|

市場調查報告書

商品編碼

2073283

非洲人工智慧能源管理軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Africa AI-Powered Energy Management Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

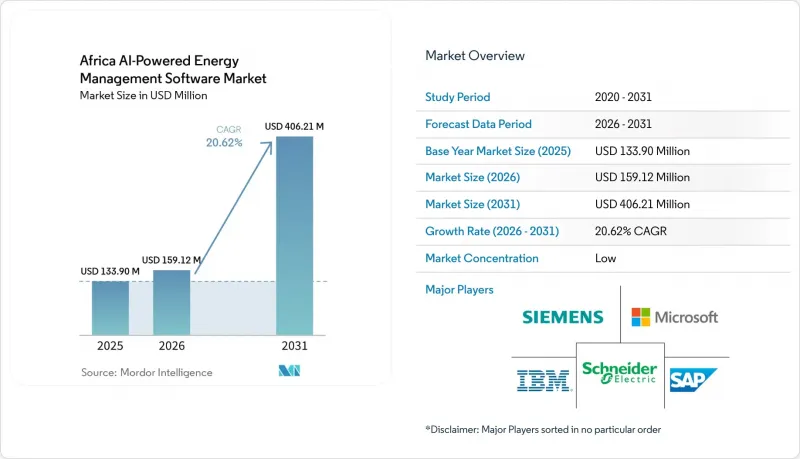

根據 Mordor Intelligence 預測,非洲人工智慧能源管理軟體的市場規模預計將在 2025 年達到 1.339 億美元,並在 2026 年至 2031 年以 20.62% 的複合年成長率成長,到 2031 年達到 4.0621 億美元。

本報告按組件(軟體和服務)、部署模式(雲端等)、應用(能源消耗和需求最佳化、資產性能和預測性維護、可再生能源預測和整合等)、最終用戶(商業建築等)以及地區進行細分。市場預測以美元計價。

非洲人工智慧能源管理軟體市場趨勢與洞察

商業和工業設施對即時能源最佳化的需求日益成長。

非洲人工智慧能源管理軟體市場的商業和工業用戶正面臨持續的能源成本問題,這些問題無法透過人工監控解決。在南非,不斷上漲的價格和反覆出現的供應不穩定促使許多營運商採用人工智慧驅動的需量反應和負載轉移工具,以降低尖峰時段用電量並緩解價格波動風險。 2026年4月,Honeywell在拉各斯的丹格特煉油廠部署了其Forge Performance+平台,展示了即時數位化效能管理在非洲最大工業場所之一的實際應用。 2026年6月在奈及利亞的部署表明,將人工智慧驅動的負載管理與太陽能和電池儲能相結合,可以將製造業的電力成本降低70%,從而增強了更廣泛應用該技術的商業性合理性。隨著價格壓力和供應不穩定性的加劇,投資回收期正在縮短,加速了人工智慧能源管理軟體在非洲市場的普及。

人工智慧與智慧電網和分散式能源的整合

非洲對人工智慧驅動的能源管理軟體的需求正日益成長,這得益於電力公司為提升整個電網的可視性而開展的現代化改造項目。長期以來,非洲電網的數位化程度一直較低。落基山研究所 (Rocky Mountain Institute) 於 2025 年 10 月發布報告稱,許多非洲電力公司仍然主要運行模擬系統,導致對客戶需求概況和資產位置的了解有限。這為採用基於人工智慧的情境察覺和編配工具提供了絕佳的機會。 GE Vernova 和 Larsen & Toubro 已與肯亞輸電公司 (KETRACO) 國家系統控制中心簽訂契約,將在該國的輸電環境中部署 GridOS 先進能源管理系統和廣域監控功能。在西非,GE Vernova 的軟體也為西非電力聯營體 (WAPP) 的電網運作、穩定性監控和市場管理提供支持,該聯營體涵蓋西非國家經濟共同體 (ECOWAS) 的 14 個成員國。隨著分散式能源資源接近落基山研究所確定的 5% 至 15% 的尖峰時段分配閾值,人工智慧軟體正不再只是可選的數位升級,而是成為輸配電基礎運作不可或缺的一部分。

