|

市場調查報告書

商品編碼

2073301

程序化招募平台:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)Programmatic Job Advertising Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

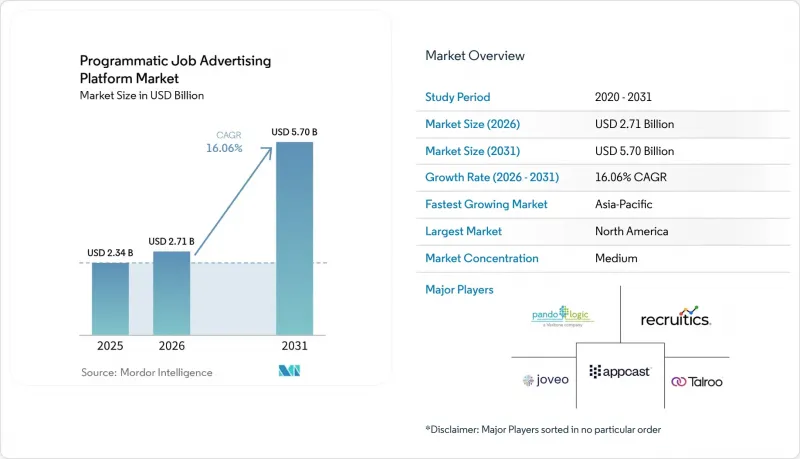

根據 Mordor Intelligence 預測,程式化招募廣告平台市場規模將從 2025 年的 23.4 億美元和 2026 年的 27.1 億美元成長到 2031 年的 57 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 16.06%。

本報告按組件(解決方案和服務)、部署類型(雲端和本地部署)、企業規模(中小企業和大型企業)、行業(IT與電信、銀行、金融服務與保險、零售與電子商務等)以及地區進行細分。市場預測以美元計價。

全球程序化招聘平台市場趨勢與洞察

程序化轉型為以效果為基礎的招募廣告

雇主們正在重新分配預算,轉向那些僅在申請完成後才收費的平台。這種轉變,結合自動化品質追蹤和程序化競標,使得合格候選人的招募成本降低了15%,在某些案例中,招募時間縮短了25%。透過將職位發佈到數千個招聘網站,並減少在低效資訊來源上的支出,負責人現在可以將先前用於手動發布職位資訊的38%的時間用於與候選人互動。

人工智慧驅動的人才招募工作流程的廣泛應用

84%的人才招聘計劃在2026年前部署基於代理的人工智慧,負責人在亞太地區,印度、新加坡和澳洲超過75%的負責人已經採用了人工智慧。整合到程式化平台中的對話機器人現在可以全天候(24/7)以100多種語言篩檢候選人並安排面試,為Radancy的客戶減少了90%以上的人工安排工作。

逐步淘汰第三方 Cookie 對受眾定向準確性的影響

Chrome逐步淘汰第三方Cookie正在削弱行為定向訊號。此外,加州的「自動化決策技術」法規要求對演算法工具進行新的隱私評估,這增加了供應商的合規成本。雖然將第一方ATS數據與伺服器端轉換追蹤相結合的平台可以緩解訊號損失,但缺乏必要工程技術的小規模供應商則面臨利潤率下降的風險。

細分市場分析

截至2025年,服務業佔程序化招聘廣告平台市場的34.67%,但預計到2031年,該市場將以19.03%的複合年成長率成長,屆時將出現向基於效果的宣傳活動管理和隱私諮詢的重大轉變。買家依賴供應商團隊進行ATS映射、分類系統標準化和招募品質分析,以檢驗支出。實施方案通常與變革管理計畫同步進行,旨在重新負責人,使其適應數據驅動的工作流程。託管服務的範圍正在不斷擴大,Appcast和Radancy等公司整合了搜尋、社群媒體和影片面試,為資源有限的人才團隊打造極具吸引力的捆綁式提案。

軟體授權仍將是收入的基礎,但服務正從單純的可選項演變為加速價值實現的關鍵因素。面臨多國管理體制挑戰的公司正依賴供應商專家來在地化授權流程並記錄偏見。因此,儘管軟體利潤率保持穩定,但業務收益預計將在程序化招聘廣告平台市場規模中佔據更大的佔有率。

即使到了2025年,本地部署環境仍將維持58.45%的市場佔有率。這是因為金融服務和醫療保健行業的雇主更傾向於在公司內部管理候選人資料。然而,由於雲端平台具有彈性容量、零停機升級以及與大規模發布商生態系統進行API級連接等優勢,其市場成長速度幾乎是整體市場的三倍。供應商現在對雲端原生版本進行標準化,以確保其用戶群的功能和安全性修補程式的一致性。

