|

市場調查報告書

商品編碼

2073454

印度種子加工:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)India Seed Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

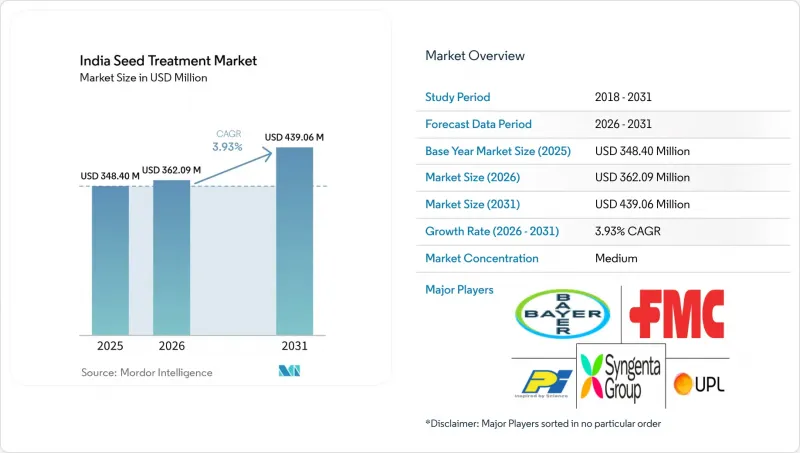

據 Mordor Intelligence 稱,印度種子加工市場預計到 2026 年價值 3.6209 億美元,高於 2025 年的 3.484 億美元,預計到 2031 年將達到 4.3906 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 3.93%。

本報告按功能(殺菌劑、殺蟲劑、殺線蟲劑)和作物類型(經濟作物、水果和蔬菜、穀物、豆類和油籽、草坪和觀賞植物)進行分類。市場預測以價值(美元)和數量(公噸)表示。

印度種子加工市場趨勢與洞察

引入生物種子處理

生物種子處理技術正在改變印度的種子處理市場,其提供的持續植物健康益處遠超短期病蟲害防治。快速註冊流程使得特性明確的微生物菌株可在12-18個月內獲得批准——僅為傳統流程的一半——從而降低了合規成本。農民青睞以芽孢桿菌和木黴為基礎的棉花、大豆和蔬菜處理產品,因為它們能夠增強根系活力、促進養分吸收並提高抗旱性。出口型生產商也非常青睞這些無殘留處理方法,因為它們符合歐盟嚴格的殘留標準。在卡納塔克邦和馬哈拉斯特拉邦,聯邦政府對經認證的生物材料提供50%的補貼,進一步加速了生物處理技術的普及。因此,印度的種子處理市場正迅速從純粹的化學處理轉向一系列符合永續農業目標的綜合性生物產品。

精密農業的擴展

精密農業技術正在革新種子處理方法,使農民能夠根據田間具體的病蟲害爆發情況和土壤條件進行差異化施藥。將無人機田間調查與GPS導航播種機結合,可以幫助農民最佳化施藥量,在降低投入成本的同時維持防治效果。這種技術融合尤其惠及旁遮普邦、哈里亞納邦和馬哈拉斯特拉邦邦西部的大型商業作物種植戶,在這些地區,精準施藥系統能夠有效地應用於機械化耕作作業。隨著設備成本的降低和政府支持的農業技術中心的技術支援基礎設施的擴展,這一趨勢正在加速發展。此外,精準噴灑透過確保最佳劑量,最大限度地保護作物並最大限度地減少對環境的影響,從而解決了化學殘留的監管問題。

進口導致原物料價格波動

印度對進口技術級活性成分的依賴制約了市場擴張,並造成了巨大的成本壓力,限制了農民採用高品質的種子處理劑。印度約70%的技術級農藥活性成分依賴進口,其中超過60%來自中國,使得印度極易受到供應鏈中斷和價格波動的影響。 2024年,由於環境法規的影響,中國製造業受到衝擊,導致包括Imidacloprid和Thiamethoxam在內的關鍵活性成分價格上漲了25%至40%,迫使國內製劑生產商在自行承擔成本或將價格上漲轉嫁給農民之間做出選擇。這種價格波動對缺乏足夠財力應對投入成本波動的中小型企業影響尤為嚴重,可能導致市場結構重組,使規模更大、財務更穩健的企業佔據優勢。外匯波動進一步加劇了這一局面,盧比對人民幣貶值直接影響了種子處理劑生產商的進口成本。

