|

市場調查報告書

商品編碼

2073317

製造業學習管理系統(LMS):市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Learning Management System (LMS) In Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

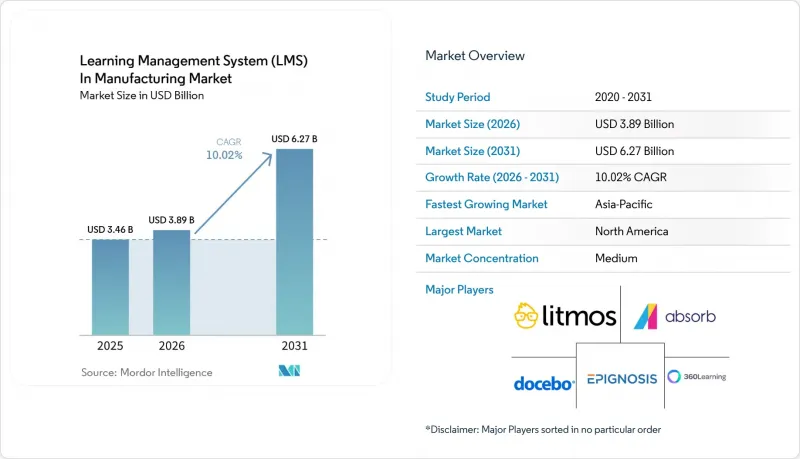

據 Mordor Intelligence 稱,2025 年製造業學習管理系統 (LMS) 市場價值為 34.6 億美元,2026 年為 38.9 億美元,預計到 2031 年將達到 62.7 億美元,2026 年至 2031 年的複合年成長率為 10.02%。

本報告按元件(軟體和服務)、部署模式(雲端、本地部署、混合部署)、最終用戶企業規模(大型企業和中小企業)、培訓能力(技術技能培訓等)、最終用戶行業(汽車行業等)和地區進行細分。市場預測以美元計價。

全球製造業學習管理系統(LMS)市場趨勢與洞察

面向智慧工廠工業4.0的技能再培訓

隨著數位化工具的運用改變了生產車間所需的技能,製造業學習管理系統(LMS)市場正受到工廠營運模式全面重塑的影響。世界經濟論壇(WEF)預測,到2030年,現有員工39%的技能將被改造或過時,領先的製造業雇主指出,人工智慧、巨量資料、機器人技術和新材料是目前最迫切的能力缺口。這種轉變要求學習系統不能僅僅提供課程和更新年度合規培訓,而應支持特定職位的能力建設。世界經濟論壇和麥肯錫公司的研究表明,如果缺乏職業發展和技能提升途徑,超過40%的Z世代製造業員工會在3-6個月內考慮離職,而這種人員流動造成的成本高達每位員工5.2萬美元。在製造業LMS領域,能夠將技能與機器類型、工作單元和職位組關聯起來,並在初始部署後仍能保持效用的平台,其價值就顯得尤為重要。僅提供課程庫的供應商可能會失去長期競爭力,因為製造商越來越將結構化的技能架構視為工廠核心基礎設施的組成部分,而不僅僅是培訓的附加部分。

追蹤合規性和認證情況,以應對審計挑戰

製造業的學習管理系統 (LMS) 持續受益於員工在安全、品質和操作流程方面準備的記錄需求。製造商面臨雙重文件負擔:監管要求提供清晰的培訓記錄,而更廣泛的管理系統則需要證明受控流程、認證和定期更新。這使得集中式報告、自動提醒和版本控制的內容比在監管較少的辦公環境中更為重要。在製造業 LMS 市場,關鍵的採購決策在於平台能否快速、一致地跨地域建立可審計的記錄。這一趨勢有利於那些能夠簡化製造商對電子表格和分散工具的整合,並將認證、培訓完成狀態和角色特定權限整合到單一、可審計的工作流程中的供應商。因此,可審計的報告功能和證書可追溯性正在創造一種定價環境,比單純的學習交付功能更能帶來商業性優勢。