與傳統OT和IT系統整合的複雜性

非洲人工智慧能源管理軟體市場面臨的主要障礙之一是難以將人工智慧軟體與過時的操作技術(OT) 和控制環境連接起來,這些環境並非為資料豐富的自動化而設計。截至 2025 年 3 月,該地區許多工業能源部署仍在使用過時的 SCADA 和自動化系統,這些系統與雲端原生平台相容性差,導致採購和引進週期延長。 IT 和 OT 之間的管治差距加劇了這個問題,因為不同的團隊往往基於不同的營運假設來處理保護、運作和安全性等優先事項。 《巨量資料雜誌》2025 年的一篇綜述指出,傳統基礎設施和脆弱的數位資料架構是能源系統採用人工智慧的主要障礙,在資產更新周期長的非洲營運環境中,這項挑戰尤為突出。因此,非洲人工智慧能源管理軟體市場的短期部署主要集中在大型電力公司和工業集團,這些公司有能力在不中斷日常營運的情況下投資整合工作。

細分市場分析

2025年,軟體銷售額佔總銷售額的68.41%,在非洲人工智慧能源管理軟體市場佔最大佔有率。買家最初青睞軟體,是因為它允許他們在進行更廣泛的轉型工作之前,將分析、視覺化和最佳化工具疊加到現有系統上。這一趨勢在南非、埃及和奈及利亞最為顯著,這些國家的早期採用者希望在無需承擔全部整合負擔的情況下,快速實現監控和控制。軟體也符合許多電力公司和工業設施的早期採購階段,在這些階段,能源使用情況和運作異常的可見性比詳細的諮詢支援更為重要。這種對早期採用的重視意味著平台授權和訂閱仍然是非洲人工智慧能源管理軟體市場支出的核心。

預計到2031年,服務業將以23.34%的複合年成長率成長,成為非洲人工智慧能源管理軟體市場中成長最快的細分領域。這是因為許多使用者即使在初始軟體部署運作後,仍然需要長期支持,包括配置、培訓、系統調優和分析管理。能夠將可衡量的能源成本節約與定價掛鉤的供應商,正受到尋求持續營運支援而非一次性部署的客戶的青睞。Schneider Electric在非洲區域推廣的「EcoStruxure Energy Intelligence」正是這種轉變的體現,該公司正從產品主導合約轉向與人工智慧整合的循環軟體和服務模式。從長遠來看,這些服務可能會對純粹的軟體公司構成壓力,因為業務範圍更廣的現有企業可以將分析、部署和長期最佳化打包成單一的商業方案。

到2025年,基於雲端的部署將佔據66.29%的市場佔有率,成為非洲人工智慧能源管理軟體市場的主導交付模式。雲端系統之所以受到買家青睞,是因為它們降低了初始基礎設施成本,並簡化了分佈在廣大地理區域的資產的設置、監控和更新。此外,它們還滿足了企業尋求更快部署以及對多個建築物、變電站和營運場所進行集中式視覺化管理的需求。對於許多商業用戶而言,基於雲端的平台提供了一個便捷的人工智慧能源管理入口,無需進行大規模的現場運算投資。因此,雲端技術在非洲人工智慧能源管理軟體市場中取得了顯著的早期領先優勢。

混合部署預計將以22.77%的複合年成長率成長至2031年,這反映出在關鍵營運中將雲端分析與本地控制相結合的需求。電力公司、礦場和大規模工業設施越來越需要現場響應能力,因為它們無法總是等待穩定的網路連接或往返雲端處理時間來進行即時決策。這種需求在2025年的採礦業尤為突出,屆時基於邊緣的AI解決方案將部署在電力和通訊環境惡劣的偏遠地區。 PotisEdge在尚比亞的微電網專案也顯示了現場營運管理能力的重要性,因為需要持續平衡太陽能、電池和柴油發電系統。因此,能夠透過單一介面管理邊緣和雲端環境的供應商正在非洲的AI能源管理軟體市場中佔據更有利的地位。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 商業和工業設施對即時能源最佳化的需求日益成長。

