|

市場調查報告書

商品編碼

2063727

人力資源資訊系統(HRIS):市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031)Human Resource Information System (HRIS) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

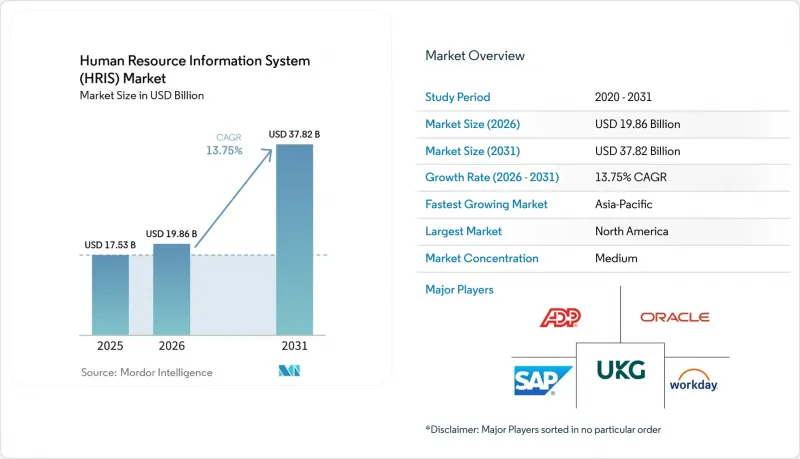

根據 Mordor Intelligence 預測,人力資源資訊系統 (HRIS) 市場將從 2025 年的 175.3 億美元成長到 2026 年的 198.6 億美元,到 2031 年達到 378.2 億美元,2026 年至 2031 年的複合成長率為 13.75%。

本報告按組件(軟體和服務)、部署模式(本地部署和雲端部署)、組織規模(中小企業和大型企業)、最終用戶行業(IT和電信、銀行、金融服務和保險、醫療保健、製造業、零售和電子商務、政府等)以及地區進行細分。市場預測以價值(美元)表示。

全球人力資源資訊系統(HRIS)市場趨勢與洞察

雲端人力資源平台的普及應用日益廣泛

隨著企業將基礎設施所有權外包並實現即時全球資料整合,雲端訂閱正以每年 16.55% 的速度成長,超過了人力資源資訊系統 (HRIS) 市場的整體成長速度。到 2025 年,69% 的雇主將至少遷移一個核心模組到 SaaS(軟體即服務)模式,83% 的雇主預計到 2027 年將全面採用雲端服務。儘管資料中心分佈廣泛,但在政府強制推行電子申報和低成本寬頻環境的推動下,亞太地區 70% 的企業表示計劃在 2026 年前部署人工智慧 (AI) 賦能的人力資源工具。供應商正在積極回應,為中型企業提供捆綁式產品,例如 Workday GO,該產品包含預先建置的工作流程,可將部署時間從九個月縮短到四個月。

對勞動力分析的需求日益成長。

預測離職率、最佳化加班和模擬人事費用的預測儀錶板正從高階附加功能轉變為標準配置。計劃在2026年部署人工智慧驅動的人力資源模組的組織,平均將為分析功能預留160萬美元的預算,比2023年成長十倍。這項成果在醫療產業尤為顯著。一家擁有400張床位的醫院在將排班演算法整合到其人力資源資訊系統(HRIS)後,護理師的加班時間減少了18%。然而,只有9%的雇主具備全公司範圍的人工智慧專業知識,因此低程式碼查詢工具和自然語言介面對於推動人工智慧的普及至關重要。

多租戶雲端中的資料安全和隱私

2024年,因租戶隔離不足而導致的GDPR違規罰款飆升至29.2億歐元(31.1億美元)。亞太地區的資料在地化法律迫使供應商在每個國家/地區建立資料中心,削弱了支撐公共雲端吸引力的規模經濟。單一租戶方案(客戶自行管理加密金鑰)雖然可以降低風險,但可能會使訂閱費用上漲高達50%。

