|

市場調查報告書

商品編碼

2066390

美國種子加工:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)United States Seed Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

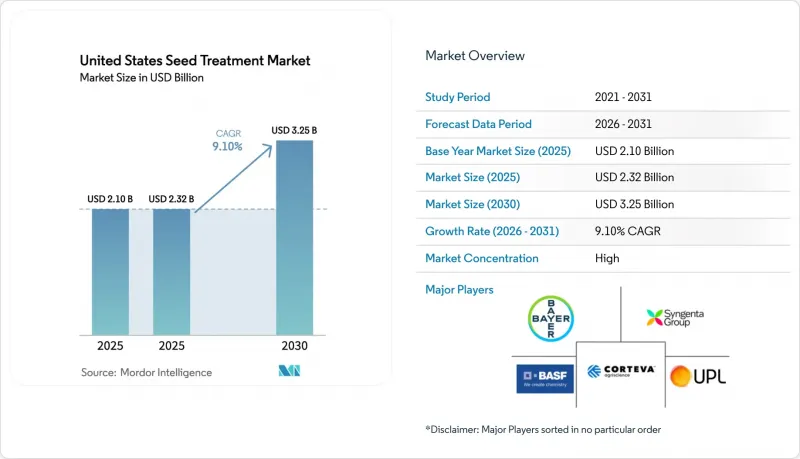

據 Mordor Intelligence 稱,2025 年美國種子處理市場價值為 21 億美元,預計到 2031 年將從 2026 年的 23.2 億美元成長至 32.5 億美元,預測期(2026-2031 年)複合年成長率為 9.10%。

本報告按產品類型(殺菌劑、殺蟲劑、殺線蟲劑)和作物類型(經濟作物、水果和蔬菜、穀物、豆類和油籽、草坪和觀賞植物)進行分類。市場預測以貨幣價值(美元)表示。

美國種子加工市場趨勢與洞察

對傳統農藥的監管壓力

2024年7月,美國環保署(EPA)更新了噻蟲胺、Imidacloprid和Thiamethoxam的職業接觸評估,加重了葉面噴布新菸鹼類殺蟲劑的合規負擔,並引導種植者轉向種子處理替代方案。計劃於2025年進行的標籤修訂預計將強制要求在田間噴灑時設置更大的緩衝區並更嚴格地使用個人防護設備,這將進一步強化種子處理是監管挑戰最小的選擇這一觀點。由於《瀕危物種法》規定的漫長磋商,除草劑的核准流程已經十分繁瑣,預計新的葉面噴布殺蟲劑也將面臨類似的障礙。種子製劑生產商正利用較短的重新註冊期,透過將現有活性成分重新組合成種子專用配方來縮短產品上市時間。因此,投資於專用種子製劑平台的公司不僅獲得了速度優勢,也贏得了種植者的信任,因為種植者更傾向於使用操作要求較低的產品。

將處理過的包覆作物種子的碳權額貨幣化

碳市場透過獎勵農民固碳來津貼覆蓋作物的種植,但種子處理的投入很少被納入這些協議中。自然資源保護局 (NRCS) 擴大了動態土壤特性監測的範圍,並為量化處理種子帶來的生物量增加的調查方法鋪平了道路。由於目前尚無實證研究將處理過的覆蓋作物的發芽與已驗證的碳增加聯繫起來,因此目前增加收益的前景仍停留在假設階段。早期採用者自行承擔種子處理的成本,希望未來能獲得可靠的結果,以便在短暫的秋季播種季節穩定播種。如果像 Verra 這樣的註冊機構發布包含種子在內的碳規則,製劑生產商將能夠提供處理和專案參與的打包服務,但在此之前,推廣動能仍將有限。

