|

市場調查報告書

商品編碼

2073264

人力資源領域的生成式人工智慧:市場佔有率分析、產業趨勢與統計數據以及成長預測(2026-2031 年)Generative AI In HR - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

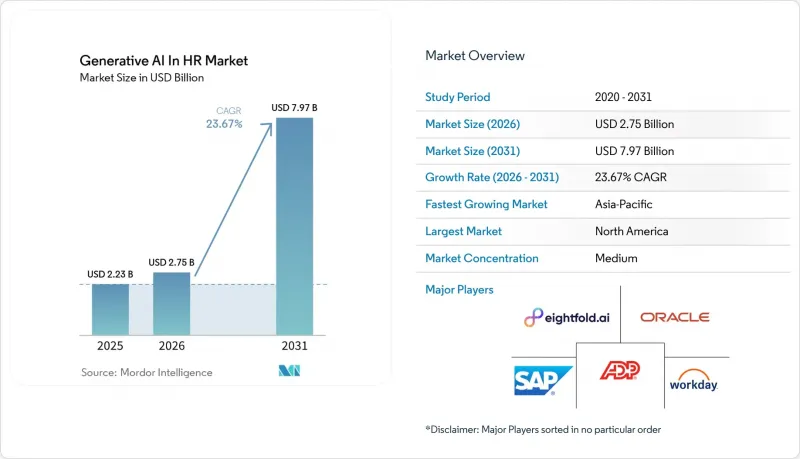

據 Mordor Intelligence 稱,人力資源領域生成式人工智慧的市場規模預計將從 2025 年的 22.3 億美元成長到 2026 年的 27.5 億美元,到 2031 年達到 79.7 億美元,預計 2026 年至 2031 年的複合年成長率為 23.67%。

本報告按部署模式(雲端、本地部署、混合部署)、人力資源職能(招聘與獲取、學習與發展、員工敬業度與體驗、績效管理等)、組織規模(大型企業等)、最終用戶行業(IT和電信、銀行、金融服務和保險等)以及地區進行細分。市場預測以美元計價。

人力資源領域生成式人工智慧的全球趨勢與洞察

企業級SaaS中大規模語言模式的快速發展

隨著雇主對可解釋性、可審計性和特定領域準確性的需求日益成長,領域特定的基礎模型正在取代通用聊天機器人。 Workday Illuminate 能夠攝取超過 8000 億個業務交易資料點,從而實現自動化職位說明生成、人才概覽和繼任計劃,同時在整個人力資源和財務環境中保持流程上下文的一致性。 2026 年 2 月,微軟與 IBM 合作,將 WatsonX 的管治控制與 Copilot 的協作層相結合,從而能夠在不將個人資料暴露於公共訓練循環的情況下,以保密方式部署人力資源代理,用於福利諮詢和入職流程。像 Wisq 這樣的專業供應商正在發布專有的人力資源語言模型,這些模型內建了符合美國平等就業機會委員會 (EEOC) 和通用資料保護規範 (GDPR) 框架的偏見檢查功能,彌合了模型功能與監管預期之間的差距。隨著這些模型的成熟,即使在以前僅限於低風險任務的規避風險行業中,人力資源領域的生成式人工智慧市場也正在獲得認可。

大規模人才招聘流程自動化面臨的壓力日益增大。

儘管現場工作人員和小時工在全球勞動力招聘中佔據相當大的比例,但這一流程的潛力仍遠未充分挖掘。 ICIMS 的「Frontline AI」可透過簡訊、WhatsApp 和線上聊天全天候與求職者溝通,將招募時間縮短高達 75%,並將每位招募人員的招募效率提高十倍。 Paradox 的「Olivia」助理可處理大規模面試安排和預先篩檢。同時,Eightfold AI 的結構化視訊面試系統可將文件建立時間縮短 90%,並符合紐約市第 144 號地區法案的新審計要求。這些效率提升正促使雇主加強投資,推動生成式人工智慧在人力資源領域成為曾經依賴人工的招募流程的核心。