細分市場分析

預計到2025年,殺蟲劑將佔據89.60%的市場佔有率,這反映了印度與作物害蟲持續鬥爭的現狀,以及早期植物保護對最終產量至關重要。該細分市場到2031年的複合年成長率(CAGR)為3.99%,顯示在商業作物種植面積擴大和氣候變遷導致的病蟲害壓力加劇的推動下,市場將持續成長。殺蟲劑種子處理能夠有效防止幼苗因白蟻、金針蟲和地老虎等土壤害蟲而死亡,從而佔據絕對主導地位,這主要得益於其立竿見影的效果。這些害蟲會摧毀不同農業氣候區的作物種植。儘管國際市場對其監管日益嚴格,但由於新菸鹼類殺蟲劑,特別是Imidacloprid和噻Thiamethoxam嗪製劑,憑藉其內吸性和持久的保護作用,仍然受到農民的青睞。

殺菌劑雖然市佔率較小,但策略意義重大,主要用於防治種子和土壤傳播的病害,這些病害在高濕度環境和集約化種植系統中會造成顯著的產量損失。隨著人們對真菌抗性管理的認知不斷提高,以及對預防性病害控制策略的需求日益成長(這些策略可以減少後續的葉面噴布),殺菌劑市場也從中受益。殺線蟲劑則佔據著獨特的市場地位,主要用於蔬菜和經濟作物等高價值作物,因為線蟲造成的損害足以抵消高昂的防治成本。印度農業研究理事會(ICAR)對綜合蟲害管理的重視,為同時防治多種害蟲的聯合防治方案創造了機遇,並有可能重塑傳統的功能性細分格局。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

- 調查方法

第2章:本報告的內容

第3章:執行摘要和主要發現

第4章:主要產業趨勢

- 每公頃農藥使用量

- 活性成分價格分析

- 法律規範

- 印度

- 價值鍊和通路分析

- 市場促進因素

- 生物種子處理技術的引入

- 精密農業的整合

- 政府對永續投入的支持

- 符合殘留物標準的農產品出口需求

- 種子披衣技術的創新

- 綜合蟲害管理方案

- 市場限制因素

- 進口導致原物料價格波動

- 法規核准的複雜性

- 東部各省分散的經銷網路

- 外匯波動導致進口成本上升

第5章 市場規模與成長預測

- 功能

- 消毒劑

- 殺蟲劑

- 尼馬奇賽德

- 作物類型

- 經濟作物

- 水果和蔬菜

- 穀物和穀類

- 豆類和油籽

- 草坪和觀賞植物

第6章 競爭情勢

- 關鍵策略趨勢

- 市佔率分析

- 企業狀況

- 公司簡介。

- ADAMA Agricultural Solutions Ltd

- BASF SE

- Bayer AG

- Corteva Agriscience

- Crystal Crop Protection Ltd

- FMC Corporation

- PI Industries

- Rallis India Ltd

- Syngenta Group

- UPL Limited

- Dhanuka Agritech Ltd

- Sumitomo Chemical India Ltd

- Nagarjuna Agrichem Ltd

- Bharat Rasayan Ltd

- Meghmani Organics Ltd

- NACL Industries Ltd

- Sharda Cropchem Ltd

- Gharda Chemicals Ltd

- Tagros Chemicals India Pvt Ltd

- Willowood Chemicals Pvt Ltd

第7章 作物保護化學品公司執行長面臨的關鍵策略挑戰

According to Mordor Intelligence, india seed treatment market size in 2026 is estimated at USD 362.09 million, growing from 2025 value of USD 348.4 million with 2031 projections showing USD 439.06 million, growing at 3.93% CAGR over 2026-2031.

This report is Segmented by Function (Fungicide, Insecticide, and Nematicide), Crop Type (Commercial Crops, Fruits and Vegetables, Grains and Cereals, Pulses and Oilseeds, and Turf and Ornamental). The Market Forecasts are Provided in Terms of Value (USD) and Volume(Metric Tons).

