|

市場調查報告書

商品編碼

2066634

大豆殺菌劑種子處理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Soybean Fungicide Seed Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

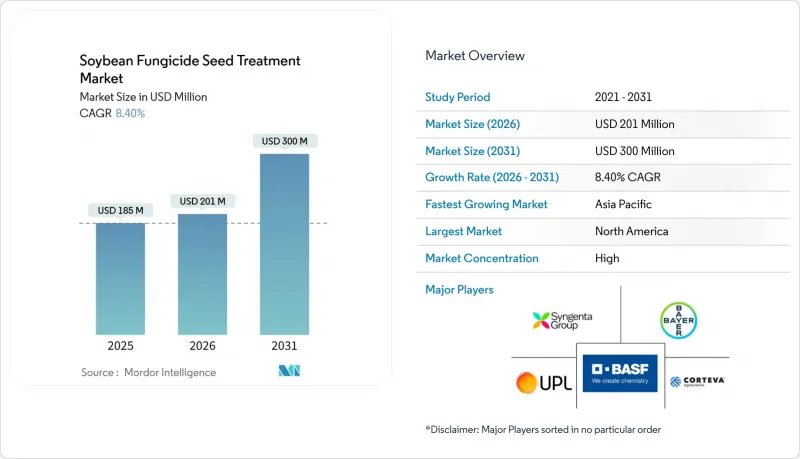

根據 Mordor Intelligence 預測,大豆殺菌劑種子處理市場規模預計將在 2025 年達到 1.85 億美元,在 2026 年成長至 2.01 億美元,並在 2031 年達到 3 億美元,2026 年至 2031 年的複合年成長率為 8.4%。

本報告按類型(化學和非化學/生物)和地區(北美、南美、歐洲、亞太地區以及中東和非洲)進行細分。市場預測以貨幣價值(美元)表示。

全球大豆殺菌劑種子處理市場趨勢及洞察

大豆疫黴菌抗殺菌劑菌株的發生率增加。

田間調查已發現多種大豆疫黴變種能夠克服長期以來被認為有效的Rps基因,從而降低了遺傳抗性,並促使種植者採用多模式種子處理方法。這種變異性正在加速苯醯胺類、乙醯胺類和生物拮抗劑等聯合療法的應用。此外,南美洲的研究人員報告了對嘧菌酯具有抗性的炭疽菌,凸顯了開發新型活性成分的必要性。病原菌族群的演化速度超過了新型活性成分上市的速度,因此種植者需要採用具有多種作用機制的種子處理方法。

對高品質農作物產量的需求不斷成長

由於出口商面臨對黴菌毒素和蛋白質含量差異更嚴格的監管,種子處理已成為至關重要的品質保證措施。例如,中國進口商經常拒收Deoxynivalenol)含量超過1ppm的貨物,而控制發芽期間的鐮刀菌感染可以降低這種風險。在阿根廷,為了與歐洲榨油廠簽訂優質契約,生產商正在其所有育苗田中推行標準化的種子處理流程。據種子企業稱,目前大多數原種都經過處理,以確保品種純度。

化學殺菌劑對土壤微生物組的不利影響

由於化學殺菌劑會對有益土壤微生物,特別是固氮根瘤菌屬(Rhizobium)產生不利影響,因此在大豆種子處理中使用化學殺菌劑正受到越來越多的限制。這些殺菌劑會抑制根瘤的形成,可能降低生物固氮的效率。發表在《生物科學》(Bioscience)雜誌上的一項研究表明,經殺菌劑處理的大豆種子根瘤數量減少了36%,對植物-微生物共生關係和養分吸收產生了負面影響。這種減少可能會降低低肥力土壤的產量,因此需要加強監管,並促進對微生物組友善或生物種子處理的方法。

細分市場分析

預計到2025年,大豆殺菌劑種子處理市場中,化學製劑將佔據最大的市場佔有率,達到68%。同時,生物來源產品的市場規模預計將在2026年至2031年間以9.3%的複合年成長率(CAGR)高速成長。三唑類和苯醯胺類複方製劑因其長期應用歷史、每公頃成本效益高以及廣泛的監管批准,繼續被廣泛用於防治疫黴屬和絲核菌屬真菌,成為一般作物的主要防治劑。然而,巴西和美國對抗藥性的擔憂促使作物輪作和多種殺菌劑聯合使用,促使種植者選擇優質的多成分組合藥物。