各州對新菸鹼類殺蟲劑監管的趨勢和影響

佛蒙特州第182號法案禁止2029年1月起使用新菸鹼類殺蟲劑處理過的大豆和穀物種子,紐約州和康乃狄克州的立法機構也在審議類似的法案。作為應對措施,供應商正在使用活性成分,例如先正達的普利那唑林(PLINAZOLIN),這是加拿大首個商業化用於穀物的此類產品,以及科迪華的LumiGEN組合藥物,這些配方使用非新菸鹼類殺蟲劑。雖然產品系列的分散增加了物流難度,但也為那些已獲得替代化學品早期註冊的靈活配方生產商帶來了機會。各州新菸鹼類殺蟲劑(新菸鹼)法規對市場的影響表明,美國種子處理市場將按監管區域分類。這將要求配方生產商管理多個產品系列,從而增加供應鏈物流的複雜性。另一方面,對於那些早期投資於非新菸鹼類替代品並搶先獲得監管部門批准的公司來說,這將是一個機會。

細分市場分析

殺菌劑佔最大的市場佔有率,預計到2025年將占美國種子處理市場46%的佔有率,幫助種植者對抗鐮刀菌、腐黴菌和立枯絲核菌等病害。其主導地位源自於殺菌劑在保護種子和幼苗免受土壤傳播和早期病害(如猝倒病、根腐病和種子腐爛病)侵害方面發揮的關鍵作用。殺菌劑的廣泛使用確保了植物的成活和均勻發芽,尤其是在玉米、大豆和小麥等作物中。大豆種植者經常使用殺菌劑處理種子,以保護作物免受腐霉菌和立枯絲核菌等病原體的侵害,如果不加以控制,這些病害會大幅減少植株數量。這種持續的預防性保護使得殺菌劑成為眾多種植區農民不可或缺的資源。

殺蟲劑產業是成長最快的領域,預計2026年至2031年將以13.5%的複合年成長率成長。這一成長主要受害蟲危害加劇、抗藥性問題以及作物早期保護需求的推動。諸如金針蟲、玉米種蠅和蚜蟲等害蟲持續威脅作物產量,促使農民採用殺蟲劑種子處理作為預防措施。隨著綜合蟲害管理(IPM)和精密農業實踐的日益普及,殺蟲劑的定向使用正根據田間具體風險逐步推進。易受早期蟲害侵害地區的玉米種植者傾向於選擇殺蟲劑處理過的種子,以防止播種損失並避免補種成本,這推動了該領域的快速擴張。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對傳統農藥的監管壓力

- 病蟲害防治中抗藥性管理的迫切性

- 過渡到聚合物封裝以減少灰塵

- 將經處理的覆蓋作物所產生的碳權額貨幣化

- 為提高作物產量,對農場種子加工的需求日益成長。

- 精密農業中數位處方栽培的引入

- 市場限制因素

- 大規模生產者整合對農業市場的影響

- 美國環保署 (EPA) 對新活性成分的核准出現延誤

- 各州對新菸鹼類殺蟲劑監管的趨勢和影響

- 彌合人們對完全有機農業系統認知的差距。

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 依產品類型

- 殺蟲劑

- 消毒劑

- 線蟲防治劑

- 複合材料

- 按作物類型

- 穀物和穀類

- 油籽/豆類

- 水果和蔬菜

- 經濟作物

- 草坪和觀賞植物

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Bayer AG

- Syngenta AG

- Corteva, Inc.

- BASF SE

- UPL Limited

- ADAMA Ltd.

- Germains Seed Technology Ltd.

- Incotec Group BV

- Valent USA LLC

- Nufarm Limited

- Chromatech Incorporated

- BrettYoung

- Loveland Products, Inc.(Nutrien Ltd.)

- Helena Agri-Enterprises, LLC

- Roquette Freres

- Precision Laboratories, LLC

第7章 市場機會與未來展望

According to Mordor Intelligence, the united states seed treatment market size was valued at USD 2.10 billion in 2025 and estimated to grow from USD 2.32 billion in 2026 to reach USD 3.25 billion by 2031, at a CAGR of 9.10% during the forecast period (2026-2031).

This report is Segmented by Product Type (Fungicide, Insecticide, and Nematicide), and by Crop Type (Commercial Crops, Fruits and Vegetables, Grains and Cereals, Pulses and Oilseeds, and Turf and Ornamental). The Market Forecasts are Provided in Terms of Value (USD).

