|

市場調查報告書

商品編碼

2073365

西班牙付款閘道:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)Spain Payment Gateway - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

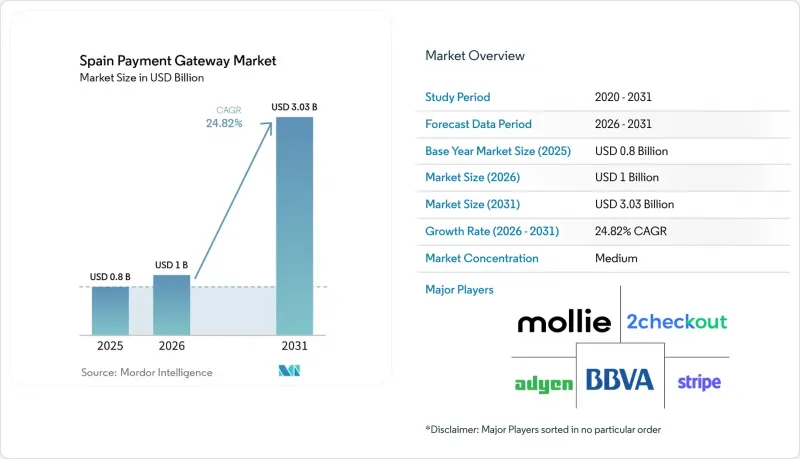

根據 Mordor Intelligence 預測,西班牙付款閘道市場規模將從 2025 年的 8 億美元成長到 2026 年的 10 億美元,然後在 2031 年達到 30.3 億美元,2026 年至 2031 年的複合年成長率為 24.82%。

本報告按支付方式(銀行卡、電子錢包等)、閘道器類型(託管式、非託管/API)、公司規模(大型企業、中小企業)、終端用戶行業(零售/電子商務、旅遊/酒店等)、交易管道(行動端、桌面端)和地區進行細分。市場預測以美元(USD)為單位。

西班牙付款閘道市場的趨勢與洞察

自從 Bizum 與各大商家建立合作關係以來,行動錢包的使用量激增。

Bizum從P2P轉帳轉向店內和線上商家支付,使其應用範圍超越了銀行應用程式。隨著「Bizum Pay」於2025年上線,用戶將能夠利用現有的POS終端,免除卡片組織費用,並直接從其活期帳戶進行NFC非接觸式支付。採用Bizum支付的大型零售商報告稱,購物車放棄率降低,復購率提高。 Bizum擁有2,600萬用戶(佔西班牙銀行帳戶持有人的60%),目前處理近一半的銀行間交易。隨著智慧型手機普及率在2029年接近97%,無縫整合Bizum的行動優先付款閘道可望在西班牙付款閘道市場佔據日益成長的交易量。

歐盟數位支付方案為中小企業提供財政支持。

西班牙耗資30.67億歐元的「數位化工具包」(Kit Digital)計畫為中小企業提供電子商務平台、網路安全和認證發票軟體方面的補貼。截至2024年底,該計畫已批准超過53萬筆津貼,線上支付工具的普及率也呈現爆炸性成長,形成良性循環。許多先前依賴現金支付的小規模企業現在開始採用整合發票和會計模組的付款閘道,這不僅擴大了商家群體,也提升了西班牙付款閘道市場的總交易量。

3-D Secure 2.0 對轉換率的影響

如果忽略基於風險的豁免條款,PSD2 下 3-D Secure 2.0 的全面實施可能會導致交易完成數量減少高達 20%。因此,西班牙商家正依賴具備自適應風險評分功能的付款閘道,這些閘道器僅對高風險交易流程觸發分級身分驗證。能夠在保持合規性的同時提供一鍵支付體驗的支付服務商正在贏得市場佔有率,而那些缺乏精細化控制的支付服務商則面臨著西班牙付款閘道市場商戶流失的風險。

細分市場分析

2025年,銀行卡在西班牙付款閘道市場仍佔44.30%的佔有率。這是因為85%的居民至少擁有一張簽帳金融卡卡或信用卡。然而,數位錢包正以27.14%的複合年成長率成長,隨著Apple Pay和Google Pay的普及率分別達到30%和27%,預計到2031年,它們將在西班牙付款閘道市場佔據更大的佔有率。

這一成長勢頭得益於便捷的代幣化支付、生物識別以及商家使用量的增加。 Bizum 和 SEPA即時轉帳為消費者和商家提供免手續費選項,而先買後付 (BNPL) 皮夾則提升了非自由裁量權領域的平均交易量。這些趨勢共同導致銀行卡利潤率下降,而總交易量卻在成長,從而維持了西班牙付款閘道市場兩位數的成長。