與傳統ERP、MES和HRIS系統整合的複雜性。

在製造業領域,學習管理系統(LMS)在與深度嵌入式企業軟體堆疊整合時仍面臨許多挑戰。預計到2026年,製造業ERP整合專案的平均預算超支將達到72%,而離散型製造商的預算超支甚至高達215%。這個問題也蔓延至學習系統部署,因為使用者配置、資質記錄、職位角色、工廠層級和訓練觸發機制通常需要在ERP、MES和HRIS等原本不具備互通性的系統中進行管理。對於中型製造商而言,這一負擔尤其沉重,因為他們已經投資了核心系統,但缺乏內部團隊來開發客製化API,而且整合週期往往更長。在製造業LMS市場,現成的連接器不再是高階差異化優勢,而是准入的最低要求,因為買家在考慮某個平台之前就期望這些功能是標配。因此,連接器庫不足或實施深度有限的供應商將面臨更長的銷售週期、更高的專案風險,以及在真正需要數位化培訓系統的目標客戶群中更低的採用率。

細分市場分析

預計到2025年,軟體將佔製造業學習管理系統(LMS)市場規模的72.34%,凸顯了平台授權已成為大型製造商和受監管工廠採用LMS的基礎。軟體層是大多數LMS採用的核心,因為製造商最初需要一個能夠集中管理學習路徑、認證記錄和使用者的系統。 2019年至2025年間,隨著越來越多的工廠採用雲端平台取代傳統的講師主導或以電子表格為基礎的培訓管理方式,這個採用群體不斷擴大。在製造業LMS市場,軟體也受益於運行常規合規計畫並最大限度減少跨工廠和班次的人工監管的需求。這在更深層的服務需求顯現之前,就形成了以平台主導的元件結構。

然而,預計到2031年,服務業的複合年成長率將達到11.23%,這表明在初始部署之後,買家的期望發生了轉變。隨著部署從基本的合規性追蹤轉向技能智慧、人工智慧驅動的內容創建、跨工廠分析和工作流程整合,製造商對部署、配置和託管支援的需求日益成長。在學習管理系統(LMS)方面,製造商更傾向於選擇了解其製造流程的供應商和合作夥伴,而不是那些僅提供通用企業級LMS功能的供應商。這也反映出製造業LMS市場正在發生廣泛的轉變,轉向捆綁式交付模式,這種模式不僅重視軟體許可,還重視成果、管治和部署支援。因此,能夠將平台深度與工廠級執行能力結合的供應商,在培訓項目日益融入營運的過程中,將佔據越來越大的業務收益佔有率。

截至2025年,基於雲端的部署將佔據製造業學習管理系統(LMS)市場68.47%的佔有率,預計到2031年將以12.37%的複合年成長率保持最高成長率。這一組合意義重大,因為它表明,最大的部署模式在不被小眾替代方案蠶食市場佔有率的情況下,持續擴大其領先優勢。製造商之所以青睞雲端系統,是因為它們能夠實現跨分散式工廠的快速部署,並減輕管理本地伺服器相關的基礎設施負擔。在製造業LMS市場,雲端部署也對那些尋求定期更新、易於管理且初始投資較低的買家極具吸引力。這些特性對需要企業級培訓管理但又無法承擔在每個地點部署複雜現場基礎設施成本的中型製造商尤其具有吸引力。

然而,當公共雲端環境的使用受到培訓資料、檢驗規則或特定產業法規的限制時,本地部署和混合模式仍然是重要的選擇。製藥公司仍優先考慮受控變更管理,而國防相關企業可能面臨更嚴格的培訓記錄及相關資料處理法規。因此,混合部署仍然是一種切實可行的折衷方案,它允許企業在利用雲端提供的內容和各種管理工具的同時,將敏感記錄保留在自身控制之下。在製造業學習管理系統 (LMS) 領域,這種平衡在歐洲和亞洲部分地區至關重要,因為這些地區的資料居住法規以及成本和速度都會顯著影響架構決策。因此,儘管製造業 LMS 市場正朝著雲端整合以實現規模經濟,但在需要兼顧柔軟性和更嚴格控制的高度監管行業中,混合模式仍然有其存在的空間。

區域分析

到2025年,北美將佔據製造業學習管理系統(LMS)市場38.69%的佔有率。這主要歸功於該地區多層級合規要求的集中以及多工廠製造商對符合審核要求的培訓基礎設施的需求。美國佔據了該地區最大的需求佔有率,因為記錄學習、定期認證和工廠級報告在製造業合規和員工管理中仍然發揮核心作用。加拿大和墨西哥透過跨境生產網路進一步推動了這一需求,這些國家的製造商需要符合美國標準的同步學習工作流程和多語言交付。因此,製造業LMS市場在北美已根深蒂固,因為培訓系統不僅用於提供學習,還用於證據展示、可追溯性和營運一致性。這在該地區形成了強大的應用基礎,使得其他地區難以匹敵其目前的市場佔有率。

