|

市場調查報告書

商品編碼

2073285

北美人工智慧能源管理軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)North America AI-Powered Energy Management Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

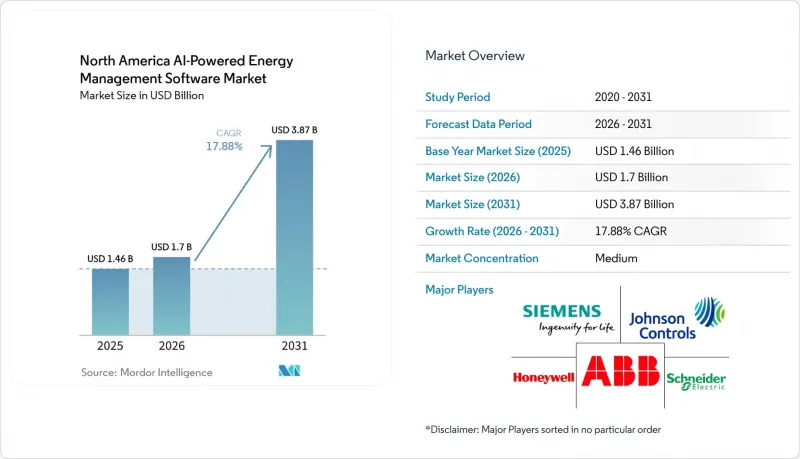

根據 Mordor Intelligence 預測,北美人工智慧能源管理軟體市場規模將從 2025 年的 14.6 億美元和 2026 年的 17 億美元成長到 2031 年的 38.7 億美元,2026 年至 2031 年的複合年成長率為 17.88%。

本報告按元件(軟體和服務)、部署模式(雲端、本地部署、混合部署)、應用(例如,能源消耗和需求最佳化、資產性能和預測性維護)、最終用戶(例如,商業建築、工業設施)和地區進行細分。市場預測以美元計價。

北美人工智慧能源管理軟體市場趨勢與洞察。

智慧電錶和物聯網感測器在商業設施中的迅速普及

儀表和感測器的快速部署正在擴展建築和設施軟體可用的資料庫,使其能夠學習正常運作模式。這對於北美人工智慧驅動的能源管理軟體市場意義重大,因為更高品質的間隔數據使平台更容易從簡單的監控過渡到主動預測和自動回應。在商業設施中,暖通空調控制、逆變器供電和占用訊號正在整合到一個共用的數位層中,從而使跨多個地點的基準測試更加可行。這種轉變減少了每個地點對專用硬體的需求,並為在整個產品組合中採用軟體主導的部署提供了依據。此外,第二波儀器和感測器升級正在改善加密、邊緣處理和設備可靠性,從而支援在運行環境中進行更安全的分析。隨著部署基礎架構的日益統一,北美人工智慧驅動的能源管理軟體市場的供應商更有能力在現有客戶地點擴展正在進行的軟體合約。

提高尖峰負載用戶的電力和需求費用

不斷上漲的電費正將能源最佳化從單純的成本管理工具轉變為能夠直接提升大型設施營運利潤率的工具。需求定價仍然至關重要,因為即使是短暫的尖峰需求也會影響商業和工業用戶的整個月度帳單。從2025年10月到2026年3月,德克薩斯州電力交易所 (ERCOT) 的電力需求年增超過9%。這反映了資料中心的建設、工業電氣化以及電動車充電需求的成長。這種成長給電網帶來了壓力,也提升了能夠轉移負載、自動響應以及更精確地控制電池運作時間的軟體的價值。尚未部署此類工具的設施不僅面臨電費飆升,而且隨著電網營運商採用更動態的收費系統,它們也更容易受到短期價格波動的影響。因此,北美人工智慧驅動的能源管理軟體市場與高負荷州的電價壓力密切相關。

