|

市場調查報告書

商品編碼

2073226

歐洲昆蟲飼料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Europe Insect Feed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

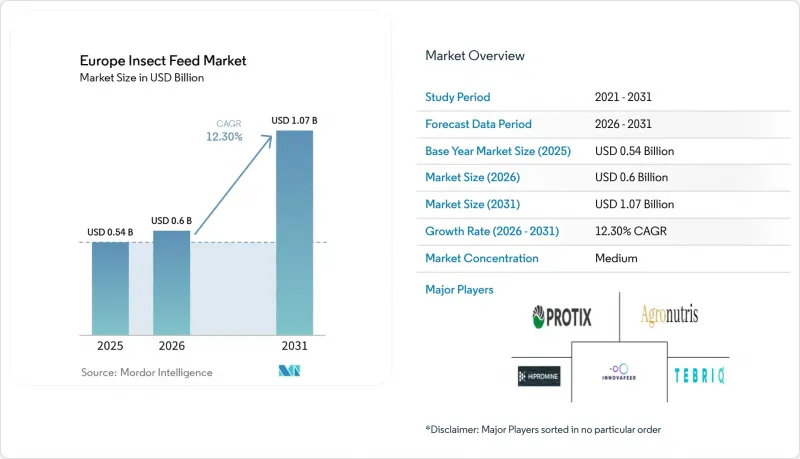

據 Mordor Intelligence 稱,歐洲昆蟲飼料市場預計將在 2025 年達到 5.4 億美元,從 2026 年的 6 億美元成長到 2031 年的 10.7 億美元,在預測期(2026-2031 年)內實現 12.3% 的複合年成長率。

本報告按昆蟲種類(黑水虻、穀蟲、家蠅等)、產品形態(蛋白粉、乾幼蟲、昆蟲油和糞肥)、動物種類(水產養殖、家禽、豬等)、最終用戶(商業飼料廠等)和地區(德國、法國等)進行細分。市場預測以美元計價。

歐洲昆蟲飼料市場的趨勢與洞察

擴大歐盟飼料核准範圍將增加對昆蟲蛋白質的潛在需求。

過去幾年,歐盟飼料法規的逐步改善直接惠及了歐洲昆蟲飼料市場。歐盟2017/893號法規首次允許在水產養殖飼料中使用昆蟲源動物蛋白,2021年的修訂案將此許可範圍擴大至豬和家禽,顯著拓寬了可商業化使用的牲畜種類。 2024年的法規澄清也確認了活昆蟲可用作豬、家禽和水產養殖飼料的原料。這為小規模企業提供了一種比生產完整的動物性蛋白質(PAP)成本更低的加工途徑。每項授權都擴大了水產養殖、家禽、豬和寵物食品行業的生產商基本客群,使工業化規模的擴張更具商業性可行性。歐洲昆蟲飼料市場也將受益於2025年國際食品和飼料昆蟲平台(IPIFF)良好衛生指南的正式採納。這將提高可追溯性,並減輕首次涉足該領域的飼料生產商的採購擔憂。儘管由於反芻動物仍被排除在外,成長受到限制,但單胃動物和水產養殖業已然成為歐洲昆蟲飼料市場短期內規模化發展最明確的途徑。

水產養殖飼料中需要魚粉和魚油的替代品。

由於魚粉供應緊張而水產飼料需要持續成長,水產養殖業仍然是歐洲昆蟲飼料市場需求最強勁的支柱之一。預計到2023年,歐盟海鮮自給率將降至38.1%,而歐盟大部分飼料蛋白依賴進口,因此,人們對供應的穩定性和永續性日益擔憂。針對虹鱒、大西洋鮭、歐洲鱸魚和加州石首魚等魚類的研究表明,透過適當的配方控制,昆蟲粉可以取代相當一部分魚粉,且不會影響魚類的生長、消化率或產品品質。挪威是一個特別重要的市場,因為昆蟲來源的成分不僅被視為重要的蛋白質替代品,而且鑑於鮭魚飼料飼料相關排放量較高,昆蟲來源的排放也被視為減少現有飼料系統碳排放的一種手段。因此,歐洲昆蟲飼料市場正從水產養殖業的性能檢驗和政策壓力中獲得支持。未來幾年,隨著產業團體推動水產養殖飼料的正式配方目標,這兩個因素的結合將變得越來越重要。

