|

市場調查報告書

商品編碼

2073302

薪資不平等分析平台:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Pay Equity Analytics Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

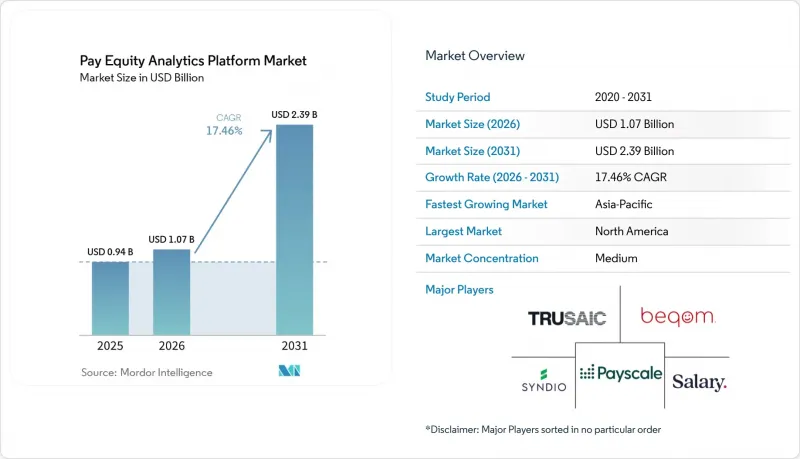

根據 Mordor Intelligence 預測,薪資差距分析平台的市場規模預計將從 2025 年的 9.4 億美元和 2026 年的 10.7 億美元成長到 2031 年的 23.9 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 17.46%。

本報告按部署模式(雲端部署和本地部署)、組織規模(大型企業和中小企業)、應用領域(薪酬差距分析、基準測試和薪酬分析、合規和監管報告等)、最終用戶行業(銀行、金融服務和保險、IT和電信等)以及地區進行細分。市場預測以美元計價。

全球薪資差距分析平台市場趨勢及洞察

歐盟工資透明度指令即時引發了對合規性的要求。

2026年6月7日是將相關規定納入國內法的最後期限,無疑是薪資差距分析平台市場最明確的短期促進因素。該指令要求公開求職者的薪資範圍,確保員工能夠獲取薪資水平信息,限制查閱薪資歷史的做法,並禁止薪資保密條款,從而將薪酬數據從一次性審查轉變為受監管的業務流程。擁有150名或以上員工的雇主必須在2027年6月7日前發布首份性別薪資差距報告,擁有100名或以上員工的雇主則需在2031年前跟進。該指令也設定了5%的不合理薪資差距閾值,要求雇主在六個月內若未能糾正差距,則必須與員工代表合作進行薪資評估。這些因素共同推動薪資差距分析平台市場朝向能夠進行員工分類、追蹤整改期限並在多個司法管轄區維護完整記錄的、可隨時接受審計的系統發展。同樣的法規也擴大了薪資差距分析平台的客戶群。這是因為以前不受正式報告要求約束的中型雇主現在正在採取措施解決合規問題。

美國各州工資透明法案正在推動合規市場出現片段化現象。

州級監理發展是薪資差距分析平台市場的第二大需求來源。科羅拉多持續執行其《同工同酬法》,據報道,違規罰款總額已達 841,500 美元。這表明,違規不再只是聲譽風險,而是實實在在的經濟損失。馬薩諸塞州現在強制要求在特定情況下披露薪資範圍,該法律適用於擁有 25 名或以上員工的雇主。這實際上降低了實施正式工資透明度管理的門檻。對於營運遠距和分散式團隊的雇主而言,挑戰不在於單一的法規,而是如何同時協調多個州關於發布、記錄保存和報告的規定。因此,薪資差距分析平台市場受益於對集中式政策邏輯、可重複使用職位結構和標準化揭露工作流程的需求。這種零散的局面也有利於那些能夠快速更新規則庫並透過單一報告層呈現特定州輸出結果的供應商。