歐洲仍然是製造業學習管理系統 (LMS) 市場的關鍵區域。這是因為與其他許多地區相比,合規性要求和資料管治需求對平台選擇的影響更為直接。需求主要集中在德國、英國和法國,這些國家的負責人必須在培訓管理與對資料架構和資料儲存位置的嚴格要求之間取得平衡。 2026 年 2 月,位於德國普弗龍滕的一座 4,500 平方米的培訓中心正式啟用,這凸顯了該地區對系統化人力資源開發基礎設施的持續投入,而不僅限於正式的 LMS 部署。歐洲的部署選擇也受到以下需求的驅動:既要滿足可擴展的內容傳送需求,又要兼顧區域特定的記錄和使用者資料管理。這些趨勢持續推動混合雲和注重合規性的雲端模式在該地區領先的製造群中得到應用。

亞太地區是成長最快的地區,預計到2031年將以14.37%的複合年成長率成長,這主要得益於中國、印度、韓國、日本以及正在蓬勃發展的東南亞地區的製造地。在中國,一項針對2025年數位化生產管理的調查顯示,超過65%的製造業企業正在試用人工智慧驅動的培訓推薦系統,預計採用率將超過85%。日本經濟產業省指出,製造業的數位轉型進展仍然不平衡,許多企業仍專注於單一流程的「改善」(kaizen)改進,而不是全公司範圍內的數位化技能發展。印度製造業的擴張和東南亞近岸外包的推進,持續催生一支新的勞動力隊伍,他們需要快速入職、職位認證和多語言學習支援。南美洲、中東和非洲雖然目前市場佔有率仍然較小,但隨著產業多元化和對正式資格認證的追蹤變得日益重要,這些地區的市場佔有率正在擴大。據報道,到 2026 年,南美洲工廠 23% 的非計劃停產將是由於不合格人員的不當安排造成的。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 宏觀經濟因素對市場的影響

- 市場促進因素

- 智慧工廠中為符合工業4.0要求而進行的技能再培訓

- 追蹤可審計的合規性和認證情況。

- 跨工廠和班次的多地點培訓標準化

- 針對非辦公室人員的行動與離線學習

- 利用人工智慧將標準作業程序 (SOP) 轉化為微學習內容

- 在工廠門口對承包商和臨時工進行身份驗證。

- 市場限制因素

- 將傳統ERP、MES和HRIS系統整合起來的複雜性

- 限制學習時間:效率與時間之間的權衡

- 各工廠多語言內容的管治

- 資料居住要求和智慧財產權外洩問題

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 軟體

- 服務

- 按部署模式

- 基於雲端的

- 現場

- 混合

- 最終用戶公司規模

- 大公司

- 小型企業

- 按功能進行訓練

- 技術技能培訓

- 安全與合規培訓

- 設備和機械培訓

- 品質和精益生產方法培訓

- 業務流程培訓

- 新進員工培訓

- 其他培訓職能

- 按最終用戶行業分類

- 車

- 電子和半導體

- 工業機械和設備

- 藥品和化學品

- 食品/飲料

- 航太/國防

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 紐西蘭

- 印尼

- 泰國

- 越南

- 馬來西亞

- 新加坡

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介。

- Docebo SpA

- Absorb Software Inc.

- Litmos US, LP

- Epignosis LLC

- iSpring Solutions, Inc.

- Intellum, Inc.

- Alchemy Systems, LP

- Vector Solutions LLC

- 360Learning SAS

- Zensai ApS

- Dozuki, Inc.

- Valamis Group Oy

- PlatCore, LLC

- Continu, Inc.

- eLeaP Software LLC

- Nvolve Group Limited

- Schoox, Inc.

- SkyPrep Inc.

- Gyrus Systems LLC

- Moodle Pty Ltd.

- Latitude CG, LLC

第7章 市場機會與未來展望

According to Mordor Intelligence, the learning management system (LMS) market in manufacturing was valued at USD 3.46 billion in 2025 and USD 3.89 billion in 2026, and is forecast to reach USD 6.27 billion by 2031, expanding at a CAGR of 10.02% over 2026-2031.

