|

市場調查報告書

商品編碼

2065751

中國付款閘道:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)China Payment Gateway - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

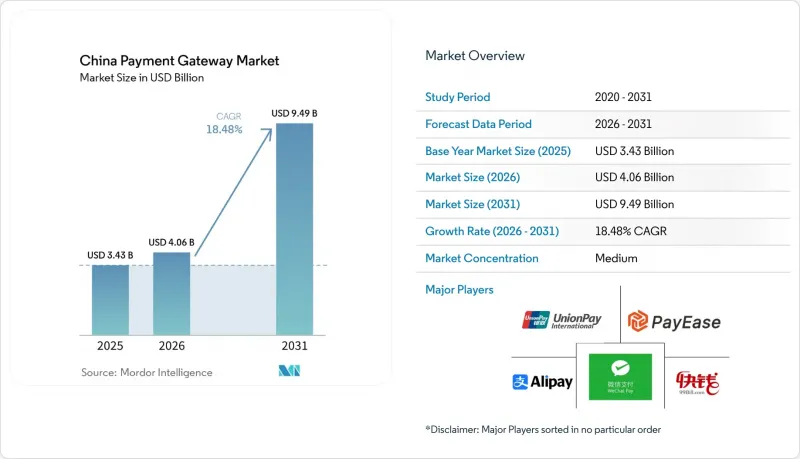

根據 Mordor Intelligence 估計,中國付款閘道市場規模從 2025 年的 34.3 億美元成長到 2026 年的 40.6 億美元,預計到 2031 年將達到 94.9 億美元。

預計 2026 年至 2031 年的複合年成長率為 18.48%。

本報告按類型(託管型、非託管型、基於平台的超級應用閘道器等)、企業規模(微型、小規模、中型等)、終端用戶行業(零售/電子商務、旅遊/酒店等)、支付方式整合(數位錢包等)、部署環境(行動應用SDK等)和地區進行細分。市場預測以美元(USD)為單位。

中國付款閘道市場的趨勢與洞察

電子商務和行動商務的快速成長

預計到2024年,行動商務將佔線上消費總額的82%,從而推動主要支付閘道器供應商的交易量成長。直播帶貨、社交購物以及網紅主導「即時購買」功能,都促使商家對亞秒級支付速度的需求日益成長。商家越來越傾向於選擇僅支援API介面或嵌入式支付閘道器,以簡化支付流程,提高轉換率和重購率。人口結構的變化正在擴大潛在用戶群體,其中首次使用數位支付的用戶大多來自低收入群體。這些因素,加上線上零售業從沿海大都會圈向外擴張,預計將推動中國付款閘道市場保持兩位數以上的持續成長。

政府措施和政策支持無現金支付

2024年3月,國務院發布指令,要求在公共服務和零售業全面推廣數位支付,加速微企業商家註冊。中國人民銀行簡化了外國訪客的「了解你的客戶」(KYC)流程,提高了交易限額,並最佳化了報名手續。 2024年頒布的統一資料流規則促進了跨境支付處理,推動付款閘道拓展至新的貿易走廊。針對小規模企業的優惠手續費上限降低了進入門檻,直接促進了本地零售業對付款閘道的採用。這些積極的管治措施共同確保了中國付款閘道市場維持包容性成長。

支付寶和微信支付的雙向壟斷阻礙了新進入者。

到2024年,支付寶和微信支付將佔據超過90%的行動交易佔有率,將商家和消費者困於一個封閉的生態系統中。這兩家公司在社交、電商和金融領域的深度整合造成了高昂的轉換成本,阻礙了其他付款閘道的試驗。海外支付服務商難以擴大規模,許多服務商仍侷限於小眾的跨境應用場景。隨著這兩大巨頭不斷將生物識別、小程式和超級應用程式等功能融入支付方式,競爭差距進一步擴大。儘管交易總量持續成長,但這種趨勢對中國付款閘道市場的多元化構成了結構性限制。

細分市場分析

預計2025年,託管式支付閘道器將主導中國付款閘道市場,佔77.15%的市佔率。然而,隨著商家轉向敏捷架構,該領域的成長速度正在放緩。預計到2025年,託管式付款閘道市場規模將達到約26.5億美元,反映出中小企業對易於合規、承包的解決方案的廣泛採用。僅提供API介面和嵌入式支付閘道器的複合年成長率最高,達到18.62%,這主要得益於品牌商對將支付功能整合到直播、社群媒體和遊戲內收費等應用程式的需求。騰訊和螞蟻集團提供的超級應用程式支付閘道器整合了流量、會員忠誠度和行銷工具,降低了商家的獲客成本。對於那些優先考慮資料控制的企業,尤其是金融和電信等受監管行業的企業而言,非託管或本地部署仍然是首選方案。騰訊的手掌掃描支付試點計畫就是一個很好的例子,它展示了嵌入式認證層如何改善使用者體驗並培養使用者忠誠度。