與原有建築管理系統整合的複雜性。

舊有系統的複雜性仍然是一大障礙,因為許多建築仍然使用多種協議和過時的控制器。在北美人工智慧能源管理軟體市場,建築自動化不同層級共用通用資料結構和使用者友善的應用程式介面,阻礙了軟體的普及。許多設施長期以來採用分階段部署BACnet、Modbus和專有控制系統的方式,而不是設計成單一的互聯架構。這迫使軟體供應商在初始分析模型能夠發揮作用之前,必須花費大量時間在中間件、自訂映射和檢驗。中型商業設施受到的影響最大,它們往往缺乏專業的整合技能和人才來證明軟體投資的合理性。這使得軟體的普及成本居高不下,尤其是在北美地區。

細分市場分析

到2025年,軟體將佔據北美人工智慧能源管理軟體市場74.12%的佔有率,供應商的收入來源也將從硬體主導的專案利潤轉向經常性訂閱和授權費。軟體之所以繼續主導北美人工智慧能源管理軟體市場,是因為客戶通常需要快速視覺化、最佳化邏輯和報告功能,而無需大量額外的現場硬體。這種收入結構也為供應商提供了充足的業務擴展空間,包括分析升級、儀表板、預測工具和合規模組。 2026年3月,伊頓公司針對醫療保健、教育和零售業的商業建築推出了Brightlayer Energy。該產品具備即時分析、預測、自動化控制和分散式能源最佳化功能。此類產品的推出表明,軟體供應商正日益將能源最佳化與營運管理和本地合規性相結合。

儘管服務業的絕對規模小規模,但預計從2026年到2031年,其複合年成長率將達到17.93%,略高於整體市場成長率。在北美人工智慧驅動的能源管理軟體市場,基本客群對初始部署後的整合支援、託管分析和模型調優的需求日益成長。許多組織缺乏足夠的能源分析和資料科學專業知識來維護複雜的內部最佳化工具。因此,供應商不僅需要在軟體功能上競爭,還需要在服務的豐富性、部署支援的品質以及持續的效能支援方面展開競爭。

到2025年,基於雲端的部署將佔市場佔有率的63.14%,這反映出簡化部署和減輕基礎設施管理負擔對眾多建築和企業用戶的吸引力。北美人工智慧驅動的能源管理軟體市場正在向雲端轉型,因為擁有多個辦公地點的用戶通常需要集中式報告其所有業務組合,並需要更快的軟體更新。混合部署仍然是成長最快的形式,預計從2026年到2031年將維持18.02%的複合年成長率。這是因為許多受監管的敏感環境希望確保分析能力的擴展,同時又不將控制平面資料完全移出本地安全邊界。因此,對於必須更嚴格地管理其營運系統的公共產業和工業運營商而言,混合架構是一個切實可行的選擇。對於供應商而言,這也有助於他們滿足客戶對即時邊緣決策的需求,同時利用雲端進行更廣泛的分析和監控。

NERC 的要求凸顯了軟體與電網互動時進行周密網路安全設計的必要性。 AWS 和西門子能源於 2026 年 4 月擴大了合作夥伴關係,以支援數位轉型和能源基礎設施解決方案,這體現了領先技術供應商的雲端能力與能源產業營運需求的契合度。在北美人工智慧驅動的能源管理軟體市場,這印證了混合框架將繼續發揮核心作用的觀點,因為公共產業和大型企業需要在規模、延遲和合規性之間取得平衡。雖然純粹的本地部署模式在更嚴格的環境中仍然很重要,但在預測期內,其成長可能會落後於更靈活的架構。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 智慧電錶和物聯網感測器在商業設施中的迅速普及