薪資資料的隱私風險限制了企業採用這些資料。

資料保密性仍然是薪資差距分析平台市場面臨的最大障礙之一。由於這些平台必須處理薪酬、人口統計屬性、績效資訊和工作經驗等數據,買家通常會根據適用於整個人力資源系統的最嚴格標準來評估它們。 Evenpay 將符合 GDPR 標準的歐盟資料儲存和安全管理作為其產品價值的一部分,這表明在受監管的市場中,隱私期望與產品應用緊密相關。 beqom 的「PayAnalytics」專注於在企業級框架內進行薪酬差距校正和勞動力分析,反映了當前認證和管治已成為購買的最低要求的現狀。在薪資差距分析平台市場,這對規模小規模的供應商來說是一個巨大的挑戰,因為買家要求在整合薪資數據和員工記錄之前,必須提供清晰的數據處理證據。因此,雖然隱私法規增加了對專業平台的需求,但也延緩了一些交易的完成。

細分市場分析

預計到2025年,基於雲端的部署將佔薪資差距分析平台市場規模的76.18%,並有望在2031年之前以18.94%的複合年成長率成長。這種在薪資差距分析平台市場的主導地位反映了整合薪資、人力資源資訊系統(HRIS)、招募管理系統(ATS)和薪酬方案資料的實際需求,而無需依賴重複的檔案傳輸。此外,雲端模式允許供應商從單一管理環境更新所有客戶的報告邏輯,從而更有效地應對跨國政策的變化。這在歐洲和北美地區變得日益重要,因為這些地區的法規往往相互重疊,雇主需要能夠適應頻繁法律變更的系統,而無需每次都啟動新的IT專案。

在一些金融機構、政府機構和對託管要求嚴格的組織中,本地部署工具仍然佔據一定地位。然而,對於許多買家而言,快速部署、集中管理和強大的整合路徑如今比他們先前對雲端的擔憂更為重要,這使得薪資差距分析平台市場的需求重心轉向了託管環境。 Payscale 計劃在 2025 年初擴展其整合功能,這清楚地表明了競爭焦點從獨立分析轉向整合部署的轉變。類似的趨勢也出現在企業採購活動中,買家越來越重視平台能否從一開始就整合到現有的人力資源管理 (HCM) 工作流程中。因此,在薪資差距分析平台產業,部署方式的選擇正從基礎設施偏好轉向客戶能夠多快地從原始資料過渡到合理的決策。

預計到2025年,大型企業(SME)將佔據66.42%的市場佔有率,而中小企業(SME)預計到2031年將以20.87%的複合年成長率成長。薪資差距分析平台市場仍嚴重偏向大型企業。這是因為大型企業的業務涉及更多法人實體、更廣泛的地理範圍和更複雜的薪酬結構,這既增加了報告的複雜性,也增加了糾正措施的風險。據Syndio稱,其平台管理遍布100個國家超過1000萬名員工的薪資,並為全球約400家公司提供服務,其中包括超過50%的財富100強企業。如此高的應用水準表明,大型企業客戶仍然是薪酬差距分析平台市場的商業性基礎。

然而,預計成長最快的將是中小企業雇主,他們將首次受到正式揭露和報告義務的約束。在歐洲,員工人數達到或超過100人的報告門檻將在預測期內大幅擴大潛在客戶群。在美國,一些州已經制定了適用於小規模雇主的法規。例如,麻州規定,在適用情況下,擁有25名或以上員工的雇主必須揭露薪資範圍。 Ravio在2025年5月完成的1,200萬美元A輪資金籌措旨在拓展國際業務,反映出投資者對能夠惠及全球企業和成長型企業的工具的興趣。因此,隨著供應商搶佔這一新興中型市場的需求,預計薪資差距分析平台市場將出現更簡化的包裝、更快的設定和模組化定價等趨勢。

區域分析

到2025年,北美將佔據薪資差距分析平台市場44.26%的佔有率,成為最大的市場區域。該地區受益於獨特的法律執行力度、雇主意識以及軟體應用的高接受度,尤其是在美國和加拿大。在美國,薪資差距分析平台市場的發展得益於各州不斷擴展的薪資揭露和報告要求,雇主必須管理其分散的員工隊伍。科羅拉多的執法記錄顯示了這一環境的嚴峻性,該州報告稱,因違反《同工同酬法》而開出的罰款總合841,500美元。