需求仍然集中在高階應用領域。

需求集中是限制歐洲昆蟲飼料市場發展的主要阻礙因素之一。事實上,昆蟲飼料應用最廣泛的領域並非家禽和生豬飼料,而是水產幼畜飼料、鮭魚飼料、高階寵物食品以及其他高附加價值領域。儘管家禽和生豬飼料合計佔歐洲飼料總量的絕大部分,但這些應用領域對價格競爭力的要求遠高於目前大豆粕競爭方面。社會經濟研究也表明,即使規模顯著擴大,主流經濟狀況仍然充滿挑戰,這意味著昆蟲飼料的廣泛應用很可能是一個漸進的過程,而非快速發展。這種需求集中至關重要,因為高階市場極易受到配方調整和品牌定位變化的影響。因此,歐洲昆蟲飼料市場要從選擇性應用走向真正的大眾市場滲透,持續降低成本和提升產業信譽至關重要。

細分市場分析

到2025年,黑水虻幼蟲將佔據歐洲昆蟲飼料市場49.5%的佔有率,這主要得益於其擴充性、營養優勢和加工柔軟性。這些幼蟲因其飼料轉換率高、富含可利用的蛋白質和脂肪,以及與工業產品特定採購模式的兼容性而備受青睞。因此,黑水虻幼蟲已成為歐洲昆蟲飼料市場大規模商業化的主要平台。研究進一步證實了這一趨勢,顯示黑水虻粉可以有效地取代肉食性魚類飼料中相當一部分魚粉,且不會對魚類的生長表現產生負面影響。

此外,黑水虻非常符合當前歐洲的植物經濟模式,因為生產者可以從單一生質能流中提取粉劑、油脂和肥料。這提高了獲利能力,並使生產者能夠調整其在飼料及相關市場的產品組合。同時,穀蟲也迅速普及,預計2031年年複合成長率(CAGR)將達到13.6%。穀蟲在高階寵物食品和其他特殊應用領域尤其具有吸引力,在這些領域,消化率和低致敏性比大規模生產更為重要。歐盟於2025年1月批准了紫外線處理的穀蟲粉,這進一步拓展了加工機會,並促進了穀蟲生產設施的共用。其他昆蟲種類,例如家蠅和蟋蟀,目前在歐洲昆蟲飼料市場佔據的佔有率較小,主要服務於更具體的飼料應用,而非大規模工業用途。

到2025年,昆蟲粉將佔歐洲昆蟲飼料市場58.0%的佔有率,成為此階段的核心商業產品。其市場主導地位源自於其可直接應用於飼料飼料和複合飼料配方,而蛋白質濃度和消化率是這些產品的關鍵採購因素。市場仍依賴昆蟲粉作為現有飼料配方中蛋白質來源最方便的替代品。技術數據進一步佐證了其優勢,昆蟲粉具有高消化率和優異的氨基酸組成,使其越來越適用於特殊配方。因此,儘管整體產品系列日益多元化,但昆蟲粉仍然是應用最廣泛的產品。

昆蟲油是市場上成長最快的產品形式,預計2026年至2031年將以14.4%的複合年成長率成長。這一成長主要得益於寵物食品和單胃動物飼料對黑水虻油需求的不斷成長,尤其是其富含月桂酸和抗菌特性。整隻乾昆蟲的使用規模較小,主要用於點心、異寵和一些小眾特殊用途。其他產品形式,例如食物泥和水解物,也越來越受到關注,尤其是在寵物濕食和水產幼畜飼料領域,功能性產品在這些領域的重要性日益凸顯。歐洲昆蟲飼料產業正轉向利潤率更高的產品,例如油脂和特殊產品,以緩解銷售通用蛋白的成本壓力。 HiProMine和Nasekomo等公司的案例表明,在歐洲昆蟲飼料市場,產品策略的重要性正與規模擴大策略不相上下。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 歐盟飼料核准正在擴大對昆蟲蛋白質的潛在需求。

