|

市場調查報告書

商品編碼

2073467

一次電池:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Primary Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

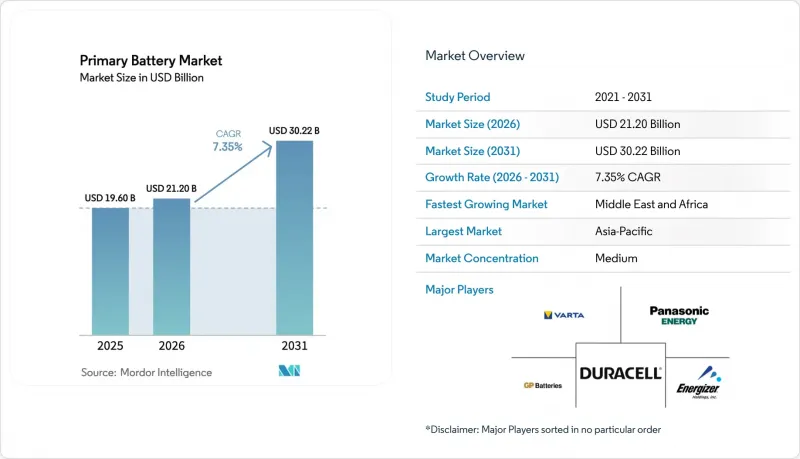

根據 Mordor Intelligence 估計,2026 年一次電池市值為 212 億美元,預計在預測期(2026-2031 年)內將以 7.35% 的複合年成長率成長,到 2031 年達到 302.2 億美元。

本報告按類型(鹼性電池、一次鋰電池、鋅空氣電池、鋅碳/氯化物電池、氧化銀電池等)、形狀(圓柱形、紐扣式電池、棱柱形/封裝式電池等)、應用(家用電子電器、工業和OEM、物聯網感測器和智慧基礎設施等)以及地區(北美、歐洲、亞太地區、分類、以及中東和非洲)。

全球一次電池市場趨勢及洞察

智慧家庭和物聯網對一次性感測器的需求激增。

2024年,LoRaWAN網路上的連網設備數量超過1.25億,年增25%。這些終端設備,例如門感應器、漏水感應器和人體感應器,大多設計為使用單節AA鹼性電池或羈扣電池供電,續航時間長達10年。這使得部署者無需為每個節點額外支付15至30美元的充電基礎設施成本,從而降低了整體擁有成本。多家廠商的Wi-Fi HaLow晶片組承諾使用兩顆AA鹼性電池即可運作10年,無需為商業建築佈線即可進行改造。 GSM協會預測,到2030年,將部署11億台環境物聯網設備,但其中約4.73億台設備仍將依賴一次電池,用於光照不足以進行能源採集的地區。 ITU-T L.1310定義的超級電容可以承受數十萬次充放電循環,但其備用時間非常短。因此,它們被證明對長壽命一次電池化學系統起的是補充作用,而不是替代作用。

新興市場中離網醫療設備的快速普及

2024年,世界衛生組織(世衛組織)報告稱,可靠的電力供應仍然不足以滿足撒哈拉以南非洲和南亞十億人口的醫療設施需求。這促使人們開始採用由保存期限長達10年的鋰電池供電的脈動式血氧監測儀系統、攜帶式超音波診斷設備和疫苗監測儀。這些電池通常用於低功耗設備,因為在這些設備中,電池管理系統的成本超過了定期更換電池的成本。此外,在由多邊銀行資助的結合太陽能和儲能的微電網中,這些電池也得到了廣泛應用。到2025年中期,全球穿戴式醫療設備的出貨量將達到5.565億台,其中18%的設備需要使用氧化銀或鋰紐扣電池來滿足嚴格的體積能量密度要求。在助聽器領域,鋅空氣連結電池仍然佔據主導地位,因為它們可以在極小的機殼內提供高達650毫安培時(1.4伏)的容量,而可充電電池在不犧牲佩戴舒適度的前提下無法做到這一點。