- 提高尖峰負載用戶的電費和需求費用

- 企業和校園為實現投資組合脫碳所採取的舉措

- 分散式能源和電池的整合

- 人工智慧故障檢測技術可減少因設備漂移未被發現而造成的能源浪費。

- 為鼓勵電力公司參與自動需量反應,政府推出了新的獎勵

- 市場限制因素

- 與傳統建築管理系統整合的複雜性

- 互聯能源資料的網路安全與資料管治問題

- 企業銷售週期延長以及解決方案檢驗的要求。

- 中端市場終端用戶缺乏熟練的設施分析師。

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 軟體

- 服務

- 部署模式

- 基於雲端的

- 現場

- 混合

- 透過使用

- 最佳化能源消耗和需求

- 資產性能和預測性維護

- 智慧電網和分散式能源(DER)管理

- 可再生能源預測與整合

- 能源交易、定價和市場訊息

- 最終用戶

- 公用事業

- 商業建築

- 工業設施

- 住宅大樓

- 按地區

- 美國

- 加拿大

- 墨西哥

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Schneider Electric SE

- Siemens AG

- Johnson Controls International plc

- Honeywell International Inc.

- ABB Ltd.

- IBM Corporation

- Oracle Corporation

- Cisco Systems, Inc.

- Enel X North America, Inc.

- Delta Electronics, Inc.

- SAP SE

- Eaton Corporation plc

- Carrier Global Corporation

- Trane Technologies plc

- GridPoint, Inc.

- AutoGrid Systems, Inc

- EnergyHub

- Acuity Brands, Inc.

- AutoGrid Systems, Inc.

- Amperon

第7章 市場機會與未來展望

According to Mordor Intelligence, the north america AI-Powered energy management software market size is projected to expand from USD 1.46 billion in 2025 and USD 1.70 billion in 2026 to USD 3.87 billion by 2031, registering a CAGR of 17.88% between 2026 and 2031.

This report is Segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Application (Energy Consumption and Demand Optimization, Asset Performance and Predictive Maintenance, and More), End User (Commercial Buildings, Industrial Facilities, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America AI-Powered Energy Management Software Market Trends and Insights

Rapid Smart Meter and IoT Sensor Penetration Across Commercial Sites

Rapid meter and sensor adoption is expanding the database that building and facility software can use to learn normal operating patterns. In the North America AI-Powered Energy Management Software Market, this matters because better interval data helps platforms move from simple monitoring to active prediction and automated response. Commercial sites are also bringing HVAC controls, inverter feeds, and occupancy signals onto shared digital layers, which makes multi-site benchmarking more practical. That shift reduces the need for proprietary hardware in every location and improves the case for software-led rollouts across portfolios. Second-wave metering and sensor upgrades are also improving encryption, edge processing, and device reliability, which supports more secure analytics use in operating environments. As that installed base becomes more consistent, vendors in the North America AI-Powered Energy Management Software Market are better positioned to scale recurring software contracts across existing customer sites.

Rising Utility Tariffs and Demand Charges for Peak Load Customers

Rising electricity tariffs are turning energy optimization from a cost-control tool into a direct operating-margin tool for large facilities. Demand charges remain especially important because a short peak event can shape the full monthly bill for commercial and industrial users. Electricity demand in ERCOT grew by more than 9% year over year from October 2025 through March 2026, reflecting data center construction, industrial electrification, and growth in electric vehicle charging. That increase tightened grid conditions and strengthened the value of software that can shift load, automate response, and time battery dispatch more accurately. Facilities without these tools are facing not only higher bills but also greater exposure to short-term price swings as grid operators use more dynamic pricing structures. This is keeping the North America AI-Powered Energy Management Software Market closely tied to tariff pressure in high-load states.

