|

市場調查報告書

商品編碼

2027635

付款閘道市場機會、成長要素、產業趨勢分析及2026-2035年預測Payment Gateway Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

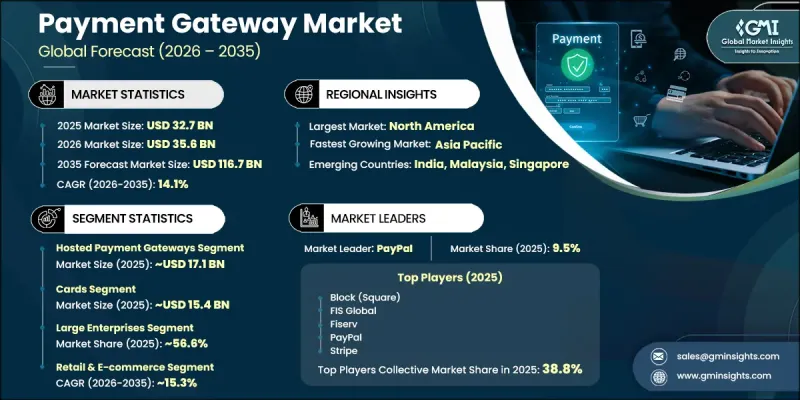

預計到 2025 年,全球付款閘道市場規模將達到 327 億美元,並將以 14.1% 的複合年成長率成長,到 2035 年達到 1,167 億美元。

隨著消費者和企業日益轉向安全便捷的電子交易,全球數位支付的快速普及正強勁推動市場成長。付款閘道生態系統在實現各行業線上支付的安全核准、處理和路由方面發揮著至關重要的作用。隨著對交易安全、合規性和詐欺防範的日益重視,系統結構和創新也在不斷演變。監管要求和不斷發展的網路安全標準正在推動加密、令牌化和多因素認證等先進安全機制的整合。隨著全球付款管道的服務能力超越基本的交易處理,產業競爭也日益激烈。各公司致力於提供整合化的數位支付生態系統,以提升使用者體驗並支援跨境商務。電子商務滲透率的提高、智慧型手機使用量的增加以及對即時支付處理的需求,進一步促進了市場擴張。持續的技術進步和向無現金經濟的轉型預計將支撐付款閘道市場的長期成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 327億美元 |

| 預計金額 | 1167億美元 |

| 複合年成長率 | 14.1% |

隨著企業將安全、高效且擴充性的數位支付解決方案置於優先地位,付款閘道市場正在迅速發展。對線上交易日益成長的依賴正在推動支付基礎設施的持續創新。服務供應商正在增強系統功能,以支援更快的處理速度、更強的詐欺偵測能力以及跨平台無縫整合。對合規性和資料保護日益成長的需求也進一步推動了安全支付技術的進步。

到2025年,託管付款閘道市佔率將達到52.3%,市場規模將達171億美元。該細分市場的主導地位得益於其簡化的部署模式,從而減輕了企業的營運負擔。透過外部系統安全地處理高度敏感的支付數據,企業無需投資建造大規模的內部基礎設施即可滿足合規標準。其易於整合和強大的安全框架也持續推動其廣泛應用。

預計到2025年,銀行卡支付將佔據47%的市場佔有率,市場規模達154億美元。該領域之所以保持主導地位,得益於其全球滲透率、完善的基礎設施以及消費者的高度信任。銀行卡交易在網路和線下支付管道中均廣泛應用。主要銀行卡網路的存在確保了國內外支付交易處理的標準化和可靠性。

美國付款閘道市場預計到2025年將達到98億美元,並預計在2026年至2035年間以12.4%的複合年成長率成長。這一成長主要得益於美國高度發展的數位經濟和安全線上支付系統的廣泛應用。網路普及率高以及對快速便捷交易日益成長的需求持續推動著市場擴張。此外,支付基礎設施的不斷現代化也進一步促進了產業發展。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 電子商務和數位商務的快速成長

- 行動支付的普及和智慧型手機的普及率

- 商業交易和跨國貿易向全球化世界的轉變。

- 疫情後人們更傾向於非接觸式支付。

- 產業潛在風險與挑戰

- 監理合規的複雜性和區域差異

- 對銀行基礎設施和網路可靠性的依賴

- 市場機遇

- 區塊鏈和加密資產的整合

- 新興市場中,銀行服務涵蓋不足的地區人口眾多。

- 開放銀行和API主導的生態系統擴展

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 美國聯邦儲備委員會

- 加拿大 - 加拿大銀行

- 歐洲

- 歐盟 - 歐洲中央銀行

- 英國金融行為監理局(FCA)