This report is Segmented by Component (Software and Services), Deployment Model (Cloud-Based, On-Premises, and Hybrid), End-User Enterprise Size (Large Enterprises and Small and Medium-Sized Enterprises), Training Function (Technical Skills Training, and More), End-User Industry (Automotive and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Learning Management System (LMS) In Manufacturing Market Trends and Insights

Industry 4.0 Reskilling Across Smart Factories

The LMS in the manufacturing market is being shaped by a broader redesign of factory work as digital tools change the skills required on the production floor. The World Economic Forum projected that 39% of existing worker skill sets will be transformed or outdated by 2030, with advanced manufacturing employers ranking AI and big data, robotics, and new materials among their most urgent capability gaps. That shift means learning systems are now expected to support role-based capability building, not just course delivery or annual compliance refreshers. The World Economic Forum and McKinsey and Company also found that more than 40% of Gen Z employees in manufacturing consider leaving within 3-6 months when career development and skill-building pathways are missing, and the attrition cost reached USD 52,000 per departing frontline employee. In the LMS in the manufacturing market, this raises the value of platforms that can map skills to machine types, work cells, and job families in a way that stays useful after the first deployment. Vendors that provide only course libraries face weaker long-term positioning because manufacturers are increasingly treating structured skills architecture as part of core plant infrastructure rather than a simple training add-on.

Audit-Ready Compliance And Certification Tracking

The LMS in the manufacturing market continues to benefit from the need to maintain documented evidence of workforce readiness across safety, quality, and operating procedures. Manufacturers face a dual documentation burden because regulatory requirements call for explicit training records, while broader management systems require proof of controlled processes, certifications, and recurring refresh cycles. This makes centralized reporting, automated reminders, and version-controlled content much more important than in less regulated office environments. In the LMS manufacturing market, purchasing decisions are often driven by whether the platform can produce inspection-ready records quickly and consistently across sites. That preference strengthens vendors that can tie certifications, training completions, and role permissions into a single auditable workflow, rather than leaving manufacturers to reconcile spreadsheets and disconnected point tools. The result is a pricing environment in which audit-ready reporting and credential traceability support stronger commercial positioning than basic learning-delivery features alone.

Legacy ERP, MES, And HRIS Integration Complexity

The LMS in the manufacturing market still faces a major restraint when new learning systems have to connect with deeply embedded enterprise software stacks. In 2026, manufacturing ERP integration projects exceeded initial budgets by an average of 72%, while discrete manufacturers saw overruns as high as 215%. That problem carries over into learning deployments because user provisioning, credential records, job roles, plant hierarchies, and training triggers often sit across ERP, MES, and HRIS systems that were not designed to work together. The burden is especially heavy for mid-market manufacturers that have already invested in core systems but lack internal teams for custom API work and long integration cycles. In the LMS manufacturing market, pre-built connectors now function more as minimum entry requirements than as premium differentiators, because buyers expect them before a platform is even shortlisted. Vendors with weak connector libraries or limited implementation depth, therefore, face slower sales cycles, higher project risk, and lower adoption among buyers that otherwise need digital training systems.

Other drivers and restraints analyzed in the detailed report include:

- Multi-Site Training Standardization Across Plants And Shifts

- Mobile And Offline Learning For Deskless Workers

- Production-Time Trade-Offs That Limit Learning Hours

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 72.34% of the LMS market size in manufacturing in 2025, underscoring how strongly platform licenses already anchor adoption across large manufacturers and regulated plants. The software layer became the center of most deployments because manufacturers first needed systems that could manage learning paths, certification records, and user administration in one place. That installed base grew across 2019-2025 as cloud platforms replaced instructor-led and spreadsheet-led training administration in more facilities. In the LMS in the manufacturing market, software also benefited from the need to run recurring compliance programs with less manual oversight across plants and shifts. This made the component mix look heavily platform-led before deeper service demand emerged.

Services, however, are projected to grow at a 11.23% CAGR through 2031, suggesting a shift in what buyers now expect after the first rollout. As deployments move from basic compliance tracking into skills intelligence, AI-assisted content creation, cross-plant analytics, and workflow integration, manufacturers increasingly need implementation, configuration, and managed support. In the LMS, the manufacturing industry favors providers and partners with manufacturing process knowledge over generic enterprise LMS capacity alone. It also reflects a broader shift in the LMS market for manufacturing toward bundled delivery models where the value lies in outcomes, governance, and adoption support, not just in access to software seats. Vendors that can combine platform depth with plant-level execution are therefore better positioned to capture a growing share of services revenue as training programs become more embedded in operations.