細分市場分析

預計到2031年,業務收益將以16.21%的年均成長率成長,超過人力資源資訊系統(HRIS)市場的整體成長率,這主要得益於買家對整合、變更管理和營運管理專業知識的需求。雖然預計到2025年軟體仍將維持67.12%的最大市場佔有率,但薪資核算引擎的商品化正在將價值轉向分析、人工智慧和更佳的用戶體驗。 ADP在2024年投入12.7億美元研發的現成連接器,將中型企業的部署時間從9個月縮短至4個月,凸顯了買家對速度的重視。在亞太地區,63%的系統所有者實施人力資源技術的經驗不足三年,因此,培訓和支援合約正被納入多年期協議,以保持部署動能。

諮詢預算越來越重視用戶採納而非代碼客製化,這與德勤的研究結果相符——參與度評分最高的25%的公司在變更管理方面的支出比其他公司高出40%。雲端訂閱模糊了傳統的「軟體與服務」界限,因為託管、修補程式和一級支援都包含在月費中。儘管如此,那些需要客製化核准流程或複雜工會規則的公司仍然會購買全面的支援服務,以防止升級後出現故障。

預計2025年至2026年間,雲端實例將成長16.55%,逐步蠶食曾經佔據人力資源資訊系統市場71.05%佔有率的大規模本地部署基礎。中小企業(SME)傾向於選擇訂閱套餐,以消除資本支出(CAPEX)並實現即時合規性更新。跨國公司則更傾向於採用雲端單一實例架構,以便跨境應用通用的職位代碼、薪資等級和評估週期。然而,歐洲銀行管理局(EBA)的外包指南迫使許多歐洲銀行不得不保留本地薪資核算核心系統,並搭配雲端人力資源附加元件,從而形成混合配置,而供應商正逐步停止對此類配置的支援。

本地部署環境的持續存在源自於審計延遲管理和升級時機等挑戰。然而,德勤估計,本地部署人力資源資訊系統 (HRIS) 所需的 IT 人員數量是基於雲端的系統 2.5 倍,而且五年總擁有成本 (TCO) 也明顯傾向於託管方案。因此,許多受監管的採購公司正在協商豁免其遵守主權雲端法規的義務,而不是無限期地繼續使用內部資料中心。

區域分析

2025年,北美地區貢獻了38.02%的收入,這得益於財富500強企業的早期採用以及強大的薪資核算提供者生態系統。目前,成長主要集中在擁有500至2500名員工的中型企業,這些企業傳統上依賴外包薪資核算和電子表格。 Workday GO於2025年11月發布,透過打包標準化工作流程並支援六週內完成部署,滿足了這項需求。從加州的薪資透明度法規到科羅拉多的職位發布要求,日益複雜的合規要求促使用戶需要可配置的規則引擎,而不是硬編碼的邏輯。

亞太地區是成長最快的地區,預計複合年成長率將達到15.34%,到2031年將大幅提升該地區在人力資源資訊系統市場的佔有率。印度就是這項「突破」的典型例證。儘管三分之二的中小企業已做好數位轉型的準備,但絕大多數企業僅限於採購薪資核算和考勤管理系統,這凸顯了供應商進行宣傳活動的必要性。中國強制推行的社保電子申報正迫使製造商遷移到雲端。同時,日本和韓國正謹慎地從本地部署模式過渡到自主雲端模式。澳洲和紐西蘭的市場飽和度與北美類似,但對於能夠保證符合公平工作委員會規定的供應商而言,這兩個市場仍然是重要的成長目標。

歐洲的發展趨勢以GDPR和歐盟人工智慧法律的嚴格執行為特徵。預計2023年至2024年間,罰款金額將增加九倍,迫使企業投資於用戶許可管理儀錶板和演算法邏輯文件。 Workday計畫於2025年11月在法蘭克福和都柏林擴大資料中心,投資金額達1.75億歐元(約1.86億美元),以滿足客戶在歐盟境內儲存資料的需求。西班牙、義大利和希臘等南歐市場仍然較為分散,當地的薪資核算外包商正努力抵禦來自新興雲端參與企業的市場佔有率競爭。南美洲、中東和非洲雖然市佔率較小,但隨著各國政府推動員工登記數位化以及跨國公司實現全球人力資源平台的標準化,這些地區的市場正經歷兩位數的成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 雲端人力資源平台的廣泛應用