- 探索水產養殖飼料中魚粉和魚油的替代材料。

- 採用再生飼料採購和範圍 3 減排目標正在推動其實施。

- 寵物食品的日益精細化正在推動對新型昆蟲衍生原料的需求。

- 透過分離產品並與廢熱產生相協調,可以提高工廠的經濟效益。

- 功能性脂質、幾丁質和生物活性成分擴大了價值創造。

- 市場限制因素

- 生產成本仍然高於現有蛋白質替代品。

- 歐盟批准的原料清單限制了基材的柔軟性。

- 企業擴張失敗後對風險的重新評估將增加資金籌措的難度。

- 需求仍然集中在高階應用領域。

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 昆蟲種類

- 黑水虻

- 穀蟲

- 蒼蠅

- 其他

- 按產品形式

- 蛋白質餐

- 乾燥幼蟲(整隻)

- 昆蟲油

- 糞肥

- 依動物類型

- 水產養殖

- 家禽

- 豬

- 反芻動物

- 寵物

- 最終用戶

- 商業飼料廠

- 綜合畜牧養殖業務

- 小規模農戶/農場系統

- 按地區

- 德國

- 法國

- 英國

- 荷蘭

- 西班牙

- 義大利

- 波蘭

- 俄羅斯

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- InnovaFeed SAS

- Protix BV

- nextProtein SAS

- HiProMine SA

- Tebrio(Tebrio Group SL)

- Agronutris

- Volare

- Nasekomo

- BioflyTech

- Better Origin(Entomics Biosystems Limited)

- Hermetia Baruth

- Illucens

- Insectius

- FarmInsect

- EntoGreen

第7章 市場機會與未來展望

According to Mordor Intelligence, the europe insect feed market was valued at USD 0.54 billion in 2025 and is projected to grow from USD 0.60 billion in 2026 to USD 1.07 billion by 2031, registering a CAGR of 12.3% during the forecast period (2026-2031).

This report is Segmented by Insect Species (Black Soldier Fly, Mealworm, Housefly, and Others), by Product Form (Protein Meal, Whole Dried Larvae, Insect Oil, and Frass Fertilizer), by Animal Type (Aquaculture, Poultry, Swine, and More), by End User (Commercial Feed Mills and More), and by Geography (Germany, France, and More). The Market Forecasts are Provided in Terms of Value (USD).

Europe Insect Feed Market Trends and Insights

EU Feed Authorizations Expand Insect Protein Addressable Demand

The Europe insect feed market has benefited directly from the stepwise expansion of EU feed rules over the past several years. Regulation (EU) 2017/893 first allowed insect-processed animal proteins in aquaculture feed, and the 2021 amendment extended that permission to swine and poultry, which opened much larger livestock categories for commercial use. A 2024 regulatory clarification also confirmed that live insects can be used as feed materials for swine, poultry, and aquaculture, which gives smaller operators a lower processing route than full PAP production. Each authorization has widened the customer base for producers across aquaculture, poultry, swine, and pet food, and this has made industrial scaling more commercially rational. The Europe insect feed market is also supported by the formal adoption of the International Platform of Insects for Food and Feed (IPIFF) good hygiene guidance in 2025, which improves traceability and reduces procurement concerns for feed mills entering the category for the first time. Growth is still limited by the continued exclusion of ruminants, but monogastric and aquaculture categories already represent the clearest short-term route for scale in the Europe insect feed market.