歐洲薪資差距分析平台市場是該地區第二大市場,正經歷一些最徹底的監管改革。歐盟的工資透明度法規適用於所有27個成員國,這使得該地區的合規範圍異常廣泛,涵蓋了私部門和公共部門的就業。在2026年6月各國法律納入該法規的最後期限之後,報告義務將逐步對擁有150名或以上員工的雇主實施,隨後是擁有100名或以上員工的雇主,這將形成一個多年周期,而非一次性的快速響應。 5%的「不合理差距」閾值也增加了營運風險,因為未解決的問題可能導致雇主被納入聯合薪資評估流程。

亞太地區是薪資差距分析平台市場成長最快的區域市場,預計到2031年將以22.41%的複合年成長率成長。這項成長主要得益於跨國公司尋求在其全球營運中建立統一的報告框架,以及當地企業開始正式實施薪酬透明度措施。與北美和西歐相比,亞太地區的趨勢仍較為被動,一旦法律義務明確,採用率就會加快。隨著區域雇主改善其人力資源數據基礎設施並要求更緊密地整合薪資核算和福利管治,這一差距為進一步成長留下了空間。南美洲、中東和非洲在薪資差距分析平台市場仍處於起步階段,但當地的報告要求正開始為能夠在地化工作結構和合規工作流程的供應商創造商機。 beqom的PayAnalytics已發布了針對南非雇主的指南,內容涉及《就業平等法》下的年度報告和即將訂定的透明度要求,這表明該地區存在不斷擴大的商機。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 歐盟工資透明度指令的實施期限為2026年。

- 美國各州擴大工資透明度和工資數據報告法律的範圍

- 持續進行薪酬差距審計,並將課責轉移到董事會層級。

- 雲端人力資源堆疊整合和工作流程自動化

- 將公平薪酬指南納入招募、晉升和績效考核決策中。

- 對工作架構和同等價值工作分類的需求日益成長。

- 市場限制因素

- 高度敏感獎勵資料的隱私和安全風險

- 不合理的工作架構和分散的人力資源數據

- 未糾正的審計結果引發的法律揭露風險

- 薪資基準資料的授權和本地化成本負擔

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 部署模式

- 基於雲端的

- 現場

- 按組織規模

- 大公司

- 小型企業

- 透過使用

- 薪資差距分析

- 基準測試和獎勵分析

- 合規與監理報告

- 其他用途

- 按最終用戶行業分類

- BFSI

- IT/通訊

- 醫療保健和生命科學

- 零售與電子商務

- 工業製造

- 政府/公共部門

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Syndio Solutions, Inc.

- Trusaic

- Salary.com, LLC

- Payscale, Inc.

- beqom SA

- Performing Ideas HR AB

- Sysarb AB

- PayGap ApS

- Evenpay Oy

- Claritava GmbH

- Opacity ApS

- Figures SAS

- OpenComp, Inc.

- ThinkWhy LLC

- Compport Private Limited

- HRsoft, Inc.

- Ravio Technologies Ltd.

- Parity Software, LLC

- Decusoft

- Compa Technologies, Inc.

- equidi Pty Ltd

- EDGE Strategy AG

第7章 市場機會與未來展望

According to Mordor Intelligence, the pay equity analytics platform market size is projected to expand from USD 0.94 billion in 2025 and USD 1.07 billion in 2026 to USD 2.39 billion by 2031, registering a CAGR of 17.46% between 2026 and 2031.