人們對與勞動力相關的AI模型中的資料隱私和偏見表示擔憂。

演算法偏見、隱私洩漏和不透明的決策邏輯可能會給雇主帶來巨額罰款的風險。歐盟人工智慧法規定,實施違禁系統的企業最高可被處以3,500萬歐元(3,960萬美元)或全球營業額7%的罰款,但只有18%的企業認為已為2026年8月的最後期限做好了充分準備。紐約市第144號地區法案已強制要求對自動化招聘工具進行偏見審計,並要求供應商公佈審計結果並通知候選人。同時,ISO 42001提供了一套自願性的管治藍圖。合規方面的複雜性阻礙了人力資源領域,特別是績效評估和晉升選拔中高風險應用情境的推廣。

細分市場分析

隨著雇主對將雲端推理的敏捷性與本地個人資料管理相結合的柔軟性,混合部署預計將以 26.77% 的複合年成長率 (CAGR) 成長。儘管如此,到 2025 年,雲端服務仍將佔據人力資源領域生成式人工智慧 (AI) 市場 64.29% 的佔有率,因為訂閱式定價、快速發布週期和供應商管理的安全保障更受中型企業買家的青睞。在中國和中東地區營運且受到嚴格本地化要求約束的跨國公司,目前正在試點主權雲端區域和敏感運算飛地,以避免資料回流的風險,將敏感記錄保留在本地,同時將匿名化的元資料傳送到雲端引擎。領先的超大規模資料中心業者正在透過提供適用於 Workday、SAP SuccessFactors 和 Oracle HCM 的專用人力資源連接器來應對這項挑戰,使客戶能夠在不遷移核心資料的情況下利用生成式 AI 功能。這種共存模式正在加速生成式 AI 在人力資源領域滲透到具有嚴格合規要求的產業,同時維持現有的稽核控制。

在國防、情報和關鍵基礎設施領域,本地部署仍然十分普遍。然而,隨著供應商不斷證明其雲端平台擁有主權認證,並能與傳統的空氣間隙相媲美,本地部署的整體佔有率持續下降。 ADP 和 SAP 的全球薪資核算系統整合正是這一轉變的標誌。如今,企業無需從根本上改變現有的人力資源系統,即可在 140 個國家/地區整合薪資核算異常檢測、報告和員工自助服務功能。這種 API 優先的擴展方式降低了遷移風險,並將混合模式確立為人力資源領域生成式人工智慧市場的預設營運模式。

人力資源分析和人才規劃預計將以25.85%的複合年成長率實現最高成長,這表明其關注點正從與招聘相關的交易指標轉向預測性技能預測、情境建模和組織設計。儘管到2025年,招聘相關解決方案仍將佔據人力資源領域生成式人工智慧市場規模的28.45%,但隨著聊天機器人和日程安排工具的功能日益趨同,買家正將目光轉向下游,尋求更高的附加價值。 Workday Illuminate等平台能夠擷取企業特定的流程數據,產生關於入職瓶頸、繼任候選人名單和薪酬洞察的報告。同時,學習系統利用生成式引擎產生客製化的微課程,進而減少對外部內容庫的投入。

員工敬業度套件融合了情緒分析和人工智慧生成的行動計劃,使管理者能夠即時應對員工倦怠的徵兆,從而提升了生成式人工智慧在人力資源領域人力資本策略中的市場滲透率。儘管出於法律責任的考慮,績效管理仍需謹慎對待,但可解釋的人工智慧儀錶板和「人機協作」核准流程正逐漸獲得經營團隊的支持。

區域分析

由於雄厚的創業投資、人力資源技術供應商的集中以及歷來較為寬鬆的法規環境,預計到2025年,北美將在人力資源領域的生成式人工智慧市場中佔據35.27%的佔有率。隨著監管日益碎片化——例如加州的《消費者隱私法案》(CCPA)、紐約州的第144號地方法律以及即將訂定的聯邦指南——選擇標準正轉向那些擁有便捷合規儀表板的平台。如今,大西洋兩岸的雇主都將監管彈性和功能範圍放在首位,這使得具備整合審計報告功能的供應商擁有了競爭優勢。