Aquaculture Feed Seeks Fishmeal and Fish Oil Replacement

Aquaculture remains one of the strongest demand anchors for the Europe insect feed market because fishmeal supply is constrained while aquaculture feed demand keeps increasing. EU aquatic food self-sufficiency fell to 38.1% in 2023, and the bloc imports a large share of the feed proteins it consumes, which raises both supply security and sustainability concerns. Research in species such as rainbow trout, Atlantic salmon, European perch, and totoaba shows that insect meals can replace a meaningful share of fishmeal without damaging growth, digestibility, or product quality when inclusion is managed correctly. Norway is especially important because salmon farming has high feed-related emissions, which makes insect ingredients relevant not only as protein substitutes but also as carbon reduction tools inside existing feed systems. The Europe insect feed market is therefore drawing support from both performance validation and policy pressure in aquaculture. That combination becomes more important as industry groups push for formal inclusion targets in aquafeed over the next several years.

Demand Remains Concentrated in Premium Applications

Demand concentration is one of the major restraints shaping the Europe insect feed market. In practice, the strongest adoption still sits in aquaculture starter feeds, salmonid diets, premium pet food, and other higher-value channels rather than in broad poultry and swine formulations. Poultry and swine together make up most of the European compound feed tonnage, but those applications require much tighter price parity with soybean meal than the category can yet provide. Socio-economic research also suggests that mainstream economics remain tight even under significant scale increases, which means broad-based penetration is more likely to be gradual than sudden. This concentration matters because premium channels can be subject to reformulation cycles and brand positioning shifts. The Europe insect feed market, therefore, needs continued progress in cost reduction and industrial reliability before it can move from selective adoption into true mass-market inclusion.

Other drivers and restraints analyzed in the detailed report include:

- Pet Food Premiumization Lifts Demand for Novel Insect Ingredients

- Functional Lipids, Chitin, and Bioactive Fractions Broaden Value Capture

- EU-Approved Feedstock List Constrains Substrate Flexibility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Black soldier fly accounted for 49.5% of the Europe insect feed market in 2025, driven by its scalability, nutritional benefits, and processing flexibility. These larvae are highly preferred due to their efficient feed conversion, production of usable protein and oil fractions, and compatibility with industrial side-stream sourcing models. Consequently, the Europe insect feed market has predominantly adopted black soldier fly larvae as the primary platform for large-scale commercialization. Research has further validated this trend, demonstrating that black soldier fly meal can effectively replace a significant portion of fishmeal in carnivorous species without negatively impacting growth performance.

Black soldier fly also aligns well with current European plant economics, as producers can extract meal, oil, and fertilizer from a single biomass stream. This enhances revenue potential and allows producers to adjust their product mix across feed and related markets. Meanwhile, mealworms are rapidly gaining traction, with a projected CAGR of 13.6% through 2031. Mealworms are particularly appealing in premium pet food and other specialized applications where digestibility and hypoallergenic properties are prioritized over large-scale production. The EU's authorization of UV-treated mealworm powder in January 2025 has further expanded processing opportunities and facilitated facility-sharing for mealworm production. Other insect types, such as houseflies and crickets, currently occupy smaller niches within the Europe insect feed market, catering to more specific feed applications rather than large-scale industrial use.

Insect meal accounted for 58.0% of the Europe insect feed market in 2025, making it the core commercial product at this stage. Its prominence is attributed to its direct applicability in aquafeed and compound feed formulations, where protein concentration and digestibility are key purchasing factors. The market continues to rely on insect meal, as it is the most straightforward substitute for existing protein sources in established feed formulations. Technical data further supports its role, with insect meals demonstrating strong digestibility and amino acid profiles, making them increasingly suitable for specialized formulations. As a result, insect meal remains the most widely utilized product, even as the overall product portfolio diversifies.