United States Seed Treatment Market Trends and Insights

Regulatory Pressure on Conventional Pesticides

The Environmental Protection Agency updated occupational exposure assessments for clothianidin, imidacloprid, and thiamethoxam in July 2024, intensifying compliance burdens for foliar neonicotinoids and steering growers toward seed-applied alternatives. Anticipated 2025 label amendments are likely to mandate wider buffers and stricter personal protective equipment for broadcast sprays, reinforcing the perception that seed placement is the regulatory path of least resistance. Extended Endangered Species Act consultations have already lengthened herbicide approvals, signaling similar hurdles for new foliar insecticides. Seed formulators exploit a shorter re-registration window by reformulating existing actives into seed-specific packages, giving them a faster route to market. As a result, companies investing in dedicated seed formulation platforms capture both time-to-market advantage and stewardship goodwill with growers who prefer products that require fewer handler precautions.

Carbon-Credit Monetization for Treated Cover-Crop Seeds

Cover-crop adoption is subsidized through carbon markets that pay farmers for sequestering soil carbon, yet protocols rarely account for seed treatment inputs. The Natural Resources Conservation Service expanded dynamic soil property monitoring, paving the way for methodologies to quantify the biomass acceleration delivered by treated seed. Empirical studies linking treated cover-crop emergence to verified carbon gains are still absent, so revenue upside is hypothetical. Early adopters self-fund seed treatment to stabilize stands in narrow autumn planting windows, betting on future credibility. Once registries such as Verra publish seed-inclusive carbon rules, formulators can bundle treatments with project enrollment, but until then, the driver remains modest in scope.

Emerging State-Level Restrictions on Neonics and Their Impact

Vermont's Act 182 bans neonic-treated soybean and cereal seed from January 2029, and similar proposals are pending in the New York and Connecticut legislatures. Suppliers answer with actives such as Syngenta's PLINAZOLIN, first commercialized in Canadian cereals, and Corteva's LumiGEN recipes that rely on non-neonic insecticides. Portfolio fragmentation complicates logistics but creates an opening for agile formulators that secure early registrations of alternative chemistries. The market implications of state-level neonicotinoid (neonics) restrictions suggest a fragmented United States seed treatment market divided into regulatory zones. This will require formulators to manage multiple product portfolios, complicating supply chain logistics. It also presents opportunities for companies that invest early in non-neonic alternatives and secure regulatory approvals ahead of competitors.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Demand for On-Farm Seed Treating to Enhance Crop Yields

- Adoption of Digital Prescription Planting for Precision Agriculture

- Addressing the Perception Gap Compared to Fully Organic Farming Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fungicides hold the largest position, accounting for 46% of the United States seed treatment market share in 2025, helping growers combat Fusarium, Pythium, and Rhizoctonia. This dominance is attributed to their essential role in protecting seeds and seedlings from soil-borne and early-season diseases such as damping-off, root rot, and seed decay. Their widespread use ensures strong crop establishment and uniform germination, particularly in crops like corn, soybeans, and wheat. Soybean growers frequently use fungicide seed treatments to protect against pathogens such as Pythium and Rhizoctonia, which can significantly reduce stand counts if left unmanaged. This consistent and preventive protection has made fungicides a critical input for farmers across various growing regions.

Insecticides are the fastest-growing segment, projected to grow at a 13.5% CAGR through 2026-2031, whose growth is driven by increasing pest pressures, concerns over resistance, and the need for early-stage crop protection. Pests such as wireworms, seedcorn maggots, and aphids continue to threaten yields, prompting farmers to adopt insecticide seed treatments as a proactive measure. The adoption of integrated pest management and precision agriculture practices is promoting the targeted use of insecticides based on field-specific risks. Corn farmers in areas prone to early-season pest infestations may choose insecticide-treated seeds to prevent stand loss and avoid replanting costs, thereby fueling the rapid expansion of this segment.

List of Companies Covered in this Report:

- Bayer AG

- Syngenta AG

- Corteva, Inc.