預計到2031年,亞太地區的複合年成長率將達到26.20%,位居全球之首。中國的國家人工智慧戰略要求進行大規模技能再培訓和勞動力分析,推動國營企業採用可擴展的、支援中文的模型。印度領先的IT服務公司正在利用生成式代理實現海外招聘流程自動化、降低離職率並實現學習路徑個性化;而日本正在試點人工智慧驅動的繼任計劃,以應對人口老齡化問題。澳洲和紐西蘭正在效仿歐盟的透明度規則來建立其系統,使該地區成為一個“沙盒”,供應商可以在此展示其合規準備情況,然後再進軍歐洲市場。

歐洲、中東和非洲的發展動能並不均衡。歐洲雇主正面臨歐盟人工智慧法律下繁瑣的程序,由於必須與員工代表委員會協商並進行適用性評估,採購週期被延長,這暫時減緩了人力資源領域生成式人工智慧市場的成長。 Littler 2025年的一項調查顯示,只有18%的雇主為2026年8月的最後期限做好了準備,凸顯了短期瓶頸問題。在中東,尤其是在阿拉伯聯合大公國和沙烏地阿拉伯,主權財富基金正在投資人工智慧驅動的人才在地化計畫。同時,非洲的需求集中在針對低頻寬最佳化的行動優先聊天機器人。在南美洲,以巴西和阿根廷為首,對話式人工智慧正被應用於零售和農業等大規模招聘領域的招募活動中,但由於宏觀經濟波動,多年轉型預算仍然有限。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 企業級SaaS中大規模語言模式的快速發展

- 大規模人才招聘流程自動化面臨的壓力日益增大。

- 擴大對話式人工智慧在員工自助服務環境中的應用。

- 將基於技能的勞動力規劃架構納入主流

- 將 GenAI 與低程式碼 HR 技術堆疊整合

- 雇主對高度個人化學習內容的需求日益成長

- 市場限制因素

- 人們對與勞動力相關的AI模型中的資料隱私和偏見表示擔憂。

- 難以獲得高品質的人力資源培訓數據。

- 微調生成式人工智慧模型的總擁有成本不斷上升

- 人工智慧生成內容相關的智慧財產權問題不透明

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 按部署模式

- 雲

- 現場

- 混合

- 按人力資源職能

- 招募和人才獲取

- 學習與技能發展

- 員工敬業度與體驗

- 績效管理

- 人力資源分析與勞動規劃

- 其他人力資源職能

- 按組織規模

- 大公司

- 小型企業

- 產業最終用途

- 資訊科技/通訊

- BFSI

- 醫療保健和生命科學

- 製造業

- 零售與電子商務

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- ADP, Inc.

- Workday, Inc.

- Oracle Corporation

- SAP SE

- International Business Machines Corporation

- Microsoft Corporation

- Google LLC

- Eightfold AI, Inc.

- Phenom People, Inc.

- Paradox.ai, Inc.

- Beamery Ltd.

- HireVue, Inc.

- iCIMS, Inc.

- Greenhouse Software, Inc.

- Lever, Inc.

- Textio, Inc.

- Gloat, Inc.

- Retrain.ai Ltd.

- SeekOut Inc.

- Lattice, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the generative AI in HR market size is expected to increase from USD 2.23 billion in 2025 to USD 2.75 billion in 2026 and reach USD 7.97 billion by 2031, growing at a CAGR of 23.67% over 2026-2031.