對於獨立軟體供應商而言,API優先設計可將整合週期從數週縮短至數天,並降低工程開銷。這種架構還支援快速部署增值功能,例如分期付款計劃、獎勵和保險。由於5G和邊緣運算帶來的低延遲,閘道器能夠提供即時詐欺評分,在不影響安全性的前提下提高核准通過率。在預測期內,以API為中心的產品預計將逐步蠶食託管平台的市場佔有率,而混合架構將繼續受到既需要簡易性又需要客製化的多通路營運商的青睞。

儘管微企業的絕對銷售額仍保持在個位數,但其複合年成長率 (CAGR) 高達 19.91%,是中國付款閘道市場中成長率最高的。簡化的入駐流程、降低的商家折扣率 (MDR) 以及政府補貼降低了准入門檻,使得攤販和本地零售商也能在幾分鐘內接受QR碼支付。大型企業持續推動規模擴張,通常會部署多個支付閘道器以確保冗餘性和區域覆蓋。預計到 2025 年,中國付款閘道市場的中小企業細分市場規模將達到約 21.4 億美元,凸顯了其對支付處理商和收購方的重要性。隨著鄉鎮級企業供應鏈數位化進程的加速,支付閘道器供應商正在發布小程式工具包,將庫存管理、行銷和支付整合到單一工作流程中。

中型企業通常會先部署託管支付閘道器,隨著交易量的成長和客製化流程的出現,再遷移到功能豐富的API平台。政府針對中小企業融資的評估指標鼓勵銀行與金融科技公司合作,拓展客製化支付支援。這種合作正在推動創新,例如為網路連接不佳的地區提供離線QR碼。對於微型企業而言,透過免手續費期和客製化培訓計畫提升其數位素養,進一步擴大了中國付款閘道市場的潛在基本客群。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電子商務和行動商務的快速成長

- 政府措施和政策支持無現金支付

- 智慧型手機和5G技術實現了無縫支付。

- 跨境電子商務的需求

- 數位人民幣(e-CNY)的推出將促進支付閘道器的普及。

- 人工智慧驅動的防詐騙技術正在吸引會員商店。

- 市場限制因素

- 支付寶和微信的雙向壟斷阻礙了新進入者。

- 合規負擔和許可成本增加

- 外國支付服務供應商面臨的資料在地化和網路安全障礙

- 都市區市場飽和,農村普及緩慢。

- 監理情勢

- 技術展望

- 波特五力分析

- PESTLE分析

第5章 市場規模與成長預測

- 按類型

- 託管類型

- 非託管類型

- 基於平台的超級應用閘道器

- 僅限 API /嵌入式

- 本機自架

- 按公司規模

- 微企業

- 小型企業

- 大公司

- 按最終用戶行業分類

- 零售與電子商務

- 旅遊與飯店

- BFSI

- 媒體與娛樂

- 教育

- 醫療保健和遠端醫療

- 政府和公共服務

- 其他

- 支付方式的整合

- 數位錢包

- 信用卡品牌

- 帳戶間轉帳/QR碼

- 先買後付

- 加密貨幣/央行數位貨幣(電子人民幣)

- 按部署環境

- 行動應用程式SDK

- 網站常見問題解答

- 店內POS/2D碼

- 跨境門戶

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- Analyst Ranking of Payment Gateways in China

- 市佔率分析

- 公司簡介

- Alipay(Ant Group)

- WeChat Pay(Tencent Holdings)

- UnionPay International

- PayEase

- 99Bill Corporation

- Mastercard Inc.

- JD Pay

- ChinaPnR

- iPS

- Lakala Payment

- Yeepay

- Allinpay

- LianLian Pay

- PingPong Payments

- Airwallex

- Adyen

- Worldpay(FIS)

- GZ Bill

- Ping An OneConnect

第7章 市場機會與未來展望

According to Mordor Intelligence, china payment gateway market size in 2026 is estimated at USD 4.06 billion, growing from 2025 value of USD 3.43 billion with 2031 projections showing USD 9.49 billion, growing at 18.48% CAGR over 2026-2031.