- 人工智慧與智慧電網和分散式能源的整合

- 擴展ESG報表和碳核算工作流程

- 引進邊緣人工智慧進行站點級故障偵測與控制

- 由於建築物老化和工業基礎設施老化,維修需求增加。

- 採礦和重工業的電氣化和負載平衡需求

- 市場限制因素

- 與傳統OT和IT系統整合難度很高。

- 與數據品質、互通性和感測器碎片化相關的挑戰。

- 對關鍵能源資產的網路安全和數據主權問題的擔憂

- 中小型網站投資回報前景存在不確定性。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 軟體

- 服務

- 部署模式

- 基於雲端的

- 現場

- 混合

- 透過使用

- 最佳化能源消耗和需求

- 資產性能和預測性維護

- 智慧電網和分散式能源(DER)管理

- 可再生能源預測與整合

- 能源交易、定價和市場訊息

- 最終用戶

- 公用事業

- 商業建築

- 工業設施

- 住宅大樓

- 按地區

- 南非

- 埃及

- 其他非洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Siemens AG

- Schneider Electric SE

- ABB Ltd.

- Honeywell International Inc.

- IBM Corporation

- Johnson Controls International plc

- General Electric Company

- Eaton Corporation plc

- Emerson Electric Co.

- Oracle Corporation

- Microsoft Corporation

- Amazon Web Services, Inc.

- SAP SE

- C3.ai, Inc.

- Bidgely, Inc.

- Grid4C Ltd.

- Innowatts, Inc.

- Enel X Srl

- GridPoint, Inc.

- Dexma Sensors, SL

第7章 市場機會與未來展望

According to Mordor Intelligence, the africa AI-Powered energy management software market size was USD 133.90 million in 2025 and is forecast to reach USD 406.21 million by 2031 at 20.62% CAGR from 2026 to 2031.

This report is Segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, and More), Application (Energy Consumption and Demand Optimization, Asset Performance and Predictive Maintenance, Renewable Energy Forecasting and Integration, and More), End User (Commercial Buildings, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Africa AI-Powered Energy Management Software Market Trends and Insights

Rising Need for Real-Time Energy Optimization in Commercial and Industrial Facilities

Commercial and industrial users across the Africa AI-Powered Energy Management Software Market are dealing with a sustained energy cost problem that manual monitoring cannot solve. In South Africa, rising tariffs and recurring supply instability have pushed many operators toward AI-enabled demand response and load-shifting tools to reduce peak consumption and lower exposure to volatile pricing. Honeywell deployed its Forge Performance+ platform at the Dangote Petroleum Refinery in Lagos in April 2026, demonstrating that real-time digital performance management is now in use at one of the continent's largest industrial sites. A June 2026 deployment in Nigeria also showed that AI-driven load management tied to solar and battery storage could reduce manufacturing power costs by 70%, which strengthened the commercial case for broader adoption. As tariff pressure and supply unreliability rise together, payback periods are shortening, and procurement is moving faster across the Africa AI-Powered Energy Management Software Market.

AI Integration With Smart Grids and Distributed Energy Resources

The Africa AI-Powered Energy Management Software Market is also gaining support from utility modernization programs that need better visibility across grids that were long operated with limited digital intelligence. Rocky Mountain Institute reported in October 2025 that many African utilities were still running largely analog systems with limited visibility into customer demand profiles and asset locations, leaving a clear opening for AI-based situational awareness and orchestration tools. GE Vernova, Larsen, and Toubro secured the KETRACO National System Control Center contract in Kenya, bringing GridOS Advanced Energy Management Systems and wide area monitoring capabilities into the national transmission environment. In West Africa, GE Vernova software is also supporting dispatch, stability monitoring, and market operations for the West African Power Pool across 14 ECOWAS member countries. As distributed energy resources approach the 5% to 15% distribution peak threshold noted by RMI, AI software is becoming part of basic grid operations rather than a discretionary digital upgrade.