This report is Segmented by Deployment Model (Cloud, On-Premises, and Hybrid), HR Function (Recruitment and Talent Acquisition, Learning and Development, Employee Engagement and Experience, Performance Management, and More), Organization Size (Large Enterprises, and More), End-Use Industry (IT and Telecom, BFSI, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Generative AI In HR Market Trends and Insights

Rapid Advancement of Large Language Models in Enterprise SaaS

Domain-tuned foundation models are overtaking generic chatbots as employers require explainability, auditability and domain-specific accuracy. Workday Illuminate ingests more than 800 billion business transactions to automate job description creation, talent summarization and succession planning, while preserving process context across HR and finance environments. Microsoft joined forces with IBM in February 2026 to pair watsonx governance controls with the Copilot collaboration layer, enabling confidential deployment of HR agents for benefits queries and onboarding without exposing personal data to public training loops. Specialist vendors such as Wisq are launching proprietary HR language models that embed bias checks aligned to EEOC and GDPR frameworks, closing the gap between model capability and regulatory expectation. As these models mature, the generative AI in HR market gains credibility among risk-averse sectors that previously limited pilots to low-stakes tasks.

Rising Pressure to Automate High-Volume Talent Acquisition Tasks

Frontline and hourly hiring remains largely undigitized even though it represents a majority of global headcount. ICIMS Frontline AI now engages applicants around the clock across SMS, WhatsApp and web chat, reducing time-to-fill by up to 75% and allowing tenfold more hires per recruiter.Paradox's Olivia assistant schedules interviews and conducts pre-screens at scale, while Eightfold AI's structured video interviewer compresses documentation time by 90% to satisfy emerging audit mandates under NYC Local Law 144. These efficiency gains fuel employer willingness to invest, propelling the generative AI in HR market into core hiring workflows once dominated by manual labor.

Data Privacy and Bias Concerns in Workforce-Related AI Models

Algorithmic bias, privacy lapses and opaque decision logic expose employers to hefty penalties. The EU AI Act imposes fines of up to EUR 35 million (USD 39.6 million) or 7% of global turnover for deploying prohibited systems, yet only 18% of organizations feel very prepared for the August 2026 deadline. NYC Local Law 144 already requires bias audits for automated hiring tools, forcing vendors to publish audit results and notify candidates, while ISO 42001 offers an optional governance blueprint. Compliance complexity is delaying high-risk use cases in the generative AI in HR market, particularly performance evaluation and promotion selection.

Other drivers and restraints analyzed in the detailed report include:

- Growing Adoption of Conversational AI for Employee Self-Service

- Mainstreaming of Skills-Based Workforce Planning Frameworks

- Limited Availability of HR-Specific High-Quality Training Data

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid deployments are forecast to expand at a 26.77% CAGR as employers seek the agility of cloud inference paired with on-premises control of personal data. Cloud services nonetheless retained 64.29% of the 2025 generative AI in HR market share because subscription pricing, rapid release cycles and vendor-managed security appeal to mid-market buyers. Multinationals operating under strict localization mandates in China or the Middle East now pilot sovereign-cloud regions and confidential-computing enclaves to avoid repatriation risk, keeping sensitive records on-premises while sending de-identified metadata to cloud engines. Major hyperscalers have responded with dedicated HR connectors for Workday, SAP SuccessFactors and Oracle HCM that let customers unlock generative features without moving core data. This coexistence model preserves existing audit controls yet accelerates the generative AI in HR market penetration among compliance-heavy industries.

On-premises installations persist in defense, intelligence and critical-infrastructure environments, but their overall share continues to slide as vendors document equivalence between sovereign-cloud certifications and traditional air-gaps. ADP's global payroll integration with SAP exemplifies the shift: firms can now orchestrate payroll anomaly detection, reporting and employee self-service across 140 countries without uprooting incumbent HR stacks.Such API-first extensions lower migration risk and reinforce hybrid as the default operating model within the generative AI in HR market.

HR analytics and workforce planning is projected to grow at the fastest 25.85% CAGR, signaling a pivot from transactional hiring metrics toward predictive skills forecasting, scenario modeling and organizational design. Recruitment still commanded 28.45% of the 2025 generative AI in HR market size, but feature parity in chatbots and scheduling tools is pushing buyers to look further downstream for incremental value. Platforms such as Workday Illuminate generate onboarding bottleneck reports, succession shortlists and compensation insights by ingesting enterprise-specific process data. Meanwhile learning systems leverage generative engines to produce customized micro-lessons, reducing spend on external content libraries.