與二次電池和超級電容的競爭

到2025年,可充電鋰離子電池將佔全球電池容量的83%,將使電池組價格降至每千瓦時100美元以下,並蠶食周邊設備、揚聲器和個人護理設備中一次電池的市場佔有率。超級電容儘管能量密度有限,但其充放電循環次數超過50萬次,在通訊設備的備用電源應用上正日益普及。然而,它們無法滿足未來幾年的低功耗供電需求。鎳氫(NiMH)AA電池繼續取代中等功耗消費性設備中的鹼性一次電池,但假冒鹼性電池的進口進一步壓低了價格,並危及了安全性。

細分市場分析

預計2026年至2031年間,各類一次性鋰電池的複合年成長率將達到9.5%,成為一次電池市場中成長最快的產品。這主要得益於工業測量儀器和國防通訊領域對單節電壓3.0-3.6V、工作溫度範圍為-40 度C至+85 度C的電池的需求成長。同時,由於鹼性電池擁有廣泛的零售分銷網路,預計到2025年,其銷量將占到總銷量的63.5%。在助聽器市場,輸出電壓為1.4V、最大容量為650mAh的鋅空氣電池佔據主導地位。氧化銀紐扣電池在精密手錶和血糖值儀領域價格較高。近期美國進口數據顯示,由於製造商尋求對沖其在中國提煉市場佔據主導地位所帶來的風險,錳礦進口量激增。

現有鹼性電池製造商正透過材料科學維持其市場佔有率。Panasonic的「EVOLTA NEO」採用高純度二氧化錳並添加鈦,使其續航時間延長了1.3倍。同時,由於保存期限有限,鎳鋅電池仍屬於小眾產品。鋅碳電池在價格敏感型細分市場中依然表現強勁,但隨著與鹼性電池的價格差距縮小,其市場佔有率正在下降。這進一步加速了一次電池市場的優質化。

區域分析

2025年,亞太地區佔全球銷售額的46.1%。這反映了中國在二氧化錳精煉、鋅粉生產和電池組裝等垂直整合環節的成本優勢。原一次電池生產集中在小規模的國內工廠,因為印度的生產連結獎勵計畫計劃(PLI)分配了18吉瓦時的電池產能,主要用於鋰離子電動車電池組。日本錦濱廠於2023年下半年全面投產,每月生產4,800萬顆鹼性電池,是高級產品在中國以外的主要供應地。泰國、越南和印尼等新興的東協地區中心正利用其低廉的人事費用和供應鏈接近性,吸引助聽器紐扣電池的組裝。

在中東和非洲地區,預計到2031年,分散式能源專案將以9.0%的複合年成長率成長。根據世界銀行估計,撒哈拉以南非洲地區仍有6.4億至6.5億人無法連接電網,因此該地區普遍採用太陽能和微電網相結合的方式,而一次電池的應用則僅限於低功率監測應用。在南非,2024年計畫建造的360兆瓦電池競標和1,200兆瓦電池計畫主要採用具有長放電能力的可充電電池,而一次電池仍限於外圍遙測應用。假電池依然猖獗,不僅危害安全,也侵蝕了正規品牌的市場佔有率。

在北美和歐洲,市場正在重組,以高階細分市場為中心。勁量電池將在2025會計年度獲得1.124億美元的45X條款稅額扣抵,以支持其國內生產。該公司於2025年5月收購了Advanced Power Solutions NV,增加了在波蘭的產能,但也導致短期利潤率下降。由於歐盟生產者延伸責任制(EPR)法規的實施,遵循成本持續上升,但成熟企業比新參與企業更容易消化這些成本。在南美洲,巴西和阿根廷處於成長前沿,電子商務刺激了當地需求,但亞馬遜和Patagonia面臨的物流挑戰阻礙了其進一步的市場滲透。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 智慧家庭和物聯網對一次性感測器的需求激增。

- 新興市場離網醫療設備的快速成長

- 國防部門攜帶式電子設備預算增加

- 過渡到無汞化學物質和綠色採購義務

- 消費性電子產品的更換週期

- 電子商務的普及擴大了零售商的業務範圍。

- 市場限制因素

- 與二次電池和超級電容的競爭

- 因生產者延伸責任制(EPR)費用而增加的成本

- 原物料價格波動(鋅、鋰、錳)

- 假電池湧入亞洲和非洲

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按類型

- 鹼性電池

- 一次鋰電池(Li-MnO2、Li-SOCl2、Li-CFx)

- 鋅 - 空氣

- 鋅/碳/氯化物

- 氧化銀及其他

- 按外形規格

- 圓柱形(AA、AAA、C、D)

- 紐扣電池和紐扣電池

- 棱鏡/包裝

- 其他(特殊形狀)

- 透過使用

- 家用電子產品

- 工業和OEM

- 醫療保健

- 國防/航太

- 物聯網感測器和智慧基礎設施

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 北歐國家

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 澳洲和紐西蘭

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 埃及

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- Duracell Inc.