對於旅行預訂、租車和公司費用支付而言,銀行卡仍然不可或缺,這得益於忠誠度計畫和全球網路的支援。然而,為了維持交易量,發卡機構正在將卡片資訊整合到電子錢包中,模糊了傳統塑膠卡和行動支付卡之間的界線。即將推出的數位歐元試點計畫未來可能會引入公共部門電子錢包選項,但就目前而言,推動動態消費管理和線上優惠券等創新的主要是私人電子錢包。

到2025年,託管式支付閘道器將佔總收入的68.20%,這主要得益於即插即用的部署方式和PCI合規外包服務。同時,非託管/API模式正以26.12%的複合年成長率快速成長,因為數據驅動型商家需要完全控制品牌形象和精細化的分析數據。這種轉變正在深化西班牙付款閘道市場,因為API閘道器通常會捆綁增值模組,從而提高每位商家的平均收入。

主流平台正利用客製化的結帳流程、網路令牌化和智慧路由的授權流程來提高交易通過率。非託管架構會公開原始交易數據,使商家能夠利用這些數據進行用戶群分析、生命週期價值追蹤和即時詐欺洞察。另一方面,託管服務供應商則提供混合服務——內建結帳Widgets以及嵌入式的伺服器間通訊——以留住那些希望遷移到更高階服務的中小型企業 (SME) 客戶。

這種採用趨勢在時尚電商平台和訂閱制媒體應用中尤其明顯,這些平台不僅需要全球支付方式,還需要在地化的支付選項。此外,API收購方簡化了支付編配實驗,並允許商家在收單機構之間動態路由流量,從而最佳化成本和可靠性,但這也加劇了西班牙付款閘道市場的競爭,導致客戶流失率進一步上升。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- Bizum與主要商家合作後,行動錢包使用量激增。

- 歐盟數位支付方案為中小企業提供財政支持。

- 強制性即時支付網路(SEPA Inst)將於 2025 年第四季全面運作。

- 旅遊業的復甦帶動了跨國刷卡消費。

- 人工智慧驅動的詐欺偵測可降低閘道器切換成本。

- 使用「綠色收據」開立電子帳單可享有稅務優惠

- 市場限制因素

- 3-D Secure 2.0 對轉化率的抑製作用

- 限制互通收費標準給支付服務提供者的利潤率帶來了壓力。

- 網路犯罪在銀行間支付領域激增

- 銀行主導的EPI ONE計畫正在威脅獨立門戶網站。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- PESTLE分析

第5章 市場規模與成長預測

- 透過付款方式

- 卡片

- 數位錢包

- 帳間轉帳(Bizum、SEPA Inst)

- Buy-Now-Pay-Later

- 依閘道器類型

- 託管

- 非託管/API

- 按公司規模

- 大公司

- 小型企業

- 按最終用戶行業分類

- 零售與電子商務

- 旅遊與飯店

- 銀行業、金融服務業及保險業

- 媒體與娛樂

- 其他(教育、公共產業等)

- 透過交易管道

- 移動的

- 桌面/其他

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Adyen NV

- Stripe Inc.

- Mollie BV

- 2Checkout(Verifone Payments BV)

- Banco Bilbao Vizcaya Argentaria SA

- PayPal Holdings Inc.

- Authorize.Net(Visa Inc.)

- Amazon Payments Inc.

- Klarna Bank AB

- Bizum SL

- Redsys Servicios de Procesamiento SL

- Worldline SA

- Global Payments Inc.

- CaixaBank Payments and Consumer EFCEPSAU

- Banco Sabadell, SA

- ING Bank NV

- Apple Inc.(Apple Pay)

- Alphabet Inc.(Google Pay)

- PayXpert SLU

- SumUp Payments Ltd.

第7章:西班牙付款閘道分析師排名

第8章 市場機會與未來展望

- 評估未開發的領域和未滿足的需求

According to Mordor Intelligence, the spain payment gateway market size is expected to grow from USD 0.80 billion in 2025 to USD 1.00 billion in 2026 and is forecast to reach USD 3.03 billion by 2031 at 24.82% CAGR over 2026-2031.

This report is Segmented by Payment Method (Cards, Digital Wallets and More), Gateway Type (Hosted, Non-Hosted/API), Enterprise Size (Large Enterprise, Small & Medium Enterprise), End-User Industry (Retail & E-Commerce, Travel & Hospitality and More), Transaction Channel (Mobile, Desktop), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Spain Payment Gateway Market Trends and Insights

Surge in Mobile-Wallet Usage Post-Bizum Integration with Large Merchants

Bizum's pivot from peer-to-peer transfers to in-store and online merchant payments expands acceptance beyond banking apps. The 2025 launch of Bizum Pay will enable NFC contactless payments directly from current accounts, leveraging existing POS terminals and eliminating card network fees. Large retailers that embed Bizum at checkout report lower cart-abandonment and higher repeat purchase rates. With 26 million users-60% of Spain's banked population-Bizum now underpins nearly half of all account-to-account transactions. As smartphone penetration nears 97% by 2029, mobile-first gateways that integrate Bizum seamlessly are positioned to capture incremental volumes within the Spain payment gateway market.