生物種子處理劑含有芽孢桿菌和木黴等活性微生物,以及發酵代謝物。例如,科迪華農業科技公司(Corteva AgriScience)的假單胞菌屬產品Lumicena和先正達公司(Syngenta)的芽孢桿菌屬產品Saltro,都顯示了高效能生物殺菌劑的應用日益廣泛。包封技術的進步,例如藻酸鹽基質,提高了保存期限和種子活力。如果效果持續提升,到2031年,生物種子處理劑可望佔據與傳統方法相當的市場佔有率,屆時競爭的焦點將轉向擁有龐大微生物庫和大規模發酵能力的公司。

區域分析

2025年,北美在大豆殺菌劑種子處理劑市場佔最大佔有率,達34%。這主要得益於玉米帶和草原地區廣泛採用包衣處理技術。由於種植面積趨於飽和,預計2031年,市場成長將較為溫和。然而,隨著加工商採用大氣壓力冷等離子設備,發芽率提高,合成材料的使用量減少,優質化趨勢日益明顯。此外,與氣候智慧型農業相關的補貼正在加速向生物來源藥劑和採用精準噴灑的聯合處理方式的轉變,即使種植面積趨於穩定,也有助於維持盈利能力。

預計亞太市場將在2026年至2031年間以9.8%的複合年成長率(CAGR)實現最高成長。這主要歸功於生產商積極應對亞洲大豆銹病、疫黴根腐病和豆莖癭病等挑戰。印度和中國目前仍處於應用初期,滲透率較低。然而,政府為小規模農戶提供防腐種子補貼的措施正在幫助縮小這一差距。在巴西,約四分之三的大豆種子已經包衣,但隨著馬托格羅索州和巴拉那州等地區病害威脅的加劇,預計銷售量將持續成長,同時市場也將轉向多功能和生物來源產品。

在歐洲、中東和非洲,大豆面積相對較小,由於「從農場到餐桌」戰略下更嚴格的殘留物監管以及多種三唑類殺菌劑的逐步淘汰,預計其成長速度將會放緩。在歐洲,德國、法國和義大利等國的有機農業和綜合蟲害管理(IPM)生產商率先採用了BASF農業解決方案公司和諾維信公司的微生物包衣產品,但整體銷售量仍然有限。在非洲,埃及和南非等依賴灌溉的地區正在使用種子處理劑來降低病原體高發生率的威脅。同時,土耳其正崛起為製劑中心,向周邊市場供應產品。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 大豆疫黴菌抗性菌株發生率增加

- 對優質農產品的需求不斷成長

- 政府對引進種子處理技術提供補貼

- 低溫等離子塗層技術的擴展

- 利用無人機進行種子製粒的引入

- 將基於RNA的殺菌劑整合到種子處理體系中

- 市場限制因素

- 化學殺菌劑對土壤微生物組的不利影響

- 嚴格的農藥管理規定

- 主要三唑類活性成分供應鏈的波動

- 農民對低有機質土壤中植物毒性的認知

- 監理情勢

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 類型

- 化學品

- 非化學/生物

- 地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 其他北美國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 泰國

- 越南

- 澳洲

- 其他亞太國家

- 中東

- 土耳其

- 沙烏地阿拉伯

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Syngenta Group Co., Ltd.

- Bayer AG

- BASF SE

- Corteva, Inc.

- UPL Limited

- Sumitomo Chemical Company, Limited

- FMC Corporation

- Nufarm Limited

- Novozymes A/S

- Pro Farm Group Inc.

- Valent USA LLC

第7章 市場機會與未來展望

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 大豆疫黴菌抗性菌株發生率增加

- 對優質農產品的需求不斷成長

- 政府對引進種子處理技術提供補貼

- 低溫等離子塗層技術的擴展

- 利用無人機進行種子製粒的引入

- 將基於RNA的殺菌劑整合到種子處理體系中

- 市場限制因素

- 化學殺菌劑對土壤微生物組的不利影響

- 嚴格的農藥管理規定

- 主要三唑類活性成分供應鏈的波動

- 農民對低有機質土壤中植物毒性的認知

- 監理情勢

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 類型

- 化學品

- 非化學/生物

- 地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 其他北美國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 泰國

- 越南

- 澳洲

- 其他亞太國家

- 中東

- 土耳其

- 沙烏地阿拉伯

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Syngenta Group Co., Ltd.

- Bayer AG

- BASF SE

- Corteva, Inc.

- UPL Limited

- Sumitomo Chemical Company, Limited

- FMC Corporation

- Nufarm Limited

- Novozymes A/S

- Pro Farm Group Inc.

- Valent USA LLC

第7章 市場機會與未來展望

According to Mordor Intelligence, the soybean fungicide seed treatment market was valued at USD 185 million in 2025 and is projected to grow from USD 201 million in 2026 to USD 300 million by 2031, registering a CAGR of 8.4% from 2026 to 2031.