Insect oil is the fastest-growing product form in the market, with a projected CAGR of 14.4% from 2026 to 2031. This growth is driven by rising demand for black soldier fly oil in pet food and monogastric feed, particularly for its lauric acid content and antimicrobial properties. Whole dried insects, while a smaller segment, are primarily used for treats, exotic animals, and niche specialty applications. Other product forms, such as puree and hydrolysates, are also gaining traction, especially in wet pet food and aquaculture starter feed applications, where functional formats are increasingly valued. The Europe insect feed industry is shifting toward higher-margin products like oils and specialty formats to mitigate the cost constraints associated with commodity protein sales. Companies such as HiProMine and Nasekomo illustrate that product strategy is becoming as critical as scale strategy in the Europe insect feed market.

Complete Report Scope:

- By Insect Species

- Black Soldier Fly

- Mealworm

- Housefly

- Others

- By Product Form

- Protein Meal

- Whole Dried Larvae

- Insect Oil

- Frass Fertilizer

- By Animal Type

- Aquaculture

- Poultry

- Swine

- Ruminants

- Pets

- By End User

- Commercial Feed Mills

- Integrated Livestock Producers

- Smallholder/On-farm Systems

- By Geography

- Germany

- France

- United Kingdom

- Netherlands

- Spain

- Italy

- Poland

- Russia

- Rest of Europe

List of Companies Covered in this Report:

- InnovaFeed SAS

- Protix B.V.

- nextProtein SAS

- HiProMine S.A.

- Tebrio (Tebrio Group S.L.)

- Agronutris

- Volare

- Nasekomo

- BioflyTech

- Better Origin (Entomics Biosystems Limited)

- Hermetia Baruth

- Illucens

- Insectius

- FarmInsect

- EntoGreen

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EU feed authorizations expand insect protein addressable demand

- 4.2.2 Aquaculture feed seeks fishmeal and fish oil replacement

- 4.2.3 Circular feed sourcing and Scope 3 reduction targets support adoption

- 4.2.4 Pet food premiumization lifts demand for novel insect ingredients

- 4.2.5 Co-location with side streams and waste heat improves plant economics

- 4.2.6 Functional lipids, chitin, and bioactive fractions broaden value capture

- 4.3 Market Restraints

- 4.3.1 Production costs remain above incumbent protein alternatives

- 4.3.2 EU-approved feedstock list constrains substrate flexibility

- 4.3.3 Risk repricing after scale-up failures tightens financing access

- 4.3.4 Demand remains concentrated in premium applications

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Insect Species

- 5.1.1 Black Soldier Fly

- 5.1.2 Mealworm

- 5.1.3 Housefly

- 5.1.4 Others

- 5.2 By Product Form

- 5.2.1 Protein Meal

- 5.2.2 Whole Dried Larvae

- 5.2.3 Insect Oil

- 5.2.4 Frass Fertilizer

- 5.3 By Animal Type

- 5.3.1 Aquaculture

- 5.3.2 Poultry

- 5.3.3 Swine

- 5.3.4 Ruminants

- 5.3.5 Pets

- 5.4 By End User

- 5.4.1 Commercial Feed Mills

- 5.4.2 Integrated Livestock Producers

- 5.4.3 Smallholder/On-farm Systems

- 5.5 By Geography

- 5.5.1 Germany

- 5.5.2 France

- 5.5.3 United Kingdom

- 5.5.4 Netherlands

- 5.5.5 Spain

- 5.5.6 Italy

- 5.5.7 Poland

- 5.5.8 Russia

- 5.5.9 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 InnovaFeed SAS

- 6.4.2 Protix B.V.

- 6.4.3 nextProtein SAS

- 6.4.4 HiProMine S.A.

- 6.4.5 Tebrio (Tebrio Group S.L.)

- 6.4.6 Agronutris

- 6.4.7 Volare

- 6.4.8 Nasekomo

- 6.4.9 BioflyTech

- 6.4.10 Better Origin (Entomics Biosystems Limited)

- 6.4.11 Hermetia Baruth

- 6.4.12 Illucens

- 6.4.13 Insectius

- 6.4.14 FarmInsect

- 6.4.15 EntoGreen