年產業預測 LED 照明和 OLED 照明:市場分析和製造趨勢

LED 照明和 OLED 照明:市場分析和製造趨勢 LED面板燈市場報告:按應用和地區分類(2026-2034)

LED面板燈市場報告:按應用和地區分類(2026-2034) LED照明市場規模、佔有率和成長分析:按產品類型、安裝類型、流明、應用、銷售管道和地區分類-2026-2033年產業預測

LED照明市場規模、佔有率和成長分析:按產品類型、安裝類型、流明、應用、銷售管道和地區分類-2026-2033年產業預測 LED環形燈市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測

LED環形燈市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測 LED照明系統市場預測至2034年-按產品、通路、技術、應用、最終用戶和地區分類的全球分析LED嵌燈市場報告:按應用和地區分類(2026-2034年)LED照明市場規模、佔有率、趨勢和預測:按應用和地區分類,2026-2034年

LED照明系統市場預測至2034年-按產品、通路、技術、應用、最終用戶和地區分類的全球分析LED嵌燈市場報告:按應用和地區分類(2026-2034年)LED照明市場規模、佔有率、趨勢和預測:按應用和地區分類,2026-2034年