This report is Segmented by Deployment Mode (Cloud-Based, and On-Premises), Organization Size (Large Enterprises, and SMEs), Application (Pay Gap Analytics, Benchmarking and Compensation Analysis, Compliance and Regulatory Reporting, and More), End-User Industry (BFSI, IT and Telecommunications, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Pay Equity Analytics Platform Market Trends and Insights

EU Pay Transparency Directive Creates Immediate Compliance Demand

The June 7, 2026, transposition deadline has become the clearest near-term trigger for the pay equity analytics platform market. The directive requires salary-range transparency for candidates, gives employees access to pay-level information, restricts salary history practices, and bars pay secrecy clauses, which turns compensation data into a regulated operating process rather than a one-time review. Employers with 150 or more employees must publish their first gender pay gap reports by June 7, 2027, and employers with 100 or more employees must follow by 2031. The directive also sets a 5% threshold for unjustified pay gaps, and if the gap is not corrected within 6 months, the employer must carry out a joint pay assessment with worker representatives. That combination is pushing the pay equity analytics platform market toward audit-grade systems capable of classifying workers, tracking remediation windows, and preserving defensible records across multiple jurisdictions. The same rule set is also expanding the buyer base in the pay equity analytics platform market, as mid-sized employers that were previously outside formal reporting cycles are now moving toward compliance.

U.S. State Pay Transparency Laws Drive A Patchwork Compliance Market

State-level rulemaking is creating a second major demand engine for the pay equity analytics platform market. Colorado continues to enforce its Equal Pay for Equal Work Act and reported USD 841,500 in total citation fines, which shows that noncompliance now carries visible financial consequences rather than only reputational risk. Massachusetts now requires salary range disclosure in defined circumstances, and the law applies to employers with 25 or more employees, which lowers the practical entry point for formal pay transparency controls. For employers operating across remote and distributed teams, the issue is less about one statute and more about coordinating several state-specific posting, recordkeeping, and reporting rules at the same time. That is why the pay equity analytics platform market is benefiting from demand for centralized policy logic, reusable job structures, and standardized disclosure workflows. The patchwork model also favors vendors that can update rule libraries quickly and present state-specific outputs through a single reporting layer.

Compensation Data Privacy Exposure Constrains Enterprise Adoption

Data sensitivity remains one of the clearest brakes on the pay equity analytics platform market. These platforms must process compensation, demographic attributes, performance information, and career histories, which means buyers are often evaluating them against the strictest standards used anywhere in the HR stack. Evenpay positions GDPR-compliant EU data residency and security controls as part of its product value, which shows how closely adoption is tied to privacy expectations in regulated markets. PayAnalytics by beqom also emphasizes pay equity and workforce analytics in a framework built for enterprise use, reflecting how certification and governance have become baseline purchase conditions. In the pay equity analytics platform market, this raises the bar for smaller vendors because buyers want clear evidence of data handling discipline before they will connect payroll and employee records. Privacy rules, therefore, slow some deals even while they make specialized platforms more necessary.

Other drivers and restraints analyzed in the detailed report include:

- Continuous Audits And Board-Level Accountability Reshape Procurement Cycles

- Cloud HR Stack Integration Lowers Deployment Friction

- Fragmented HR Data And Weak Job Architectures Slow Time-To-Value

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-based deployment accounted for 76.18% share of the pay equity analytics platform market size in 2025, and cloud-based deployment is also forecast to expand at an 18.94% CAGR through 2031. In the pay equity analytics platform market, that lead reflects the practical need to connect payroll, HRIS, ATS, and compensation planning data without relying on repeated file transfers. The cloud model also supports multi-country policy changes more efficiently because vendors can update reporting logic across all clients from one governed environment. This matters more as employers face overlapping rules in Europe and North America and need a system that can absorb frequent legal changes without a fresh IT project each time.

On-premises tools still retain a place in some financial institutions, public bodies, and organizations with strict hosting requirements. Even so, the balance of demand in the pay equity analytics platform market is moving toward hosted environments because faster implementation, centralized controls, and stronger integration paths now outweigh earlier cloud hesitations for many buyers. Payscale's integration expansion in early 2025 underscored how the competitive center of gravity has shifted toward connected deployment rather than isolated analysis. The same pattern is visible in enterprise procurement, where buyers increasingly ask whether a platform can plug into existing HCM workflows on day 1. Within the pay equity analytics platform industry, deployment choice is therefore becoming less about infrastructure preference and more about how quickly a client can move from raw data to defensible decisions.