- 對勞動力分析和數據驅動決策的需求日益成長

- 勞動力合規相關法規日益複雜

- 遠距和混合辦公室模式的擴展

- 將人工智慧聊天機器人引入員工自助服務

- 產業專用的人力資源資訊系統的興起

- 市場限制因素

- 從舊版人力資源系統遷移成本高昂

- 多租戶架構中的資料安全和隱私問題

- 熟練的人力資源技術經理短缺

- 新興市場中小企業預算有限

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 軟體

- 服務

- 按部署模式

- 現場

- 雲

- 按組織規模

- 中小企業

- 大公司

- 按最終用戶行業分類

- 資訊科技/通訊

- 銀行、金融服務和保險(BFSI)

- 衛生保健

- 製造業

- 零售與電子商務

- 政府

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Workday, Inc.

- SAP SE

- Oracle Corporation

- Automatic Data Processing, Inc.

- UKG Inc.

- Paycom Software, Inc.

- Paychex, Inc.

- Ceridian HCM Holding Inc.

- Cornerstone OnDemand, Inc.

- BambooHR LLC

- Gusto, Inc.

- Zoho Corporation Pvt. Ltd.

- Namely, Inc.

- SumTotal Systems, LLC

- Cegid Group SA

- TriNet Zenefits LLC

- PeopleStrategy, Inc.

- isolved HCM LLC

- Rippling People Center Inc.

- Deputy Group Pty Limited

第7章 市場機會與未來展望

According to Mordor Intelligence, the human resource information system (HRIS) market size is expected to increase from USD 17.53 billion in 2025 to USD 19.86 billion in 2026 and reach USD 37.82 billion by 2031, growing at a CAGR of 13.75% over 2026-2031.

This report is Segmented by Component (Software, and Services), Deployment Model (On-Premise, and Cloud), Organization Size (Small and Medium Enterprises, and Large Enterprises), End-User Industry (IT and Telecom, BFSI, Healthcare, Manufacturing, Retail and E-Commerce, Government, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Human Resource Information System (HRIS) Market Trends and Insights

Growing Adoption of Cloud-Based HR Platforms

Cloud subscriptions are growing 16.55% annually, outpacing overall human resource information system market expansion as organizations offload infrastructure ownership and gain real-time global data consolidation. In 2025, 69% of employers had moved at least one core module to software-as-a-service and 83% expect full cloud adoption by 2027. Asia-Pacific enterprises, despite fragmented data centers, report 70% intent to deploy AI-enabled HR tools by 2026, stimulated by government e-filing mandates and low-cost broadband. Vendors are responding with mid-market bundles such as Workday GO, which ships pre-built workflows that cut launch times from nine months to four.

Rising Demand for Workforce Analytics

Predictive dashboards that forecast attrition, optimize overtime, and model labor costs are shifting from premium add-ons to baseline expectations. Organizations deploying AI-driven HR modules in 2026 budgeted an average of USD 1.6 million for analytics, a tenfold rise since 2023. Healthcare illustrates results: a 400-bed hospital cut nurse overtime by 18% after embedding scheduling algorithms into its HRIS. Yet only 9% of employers possess enterprise-wide AI expertise, making low-code query tools and natural-language interfaces critical adoption levers.