- Energizer Holdings Inc.

- Panasonic Energy Co., Ltd.

- GP Batteries International Ltd.

- Saft(TotalEnergies)

- Ultralife Corporation

- FDK Corporation

- Varta AG

- Maxell Holdings, Ltd.

- Sony(Murata Energy)

- Rayovac(Spectrum Brands)

- Fujitsu Batteries

- Camelion Battery Co., Ltd.

- Philips Lighting(Signify)

- Zhejiang Mustang Battery

- EVE Energy Co., Ltd.

- Tianqiu(T&E)

- Renata SA(Swatch Group)

- Xiamen 3-Circle Battery

- Tenergy Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the primary battery market size is estimated at USD 21.20 billion in 2026, and is expected to reach USD 30.22 billion by 2031, at a CAGR of 7.35% during the forecast period (2026-2031).

This report is Segmented by Type (Alkaline, Primary Lithium, Zinc-Air, Zinc-Carbon/Chloride, and Silver-Oxide and Others), Form Factor (Cylindrical, Coin and Button Cells, Prismatic/Packaged, and Others), Application (Consumer Electronics, Industrial and OEM, IoT Sensors and Smart-Infrastructure, and More), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa).

Global Primary Battery Market Trends and Insights

Surging Demand from Smart-Home & IoT Single-Use Sensors

LoRaWAN networks surpassed 125 million connected devices in 2024, growing 25% year over year, and most of these endpoints, such as door, leak, and occupancy sensors, are engineered for up to 10 years of operation on a single AA or coin-cell. Deployers avoid the USD 15-30 per node expense of adding recharging infrastructure, keeping the total cost of ownership low. Wi-Fi HaLow chipsets from multiple vendors promise a decade of runtime on two AA alkaline cells, which enables retrofits in commercial buildings without wiring for power. Although the GSM Association expects 1.1 billion ambient IoT devices by 2030, roughly 473 million units will still rely on primary batteries in locations that lack sufficient light for energy harvesting. Supercapacitors specified in ITU-T L.1310 offer hundreds of thousands of cycles but only fleeting backup time, confirming their complementary, not substitutive, role against long-duration primary chemistries.

Rapid Growth of Off-Grid Medical Devices in Emerging Markets

The World Health Organization reported in 2024 that facilities serving 1 billion people in sub-Saharan Africa and South Asia still lack reliable electricity, spurring adoption of pulse oximeters, portable ultrasound units, and vaccine monitors powered by primary lithium cells that deliver a decade-long shelf life. Solar-plus-storage microgrids financed by multilateral banks often reserve these cells for low-drain instrumentation where the cost of battery-management systems outweighs the price of periodic replacement. Global shipments of wearable medical devices reached 556.5 million units in mid-2025, 18% of which require silver-oxide or lithium coin cells to meet strict volumetric-energy-density needs. Zinc-air button cells remain dominant in hearing aids because they deliver 1.4 V and up to 650 mAh in tiny housings that rechargeable options cannot match without sacrificing comfort.

Competition from Secondary Batteries & Super-Capacitors

Rechargeable lithium-ion captured 83% of global battery capacity in 2025, pushing pack prices below USD 100 per kWh and eroding primary share in peripherals, speakers, and grooming devices. Despite energy-density limits, supercapacitors boasting 500,000-plus cycles are gaining ground in telecom backup, though they cannot supply multi-year, low-drain power. Nickel-metal-hydride AA cells continue to replace alkaline primaries in mid-drain consumer gear, while counterfeit alkaline imports further depress prices and compromise safety.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Defense Portable Electronics Budgets