Large enterprises held 66.42% share in 2025, while SMEs are projected to grow at a 20.87% CAGR through 2031. The pay equity analytics platform market still leans toward large employers because they operate across more legal entities, more geographies, and more compensation structures, which increases both reporting complexity and remediation risk. Syndio reported that its platform governs pay for more than 10 million employees across 100 countries and serves nearly 400 global enterprises, including more than 50% of the Fortune 100. That level of adoption shows why enterprise accounts remain the commercial anchor of the pay equity analytics platform market.

The faster growth, however, is moving into smaller employers that are entering formal disclosure and reporting obligations for the first time. In Europe, the reporting threshold of 100 or more employees broadens the addressable buyer pool materially over the forecast period, and in the United States, several state rules already apply to employers of smaller size. Massachusetts, for example, applies salary range requirements to employers with 25 or more employees in covered situations. Ravio's USD 12 million Series A raise in May 2025 was tied to international expansion and reflects investor interest in tools that can serve growing companies rather than only global enterprises. The pay equity analytics platform market is therefore likely to see simpler packaging, faster setup, and more modular pricing as vendors pursue this emerging mid-market demand pool.

Complete Report Scope:

- By Deployment Mode

- Cloud-based

- On-premises

- By Organization Size

- Large Enterprises

- SMEs

- By Application

- Pay Gap Analytics

- Benchmarking and Compensation Analysis

- Compliance and Regulatory Reporting

- Other Applications

- By End-User Industry

- BFSI

- IT and Telecommunications

- Healthcare and Lifesciences

- Retail and E-commerce

- Industrial Manufacturing

- Government and Public Sector

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America held 44.26% of the pay equity analytics platform market share in 2025, giving it the largest regional position. The region benefits from an unusual mix of legal enforceability, employer awareness, and high software readiness, particularly in the United States and Canada. In the United States, the pay equity analytics platform market is supported by a growing web of state-level salary disclosure and reporting obligations that employers must manage across distributed workforces. Colorado's enforcement record shows the seriousness of this environment, with the state reporting USD 841,500 in total citation fines under the Equal Pay for Equal Work Act.

The pay equity analytics platform market in Europe holds the second-largest regional position, but it is going through the deepest regulatory reset. The European Union's pay transparency rules apply across all 27 member states, giving the region an unusually broad compliance footprint across both private and public employment. The June 2026 transposition deadline, followed by staged reporting obligations for employers with 150 or more employees and then 100 or more employees, creates a multi-year implementation cycle rather than a one-time rush. The 5% unjustified gap threshold also raises the operating stakes because unresolved findings can move employers into a joint pay assessment process.

Asia-Pacific is the fastest-growing regional segment in the pay equity analytics platform market, projected to expand at a 22.41% CAGR through 2031. Growth there is being supported by multinational employers that want consistent reporting frameworks across global operations and by local employers that are starting to formalize pay transparency practices. The current pattern remains more reactive than in North America or Western Europe, which means adoption still tends to accelerate when legal obligations become clearer. That gap leaves room for further expansion as regional employers improve their HR data foundations and seek closer integration between payroll and compensation governance. South America, the Middle East, and Africa remain earlier-stage territories for the pay equity analytics platform market, although local reporting expectations are beginning to create openings for vendors that can localize job structures and compliance workflows. PayAnalytics by beqom has already published guidance for South African employers on annual Employment Equity Act reporting and pending transparency requirements, which points to a developing commercial path in the region.

- Syndio Solutions, Inc.

- Trusaic

- Salary.com, LLC

- Payscale, Inc.

- beqom SA

- Performing Ideas HR AB

- Sysarb AB

- PayGap ApS

- Evenpay Oy

- Claritava GmbH

- Opacity ApS

- Figures SAS

- OpenComp, Inc.

- ThinkWhy LLC

- Compport Private Limited

- HRsoft, Inc.

- Ravio Technologies Ltd.

- Parity Software, LLC

- Decusoft

- Compa Technologies, Inc.