Integration Complexity with Legacy Building Management Systems

Legacy system complexity remains a major barrier because many buildings still operate with mixed protocols and older controllers. In the North America AI-Powered Energy Management Software Market, this slows deployment when building automation layers do not share a common data structure or an easy application interface. Many sites carry years of BACnet, Modbus, and proprietary controls that were installed in stages rather than designed as one connected architecture. That forces software vendors to spend more time on middleware, custom mapping, and validation before the first analytic model can deliver value. Mid-sized commercial properties are affected the most because they are large enough to justify software investment but often lack specialist integration and staff. This keeps deployment costs elevated and makes the North

Other drivers and restraints analyzed in the detailed report include:

- Portfolio Decarbonization Commitments from Enterprises and Campuses

- Integration With Distributed Energy Resources and Battery Storage

- Cybersecurity and Data Governance Concerns for Connected Energy Data

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software held 74.12% of the North America AI-Powered Energy Management Software market share in 2025, keeping vendor revenue centered on recurring subscriptions and licensing rather than hardware-led project margins. The North America AI-Powered Energy Management Software Market continues to favor software because customers typically want fast visibility, optimization logic, and reporting without adding significant new field hardware. That revenue profile also gives vendors more room to expand into analytics upgrades, dashboards, forecasting tools, and compliance modules over time. Eaton launched Brightlayer Energy in March 2026 for commercial buildings in healthcare, education, and retail, with functions for real-time analysis, forecasting, automated control, and distributed energy optimization. Product launches like this show how software vendors are tying energy optimization more closely to operational management and local compliance support

Services are smaller in absolute terms, but they are projected to grow at a 17.93% CAGR from 2026 to 2031, slightly ahead of the overall market pace. In the North America AI-Powered Energy Management Software Market, the customer base increasingly needs integration support, managed analytics, and model tuning after initial deployment. Many organizations lack sufficient internal energy analytics or data science staff to maintain complex in-house optimization tools. This is pushing providers to compete on service depth, onboarding quality, and ongoing performance support as much as on software features.

Cloud-based deployment accounted for 63.14% of the market in 2025, reflecting the appeal of simpler rollout and lower infrastructure management for many building and enterprise users. The North America AI-Powered Energy Management Software Market has shifted toward the cloud because multi-site users often need centralized reporting and faster software updates across portfolios. Hybrid deployment is still the fastest-growing mode with an 18.02% CAGR from 2026 to 2031, because many regulated or sensitive environments want analytics scale without fully moving control-plane data outside the local security boundary. That makes hybrid architecture a practical fit for utilities and industrial operators that must keep tighter control over operational systems. It also helps vendors serve customers who want real-time edge decisions on-site while still using cloud layers for broader analytics and oversight.

NERC requirements reinforce the need for careful cyber design when software interfaces with the bulk electric system. AWS and Siemens Energy expanded their collaboration in April 2026 to support digital transformation and energy infrastructure solutions, reflecting how major technology providers are aligning cloud capabilities with the energy sector's operating needs. In the North America AI-Powered Energy Management Software Market, this supports the view that hybrid frameworks will remain central while utilities and large enterprises balance scale, latency, and compliance. Pure on-premises models will remain relevant in more stringent environments, but their relative growth is likely to lag that of more flexible architectures over the forecast period.

Complete Report Scope:

- By Component

- Software

- Services

- By Deployment Mode

- Cloud-Based

- On-Premises

- Hybrid

- By Application

- Energy Consumption and Demand Optimization

- Asset Performance and Predictive Maintenance

- Smart Grid and Distributed Energy Resource (DER) Management

- Renewable Energy Forecasting and Integration

- Energy Trading, Pricing and Market Intelligence

- By End User

- Utilities

- Commercial Buildings

- Industrial Facilities

- Residential Buildings

- By Geography

- United States

- Canada

- Mexico

List of Companies Covered in this Report:

- Schneider Electric SE

- Siemens AG

- Johnson Controls International plc

- Honeywell International Inc.

- ABB Ltd.

- IBM Corporation

- Oracle Corporation

- Cisco Systems, Inc.

- Enel X North America, Inc.

- Delta Electronics, Inc.

- SAP SE

- Eaton Corporation plc

- Carrier Global Corporation

- Trane Technologies plc

- GridPoint, Inc.

- AutoGrid Systems, Inc

- EnergyHub

- Acuity Brands, Inc.

- AutoGrid Systems, Inc.