Employee engagement suites embed sentiment analysis and AI-generated action plans so managers can respond to burnout signals in real time, raising stickiness of the generative AI in HR market within human capital strategies. Performance management remains a cautious frontier due to liability worries, but explainable AI dashboards and human-in-the-loop approvals are gradually winning executive sponsorship.

Complete Report Scope:

- By Deployment Model

- Cloud

- On-premises

- Hybrid

- By HR Function

- Recruitment and Talent Acquisition

- Learning and Development

- Employee Engagement and Experience

- Performance Management

- HR Analytics and Workforce Planning

- Other HR Functions

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises

- By End-use Industry

- IT and Telecom

- BFSI

- Healthcare and Life Sciences

- Manufacturing

- Retail and E-commerce

- Other End-use Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- North America

Geography Analysis

North America maintained 35.27% share of the generative AI in HR market in 2025, buoyed by venture capital depth, concentration of HR tech vendors and a historically permissive regulatory climate. Rising patchwork rules, California CCPA, New York Local Law 144 and forthcoming federal guidelines, are shifting selection criteria toward platforms with turnkey compliance dashboards. Employers operating on both sides of the Atlantic now rate regulatory agility as high as feature scope, giving advantage to vendors with embedded audit reporting.

Asia-Pacific is anticipated to post the fastest 26.20% CAGR through 2031. China's national AI strategy mandates large-scale reskilling and workforce analytics, driving adoption of Mandarin-trained models that can scale across state-owned enterprises. India's IT services giants use generative agents to automate offshore recruitment workflows, cut attrition and personalize learning paths, while Japan pilots AI-driven succession planning to hedge against population aging. Australia and New Zealand model EU-style transparency rules, turning the region into a sandbox where vendors prove compliance readiness before European rollouts.

Europe, the Middle East and Africa display uneven momentum. European employers face procedural complexity under the EU AI Act, mandatory works-council consultation and conformity assessments lengthen buying cycles, temporarily tempering the generative AI in HR market expansion. Littler's 2025 survey revealed only 18% readiness for the August 2026 deadline, spotlighting a short-term bottleneck.The Middle East channels sovereign wealth into AI workforce nationalization programs, particularly in the UAE and Saudi Arabia, while African demand centers on mobile-first chatbots optimised for low bandwidth. South America, led by Brazil and Argentina, applies conversational AI to high-volume retail and agriculture hiring, though macroeconomic volatility still limits multi-year transformation budgets.

- ADP, Inc.

- Workday, Inc.

- Oracle Corporation

- SAP SE

- International Business Machines Corporation

- Microsoft Corporation

- Google LLC

- Eightfold AI, Inc.

- Phenom People, Inc.

- Paradox.ai, Inc.

- Beamery Ltd.

- HireVue, Inc.

- iCIMS, Inc.

- Greenhouse Software, Inc.

- Lever, Inc.

- Textio, Inc.

- Gloat, Inc.

- Retrain.ai Ltd.

- SeekOut Inc.

- Lattice, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Advancement of Large Language Models in Enterprise SaaS

- 4.2.2 Rising Pressure to Automate High-Volume Talent Acquisition Tasks

- 4.2.3 Growing Adoption of Conversational AI for Employee Self-Service

- 4.2.4 Mainstreaming of Skills-Based Workforce Planning Frameworks

- 4.2.5 Integration of GenAI with Low-Code HR Tech Stacks

- 4.2.6 Increasing Employer Demand for Hyper-Personalized Learning Content

- 4.3 Market Restraints

- 4.3.1 Data Privacy and Bias Concerns in Workforce-Related AI Models

- 4.3.2 Limited Availability of HR-Specific High-Quality Training Data

- 4.3.3 Rising Total Cost of Ownership for GenAI Model Fine-Tuning

- 4.3.4 Uncertain Intellectual Property Rights Around AI-Generated Content

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products or Services

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 Cloud

- 5.1.2 On-premises

- 5.1.3 Hybrid

- 5.2 By HR Function

- 5.2.1 Recruitment and Talent Acquisition

- 5.2.2 Learning and Development

- 5.2.3 Employee Engagement and Experience

- 5.2.4 Performance Management

- 5.2.5 HR Analytics and Workforce Planning

- 5.2.6 Other HR Functions

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By End-use Industry

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Manufacturing

- 5.4.5 Retail and E-commerce

- 5.4.6 Other End-use Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ADP, Inc.