India Seed Treatment Market Trends and Insights

Biological seed treatment adoption

Biological seed treatments are reshaping the India seed treatment market by offering sustained plant health benefits that extend beyond short-term pest knockdown. Fast-tracked registration processes now clear well-characterized microbial strains in 12-18 months, half the earlier period, cutting compliance costs . Farmers favor Bacillus- and Trichoderma-based products for cotton, soybean, and vegetables because they enhance root vigor, nutrient uptake, and drought resilience. Export-oriented growers appreciate these residue-free treatments in meeting the stringent maximum residue limits enforced by the European Union. Federal subsidies covering 50% of certified biological input costs in Karnataka and Maharashtra further accelerate adoption. As a result, the India seed treatment market is rapidly shifting from purely chemical options toward integrated biological portfolios that align with sustainable agriculture goals.

Increasing precision agriculture adoption

Precision agriculture technologies are revolutionizing seed treatment application methods, enabling variable-rate treatments based on field-specific pest pressure and soil conditions. The integration of drone-based scouting and GPS-guided planting equipment allows farmers to optimize treatment rates, reducing input costs while maintaining efficacy levels. This technological convergence particularly benefits large-scale commercial crop producers in Punjab, Haryana, and western Maharashtra, where mechanized farming operations can leverage precision application systems effectively. The trend accelerates as equipment costs decline and technical support infrastructure expands through government-backed agricultural technology centers. Precision application also addresses regulatory concerns about chemical residues by ensuring optimal dosing that minimizes environmental impact while maximizing crop protection benefits.

Raw Material Price Volatility from Imports

Import dependency for technical-grade active ingredients creates significant cost pressures that constrain market expansion and limit farmer adoption of premium seed treatments. India imports approximately 70% of technical-grade pesticide ingredients, with China supplying over 60% of these materials, creating vulnerability to supply chain disruptions and price fluctuations. The 2024 disruptions in Chinese manufacturing due to environmental regulations resulted in 25-40% price increases for key active ingredients, including imidacloprid and thiamethoxam, forcing domestic formulators to either absorb costs or pass increases to farmers. This volatility particularly impacts smaller domestic companies lacking financial buffers to manage input cost fluctuations, potentially leading to market consolidation favoring larger players with stronger balance sheets. Currency fluctuations add another layer of complexity, with rupee depreciation against the Chinese yuan directly impacting import costs for seed treatment manufacturers.

Other drivers and restraints analyzed in the detailed report include:

- Government Support for Sustainable Formulations

- Export demand for residue-compliant produce

- Regulatory Approval Complexities

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Insecticides command an overwhelming 89.60% market share in 2025, reflecting India's persistent battle against crop-damaging pests and the critical importance of early-stage plant protection in determining final yields. The segment's 3.99% CAGR through 2031 indicates sustained growth driven by expanding acreage under commercial crops and increasing pest pressure from climate variability. This dominance stems from the immediate and visible impact of insecticidal seed treatments in preventing seedling mortality from soil-dwelling pests like termites, wireworms, and cutworms that can devastate crop establishment across diverse agro-climatic zones. Neonicotinoid-based treatments, particularly imidacloprid and thiamethoxam formulations, maintain preference among farmers for their systemic action and extended protection periods, despite regulatory scrutiny in international markets.

Fungicides represent a smaller but strategically important segment, addressing seed and soil-borne diseases that cause significant yield losses in high-moisture environments and intensive cropping systems. The segment benefits from increasing awareness of fungal resistance management and the need for preventive disease control strategies that reduce subsequent foliar applications. Nematicides occupy a niche position, primarily used in high-value crops like vegetables and commercial crops where nematode damage justifies premium treatment costs. The Indian Council of Agricultural Research's emphasis on integrated pest management creates opportunities for combination treatments that address multiple pest categories simultaneously, potentially reshaping traditional functional segmentation.