EU Digital Payments Package Funding for SMEs

Spain's EUR 3.067 billion Kit Digital scheme reimburses SMEs for e-commerce platforms, cybersecurity, and certified billing software. More than 530,000 grants had been approved by late-2024, creating a self-reinforcing surge in online acceptance tools. Many micro-merchants that previously relied on cash now onboard gateways bundled with invoicing and accounting modules, widening the Spain payment gateway market's merchant base and lifting total processed value.

3-D Secure 2.0 Friction on Conversion Rates

Universal application of 3-D Secure 2.0 under PSD2 can cut completed transactions by up to 20% when risk-based exemptions are ignored. Spanish merchants therefore rely on gateways equipped with adaptive risk scoring that triggers step-up authentication only for high-risk flows. Providers able to sustain compliance while preserving one-click experiences gain share, whereas those lacking granular controls risk merchant attrition within the Spain payment gateway market.

Other drivers and restraints analyzed in the detailed report include:

- Mandatory Instant-Payment Rails (SEPA Inst) Go Live Q4-2025

- Tourism Rebound Pushes Cross-Border Card Volumes

- AI-Driven Fraud Screening Lowers Gateway Switching Costs

- Interchange-fee cap squeezes PSP margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cards maintained a 44.30% share of the Spain payment gateway market in 2025 as 85% of residents held at least one debit or credit card. Nonetheless, digital wallets are growing at a 27.14% CAGR and are on track to seize a far larger slice of the Spain payment gateway market size by 2031 thanks to Apple Pay's 30% usage and Google Pay's 27% penetration.

The momentum stems from seamless tokenized checkout, biometric authentication, and widening merchant acceptance. Bizum and SEPA instant transfers provide a zero-fee alternative for both consumers and merchants, while BNPL wallets boost average ticket values in high-discretionary segments. Together these trends compress card margins yet expand overall processed value, sustaining double-digit expansion of the Spain payment gateway market.

Cards remain indispensable for travel bookings, car rentals, and corporate expenses, bolstered by loyalty schemes and global acceptance rails. Still, issuers are integrating card credentials into wallets to defend volumes, blurring lines between traditional plastic and mobile tokens. The impending digital euro pilot could later introduce public-sector wallet options, but private wallets presently lead innovations such as dynamic spending controls and inline couponing.

Hosted gateways captured 68.20% of 2025 revenues due to their plug-and-play deployment and outsourced PCI scope. Yet non-hosted/API models are advancing at a 26.12% CAGR as data-driven merchants seek full branding control and granular analytics. The shift adds depth to the Spain payment gateway market because API gateways often bundle value-added modules that raise average revenue per merchant.

Large platforms leverage custom checkout flows, network tokenization, and intelligently routed authorizations to lift approval rates. Non-hosted architectures expose raw transaction data that merchants mine for cohort analysis, lifetime-value tracking, and real-time fraud insights. Hosted providers respond with hybrid offers-embedded checkout widgets plus optional server-to-server calls-in an effort to retain SME customers migrating upward.

Adoption is visible in fashion marketplaces and subscription media apps that demand localized payment methods alongside global ones. API gateways also simplify experimentation with payment orchestration, allowing merchants to route traffic dynamically between acquirers for optimal cost and reliability, reinforcing competitive churn inside the Spain payment gateway market.

Complete Report Scope:

- By Payment Method

- Cards

- Digital Wallets

- Account-to-Account (Bizum, SEPA Inst)

- Buy-Now-Pay-Later

- By Gateway Type

- Hosted

- Non-Hosted / API

- By Enterprise Size

- Large Enterprise

- Small and Medium Enterprise

- By End-User Industry

- Retail and E-commerce

- Travel and Hospitality

- Banking, Financial Services and Insurance

- Media and Entertainment

- Others (Education, Utilities, etc.)

- By Transaction Channel

- Mobile

- Desktop / Other

List of Companies Covered in this Report:

- Adyen N.V.

- Stripe Inc.

- Mollie B.V.

- 2Checkout (Verifone Payments B.V.)

- Banco Bilbao Vizcaya Argentaria S.A.

- PayPal Holdings Inc.

- Authorize.Net (Visa Inc.)

- Amazon Payments Inc.

- Klarna Bank AB

- Bizum S.L.

- Redsys Servicios de Procesamiento S.L.

- Worldline S.A.

- Global Payments Inc.

- CaixaBank Payments and Consumer E.F.C. E.P. S.A.U.

- Banco Sabadell, S.A.

- ING Bank N.V.

- Apple Inc. (Apple Pay)

- Alphabet Inc. (Google Pay)

- PayXpert S.L.U.