- 6.4.2 Workday, Inc.

- 6.4.3 Oracle Corporation

- 6.4.4 SAP SE

- 6.4.5 International Business Machines Corporation

- 6.4.6 Microsoft Corporation

- 6.4.7 Google LLC

- 6.4.8 Eightfold AI, Inc.

- 6.4.9 Phenom People, Inc.

- 6.4.10 Paradox.ai, Inc.

- 6.4.11 Beamery Ltd.

- 6.4.12 HireVue, Inc.

- 6.4.13 iCIMS, Inc.

- 6.4.14 Greenhouse Software, Inc.

- 6.4.15 Lever, Inc.

- 6.4.16 Textio, Inc.

- 6.4.17 Gloat, Inc.

- 6.4.18 Retrain.ai Ltd.

- 6.4.19 SeekOut Inc.

- 6.4.20 Lattice, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

生成式人工智慧晶片組市場:全球產業分析、市場規模、市場佔有率及2026年至2033年預測(按晶片組類型、應用、最終用途、國家和地區分類)

生成式人工智慧晶片組市場:全球產業分析、市場規模、市場佔有率及2026年至2033年預測(按晶片組類型、應用、最終用途、國家和地區分類) 人力資源領域生成式人工智慧市場規模、佔有率和成長分析:按應用、部署、組織規模、最終用戶產業和地區分類-2026-2033年產業預測

人力資源領域生成式人工智慧市場規模、佔有率和成長分析:按應用、部署、組織規模、最終用戶產業和地區分類-2026-2033年產業預測 旅遊業生成式人工智慧市場規模、佔有率和成長分析:按應用、部署、技術、最終用戶和地區分類-2026-2033年產業預測

旅遊業生成式人工智慧市場規模、佔有率和成長分析:按應用、部署、技術、最終用戶和地區分類-2026-2033年產業預測 生成式人工智慧:市場佔有率分析、產業趨勢和統計數據、成長預測(2026-2031 年)

生成式人工智慧:市場佔有率分析、產業趨勢和統計數據、成長預測(2026-2031 年) 採購領域生成式人工智慧市場規模、佔有率和成長分析:按解決方案類型、應用、部署模式、企業規模、最終用戶產業、銷售管道和地區分類-2026-2033年產業預測

採購領域生成式人工智慧市場規模、佔有率和成長分析:按解決方案類型、應用、部署模式、企業規模、最終用戶產業、銷售管道和地區分類-2026-2033年產業預測 生成式人工智慧市場預測至2034年—按組件、模式、應用、最終用戶和地區分類的全球分析

生成式人工智慧市場預測至2034年—按組件、模式、應用、最終用戶和地區分類的全球分析 生成式人工智慧市場規模、佔有率和趨勢分析報告:按組件、技術、最終用途、應用、模型、客戶、地區和細分市場預測(2026-2033 年)

生成式人工智慧市場規模、佔有率和趨勢分析報告:按組件、技術、最終用途、應用、模型、客戶、地區和細分市場預測(2026-2033 年) 生成式人工智慧市場:按組件、類型、部署模式、應用和產業分類-2026-2032年全球市場預測

生成式人工智慧市場:按組件、類型、部署模式、應用和產業分類-2026-2032年全球市場預測 生成式人工智慧市場:依技術、實現類型、應用、地區分類

生成式人工智慧市場:依技術、實現類型、應用、地區分類 2026年全球房地產生成式人工智慧市場報告

2026年全球房地產生成式人工智慧市場報告