- Amperon

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Smart Meter And IoT Sensor Penetration Across Commercial Sites

- 4.2.2 Rising Utility Tariffs And Demand Charges For Peak Load Customers

- 4.2.3 Portfolio Decarbonization Commitments From Enterprises And Campuses

- 4.2.4 Integration With Distributed Energy Resources And Battery Storage

- 4.2.5 AI-Enabled Fault Detection Reducing Energy Waste From Hidden Equipment Drift

- 4.2.6 New Utility Incentives For Automated Demand Response Participation

- 4.3 Market Restraints

- 4.3.1 Integration Complexity With Legacy Building Management Systems

- 4.3.2 Cybersecurity And Data Governance Concerns For Connected Energy Data

- 4.3.3 Long Enterprise Sales Cycles And Solution Validation Requirements

- 4.3.4 Skilled Facility-Analytics Talent Shortage At Mid-Market End Users

- 4.4 Impact of Macroeconomic Factors on The Market

- 4.5 Industry Value-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Application

- 5.3.1 Energy Consumption and Demand Optimization

- 5.3.2 Asset Performance and Predictive Maintenance

- 5.3.3 Smart Grid and Distributed Energy Resource (DER) Management

- 5.3.4 Renewable Energy Forecasting and Integration

- 5.3.5 Energy Trading, Pricing and Market Intelligence

- 5.4 By End User

- 5.4.1 Utilities

- 5.4.2 Commercial Buildings

- 5.4.3 Industrial Facilities

- 5.4.4 Residential Buildings

- 5.5 By Geography

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Schneider Electric SE

- 6.4.2 Siemens AG

- 6.4.3 Johnson Controls International plc

- 6.4.4 Honeywell International Inc.

- 6.4.5 ABB Ltd.

- 6.4.6 IBM Corporation

- 6.4.7 Oracle Corporation

- 6.4.8 Cisco Systems, Inc.

- 6.4.9 Enel X North America, Inc.

- 6.4.10 Delta Electronics, Inc.

- 6.4.11 SAP SE

- 6.4.12 Eaton Corporation plc

- 6.4.13 Carrier Global Corporation

- 6.4.14 Trane Technologies plc

- 6.4.15 GridPoint, Inc.

- 6.4.16 AutoGrid Systems, Inc

- 6.4.17 EnergyHub

- 6.4.18 Acuity Brands, Inc.

- 6.4.19 AutoGrid Systems, Inc.

- 6.4.20 Amperon

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2026-2030年全球環境情報市場

2026-2030年全球環境情報市場 歐洲人工智慧能源管理軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)非洲人工智慧能源管理軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

歐洲人工智慧能源管理軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)非洲人工智慧能源管理軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 2026-2030年全球人工智慧能源效率工具市場

2026-2030年全球人工智慧能源效率工具市場 能源管理自動化系統市場預測至2034年—按系統類型、組件、技術、應用、最終用戶和地區分類的全球分析

能源管理自動化系統市場預測至2034年—按系統類型、組件、技術、應用、最終用戶和地區分類的全球分析 2026年全球核能人工智慧(AI)市場報告

2026年全球核能人工智慧(AI)市場報告 人工智慧在能源領域的市場規模、佔有率和趨勢分析報告:按類型、應用、地區和細分市場分類(2026-2033 年)熱電網人工智慧管理市場預測至2034年——全球解決方案類型、組件、部署模式、技術、應用、最終用戶和區域分析2026年全球能源分配人工智慧(AI)市場報告2026年全球能源領域人工智慧市場報告

人工智慧在能源領域的市場規模、佔有率和趨勢分析報告:按類型、應用、地區和細分市場分類(2026-2033 年)熱電網人工智慧管理市場預測至2034年——全球解決方案類型、組件、部署模式、技術、應用、最終用戶和區域分析2026年全球能源分配人工智慧(AI)市場報告2026年全球能源領域人工智慧市場報告