混合部署模式也日益普及,敏感的申請人記錄保留在內部伺服器上,而競標最佳化、報告和人工智慧代理則運行在供應商的雲端。加州新的審計追蹤要求使得在軟體即服務 (SaaS) 環境中集中記錄日誌變得更加容易,從而推動風險規避型產業至少部分採用雲端技術。監管壓力與產品創新之間的這種協同作用,在不損害數據主權的前提下,擴大了程序化招聘廣告平台的潛在市場規模。

區域分析

北美地區擁有全球最成熟的ATS生態系統,並率先採用人工智慧驅動的招募行銷,預計2025年該地區的招募收入將佔全球總收入的38.52%。根據美國勞工統計局(BLS)的數據,預計該地區2026年初的失業率將保持在3.8%的低位,儘管金融服務業的招聘活動出現局部放緩,但雇主仍然保持著招聘意願。雖然聯邦政府的裁員導致公共部門的需求下降,但科技和醫療保健產業的招募管道仍然強勁。

亞太地區預計將實現17.43%的複合年成長率,其中印度、新加坡和澳洲負責人的AI採用率超過75%,高於全球平均。由於每個職位發布都會收到大量申請,雇主不得不依賴自動化品質評估來篩選候選人,這使得程序化工具成為負責人工作流程的核心。班加羅爾和雪梨的新創公司正在試行「基於績效」的定價模式,即供應商只有在成功招募後才能獲得報酬,這表明該地區願意積極探索主動型經營模式。

歐洲的發展趨勢受到平衡的監管和對人工智慧的樂觀態度的影響。歐洲央行對5,000家公司的調查顯示,採用人工智慧的公司擴大員工隊伍的可能性高出4個百分點,顯示人工智慧是創造就業機會的補充,而不是取代現有工作。此外,歐洲嚴格的GDPR(一般資料保護規則)框架正引導供應商繼續採用「隱私設計」架構,目前正在向其他地區推廣。南美、中東和非洲等新興市場預計將因行動優先的招聘方式和政府數位化項目而逐步擴大人工智慧的應用,儘管非正式的勞動力結構仍然限制了即時的規模化發展。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 程序化招募廣告向效果導向招募廣告的轉型

- 人工智慧驅動的人才招聘工作流程的廣泛應用

- 專業技能領域人員短缺

- 雇主品牌在所有數位管道中的重要性日益增加

- 整合式全通路宣傳活動管理的興起。

- 擴大與求職網站的第一方資料合作關係,並專注於隱私保護。

- 市場限制因素

- ATS 和程式化平台之間存在持續的資料孤島

- 禁用 Cookie 對受眾定向準確性的影響

- 通貨膨脹導致主要終端用戶產業招聘凍結

- 在高流量招聘網站上,發布商的最低收費標準正在上漲。

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 解決方案

- 服務

- 實施服務

- 託管服務

- 支援和維護服務

- 部署模式

- 基於雲端的

- 現場

- 按公司規模

- 中小企業

- 大公司

- 按行業分類

- 資訊科技/通訊

- 銀行、金融服務和保險(BFSI)

- 衛生保健

- 零售與電子商務

- 製造業

- 其他工業部門

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Appcast, Inc.

- Joveo, Inc.

- PandoLogic, Inc.

- Talroo, Inc.

- Recruitics, LLC

- Symphony Talent, LLC

- SmartDreamers, Inc.

- JobAdX Corporation

- ClickIQ Ltd.

- HireMya, Inc.

- Adway AB

- Radancy, Inc.

- VONQ BV

- Broadbean Technology Limited

- AppVault, LLC

- Joblift GmbH

- Perengo Inc.

- Recooty Technologies Private Limited

- KRT Marketing, Inc.

- Bayard Advertising Agency, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the programmatic job advertising platform market size is projected to expand from USD 2.34 billion in 2025 and USD 2.71 billion in 2026 to USD 5.70 billion by 2031, registering a CAGR of 16.06% between 2026 to 2031.

This report is Segmented by Component (Solution, and Services), Deployment Mode (Cloud-Based, and On-Premise), Enterprise Size (Small and Medium-Sized Enterprises, and Large Enterprises), Industry Vertical (IT and Telecom, Banking, Financial Services and Insurance, Retail and E-Commerce, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Programmatic Job Advertising Platform Market Trends and Insights

Programmatic Shift Toward Performance-Based Recruitment Advertising

Employers are reallocating budgets toward platforms that charge only for completed applications, a change that cut cost-per-qualified-candidate by 15% and reduced time-to-fill by 25% in deployments combining automated quality tracking with programmatic bidding.The ability to distribute vacancies across thousands of boards and halt spend on under-performing sources enables recruiters to redeploy 38% of the time previously spent on manual posting toward candidate engagement.