This report is Segmented by Type (Chemicals and Non-Chemical/Biological), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Soybean Fungicide Seed Treatment Market Trends and Insights

Increasing Incidence of Fungicide-Resistant Phytophthora sojae Strains

Field surveys have identified multiple Phytophthora sojae pathotypes capable of overcoming long-standing Rps genes, reducing genetic resistance, and driving growers toward multi-mode seed treatments. Variability is accelerating the adoption of stacked chemistries that combine phenylamides with ethaboxam and biological antagonists. Additionally, South American researchers have reported azoxystrobin-resistant Colletotrichum truncatum, highlighting the need for new active ingredients. Pathogen populations are evolving more rapidly than the introduction of new active ingredients to the market, prompting growers to adopt seed treatments with multiple modes of action.

Growing Demand for High-Quality Crop Yields

Exporters are facing stricter regulations on mycotoxins and protein variability, making seed treatment an essential quality assurance measure. For instance, Chinese importers often reject shipments containing deoxynivalenol levels exceeding 1 part per million, a risk mitigated by managing Fusarium infections during germination. In Argentina, producers aiming for premium contracts with European crushers have standardized seed treatment practices across multiplication plots. According to seed companies, most of the foundation seed lots are now treated to ensure varietal purity.

Adverse Effects of Chemical Fungicides on Soil Microbiota

The application of chemical fungicide seed treatments in soybean cultivation is facing growing limitations due to their negative impact on beneficial soil microbiota, particularly nitrogen-fixing Rhizobium species. These fungicides can interfere with root nodulation, thereby reducing the efficiency of biological nitrogen fixation. According to a study published in Bioscience, soybean seeds treated with fungicides exhibited a 36% decrease in root nodules, adversely affecting plant-microbe symbiosis and nutrient absorption . This reduction can constrain yields in low-fertility soils, leading to increased regulatory scrutiny and driving the adoption of microbiome-friendly or biological seed treatment alternatives.

Other drivers and restraints analyzed in the detailed report include:

- Government Subsidies for Seed-Treatment Adoption

- Expansion of Cold-Plasma Coating Technologies

- Stringent Regulations on Agrochemicals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Chemical formulations accounted for the largest market share, at 68%, for the soybean fungicide seed treatment market in 2025. Meanwhile, the biological market size is projected to grow at the fastest CAGR of 9.3% from 2026 to 2031. Triazole and phenylamide combinations continue to be widely used for managing Phytophthora and Rhizoctonia due to their extensive field history, cost-effectiveness per hectare, and broad regulatory approvals, making them a staple across commodity crops. However, resistance concerns in Brazil and the United States are driving the adoption of rotation and stacking practices, encouraging growers to opt for premium multi-active blends.

Biological seed treatments include living microbes such as Bacillus and Trichoderma, along with fermentation-derived metabolites. Examples like Corteva Agriscience's Pseudomonas-based Lumisena and Syngenta's Bacillus-based Saltro highlight the growing adoption of high-performance biofungicides. Advances in encapsulation technologies, such as alginate matrices, have improved shelf life and on-seed viability. If efficacy continues to improve, biological seed treatments could achieve a comparable market share by 2031, shifting competition toward companies with extensive microbial libraries and large-scale fermentation capabilities.

Geography Analysis

North America accounted for the largest market share of 34% for soybean fungicide seed treatment revenue in 2025, driven by widespread coating practices across the Corn Belt and Prairie provinces. Growth through 2031 is projected to be moderate due to saturated acreage. However, premiumization trends are evident as processors adopt atmospheric-pressure cold-plasma units, which enhance germination and reduce synthetic inputs. Additionally, subsidies linked to climate-smart agriculture are facilitating the transition to biological and precision-applied stacks, helping to sustain revenue even as planted hectares stabilize.

The Asia-Pacific market size is projected to grow at the fastest CAGR of 9.8% from 2026 to 2031, as growers address challenges such as Asian soybean rust, Phytophthora root rot, and Diaporthe stem canker. India and China are at earlier stages of adoption, with lower penetration rates. However, government initiatives providing subsidized treated seeds to smallholders are helping to close the gap. In Brazil, where approximately three-quarters of soybean seeds are already coated, rising disease pressure in regions like Mato Grosso and Parana supports continued volume growth, alongside a shift toward multi-active or biological products.