- equidi Pty Ltd

- EDGE Strategy AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EU Pay Transparency Directive Implementation Deadline in 2026

- 4.2.2 Expansion of U.S. State Pay Transparency and Pay Data Reporting Laws

- 4.2.3 Shift Toward Continuous Pay Equity Audits and Board-Level Accountability

- 4.2.4 Cloud HR Stack Integration and Workflow Automation

- 4.2.5 Embedding Fair-Pay Guardrails Into Hiring, Promotion, and Merit Decisions

- 4.2.6 Rising Need for Job Architecture and Work-of-Equal-Value Classification

- 4.3 Market Restraints

- 4.3.1 Sensitive Compensation Data Privacy and Security Exposure

- 4.3.2 Weak Job Architecture and Fragmented HR Data

- 4.3.3 Legal Discoverability Risk From Unremediated Audit Findings

- 4.3.4 Salary Benchmarking Data Licensing and Localization Cost Burden

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Cloud-based

- 5.1.2 On-premises

- 5.2 By Organization Size

- 5.2.1 Large Enterprises

- 5.2.2 SMEs

- 5.3 By Application

- 5.3.1 Pay Gap Analytics

- 5.3.2 Benchmarking and Compensation Analysis

- 5.3.3 Compliance and Regulatory Reporting

- 5.3.4 Other Applications

- 5.4 By End-User Industry

- 5.4.1 BFSI

- 5.4.2 IT and Telecommunications

- 5.4.3 Healthcare and Lifesciences

- 5.4.4 Retail and E-commerce

- 5.4.5 Industrial Manufacturing

- 5.4.6 Government and Public Sector

- 5.4.7 Other End-user Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Syndio Solutions, Inc.

- 6.4.2 Trusaic

- 6.4.3 Salary.com, LLC

- 6.4.4 Payscale, Inc.

- 6.4.5 beqom SA

- 6.4.6 Performing Ideas HR AB

- 6.4.7 Sysarb AB

- 6.4.8 PayGap ApS

- 6.4.9 Evenpay Oy

- 6.4.10 Claritava GmbH

- 6.4.11 Opacity ApS

- 6.4.12 Figures SAS

- 6.4.13 OpenComp, Inc.

- 6.4.14 ThinkWhy LLC

- 6.4.15 Compport Private Limited

- 6.4.16 HRsoft, Inc.

- 6.4.17 Ravio Technologies Ltd.

- 6.4.18 Parity Software, LLC

- 6.4.19 Decusoft

- 6.4.20 Compa Technologies, Inc.

- 6.4.21 equidi Pty Ltd

- 6.4.22 EDGE Strategy AG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

人力資源分析市場:按組件、部署模式、組織規模和產業分類-2026-2032年全球市場預測

人力資源分析市場:按組件、部署模式、組織規模和產業分類-2026-2032年全球市場預測 人力資源管理市場規模、佔有率和成長分析:按組件、部署模式、功能、組織規模、最終用戶產業和地區分類-2026-2033年產業預測

人力資源管理市場規模、佔有率和成長分析:按組件、部署模式、功能、組織規模、最終用戶產業和地區分類-2026-2033年產業預測 多元化、股權和包容性 (DEI) 分析平台:市場佔有率分析、行業趨勢和統計數據、成長預測 (2026-2031)人力資源資訊系統(HRIS):市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031)人力資源管理市場:按組件、部署類型、組織規模、應用和產業分類-2026-2032年全球市場預測

多元化、股權和包容性 (DEI) 分析平台:市場佔有率分析、行業趨勢和統計數據、成長預測 (2026-2031)人力資源資訊系統(HRIS):市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031)人力資源管理市場:按組件、部署類型、組織規模、應用和產業分類-2026-2032年全球市場預測 全球人力資源技術市場規模、佔有率、趨勢和成長分析報告(2026-2034)人力資源技術市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測

全球人力資源技術市場規模、佔有率、趨勢和成長分析報告(2026-2034)人力資源技術市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測 勞動力管理系統市場:按應用和區域分類

勞動力管理系統市場:按應用和區域分類 2026年全球薪資核算服務市場報告

2026年全球薪資核算服務市場報告 人力資源管理市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、部署、最終用戶、模組分類

人力資源管理市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、部署、最終用戶、模組分類