This report is Segmented by Type (Hosted, Non-Hosted, Platform-Based Super-App Gateways and More), Enterprise Size (Micro, Small, Medium, and More), End-User Industry (Retail and E-Commerce, Travel and Hospitality and More), Payment-Method Integration (Digital Wallets, and More), Deployment Environment (Mobile-App SDK, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

China Payment Gateway Market Trends and Insights

Growing E-commerce and M-commerce Surge

Mobile commerce represented 82% of all online spending in 2024, lifting transaction volumes for every serious gateway provider. Live-stream sales, social shopping and influencer-led "instant buy" features escalate demand for sub-second authorisation speeds. Merchants increasingly favour API-only and embedded gateways that remove checkout friction, elevating conversion and repeat purchase rates. Demographic shifts show first-time digital payers emerging from low-income groups, expanding the total addressable user base. These factors collectively position the China payment gateway market for sustained high-teens growth as online retail diversifies beyond the coastal megacities.

Government Cash-less Initiatives and Policy Support

The State Council's March 2024 directive mandated universal acceptance of digital payments in public services and retail, accelerating merchant on-boarding across micro businesses. The People's Bank of China simplified KYC for foreign visitors, enabling larger transaction limits and smoother registration. Harmonised data-flow rules released in 2024 eased cross-border processing, supporting gateway expansion into new trade corridors. Preferential fee caps for small merchants lowered entry barriers, directly boosting gateway penetration in community retail. Collectively, proactive governance keeps the China payment gateway market on an inclusive growth path.

Alipay-WeChat Duopoly Limits New Entrants

Alipay and WeChat Pay together captured more than 90% of mobile transactions in 2024, locking merchants and consumers into closed ecosystems. Their deep integration across social, commerce and finance produces high switching costs that discourage experimentation with alternative gateways. Foreign processors have struggled to build scale, with most remaining confined to niche cross-border use cases. As the duopoly layers biometric authentication, mini-programs and super-app perks around payments, competitive gaps widen further. This dynamic acts as a structural drag on the China payment gateway market's diversity, even while total volumes keep expanding.

Other drivers and restraints analyzed in the detailed report include:

- Cross-border E-commerce Demand

- Digital Yuan (e-CNY) Rollout Boosts Gateway Adoption

- Rising Compliance Burden and Licensing Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hosted gateways dominated with 77.15% of China payment gateway market share in 2025, yet the segment faces decelerating growth as merchants migrate to agile architectures. The China payment gateway market size attributable to hosted options reached roughly USD 2.65 billion in 2025, reflecting widespread adoption among SMEs that prefer turnkey compliance. API-only and embedded gateways log the fastest 18.62% CAGR because brands want checkout embedded inside live streams, social feeds and in-game purchases. Super-app gateways from Tencent and Ant offer built-in traffic, loyalty and marketing tools, reducing acquisition costs for merchants. Enterprises demanding custodial data control still select non-hosted or on-premise deployments, particularly in regulated sectors such as finance and telecom. Palm-scan payments, piloted by Tencent, exemplify how embedded authentication layers can differentiate user experience and foster loyalty.

For independent software vendors, API-first design shortens integration cycles from weeks to days, lowering engineering overheads. The architecture also facilitates rapid roll-out of value-added features such as instalments, rewards and insurance. As 5G and edge computing cut latency, gateways offer real-time fraud scoring that enhances approval rates without sacrificing security. Over the forecast horizon, API-centric products are expected to take incremental share from hosted platforms, though hybrid stacks will persist in multi-channel merchants that require both simplicity and customisation.

Micro enterprises delivered only single-digit revenue in absolute terms but posted a 19.91% CAGR, the fastest within the China payment gateway market. Simplified onboarding, reduced MDR fees and government subsidies have lowered entry thresholds, allowing street vendors and rural stores to accept QR payments within minutes. Large enterprises continue to drive scale, often deploying multiple gateways for redundancy and regional coverage. The China payment gateway market size attached to SME segments accounted for roughly USD 2.14 billion in 2025, signifying the importance of this cohort to processors and acquirers alike. As supply-chain digitisation accelerates among township-level firms, gateway vendors are releasing mini-programme toolkits that integrate inventory, marketing and settlement in one workflow.

Medium enterprises typically adopt hosted gateways first, then transition to API-rich platforms once transaction volumes warrant customised flows. Government evaluation metrics for small-business finance push banks to extend bespoke payment support, often in partnership with fintechs. This collaboration spurs innovation such as offline-capable QR codes for low-connectivity areas. For micro merchants, fee holidays and curated training programmes improve digital literacy, further enlarging the addressable base for the China payment gateway market.

List of Companies Covered in this Report:

- Alipay (Ant Group)

- WeChat Pay (Tencent Holdings)

- UnionPay International

- PayEase

- 99Bill Corporation

- Mastercard Inc.