Data Security and Privacy in Multi-Tenant Clouds

GDPR fines surged to EUR 2.92 billion (USD 3.11 billion) in 2024 for breaches linked to inadequate tenant segregation. Asia-Pacific data-localization laws compel vendors to spin up national data centers, diluting the economies of scale that make public clouds attractive. Single-tenant options with customer-managed encryption keys mitigate risk but lift subscription fees by as much as 50%.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Remote and Hybrid Work Models

- Integration of AI-Powered Chatbots for Employee Self-Service

- High Switching Costs From Legacy Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services revenue is projected to rise 16.21% a year through 2031, surpassing overall human resource information system (HRIS) market growth as buyers seek integration, change-management, and managed-perations expertise. Software retained the largest slice 67.12% in 2025, yet commoditization of payroll engines is shifting value toward analytics, AI, and user experience enhancements. Pre-built connectors from ADP, funded by USD 1.27 billion in 2024 research spending, have compressed mid-market rollouts from nine months to four, highlighting the premium buyers place on speed. In Asia-Pacific, where 63% of system owners have fewer than three years of HR-tech experience, training and support contracts are bundled into multiyear deals to sustain adoption momentum.

Consulting budgets increasingly emphasize user adoption rather than code customization, reflecting Deloitte findings that top-quartile engagement scores correlate with 40% higher spend on change management. Cloud subscriptions blur the classic software-versus-services line because hosting, patches, and tier-one support are baked into monthly fees. Nevertheless, enterprises customizing approval chains or complex union work rules still purchase white-glove services to guard against post-upgrade breakage.

Cloud instances grew 16.55% in 2025-2026, chipping away at the sizable on-premise installed base that once held 71.05% of the human resource information system market. Small and medium enterprises gravitate to subscription bundles that eliminate capex and deliver immediate compliance updates. Multinationals favor cloud single-instance architectures to enforce common job codes, compensation bands, and review cycles across borders. The European Banking Authority's outsourcing guidelines, however, push many continental banks to retain on-premise payroll cores paired with cloud talent add-ons, creating hybrid topologies that vendors are starting to de-support.

On-premise persistence stems from audit latency control and upgrade timing. Yet Deloitte pegs IT staffing needs for on-premise HRIS at 2.5 X those of cloud, making total cost of ownership tilt decisively toward hosted options over a five-year horizon. As a result, many regulated buyers are negotiating sovereign-cloud carve-outs rather than sticking indefinitely to in-house data centers.

Geography Analysis

North America secured 38.02% of 2025 revenue thanks to early Fortune 500 adoption and a dense ecosystem of payroll bureaus. Growth now concentrates in mid-market firms of 500-2,500 staff that historically relied on outsourced payroll and spreadsheets. Workday GO, introduced in November 2025, speaks to this gap by bundling standardized workflows into packages that implement in under six weeks. Compliance complexity, from California pay-transparency to Colorado job-posting mandates, nudges buyers toward configurable rule engines rather than hard-coded logic.

Asia-Pacific is the fastest climber, with a projected 15.34% CAGR that will lift its slice of the human resource information system market by 2031. India typifies the leapfrog effect: two-thirds of SMEs show digital readiness, yet the vast majority limit purchases to payroll and attendance, underscoring the need for vendor education. China's electronic social-insurance filing requirement is pulling manufacturers into the cloud, while Japan and South Korea tiptoe away from on-premise toward sovereign-cloud models. Australia and New Zealand exhibit North American-style saturation but remain growth targets for vendors that can guarantee Fair Work Commission compliance.

Europe's trajectory is defined by aggressive enforcement of GDPR and the EU AI Act. Fines ballooned nine-fold between 2023 and 2024, prompting companies to invest in consent-management dashboards and documentation of algorithmic logic. Workday's EUR 175 million (USD 186 million) expansion of Frankfurt and Dublin data centers in November 2025 addresses customers that demand EU-based residency. Southern markets, Spain, Italy, and Greece, remain fragmented, with local payroll outsourcers defending share against cloud newcomers. South America, the Middle East and Africa contribute smaller slices but post double-digit growth as governments digitize labor registries and multinationals standardize global HR platforms.

- Workday, Inc.

- SAP SE

- Oracle Corporation

- Automatic Data Processing, Inc.

- UKG Inc.

- Paycom Software, Inc.

- Paychex, Inc.

- Ceridian HCM Holding Inc.

- Cornerstone OnDemand, Inc.

- BambooHR LLC

- Gusto, Inc.

- Zoho Corporation Pvt. Ltd.

- Namely, Inc.

- SumTotal Systems, LLC

- Cegid Group SA

- TriNet Zenefits LLC

- PeopleStrategy, Inc.