Europe and the Middle East and Africa are projected to experience slower growth, due to smaller soybean acreage and stricter residue regulations under the Farm to Fork strategy, which is phasing out several triazoles. In Europe, organic and integrated pest management producers in countries such as Germany, France, and Italy are early adopters of microbial coatings from BASF SE agricultural solutions and Novozymes, though overall volumes remain limited. In Africa, irrigation-dependent regions in Egypt and South Africa rely on seed treatments to mitigate high pathogen pressure, while Turkey is emerging as a formulation hub serving neighboring markets.

- Syngenta Group Co., Ltd.

- Bayer AG

- BASF SE

- Corteva, Inc.

- UPL Limited

- Sumitomo Chemical Company, Limited

- FMC Corporation

- Nufarm Limited

- Novozymes A/S

- Pro Farm Group Inc.

- Valent U.S.A. LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing incidence of fungicide-resistant Phytophthora sojae strains

- 4.2.2 Growing demand for high-quality crop yields

- 4.2.3 Government subsidies for seed-treatment adoption

- 4.2.4 Expansion of cold-plasma coating technologies

- 4.2.5 Adoption of drone-enabled seed pelleting

- 4.2.6 Integration of RNA-based fungicides into seed-treatment stacks

- 4.3 Market Restraints

- 4.3.1 Adverse effects of chemical fungicides on soil microbiota

- 4.3.2 Stringent regulations on agrochemicals

- 4.3.3 Supply-chain volatility for key triazole actives

- 4.3.4 Farmer perception of phytotoxicity in low-organic-matter soils

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Force Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 Type

- 5.1.1 Chemical

- 5.1.2 Non-Chemical/Biological

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Mexico

- 5.2.1.4 Rest of North America

- 5.2.2 South America

- 5.2.2.1 Brazil

- 5.2.2.2 Argentina

- 5.2.2.3 Rest of South America

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 France

- 5.2.3.4 Spain

- 5.2.3.5 Italy

- 5.2.3.6 Russia

- 5.2.3.7 Rest of Europe

- 5.2.4 Asia-Pacific

- 5.2.4.1 China

- 5.2.4.2 Japan

- 5.2.4.3 India

- 5.2.4.4 Thailand

- 5.2.4.5 Vietnam

- 5.2.4.6 Australia

- 5.2.4.7 Rest of Asia-Pacific

- 5.2.5 Middle East

- 5.2.5.1 Turkey

- 5.2.5.2 Saudi Arabia

- 5.2.5.3 Rest of Middle East

- 5.2.6 Africa

- 5.2.6.1 South Africa

- 5.2.6.2 Egypt

- 5.2.6.3 Rest of Africa

- 5.2.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Syngenta Group Co., Ltd.

- 6.4.2 Bayer AG

- 6.4.3 BASF SE

- 6.4.4 Corteva, Inc.

- 6.4.5 UPL Limited

- 6.4.6 Sumitomo Chemical Company, Limited

- 6.4.7 FMC Corporation

- 6.4.8 Nufarm Limited

- 6.4.9 Novozymes A/S

- 6.4.10 Pro Farm Group Inc.

- 6.4.11 Valent U.S.A. LLC

7 Market Opportunities and Future Outlook

印度種子加工:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

印度種子加工:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 種子加工市場:按類型、作物和地區分類

種子加工市場:按類型、作物和地區分類 再生種子處理市場預測至2034年-按產品類型、作物類型、功能、配方、最終用戶、分銷管道和地區分類的全球分析

再生種子處理市場預測至2034年-按產品類型、作物類型、功能、配方、最終用戶、分銷管道和地區分類的全球分析 種子處理市場:2026-2032年全球市場預測(依產品類型、作物類型、配方類型、處理方案、認證、應用環境、最終用戶和分銷管道分類)美國種子加工:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

種子處理市場:2026-2032年全球市場預測(依產品類型、作物類型、配方類型、處理方案、認證、應用環境、最終用戶和分銷管道分類)美國種子加工:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) 種子處理市場規模、佔有率、趨勢和預測:按類型、應用方法、作物類型、功能和地區分類,2026-2034年

種子處理市場規模、佔有率、趨勢和預測:按類型、應用方法、作物類型、功能和地區分類,2026-2034年 2026年全球種子處理市場報告殺蟲燈市場:依光源、技術、應用、最終用途和銷售管道,全球預測(2026-2032年)

2026年全球種子處理市場報告殺蟲燈市場:依光源、技術、應用、最終用途和銷售管道,全球預測(2026-2032年) 種子處理市場規模、佔有率、成長及全球產業分析:按類型和應用分類,區域洞察及2026-2034年預測2026年全球種子處理設備市場報告

種子處理市場規模、佔有率、成長及全球產業分析:按類型和應用分類,區域洞察及2026-2034年預測2026年全球種子處理設備市場報告