High Integration Complexity With Legacy OT and IT Systems

A major brake on the Africa AI-Powered Energy Management Software Market is the difficulty of connecting AI software to older operational technology and control environments that were never designed for data-rich automation. In March 2025, many industrial energy deployments in the region still used outdated SCADA and automation systems poorly aligned with cloud-native platforms, thereby extending procurement and implementation cycles. The governance gap between IT and OT compounds the problem because different teams with distinct operating assumptions often handle protection, uptime, and safety priorities. A 2025 review in the Journal of Big Data identified legacy infrastructure and a weak digital data architecture as leading barriers to AI deployment in energy systems, and this challenge is especially evident in African operating environments with long asset replacement cycles. These conditions keep near-term adoption concentrated among larger utilities and industrial groups that can fund integration work without disrupting day-to-day operations in the Africa AI-Powered Energy Management Software Market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of ESG Reporting and Carbon Accounting Workflows

- Edge AI Adoption for Site-Level Fault Detection and Control

- Data Quality, Interoperability, and Sensor Fragmentation Issues

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 68.41% of component revenue in 2025, giving it the largest position in the Africa AI-Powered Energy Management Software Market. Buyers initially favored software because analytics, visualization, and optimization tools could be layered onto existing systems before committing to broader transformation work. This pattern was strongest in South Africa, Egypt, and Nigeria, where early adopters sought fast gains in monitoring and control without taking on the full burden of integration. Software also matched the first stage of procurement in many utilities and industrial facilities, where visibility into energy use and operational anomalies mattered more than deep consulting support. That early weighting kept platform licenses and subscriptions at the center of spending in the Africa AI-Powered Energy Management Software Market.

Services are projected to grow at a 23.34% CAGR through 2031, making them the fastest-expanding component of the Africa AI-Powered Energy Management Software Market. The reason is practical, because many users need help with configuration, training, system tuning, and managed analytics long after the first software deployment goes live. Vendors that can link fees to measurable energy cost reduction are gaining traction with customers who want ongoing operational support rather than a one-time installation. Schneider Electric's regional push toward EcoStruxure Energy Intelligence also reflects this shift, as the company is moving from product-led contracts toward AI-linked recurring software and service models. Over time, those services may put pressure on pure software specialists, because broader incumbents can bundle analytics, implementation, and long-term optimization into a single commercial offer.

Cloud-based deployment held a 66.29% share in 2025, making it the leading delivery model across the Africa AI-Powered Energy Management Software Market. Cloud systems appealed to buyers because they lowered upfront infrastructure costs and made it easier to configure, monitor, and update distributed assets across wide geographic footprints. They also fit the needs of organizations that wanted faster deployment and centralized visibility across multiple buildings, substations, or operating sites. For many commercial users, cloud-based platforms provided an accessible entry point into AI-based energy management without requiring large on-site computing investments. This gave cloud deployment a strong early lead in the Africa AI-Powered Energy Management Software Market.

Hybrid deployment is forecast to expand at a 22.77% CAGR through 2031, reflecting the need to combine cloud analytics with local control for critical operations. Utilities, mines, and large industrial sites increasingly need on-site response capacity because real-time decisions cannot always wait for stable connectivity or round-trip cloud processing. Mining deployments highlighted this need in 2025, as edge-based AI solutions were being deployed to remote sites with challenging power and communications conditions. PotisEdge's Zambia microgrid project also showed that local dispatch intelligence is becoming central, as solar, battery, and diesel systems must be continuously balanced. Vendors that can manage both edge and cloud environments through one interface are therefore gaining a stronger position in the Africa AI-Powered Energy Management Software Market.

Complete Report Scope:

- By Component

- Software

- Services

- By Deployment Mode

- Cloud-Based

- On-Premises

- Hybrid

- By Application

- Energy Consumption and Demand Optimization

- Asset Performance and Predictive Maintenance

- Smart Grid and Distributed Energy Resource (DER) Management

- Renewable Energy Forecasting and Integration

- Energy Trading, Pricing and Market Intelligence

- By End User

- Utilities

- Commercial Buildings

- Industrial Facilities

- Residential Buildings

- By Geography

- South Africa

- Egypt

- Rest of Africa

List of Companies Covered in this Report:

- Siemens AG

- Schneider Electric SE

- ABB Ltd.

- Honeywell International Inc.

- IBM Corporation

- Johnson Controls International plc

- General Electric Company

- Eaton Corporation plc

- Emerson Electric Co.