Growing Adoption of AI-Driven Talent Acquisition Workflows

Eighty-four percent of talent acquisition leaders plan to deploy agentic AI by 2026, with Asia-Pacific showing recruiter AI uptake above 75% in India, Singapore, and Australia. Conversational bots embedded in programmatic platforms now screen and schedule around the clock in more than 100 languages, trimming manual coordination by over 90% for Radancy clients.

Cookie Deprecation Impact on Audience Targeting Accuracy

Chrome's phase-out of third-party cookies is eroding behavioral targeting signals, and California's Automated Decision-Making Technology rules now require fresh privacy assessments for algorithmic tools, raising vendor compliance costs. Platforms that integrate first-party ATS data and server-side conversion tracking are mitigating signal loss but smaller vendors lacking engineering depth risk margin compression.

Other drivers and restraints analyzed in the detailed report include:

- Tight Labor Markets in Specialized Skills Segments

- Rising Importance of Employer Branding Across Digital Channels

- Persistent Data Silos Across ATS and Programmatic Platforms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services represented 34.67% of the Programmatic job advertising platform market in 2025, but their 19.03% CAGR through 2031 signals a decisive pivot toward outcome-linked campaign management and privacy consulting. Buyers lean on vendor teams for ATS mapping, taxonomy harmonization, and quality-of-hire analytics that validate spending. Implementation packages often run parallel with change-management programs that reskill recruiters for data-driven workflows. Managed-service offerings have widened as Appcast and Radancy incorporate search, social, and video interviewing, creating bundled propositions attractive to resource-strained talent teams.

Software licenses will keep anchoring topline revenue, yet services are evolving from optional extras into indispensable accelerators of time-to-value. Enterprises facing multi-country regulatory regimes rely on vendor experts to localize consent flows and bias documentation. As a result, services revenue is poised to contribute a larger slice of the Programmatic job advertising platform market size even while software margins remain stable.

On-premise environments retained a majority 58.45% share in 2025 because financial services and healthcare employers prefer in-house custody of candidate data. However, cloud platforms grew almost triple the overall market thanks to elastic capacity, zero-downtime upgrades, and API-level connections to large publisher ecosystems. Vendors now default to cloud-native releases, ensuring parity of features and security patches across their entire user base.

Hybrid adoption is rising, with sensitive applicant records remaining on internal servers while bid optimization, reporting, and AI agents execute in the vendor cloud. California's new audit-trail obligations make centralized logging easier in software-as-a-service environments, nudging risk-averse sectors toward at least partial cloud usage. This interplay of regulatory pressure and product innovation is widening the total addressable Programmatic job advertising platform market without compromising data sovereignty.

Complete Report Scope:

- By Component

- Solution

- Services

- Implementation Services

- Managed Services

- Support and Maintenance Services

- By Deployment Mode

- Cloud-Based

- On-Premise

- By Enterprise Size

- Small and Medium-Sized Enterprises (SMEs)

- Large Enterprises

- By Industry Vertical

- IT and Telecom

- Banking, Financial Services and Insurance (BFSI)

- Healthcare

- Retail and E-Commerce

- Manufacturing

- Other Industry Verticals

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America generated 38.52% of 2025 revenue, underpinned by the world's most mature ATS ecosystem and early adoption of AI-driven recruitment marketing. BLS figures indicate the region maintained unemployment near a tight 3.8% in early 2026, sustaining employer urgency despite isolated hiring slowdowns in financial services. Federal employment reductions trimmed public-sector demand, yet technology and healthcare hiring pipelines remain resilient.

Asia-Pacific is forecast to post a 17.43% CAGR as India, Singapore, and Australia display recruiter AI adoption rates above 75%, outpacing global benchmarks. High application volumes per posting compel employers to rely on automated quality scoring to sift candidates, making programmatic tools central to recruiter workflow. Startups in Bengaluru and Sydney are piloting outcome-based pricing that pays vendors only for hires, demonstrating the region's willingness to experiment with aggressive commercial models.

Europe's trajectory is shaped by balanced regulation and AI optimism. A European Central Bank survey of 5,000 firms showed AI adopters were 4 percentage points more likely to expand headcount, indicating complementarity with job creation rather than substitution.The continent's stringent GDPR regime continues to steer vendors toward privacy-by-design architectures that are now being exported to other regions. South America, Middle East, and Africa represent emerging corridors where mobile-first hiring and government digitalization programs will gradually lift adoption, though informal labor structures still limit immediate scale.