- SumUp Payments Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in mobile-wallet usage post-Bizum integration with large merchants

- 4.2.2 EU Digital Payments Package funding for SMEs

- 4.2.3 Mandatory instant-payment rails (SEPA Inst) go live Q4-2025

- 4.2.4 Tourism rebound pushes cross-border card volumes

- 4.2.5 AI-driven fraud-screening lowers gateway switching-costs

- 4.2.6 "Green receipts" tax incentives for e-invoicing

- 4.3 Market Restraints

- 4.3.1 3-D Secure 2.0 friction on conversion rates

- 4.3.2 Interchange-fee cap squeezes PSP margins

- 4.3.3 Cyber-crime surge in account-to-account payments

- 4.3.4 Bank-led push for EPI ONE threatens independent gateways

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 PESTLE Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Payment Method

- 5.1.1 Cards

- 5.1.2 Digital Wallets

- 5.1.3 Account-to-Account (Bizum, SEPA Inst)

- 5.1.4 Buy-Now-Pay-Later

- 5.2 By Gateway Type

- 5.2.1 Hosted

- 5.2.2 Non-Hosted / API

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprise

- 5.3.2 Small and Medium Enterprise

- 5.4 By End-User Industry

- 5.4.1 Retail and E-commerce

- 5.4.2 Travel and Hospitality

- 5.4.3 Banking, Financial Services and Insurance

- 5.4.4 Media and Entertainment

- 5.4.5 Others (Education, Utilities, etc.)

- 5.5 By Transaction Channel

- 5.5.1 Mobile

- 5.5.2 Desktop / Other

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level overview, Market level overview, Core segments, Financials as available, Strategic information, Market rank/share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Adyen N.V.

- 6.4.2 Stripe Inc.

- 6.4.3 Mollie B.V.

- 6.4.4 2Checkout (Verifone Payments B.V.)

- 6.4.5 Banco Bilbao Vizcaya Argentaria S.A.

- 6.4.6 PayPal Holdings Inc.

- 6.4.7 Authorize.Net (Visa Inc.)

- 6.4.8 Amazon Payments Inc.

- 6.4.9 Klarna Bank AB

- 6.4.10 Bizum S.L.

- 6.4.11 Redsys Servicios de Procesamiento S.L.

- 6.4.12 Worldline S.A.

- 6.4.13 Global Payments Inc.

- 6.4.14 CaixaBank Payments and Consumer E.F.C. E.P. S.A.U.

- 6.4.15 Banco Sabadell, S.A.

- 6.4.16 ING Bank N.V.

- 6.4.17 Apple Inc. (Apple Pay)

- 6.4.18 Alphabet Inc. (Google Pay)

- 6.4.19 PayXpert S.L.U.

- 6.4.20 SumUp Payments Ltd.

7 ANALYST RANKING OF PAYMENT GATEWAYS IN SPAIN

8 MARKET OPPORTUNITIES and FUTURE OUTLOOK

- 8.1 White-space and Unmet-need Assessment

2026年全球收據式優惠市場報告

2026年全球收據式優惠市場報告 中國付款閘道:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

中國付款閘道:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 付款閘道市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、最終用途、企業規模、地區和競爭格局分類,2021-2031 年

付款閘道市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、最終用途、企業規模、地區和競爭格局分類,2021-2031 年 付款閘道市場機會、成長要素、產業趨勢分析及2026-2035年預測

付款閘道市場機會、成長要素、產業趨勢分析及2026-2035年預測 付款閘道市場規模、佔有率和成長分析:按類型、企業規模、最終用戶和地區分類-2026-2033年產業預測

付款閘道市場規模、佔有率和成長分析:按類型、企業規模、最終用戶和地區分類-2026-2033年產業預測 付款閘道付款閘道市場:2026-2032年全球市場預測(按類型、支付方式、支付格式、部署方式、產業和組織規模分類)

付款閘道付款閘道市場:2026-2032年全球市場預測(按類型、支付方式、支付格式、部署方式、產業和組織規模分類) 付款閘道市場報告:按應用程式、互動方式和地區分類(2026-2034 年)

付款閘道市場報告:按應用程式、互動方式和地區分類(2026-2034 年) 付款閘道市場規模、佔有率和趨勢分析報告:按類型、企業規模、最終用途、地區和細分市場預測(2026-2033 年)

付款閘道市場規模、佔有率和趨勢分析報告:按類型、企業規模、最終用途、地區和細分市場預測(2026-2033 年) 行動付款閘道市場預測:至 2034 年-按組件、支付類型、部署模式、企業規模、最終用戶和地區分類的全球分析

行動付款閘道市場預測:至 2034 年-按組件、支付類型、部署模式、企業規模、最終用戶和地區分類的全球分析 全球付款閘道市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球付款閘道市場規模、佔有率、趨勢和成長分析報告(2026-2034)