- Shift Toward Mercury-Free Chemistries & Green Purchasing Mandates

- Extended Producer Responsibility Fees Inflating Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Primary lithium variants are projected to post a 9.5% CAGR between 2026 and 2031, the quickest within the primary battery market, as industrial metering and defense communications migrate to cells that operate from -40 °C to +85 °C at 3.0-3.6 V per cell. Conversely, alkaline held 63.5% revenue share in 2025 thanks to ubiquitous retail distribution. Zinc-air dominates hearing aids with 1.4-V output and up to 650 mAh capacity, while silver-oxide button cells sustain premium pricing in precision watches and glucose monitors. Recent U.S. import data show manganese-ore volumes escalating as manufacturers hedge against Chinese refining dominance.

Alkaline incumbents defend share through materials science: Panasonic's EVOLTA NEO uses high-purity manganese dioxide with titanium additives to deliver 1.3 times longer runtime. Meanwhile, nickel-zinc variants remain niche due to limited shelf life. Zinc-carbon cells persist in price-sensitive segments but are losing ground as alkaline approaches price parity, reinforcing the gradual premiumization of the primary battery market.

Complete Report Scope:

- By Type

- Alkaline

- Primary Lithium (Li-MnO2, Li-SOCl2, Li-CFx)

- Zinc-Air

- Zinc-Carbon/Chloride

- Silver-Oxide and Others

- By Form Factor

- Cylindrical (AA, AAA, C, D)

- Coin and Button Cells

- Prismatic/Packaged

- Others (Special shapes)

- By Application

- Consumer Electronics

- Industrial and OEM

- Medical and Healthcare

- Defence and Aerospace

- IoT Sensors and Smart-Infrastructure

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Spain

- NORDIC Countries

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Australia and New Zealand

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Egypt

- Rest of Middle East and Africa

- North America

Geography Analysis

Asia-Pacific commanded 46.1% of revenue in 2025, reflecting China's vertically integrated cost leadership across manganese dioxide refining, zinc powder production, and cell assembly. India's Production-Linked Incentive scheme earmarked 18 GWh of battery capacity, largely for lithium-ion EV packs, leaving primary cell output concentrated in smaller domestic plants. Japan's Nishikinohama factory, ramped up in late 2023, produces 48 million alkaline cells monthly, providing a non-Chinese source for premium EVOLTA NEO products. Emerging ASEAN hubs, Thailand, Vietnam, and Indonesia, are attracting coin-cell assembly for hearing aids, leveraging low labor costs and supply-chain proximity.

The Middle East & Africa region is expected to post a 9.0% CAGR to 2031, driven by decentralized-energy programs. The World Bank estimates 640-650 million people in sub-Saharan Africa still lack grid power, prompting solar-plus-microgrid deployments that reserve primary batteries for low-drain monitoring. South Africa's 360 MW battery tender in 2024, and its 1,200 MW pipeline, principally features rechargeable chemistries for long-duration discharge, leaving primary cells in peripheral telemetry roles. Counterfeit batteries remain pervasive, undermining safety and eroding legitimate brand share.

North America and Europe are consolidating around premium niches. Energizer received USD 112.4 million in Section 45X credits in fiscal 2025, underpinning domestic production. Its May 2025 purchase of Advanced Power Solutions NV added Polish capacity, albeit at a short-term margin cost. EU EPR mandates continue to lift compliance expenses, which established players can absorb more readily than new entrants. South American growth centers on Brazil and Argentina as e-commerce unlocks rural demand, though logistics obstacles in the Amazon and Patagonia impede deeper penetration.

- Duracell Inc.

- Energizer Holdings Inc.

- Panasonic Energy Co., Ltd.

- GP Batteries International Ltd.

- Saft (TotalEnergies)

- Ultralife Corporation

- FDK Corporation

- Varta AG

- Maxell Holdings, Ltd.

- Sony (Murata Energy)

- Rayovac (Spectrum Brands)

- Fujitsu Batteries

- Camelion Battery Co., Ltd.

- Philips Lighting (Signify)

- Zhejiang Mustang Battery

- EVE Energy Co., Ltd.