- Appcast, Inc.

- Joveo, Inc.

- PandoLogic, Inc.

- Talroo, Inc.

- Recruitics, LLC

- Symphony Talent, LLC

- SmartDreamers, Inc.

- JobAdX Corporation

- ClickIQ Ltd.

- HireMya, Inc.

- Adway AB

- Radancy, Inc.

- VONQ B.V.

- Broadbean Technology Limited

- AppVault, LLC

- Joblift GmbH

- Perengo Inc.

- Recooty Technologies Private Limited

- KRT Marketing, Inc.

- Bayard Advertising Agency, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Programmatic Shift Toward Performance-Based Recruitment Advertising

- 4.2.2 Growing Adoption of AI-Driven Talent Acquisition Workflows

- 4.2.3 Tight Labor Markets in Specialized Skills Segments

- 4.2.4 Rising Importance of Employer Branding Across Digital Channels

- 4.2.5 Emergence of Unified Omnichannel Recruitment Campaign Management

- 4.2.6 Proliferation of Privacy-Compliant First-Party Data Partnerships with Job Boards

- 4.3 Market Restraints

- 4.3.1 Persistent Data Silos Across ATS and Programmatic Platforms

- 4.3.2 Cookie Deprecation Impact on Audience Targeting Accuracy

- 4.3.3 Inflation-Driven Hiring Freezes in Key End-Use Industries

- 4.3.4 Escalating Publisher Floor Prices on High-Traffic Job Boards

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solution

- 5.1.2 Services

- 5.1.2.1 Implementation Services

- 5.1.2.2 Managed Services

- 5.1.2.3 Support and Maintenance Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premise

- 5.3 By Enterprise Size

- 5.3.1 Small and Medium-Sized Enterprises (SMEs)

- 5.3.2 Large Enterprises

- 5.4 By Industry Vertical

- 5.4.1 IT and Telecom

- 5.4.2 Banking, Financial Services and Insurance (BFSI)

- 5.4.3 Healthcare

- 5.4.4 Retail and E-Commerce

- 5.4.5 Manufacturing

- 5.4.6 Other Industry Verticals

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Appcast, Inc.

- 6.4.2 Joveo, Inc.

- 6.4.3 PandoLogic, Inc.

- 6.4.4 Talroo, Inc.

- 6.4.5 Recruitics, LLC

- 6.4.6 Symphony Talent, LLC

- 6.4.7 SmartDreamers, Inc.

- 6.4.8 JobAdX Corporation

- 6.4.9 ClickIQ Ltd.

- 6.4.10 HireMya, Inc.

- 6.4.11 Adway AB

- 6.4.12 Radancy, Inc.

- 6.4.13 VONQ B.V.

- 6.4.14 Broadbean Technology Limited

- 6.4.15 AppVault, LLC

- 6.4.16 Joblift GmbH

- 6.4.17 Perengo Inc.

- 6.4.18 Recooty Technologies Private Limited

- 6.4.19 KRT Marketing, Inc.

- 6.4.20 Bayard Advertising Agency, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2026-2030年全球數位化工作指導軟體市場

2026-2030年全球數位化工作指導軟體市場 全球數據壓縮軟體市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球數據壓縮軟體市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 數位 OSS/BSS 市場預測至 2034 年—按組件、部署模式、雲端類型、組織規模、應用程式、最終用戶和地區分類的全球分析數位社群互動解決方案市場預測至2034年-按組件、部署模式、組織規模、技術、應用、最終用戶和地區分類的全球分析

數位 OSS/BSS 市場預測至 2034 年—按組件、部署模式、雲端類型、組織規模、應用程式、最終用戶和地區分類的全球分析數位社群互動解決方案市場預測至2034年-按組件、部署模式、組織規模、技術、應用、最終用戶和地區分類的全球分析 綠色程式碼分析與最佳化軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

綠色程式碼分析與最佳化軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026-2030年全球生產調度軟體市場

2026-2030年全球生產調度軟體市場 2026年全球敏捷物聯網(IoT)市場報告2026年全球職業發展軟體市場報告人工智慧驅動的生產調度市場預測至2034年:按組件、資料來源、安全標準、應用、最終用戶和地區分類的全球分析埃格斯特朗節點市場預測至2034年-按技術、應用、最終用戶和地區分類的全球分析

2026年全球敏捷物聯網(IoT)市場報告2026年全球職業發展軟體市場報告人工智慧驅動的生產調度市場預測至2034年:按組件、資料來源、安全標準、應用、最終用戶和地區分類的全球分析埃格斯特朗節點市場預測至2034年-按技術、應用、最終用戶和地區分類的全球分析