- JD Pay

- ChinaPnR

- iPS

- Lakala Payment

- Yeepay

- Allinpay

- LianLian Pay

- PingPong Payments

- Airwallex

- Adyen

- Worldpay (FIS)

- GZ Bill

- Ping An OneConnect

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing e-commerce and m-commerce surge

- 4.2.2 Government cash-less initiatives and policy support

- 4.2.3 Smartphones and 5G enable seamless checkout

- 4.2.4 Cross-border e-commerce demand

- 4.2.5 Digital Yuan (e-CNY) rollout boosts gateway adoption

- 4.2.6 AI-driven fraud prevention attracts merchants

- 4.3 Market Restraints

- 4.3.1 Alipay-WeChat duopoly limits new entrants

- 4.3.2 Rising compliance burden and licensing costs

- 4.3.3 Data-localization and cybersecurity barriers for foreign PSPs

- 4.3.4 Urban market saturation, rural onboarding lag

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 PESTLE Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Hosted

- 5.1.2 Non-Hosted

- 5.1.3 Platform-based Super-App Gateways

- 5.1.4 API-Only / Embedded

- 5.1.5 On-premise Self-Hosted

- 5.2 By Enterprise Size

- 5.2.1 Micro Enterprises

- 5.2.2 Small and Medium Enterprises

- 5.2.3 Large Enterprises

- 5.3 By End-User Industry

- 5.3.1 Retail and E-commerce

- 5.3.2 Travel and Hospitality

- 5.3.3 BFSI

- 5.3.4 Media and Entertainment

- 5.3.5 Education

- 5.3.6 Healthcare and Tele-medicine

- 5.3.7 Government and Public Services

- 5.3.8 Others

- 5.4 By Payment-Method Integration

- 5.4.1 Digital Wallets

- 5.4.2 Card Schemes

- 5.4.3 Account-to-Account / QR

- 5.4.4 Buy-Now-Pay-Later

- 5.4.5 Cryptocurrency / CBDC (e-CNY)

- 5.5 By Deployment Environment

- 5.5.1 Mobile-App SDK

- 5.5.2 Web Checkout

- 5.5.3 In-store POS / QR

- 5.5.4 Cross-border Gateway

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Analyst Ranking of Payment Gateways in China

- 6.4 Market Share Analysis

- 6.5 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.5.1 Alipay (Ant Group)

- 6.5.2 WeChat Pay (Tencent Holdings)

- 6.5.3 UnionPay International

- 6.5.4 PayEase

- 6.5.5 99Bill Corporation

- 6.5.6 Mastercard Inc.

- 6.5.7 JD Pay

- 6.5.8 ChinaPnR

- 6.5.9 iPS

- 6.5.10 Lakala Payment

- 6.5.11 Yeepay

- 6.5.12 Allinpay

- 6.5.13 LianLian Pay

- 6.5.14 PingPong Payments

- 6.5.15 Airwallex

- 6.5.16 Adyen

- 6.5.17 Worldpay (FIS)

- 6.5.18 GZ Bill

- 6.5.19 Ping An OneConnect

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

付款閘道市場:2026-2032年全球市場預測(付款閘道類型、支付方式、支付格式、部署類型、產業和組織規模分類)

付款閘道市場:2026-2032年全球市場預測(付款閘道類型、支付方式、支付格式、部署類型、產業和組織規模分類) 西班牙付款閘道:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)

西班牙付款閘道:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年) 2026年全球收據式優惠市場報告

2026年全球收據式優惠市場報告 付款閘道市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、最終用途、企業規模、地區和競爭格局分類,2021-2031 年

付款閘道市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、最終用途、企業規模、地區和競爭格局分類,2021-2031 年 付款閘道市場機會、成長要素、產業趨勢分析及2026-2035年預測

付款閘道市場機會、成長要素、產業趨勢分析及2026-2035年預測 付款閘道市場規模、佔有率和成長分析:按類型、企業規模、最終用戶和地區分類-2026-2033年產業預測

付款閘道市場規模、佔有率和成長分析:按類型、企業規模、最終用戶和地區分類-2026-2033年產業預測 付款閘道市場報告:按應用程式、互動方式和地區分類(2026-2034 年)

付款閘道市場報告:按應用程式、互動方式和地區分類(2026-2034 年) 付款閘道市場規模、佔有率和趨勢分析報告:按類型、企業規模、最終用途、地區和細分市場預測(2026-2033 年)

付款閘道市場規模、佔有率和趨勢分析報告:按類型、企業規模、最終用途、地區和細分市場預測(2026-2033 年) 行動付款閘道市場預測:至 2034 年-按組件、支付類型、部署模式、企業規模、最終用戶和地區分類的全球分析

行動付款閘道市場預測:至 2034 年-按組件、支付類型、部署模式、企業規模、最終用戶和地區分類的全球分析 全球付款閘道市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球付款閘道市場規模、佔有率、趨勢和成長分析報告(2026-2034)