- BASF SE

- UPL Limited

- ADAMA Ltd.

- Germains Seed Technology Ltd.

- Incotec Group B.V.

- Valent U.S.A. LLC

- Nufarm Limited

- Chromatech Incorporated

- BrettYoung

- Loveland Products, Inc.(Nutrien Ltd.)

- Helena Agri-Enterprises, LLC

- Roquette Freres

- Precision Laboratories, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory pressure on conventional pesticides

- 4.2.2 Urgency in resistance management to combat pests and diseases

- 4.2.3 Shift to polymer encapsulation for reduced dust-off

- 4.2.4 Carbon-credit monetization for treated cover crops

- 4.2.5 Increasing demand for on-farm seed treating to enhance crop yields

- 4.2.6 Adoption of digital prescription planting for precision agriculture

- 4.3 Market Restraints

- 4.3.1 Impact of large grower consolidation on the agricultural market

- 4.3.2 Lag in Environmental Protection Agency (EPA) approvals for new actives

- 4.3.3 Emerging state-level restrictions on neonics and their impact

- 4.3.4 Addressing the perception gap compared to fully organic farming systems

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Insecticides

- 5.1.2 Fungicides

- 5.1.3 Nematicides

- 5.1.4 Combination Products

- 5.2 By Crop Type

- 5.2.1 Grains and Cereals

- 5.2.2 Oilseeds and Pulses

- 5.2.3 Fruits and Vegetables

- 5.2.4 Commercial Crops

- 5.2.5 Turf and Ornamentals

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market-level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for key Companies, Products and Services, and Recent Developments)

- 6.4.1 Bayer AG

- 6.4.2 Syngenta AG

- 6.4.3 Corteva, Inc.

- 6.4.4 BASF SE

- 6.4.5 UPL Limited

- 6.4.6 ADAMA Ltd.

- 6.4.7 Germains Seed Technology Ltd.

- 6.4.8 Incotec Group B.V.

- 6.4.9 Valent U.S.A. LLC

- 6.4.10 Nufarm Limited

- 6.4.11 Chromatech Incorporated

- 6.4.12 BrettYoung

- 6.4.13 Loveland Products, Inc.(Nutrien Ltd.)

- 6.4.14 Helena Agri-Enterprises, LLC

- 6.4.15 Roquette Freres

- 6.4.16 Precision Laboratories, LLC

7 Market Opportunities and Future Outlook

印度種子加工:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

印度種子加工:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 種子加工市場:按類型、作物和地區分類

種子加工市場:按類型、作物和地區分類 再生種子處理市場預測至2034年-按產品類型、作物類型、功能、配方、最終用戶、分銷管道和地區分類的全球分析大豆殺菌劑種子處理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

再生種子處理市場預測至2034年-按產品類型、作物類型、功能、配方、最終用戶、分銷管道和地區分類的全球分析大豆殺菌劑種子處理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 種子處理市場:2026-2032年全球市場預測(依產品類型、作物類型、配方類型、處理方案、認證、應用環境、最終用戶和分銷管道分類)

種子處理市場:2026-2032年全球市場預測(依產品類型、作物類型、配方類型、處理方案、認證、應用環境、最終用戶和分銷管道分類) 種子處理市場規模、佔有率、趨勢和預測:按類型、應用方法、作物類型、功能和地區分類,2026-2034年

種子處理市場規模、佔有率、趨勢和預測:按類型、應用方法、作物類型、功能和地區分類,2026-2034年 2026年全球種子處理市場報告殺蟲燈市場:依光源、技術、應用、最終用途和銷售管道,全球預測(2026-2032年)

2026年全球種子處理市場報告殺蟲燈市場:依光源、技術、應用、最終用途和銷售管道,全球預測(2026-2032年) 種子處理市場規模、佔有率、成長及全球產業分析:按類型和應用分類,區域洞察及2026-2034年預測2026年全球種子處理設備市場報告

種子處理市場規模、佔有率、成長及全球產業分析:按類型和應用分類,區域洞察及2026-2034年預測2026年全球種子處理設備市場報告