Cloud-based deployment held 68.47% of the LMS market share in manufacturing in 2025 and also posted the fastest projected CAGR at 12.37% through 2031. That combination is notable because it shows the largest deployment model is still extending its lead rather than losing ground to niche alternatives. Manufacturers have been drawn to cloud systems because they enable faster rollouts across distributed plants and reduce the infrastructure burden of local server management. In the LMS market for manufacturing, cloud adoption also appeals to buyers who want regular updates, easier administration, and lower upfront investment. These features are especially attractive to mid-sized manufacturers that need enterprise-grade training control but cannot justify the complex on-site infrastructure required at each location.

Even so, on-premises and hybrid models remain relevant where training data, validation rules, or sector-specific controls limit the use of public cloud environments. Pharmaceutical manufacturers continue to prioritize controlled change management, while defense-related operations may face stricter rules for handling training records and supporting data. Hybrid deployment, therefore, remains a practical middle ground because it lets companies keep sensitive records under local control while still using cloud-delivered content and broader administrative tools. In the LMS in the manufacturing industry, that balance matters in Europe and parts of Asia where data residency rules shape architecture decisions as much as cost and speed do. The LMS market in manufacturing is therefore consolidating around cloud for scale, but it still leaves room for hybrid models in regulated verticals that need both flexibility and tighter control.

Complete Report Scope:

- By Component

- Software

- Services

- By Deployment Model

- Cloud-Based

- On-Premises

- Hybrid

- By End-user Enterprise Size

- Large Enterprises

- Small and Medium-sized Enterprises

- By Training Function

- Technical Skills Training

- Safety and Compliance Training

- Equipment and Machinery Training

- Quality and Lean Manufacturing Training

- Operational Process Training

- Employee Onboarding

- Other Training Functions

- By End-user Industry

- Automotive

- Electronics and Semiconductors

- Industrial Machinery and Equipment

- Pharmaceuticals and Chemicals

- Food and Beverage

- Aerospace and Defense

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- New Zealand

- Indonesia

- Thailand

- Vietnam

- Malaysia

- Singapore

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America held a 38.69% share of the LMS market in manufacturing in 2025, driven by layered compliance requirements and a dense base of multi-site manufacturers that need audit-ready training infrastructure. The United States accounts for the largest share of regional demand because documented learning, recurring certifications, and plant-level reporting remain central to manufacturing compliance and workforce governance. Canada and Mexico add to that demand through cross-border production networks, where manufacturers need synchronized learning workflows and multilingual delivery that can align with U.S.-based standards. The LMS market in manufacturing is therefore deeply established in North America because training systems are used not only for learning delivery but also for proof, traceability, and operational consistency. This gives the region a strong installed base that is difficult for other geographies to match in current share.

Europe remains an important region for the LMS in the manufacturing market because compliance expectations and data governance needs shape platform selection more directly than in many other regions. Demand is concentrated in Germany, the United Kingdom, and France, where buyers must balance training control with close attention to data architecture and residency requirements. A 4,500 m2 training center opened in Pfronten, Germany, in February 2026, which underlines the region's continued commitment to structured workforce development infrastructure even outside formal LMS deployments. European deployment choices are also shaped by the need to balance scalable content delivery with region-specific control over records and user data. That dynamic keeps hybrid and compliance-aware cloud models relevant across advanced manufacturing clusters in the region.

Asia-Pacific is the fastest-growing geography at a 14.37% CAGR through 2031, led by China, India, South Korea, Japan, and the expanding Southeast Asian manufacturing base. In China, a 2025 study on digital production management reported that more than 65% of manufacturing enterprises were piloting AI-powered training recommendation systems, with penetration expected to exceed 85%. Japan's Ministry of Economy, Trade and Industry noted that manufacturers were still advancing digital transformation unevenly, with many firms remaining focused on Kaizen improvements in individual processes rather than enterprise-wide digital upskilling. India's manufacturing expansion and Southeast Asia's nearshoring gains continue to create new cohorts of workers who need rapid onboarding, role certification, and multilingual learning support. South America, the Middle East, and Africa remain smaller in terms of current share, but they are expanding as industrial diversification and formal credential tracking become more important. In 2026, it was reported that 23% of unplanned production stoppages in South American plants originated from the incorrect assignment of unqualified personnel.

- Docebo S.p.A.

- Absorb Software Inc.

- Litmos US, L.P.

- Epignosis LLC

- iSpring Solutions, Inc.

- Intellum, Inc.

- Alchemy Systems, L.P.

- Vector Solutions LLC

- 360Learning S.A.S.

- Zensai ApS

- Dozuki, Inc.