- 亞太地區

- 印度 - 印度儲備銀行

- 中國 - 中國人民銀行

- 拉丁美洲

- 巴西 - 巴西中央銀行

- 墨西哥 - 墨西哥銀行

- 中東和非洲

- 沙烏地阿拉伯 - 沙烏地阿拉伯中央銀行

- 阿拉伯聯合大公國 - 阿拉伯聯合大公國中央銀行

- 北美洲

- 投資與資金籌措分析

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 目前技術

- 分詞

- 端對端加密(E2EE/SSL/TLS)

- 基於 API 的支付整合

- 新興技術

- 人工智慧和機器學習驅動的詐欺偵測

- 支付編配平台

- 生物識別(指紋/臉部認證)

- 目前技術

- 專利趨勢(基於初步調查)

- 嵌入式金融與平台化

- 閘道器與非金融平台的整合

- 銀行即服務 (BaaS) 和白牌解決方案

- 市場和平台支付流程

- 收益分成和分期付款模式

- 跨境結算與外匯趨勢

- 多幣種處理架構

- 外匯影響及避險策略

- 按走廊跨境交易流量

- 國際和解機制與時間表

- 跨境貿易的監管挑戰

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 針對特定領域的生成式人工智慧應用案例和實施藍圖

- 風險、限制和監管考量

- 預測假設和情境分析(基於初步研究)

- 基本案例-驅動複合年成長率的關鍵宏觀經濟與產業變量

- 樂觀情境-宏觀經濟與產業的順風

- 悲觀情景-宏觀經濟放緩或產業逆風

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲(MEA)

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

- 企業級分層基準測試

- 層級分類標準與選擇標準

- 按銷售額、地區和創新能力分類的層級定位矩陣。

第5章 市場估算與預測:依付款閘道,2022-2035年

- 託管付款閘道

- 自架閘道器

- API託管付款閘道

- 本地銀行整合付款閘道

第6章 市場估計與預測:依支付方式分類,2022-2035年

- 卡片

- 網路銀行

- 統一支付介面(UPI)

- 錢包

- 其他付款方式

第7章 市場估計與預測:依公司規模分類,2022-2035年

- 大公司

- 中小企業

第8章 市場估算與預測:依部署類型分類,2022-2035年

- 雲

- 現場

- 混合

第9章 市場估計與預測:依產業分類,2022-2035年

- 零售與電子商務

- BFSI

- 旅遊與飯店

- 衛生保健

- 食品/飲料

- 交通運輸與出行

- 政府

- 其他

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 瑞典

- 荷蘭

- 波蘭

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 澳洲

- 新加坡

- 越南

- 印尼

- 馬來西亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 智利

- 中東和非洲(MEA)

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- 世界公司

- PayPal

- Stripe

- Fiserv

- FIS Global

- Adyen

- Visa

- Mastercard

- Amazon.com

- Block(Square)

- Global Payments

- US Bancorp

- Verifone Systems

- 本地公司

- Razorpay

- PhonePe

- Moneris Solutions

- Xendit

- Flutterwave

- 新興企業

- BlueSnap

- Cashfree Payments

- Midtrans

The Global Payment Gateway Market was valued at USD 32.7 billion in 2025 and is estimated to grow at a CAGR of 14.1% to reach USD 116.7 billion by 2035.

Market growth is strongly supported by the rapid expansion of digital payment adoption worldwide, as consumers and businesses increasingly shift toward secure and seamless electronic transactions. The payment gateway ecosystem plays a critical role in enabling safe authorization, processing, and routing of online payments across industries. Growing emphasis on transaction security, compliance, and fraud prevention continues to shape system architecture and innovation. Regulatory requirements and evolving cybersecurity standards are encouraging the integration of advanced security mechanisms such as encryption, tokenization, and multi-factor authentication. The industry is also witnessing increased competition as global payment platforms expand their service capabilities beyond basic transaction processing. Companies are focusing on delivering unified digital payment ecosystems that enhance user experience and support cross-border commerce. Rising e-commerce penetration, increasing smartphone usage, and the demand for real-time payment processing are further strengthening market expansion. Continuous technological advancements and the shift toward cashless economies are expected to sustain long-term growth in the payment gateway market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $32.7 Billion |

| Forecast Value | $116.7 Billion |

| CAGR | 14.1% |

The payment gateway market is evolving rapidly as businesses prioritize secure, efficient, and scalable digital payment solutions. Increasing reliance on online transactions is encouraging continuous innovation in payment infrastructure. Service providers are enhancing system capabilities to support faster processing, improved fraud detection, and seamless integration across platforms. The growing need for compliance and data protection is further driving advancements in secure payment technologies.