- isolved HCM LLC

- Rippling People Center Inc.

- Deputy Group Pty Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Adoption of Cloud-Based HR Platforms

- 4.2.2 Rising Demand for Workforce Analytics and Data-Driven Decision Making

- 4.2.3 Increasing Regulatory Complexity Around Workforce Compliance

- 4.2.4 Expansion of Remote and Hybrid Work Models

- 4.2.5 Integration of AI-Powered Chatbots for Employee Self-Service

- 4.2.6 Emergence of Industry-Specific HRIS Verticals

- 4.3 Market Restraints

- 4.3.1 High Switching Costs From Legacy HR Systems

- 4.3.2 Data Security and Privacy Concerns in Multi-Tenant Architectures

- 4.3.3 Shortage of Skilled HR Tech Administrators

- 4.3.4 Limited Budgets Among Small Enterprises in Emerging Markets

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Model

- 5.2.1 On-Premise

- 5.2.2 Cloud

- 5.3 By Organization Size

- 5.3.1 Small and Medium Enterprises (SMEs)

- 5.3.2 Large Enterprises

- 5.4 By End-User Industry

- 5.4.1 IT and Telecom

- 5.4.2 Banking, Financial Services and Insurance (BFSI)

- 5.4.3 Healthcare

- 5.4.4 Manufacturing

- 5.4.5 Retail and E-Commerce

- 5.4.6 Government

- 5.4.7 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Workday, Inc.

- 6.4.2 SAP SE

- 6.4.3 Oracle Corporation

- 6.4.4 Automatic Data Processing, Inc.

- 6.4.5 UKG Inc.

- 6.4.6 Paycom Software, Inc.

- 6.4.7 Paychex, Inc.

- 6.4.8 Ceridian HCM Holding Inc.

- 6.4.9 Cornerstone OnDemand, Inc.

- 6.4.10 BambooHR LLC

- 6.4.11 Gusto, Inc.

- 6.4.12 Zoho Corporation Pvt. Ltd.

- 6.4.13 Namely, Inc.

- 6.4.14 SumTotal Systems, LLC

- 6.4.15 Cegid Group SA

- 6.4.16 TriNet Zenefits LLC

- 6.4.17 PeopleStrategy, Inc.

- 6.4.18 isolved HCM LLC

- 6.4.19 Rippling People Center Inc.

- 6.4.20 Deputy Group Pty Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

人力資源分析市場:按組件、部署模式、組織規模和產業分類-2026-2032年全球市場預測

人力資源分析市場:按組件、部署模式、組織規模和產業分類-2026-2032年全球市場預測 薪資不平等分析平台:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

薪資不平等分析平台:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 人力資源管理市場規模、佔有率和成長分析:按組件、部署模式、功能、組織規模、最終用戶產業和地區分類-2026-2033年產業預測多元化、股權和包容性 (DEI) 分析平台:市場佔有率分析、行業趨勢和統計數據、成長預測 (2026-2031)人力資源管理市場:按組件、部署類型、組織規模、應用和產業分類-2026-2032年全球市場預測

人力資源管理市場規模、佔有率和成長分析:按組件、部署模式、功能、組織規模、最終用戶產業和地區分類-2026-2033年產業預測多元化、股權和包容性 (DEI) 分析平台:市場佔有率分析、行業趨勢和統計數據、成長預測 (2026-2031)人力資源管理市場:按組件、部署類型、組織規模、應用和產業分類-2026-2032年全球市場預測 全球人力資源技術市場規模、佔有率、趨勢和成長分析報告(2026-2034)人力資源技術市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測

全球人力資源技術市場規模、佔有率、趨勢和成長分析報告(2026-2034)人力資源技術市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測 勞動力管理系統市場:按應用和區域分類

勞動力管理系統市場:按應用和區域分類 2026年全球薪資核算服務市場報告

2026年全球薪資核算服務市場報告 人力資源管理市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、部署、最終用戶、模組分類

人力資源管理市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、部署、最終用戶、模組分類