- Tianqiu (T&E)

- Renata SA (Swatch Group)

- Xiamen 3-Circle Battery

- Tenergy Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging demand from smart-home & IoT single-use sensors

- 4.2.2 Rapid growth of off-grid medical devices in emerging markets

- 4.2.3 Expansion of defence portable electronics budgets

- 4.2.4 Shift toward mercury-free chemistries & green purchasing mandates

- 4.2.5 Mainstream consumer-electronics replacement cycle

- 4.2.6 E-commerce penetration widening retail reach

- 4.3 Market Restraints

- 4.3.1 Competition from secondary batteries & super-capacitors

- 4.3.2 Extended Producer-Responsibility (EPR) fees inflating costs

- 4.3.3 Raw-material price volatility (zinc, lithium, manganese)

- 4.3.4 Counterfeit battery inflow in Asia & Africa

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Alkaline

- 5.1.2 Primary Lithium (Li-MnO2, Li-SOCl2, Li-CFx)

- 5.1.3 Zinc-Air

- 5.1.4 Zinc-Carbon/Chloride

- 5.1.5 Silver-Oxide and Others

- 5.2 By Form Factor

- 5.2.1 Cylindrical (AA, AAA, C, D)

- 5.2.2 Coin and Button Cells

- 5.2.3 Prismatic/Packaged

- 5.2.4 Others (Special shapes)

- 5.3 By Application

- 5.3.1 Consumer Electronics

- 5.3.2 Industrial and OEM

- 5.3.3 Medical and Healthcare

- 5.3.4 Defence and Aerospace

- 5.3.5 IoT Sensors and Smart-Infrastructure

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Spain

- 5.4.2.5 NORDIC Countries

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 ASEAN Countries

- 5.4.3.6 Australia and New Zealand

- 5.4.3.7 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Egypt

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Duracell Inc.

- 6.4.2 Energizer Holdings Inc.

- 6.4.3 Panasonic Energy Co., Ltd.

- 6.4.4 GP Batteries International Ltd.

- 6.4.5 Saft (TotalEnergies)

- 6.4.6 Ultralife Corporation

- 6.4.7 FDK Corporation

- 6.4.8 Varta AG

- 6.4.9 Maxell Holdings, Ltd.

- 6.4.10 Sony (Murata Energy)

- 6.4.11 Rayovac (Spectrum Brands)

- 6.4.12 Fujitsu Batteries

- 6.4.13 Camelion Battery Co., Ltd.

- 6.4.14 Philips Lighting (Signify)

- 6.4.15 Zhejiang Mustang Battery

- 6.4.16 EVE Energy Co., Ltd.

- 6.4.17 Tianqiu (T&E)

- 6.4.18 Renata SA (Swatch Group)

- 6.4.19 Xiamen 3-Circle Battery

- 6.4.20 Tenergy Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

一次電池市場規模、佔有率、趨勢和預測:按類型、最終用途行業和地區分類,2026-2034年

一次電池市場規模、佔有率、趨勢和預測:按類型、最終用途行業和地區分類,2026-2034年 一次電池市場-全球產業規模、佔有率、趨勢、機會和預測:按類型、應用、分銷管道、最終用戶、地區和競爭格局分類,2021-2031年

一次電池市場-全球產業規模、佔有率、趨勢、機會和預測:按類型、應用、分銷管道、最終用戶、地區和競爭格局分類,2021-2031年 2026年全球鋰一次電池市場報告N型電池全球市場報告(2026年)

2026年全球鋰一次電池市場報告N型電池全球市場報告(2026年) 鹼性一次電池市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2024-2032 年)初級消費電池市場-全球產業規模、佔有率、趨勢、機會及預測(按電池化學成分、應用、地區和競爭情況,2020-2030 年預測)

鹼性一次電池市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2024-2032 年)初級消費電池市場-全球產業規模、佔有率、趨勢、機會及預測(按電池化學成分、應用、地區和競爭情況,2020-2030 年預測) 2025-2029年全球一次電池市場

2025-2029年全球一次電池市場 亞太地區一次電池-市場佔有率分析、產業趨勢和成長預測(2025-2030 年)南美洲一次電池:市場佔有率分析、產業趨勢、成長預測(2025-2030)

亞太地區一次電池-市場佔有率分析、產業趨勢和成長預測(2025-2030 年)南美洲一次電池:市場佔有率分析、產業趨勢、成長預測(2025-2030)