The hosted payment gateways segment held a 52.3% share in 2025, generating USD 17.1 billion. This segment leads due to its simplified deployment model and reduced operational burden for businesses. It allows secure handling of sensitive payment data through external systems, helping organizations meet compliance standards without extensive internal infrastructure investment. Its ease of integration and strong security framework continue to support widespread adoption.

The cards segment captured 47% share in 2025, valued at USD 15.4 billion. This segment remains dominant due to its global acceptance, established infrastructure, and high consumer confidence. Card-based transactions continue to be widely used across both online and offline payment channels. The presence of major card networks ensures standardized and reliable transaction processing for domestic and international payments.

U.S. Payment Gateway Market was valued at USD 9.8 billion in 2025 and is expected to grow at a CAGR of 12.4% from 2026 to 2035. Growth in the country is supported by a highly developed digital economy and widespread adoption of secure online payment systems. Strong internet penetration and increasing preference for fast and convenient transactions continue to drive market expansion. Ongoing modernization of payment infrastructure further supports industry development.

Key companies operating in the Payment Gateway Market include Adyen, Block (Square), FIS Global, Fiserv, Global Payments, Mastercard, PayPal, Stripe, U.S. Bancorp, and Visa. Companies in the Payment Gateway Market are strengthening their competitive position through continuous innovation and strategic expansion. They are investing heavily in advanced security technologies such as encryption, tokenization, and real-time fraud detection systems to enhance transaction safety. Expansion of API-driven platforms enables seamless integration with merchants across industries, improving scalability and user experience. Firms are also focusing on expanding cross-border payment capabilities to support global commerce. Strategic partnerships with financial institutions and technology providers are helping companies broaden their service ecosystems. Additionally, investments in cloud-based infrastructure and artificial intelligence are improving processing speed, operational efficiency, and compliance management, while customer-centric solutions and flexible pricing models are enhancing market adoption and long-term growth potential.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Gateway

- 2.2.3 Payment method

- 2.2.4 Organization size

- 2.2.5 Deployment mode

- 2.2.6 Industry vertical

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid growth in e-commerce and digital commerce

- 3.2.1.2 Mobile payment adoption and smartphone penetration

- 3.2.1.3 Globalization of business transactions and cross-border trade

- 3.2.1.4 Contactless payment preference post-pandemic

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Regulatory compliance complexity and regional variations

- 3.2.2.2 Dependency on banking infrastructure and network reliability

- 3.2.3 Market opportunities

- 3.2.3.1 Blockchain and cryptocurrency integration

- 3.2.3.2 Emerging markets with underbanked populations

- 3.2.3.3 Open banking and API-driven ecosystem expansion

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 US - Federal Reserve System

- 3.4.1.2 Canada - Bank of Canada

- 3.4.2 Europe

- 3.4.2.1 EU - European Central Bank

- 3.4.2.2 UK - Financial Conduct Authority

- 3.4.3 Asia Pacific

- 3.4.3.1 India - Reserve Bank of India

- 3.4.3.2 China - People's Bank of China

- 3.4.4 Latin America

- 3.4.4.1 Brazil - Banco Central do Brasil

- 3.4.4.2 Mexico - Banco de Mexico

- 3.4.5 Middle East & Africa

- 3.4.5.1 Saudi Arabia - Saudi Central Bank

- 3.4.5.2 UAE - Central Bank of the United Arab Emirates

- 3.4.1 North America

- 3.5 Investment & funding analysis

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Technology and innovation landscape

- 3.8.1 Current technologies

- 3.8.1.1 Tokenization

- 3.8.1.2 End-to-End Encryption (E2EE / SSL/TLS)

- 3.8.1.3 API-Based Payment Integration

- 3.8.2 Emerging technologies

- 3.8.2.1 AI & Machine Learning-Based Fraud Detection

- 3.8.2.2 Payment Orchestration Platforms

- 3.8.2.3 Biometric Authentication (Fingerprint/Face ID)

- 3.8.1 Current technologies

- 3.9 Patent landscape (Driven by Primary Research)