- Oracle Corporation

- Microsoft Corporation

- Amazon Web Services, Inc.

- SAP SE

- C3.ai, Inc.

- Bidgely, Inc.

- Grid4C Ltd.

- Innowatts, Inc.

- Enel X S.r.l.

- GridPoint, Inc.

- Dexma Sensors, S.L.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Need for Real-Time Energy Optimization in Commercial and Industrial Facilities

- 4.2.2 AI Integration With Smart Grids and Distributed Energy Resources

- 4.2.3 Expansion of ESG Reporting and Carbon Accounting Workflows

- 4.2.4 Edge AI Adoption for Site-Level Fault Detection and Control

- 4.2.5 Retrofit Demand From Aging Building and Industrial Infrastructure

- 4.2.6 Electrification and Load Flexibility Needs Across Mining and Heavy Industry

- 4.3 Market Restraints

- 4.3.1 High Integration Complexity With Legacy OT and IT Systems

- 4.3.2 Data Quality, Interoperability, and Sensor Fragmentation Issues

- 4.3.3 Cybersecurity and Data Sovereignty Concerns for Critical Energy Assets

- 4.3.4 Limited Payback Visibility in Small and Mid-Sized Sites

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Application

- 5.3.1 Energy Consumption and Demand Optimization

- 5.3.2 Asset Performance and Predictive Maintenance

- 5.3.3 Smart Grid and Distributed Energy Resource (DER) Management

- 5.3.4 Renewable Energy Forecasting and Integration

- 5.3.5 Energy Trading, Pricing and Market Intelligence

- 5.4 By End User

- 5.4.1 Utilities

- 5.4.2 Commercial Buildings

- 5.4.3 Industrial Facilities

- 5.4.4 Residential Buildings

- 5.5 By Geography

- 5.5.1 South Africa

- 5.5.2 Egypt

- 5.5.3 Rest of Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Siemens AG

- 6.4.2 Schneider Electric SE

- 6.4.3 ABB Ltd.

- 6.4.4 Honeywell International Inc.

- 6.4.5 IBM Corporation

- 6.4.6 Johnson Controls International plc

- 6.4.7 General Electric Company

- 6.4.8 Eaton Corporation plc

- 6.4.9 Emerson Electric Co.

- 6.4.10 Oracle Corporation

- 6.4.11 Microsoft Corporation

- 6.4.12 Amazon Web Services, Inc.

- 6.4.13 SAP SE

- 6.4.14 C3.ai, Inc.

- 6.4.15 Bidgely, Inc.

- 6.4.16 Grid4C Ltd.

- 6.4.17 Innowatts, Inc.

- 6.4.18 Enel X S.r.l.

- 6.4.19 GridPoint, Inc.

- 6.4.20 Dexma Sensors, S.L.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2026-2030年全球環境情報市場

2026-2030年全球環境情報市場 北美人工智慧能源管理軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲人工智慧能源管理軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

北美人工智慧能源管理軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲人工智慧能源管理軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 2026-2030年全球人工智慧能源效率工具市場

2026-2030年全球人工智慧能源效率工具市場 能源管理自動化系統市場預測至2034年—按系統類型、組件、技術、應用、最終用戶和地區分類的全球分析

能源管理自動化系統市場預測至2034年—按系統類型、組件、技術、應用、最終用戶和地區分類的全球分析 2026年全球核能人工智慧(AI)市場報告

2026年全球核能人工智慧(AI)市場報告 人工智慧在能源領域的市場規模、佔有率和趨勢分析報告:按類型、應用、地區和細分市場分類(2026-2033 年)熱電網人工智慧管理市場預測至2034年——全球解決方案類型、組件、部署模式、技術、應用、最終用戶和區域分析2026年全球能源分配人工智慧(AI)市場報告2026年全球能源領域人工智慧市場報告

人工智慧在能源領域的市場規模、佔有率和趨勢分析報告:按類型、應用、地區和細分市場分類(2026-2033 年)熱電網人工智慧管理市場預測至2034年——全球解決方案類型、組件、部署模式、技術、應用、最終用戶和區域分析2026年全球能源分配人工智慧(AI)市場報告2026年全球能源領域人工智慧市場報告