Complete Report Scope:

- Function

- Fungicides

- Insecticides

- Nematicide

- Crop Type

- Commercial Crops

- Fruits & Vegetables

- Grains & Cereals

- Pulses & Oilseeds

- Turf & Ornamental

List of Companies Covered in this Report:

- ADAMA Agricultural Solutions Ltd

- BASF SE

- Bayer AG

- Corteva Agriscience

- Crystal Crop Protection Ltd

- FMC Corporation

- PI Industries

- Rallis India Ltd

- Syngenta Group

- UPL Limited

- Dhanuka Agritech Ltd

- Sumitomo Chemical India Ltd

- Nagarjuna Agrichem Ltd

- Bharat Rasayan Ltd

- Meghmani Organics Ltd

- NACL Industries Ltd

- Sharda Cropchem Ltd

- Gharda Chemicals Ltd

- Tagros Chemicals India Pvt Ltd

- Willowood Chemicals Pvt Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 India

- 4.4 Value Chain & Distribution Channel Analysis

- 4.5 Market Drivers

- 4.5.1 Biological seed treatment adoption

- 4.5.2 Precision agriculture integration

- 4.5.3 Government support for sustainable inputs

- 4.5.4 Export demand for residue-compliant produce

- 4.5.5 Seed-coating technology innovation

- 4.5.6 Integrated pest management programs

- 4.6 Market Restraints

- 4.6.1 Raw material price volatility from imports

- 4.6.2 Regulatory approval complexities

- 4.6.3 Fragmented distribution networks in eastern states

- 4.6.4 Currency fluctuations raising import costs

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Function

- 5.1.1 Fungicides

- 5.1.2 Insecticides

- 5.1.3 Nematicide

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 ADAMA Agricultural Solutions Ltd

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 Crystal Crop Protection Ltd

- 6.4.6 FMC Corporation

- 6.4.7 PI Industries

- 6.4.8 Rallis India Ltd

- 6.4.9 Syngenta Group

- 6.4.10 UPL Limited

- 6.4.11 Dhanuka Agritech Ltd

- 6.4.12 Sumitomo Chemical India Ltd

- 6.4.13 Nagarjuna Agrichem Ltd

- 6.4.14 Bharat Rasayan Ltd

- 6.4.15 Meghmani Organics Ltd

- 6.4.16 NACL Industries Ltd

- 6.4.17 Sharda Cropchem Ltd

- 6.4.18 Gharda Chemicals Ltd

- 6.4.19 Tagros Chemicals India Pvt Ltd

- 6.4.20 Willowood Chemicals Pvt Ltd

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

種子加工市場:按類型、作物和地區分類

種子加工市場:按類型、作物和地區分類 再生種子處理市場預測至2034年-按產品類型、作物類型、功能、配方、最終用戶、分銷管道和地區分類的全球分析

再生種子處理市場預測至2034年-按產品類型、作物類型、功能、配方、最終用戶、分銷管道和地區分類的全球分析 大豆殺菌劑種子處理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

大豆殺菌劑種子處理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 種子處理市場:2026-2032年全球市場預測(依產品類型、作物類型、配方類型、處理方案、認證、應用環境、最終用戶和分銷管道分類)美國種子加工:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

種子處理市場:2026-2032年全球市場預測(依產品類型、作物類型、配方類型、處理方案、認證、應用環境、最終用戶和分銷管道分類)美國種子加工:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) 種子處理市場規模、佔有率、趨勢和預測:按類型、應用方法、作物類型、功能和地區分類,2026-2034年

種子處理市場規模、佔有率、趨勢和預測:按類型、應用方法、作物類型、功能和地區分類,2026-2034年 2026年全球種子處理市場報告殺蟲燈市場:依光源、技術、應用、最終用途和銷售管道,全球預測(2026-2032年)

2026年全球種子處理市場報告殺蟲燈市場:依光源、技術、應用、最終用途和銷售管道,全球預測(2026-2032年) 種子處理市場規模、佔有率、成長及全球產業分析:按類型和應用分類,區域洞察及2026-2034年預測2026年全球種子處理設備市場報告

種子處理市場規模、佔有率、成長及全球產業分析:按類型和應用分類,區域洞察及2026-2034年預測2026年全球種子處理設備市場報告