- 3.10 Embedded finance and platformization

- 3.10.1 Gateway integration into non-financial platforms

- 3.10.2 Banking-as-a-service (BaaS) and white-label solutions

- 3.10.3 Marketplace and platform payment flows

- 3.10.4 Revenue sharing and split payment models

- 3.11 Cross-border payments and FX dynamics

- 3.11.1 Multi-currency processing architecture

- 3.11.2 Foreign exchange rate impact and hedging strategies

- 3.11.3 Cross-border transaction flows by corridor

- 3.11.4 International settlement mechanisms and timelines

- 3.11.5 Regulatory challenges in cross-border transactions

- 3.12 Impact of AI & Generative AI on the Market

- 3.12.1 AI-driven disruption of existing business models

- 3.12.2 GenAI use cases & adoption roadmap by segment

- 3.12.3 Risks, limitations & regulatory considerations

- 3.13 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.13.1 Base Case - key macro & industry variables driving CAGR

- 3.13.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.13.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Gateway, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 Hosted payment gateways

- 5.3 Self-hosted gateways

- 5.4 API-hosted payment gateway

- 5.5 Local bank integration payment gateway

Chapter 6 Market Estimates & Forecast, By Payment method, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 Cards

- 6.3 Net banking

- 6.4 Unified Payments Interface (UPI)

- 6.5 Wallets

- 6.6 Other payment methods

Chapter 7 Market Estimates & Forecast, By Organization size, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 Large enterprises

- 7.3 Small & medium enterprises (SMEs)

Chapter 8 Market Estimates & Forecast, By Deployment mode, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 Cloud

- 8.3 On premises

- 8.4 Hybrid

Chapter 9 Market Estimates & Forecast, By Industry vertical, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 Retail & e-commerce

- 9.3 BFSI

- 9.4 Travel & hospitality

- 9.5 Healthcare

- 9.6 Food & beverage

- 9.7 Transportation & mobility

- 9.8 Government

- 9.9 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Sweden

- 10.3.7 Netherlands

- 10.3.8 Poland

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 South Korea

- 10.4.4 India

- 10.4.5 Australia

- 10.4.6 Singapore

- 10.4.7 Vietnam

- 10.4.8 Indonesia

- 10.4.9 Malaysia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Chile

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 PayPal

- 11.1.2 Stripe

- 11.1.3 Fiserv

- 11.1.4 FIS Global

- 11.1.5 Adyen

- 11.1.6 Visa

- 11.1.7 Mastercard

- 11.1.8 Amazon.com

- 11.1.9 Block (Square)

- 11.1.10 Global Payments

- 11.1.11 U.S. Bancorp

- 11.1.12 Verifone Systems

- 11.2 Regional players

- 11.2.1 Razorpay

- 11.2.2 PhonePe

- 11.2.3 Moneris Solutions

- 11.2.4 Xendit

- 11.2.5 Flutterwave

- 11.3 Emerging players

- 11.3.1 BlueSnap

- 11.3.2 Cashfree Payments

- 11.3.3 Midtrans

西班牙付款閘道:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)

西班牙付款閘道:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年) 2026年全球收據式優惠市場報告中國付款閘道:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

2026年全球收據式優惠市場報告中國付款閘道:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 付款閘道市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、最終用途、企業規模、地區和競爭格局分類,2021-2031 年

付款閘道市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、最終用途、企業規模、地區和競爭格局分類,2021-2031 年 付款閘道市場規模、佔有率和成長分析:按類型、企業規模、最終用戶和地區分類-2026-2033年產業預測

付款閘道市場規模、佔有率和成長分析:按類型、企業規模、最終用戶和地區分類-2026-2033年產業預測 付款閘道付款閘道市場:2026-2032年全球市場預測(按類型、支付方式、支付格式、部署方式、產業和組織規模分類)

付款閘道付款閘道市場:2026-2032年全球市場預測(按類型、支付方式、支付格式、部署方式、產業和組織規模分類) 付款閘道市場報告:按應用程式、互動方式和地區分類(2026-2034 年)

付款閘道市場報告:按應用程式、互動方式和地區分類(2026-2034 年) 付款閘道市場規模、佔有率和趨勢分析報告:按類型、企業規模、最終用途、地區和細分市場預測(2026-2033 年)

付款閘道市場規模、佔有率和趨勢分析報告:按類型、企業規模、最終用途、地區和細分市場預測(2026-2033 年) 行動付款閘道市場預測:至 2034 年-按組件、支付類型、部署模式、企業規模、最終用戶和地區分類的全球分析

行動付款閘道市場預測:至 2034 年-按組件、支付類型、部署模式、企業規模、最終用戶和地區分類的全球分析 全球付款閘道市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球付款閘道市場規模、佔有率、趨勢和成長分析報告(2026-2034)