- Valamis Group Oy

- PlatCore, LLC

- Continu, Inc.

- eLeaP Software LLC

- Nvolve Group Limited

- Schoox, Inc.

- SkyPrep Inc.

- Gyrus Systems LLC

- Moodle Pty Ltd.

- Latitude CG, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 Industry 4.0 Reskilling Across Smart Factories

- 4.3.2 Audit-Ready Compliance and Certification Tracking

- 4.3.3 Multi-Site Training Standardization Across Plants and Shifts

- 4.3.4 Mobile and Offline Learning for Deskless Workers

- 4.3.5 AI Conversion of SOPs Into Microlearning

- 4.3.6 Contractor and Temporary Labor Credentialing at Plant Gates

- 4.4 Market Restraints

- 4.4.1 Legacy ERP, MES, and HRIS Integration Complexity

- 4.4.2 Production-Time Trade-Offs That Limit Learning Hours

- 4.4.3 Multilingual Content Governance Across Plants

- 4.4.4 Data Residency and IP Leakage Concerns

- 4.5 Industry Value-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Comptetive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Model

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By End-user Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-sized Enterprises

- 5.4 By Training Function

- 5.4.1 Technical Skills Training

- 5.4.2 Safety and Compliance Training

- 5.4.3 Equipment and Machinery Training

- 5.4.4 Quality and Lean Manufacturing Training

- 5.4.5 Operational Process Training

- 5.4.6 Employee Onboarding

- 5.4.7 Other Training Functions

- 5.5 By End-user Industry

- 5.5.1 Automotive

- 5.5.2 Electronics and Semiconductors

- 5.5.3 Industrial Machinery and Equipment

- 5.5.4 Pharmaceuticals and Chemicals

- 5.5.5 Food and Beverage

- 5.5.6 Aerospace and Defense

- 5.5.7 Other End-user Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 New Zealand

- 5.6.4.7 Indonesia

- 5.6.4.8 Thailand

- 5.6.4.9 Vietnam

- 5.6.4.10 Malaysia

- 5.6.4.11 Singapore

- 5.6.4.12 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 Docebo S.p.A.

- 6.4.2 Absorb Software Inc.

- 6.4.3 Litmos US, L.P.

- 6.4.4 Epignosis LLC

- 6.4.5 iSpring Solutions, Inc.

- 6.4.6 Intellum, Inc.

- 6.4.7 Alchemy Systems, L.P.

- 6.4.8 Vector Solutions LLC

- 6.4.9 360Learning S.A.S.

- 6.4.10 Zensai ApS

- 6.4.11 Dozuki, Inc.

- 6.4.12 Valamis Group Oy

- 6.4.13 PlatCore, LLC

- 6.4.14 Continu, Inc.

- 6.4.15 eLeaP Software LLC

- 6.4.16 Nvolve Group Limited

- 6.4.17 Schoox, Inc.

- 6.4.18 SkyPrep Inc.

- 6.4.19 Gyrus Systems LLC

- 6.4.20 Moodle Pty Ltd.

- 6.4.21 Latitude CG, LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

銀行、金融服務和保險 (BFSI) 學習管理系統 (LMS):市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031)

銀行、金融服務和保險 (BFSI) 學習管理系統 (LMS):市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031) 到 2034 年,以神經多樣性為重點的企業培訓專案的市場預測:按培訓類型、交付形式、經營模式、最終用戶和地區進行的全球分析。創新技能學習平台市場預測至2034年-全球分析(按組件、技能類型、交付方式、平台類型、最終用戶和地區分類)

到 2034 年,以神經多樣性為重點的企業培訓專案的市場預測:按培訓類型、交付形式、經營模式、最終用戶和地區進行的全球分析。創新技能學習平台市場預測至2034年-全球分析(按組件、技能類型、交付方式、平台類型、最終用戶和地區分類) K-12輔導市場報告:趨勢、預測與競爭分析(至2031年)神經包容性職場平台市場預測至2032年:按平台類型、部署類型、組織規模、最終用戶和地區分類的全球分析

K-12輔導市場報告:趨勢、預測與競爭分析(至2031年)神經包容性職場平台市場預測至2032年:按平台類型、部署類型、組織規模、最終用戶和地區分類的全球分析 K-12教育輔導服務:全球市場佔有率和排名、總收入和需求預測(2025-2031年)

K-12教育輔導服務:全球市場佔有率和排名、總收入和需求預測(2025-2031年)