|

市場調查報告書

商品編碼

2072802

北美昆蟲飼料:市佔率分析、產業趨勢與統計及成長預測(2026-2031)North America Insect Feed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

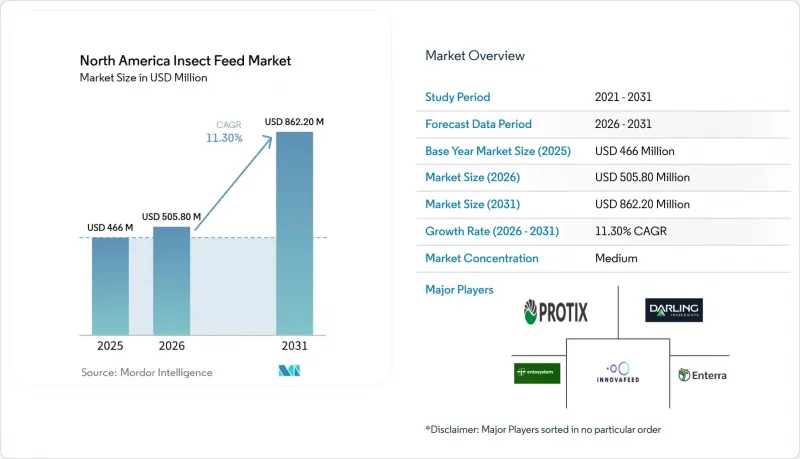

根據 Mordor Intelligence 預測,北美昆蟲飼料市場規模預計將在 2025 年達到 4.66 億美元,從 2026 年的 5.058 億美元成長到 2031 年的 8.622 億美元,在預測期(2026-2031 年)內複合年成長率為 11.3%。

本報告按昆蟲種類(例如,黑蠅、穀蟲)、產品形態(例如,昆蟲粉、昆蟲油)、應用領域(例如,水產養殖、家禽養殖)、最終用戶(例如,商業飼料廠)和地區(美國、加拿大、墨西哥、北美及其他地區)進行細分。市場預測以價值(美元)和數量(公噸)表示。

北美昆蟲飼料市場的趨勢與洞察

獲得 AAFCO 和 CFIA 的批准,擴大了其作為飼料的用途。

法規核准的進展仍然是北美昆蟲飼料市場最重要的成長要素。 2024年2月,美國飼料管理協會(AAFCO)批准了黑水虻幼蟲(BSFL)的臨時定義T60.117,授權將其用於鮭科魚類、家禽、豬和成年伴侶動物的飼料。 2024年1月,AAFCO也核准了乾穀蟲粉作為成犬飼料,這是第一個專門針對穀蟲的飼料定義。加拿大隨後於2024年7月推出了《2024年飼料法規》,更新了國家框架並簡化了部分昆蟲衍生原料的報名手續。由於每項批准都會在商業飼料廠的配製過程中增加一個新的步驟,因此新原料的採用往往是透過反覆的採購週期,而不是一次性的購買決策。這種模式支撐了北美昆蟲飼料市場需求的穩定成長,因為各種針對特定應用的批准開闢了新的、獨特的商業管道。加拿大於2026年4月提出的C-273號法案為此趨勢增添了新的要素。該法案允許在90天內對已在兩個或多個司法管轄區獲得批准的成分進行臨時註冊,預計將縮短產品商業化時間,並加強加拿大的監管地位。

魚粉和大豆粕價格的波動正在推動替代品的採用。

由於傳統飼料蛋白價格波動,北美昆蟲飼料市場相較於往年獲得了更穩固的經濟基礎。 2026年3月,全球魚粉價格達到每噸1,992美元,年增40.9%。同時,大豆粕為每噸312美元。這一價格差異意義重大,因為儘管在許多複合飼料中,昆蟲飼料的價格仍然高於豆粕,但對於面臨魚粉價格波動風險的買家而言,昆蟲飼料卻成為了更有效的對沖工具。根據聯合國糧農組織(FAO)的報告,受厄爾尼諾現象的影響,秘魯減少了鳀魚捕撈配額,導致2023年鳀漁獲量下降了28%。這表明,在氣候變遷的壓力下,海洋蛋白的供應會迅速變得緊張。此外,根據美國農業部2026年5月的市場數據,蛋白質含量為46.5%-48%的豆粕在美國玉米帶市場的交易價格為每噸315-360美元,這意味著僅就價格而言,昆蟲粉仍難以趕上豆粕的基準價格。因此,大規模飼料採購商越來越將昆蟲粉採購視為其供應鏈風險管理的一部分,這推動了昆蟲粉在高度依賴魚粉的北美昆蟲飼料市場中更廣泛的應用。

與傳統蛋白質來源相比,昆蟲粉的價格溢價較高

北美昆蟲飼料市場最大的商業性限制仍然是昆蟲粉相對於傳統蛋白質來源的價格溢價。根據美國農業部2026年5月的數據,豆粕價格為每噸315至360美元,遠低於商業性生產的昆蟲粉成本。雖然魚粉價格上漲提高了昆蟲粉作為水產養殖業替代品的可行性,但豬飼料和家禽飼料買家通常不會面臨足以僅從經濟角度出發就促使其廣泛採用昆蟲粉的價格衝擊。儘管透過規模化生產、育種技術進步、自動化和基材整合,昆蟲生產的成本曲線正在改善,但近期的挫折表明,這種轉型仍然成本高且進展不均衡。 2026年2月,達令原料公司(Darling Ingredients)累計5,800萬美元的業務重組成本和減損損失,主要與EnviroFlight和CTH的天然腸衣業務有關。這凸顯了當前嚴峻的經濟狀況。在價格有利時期,除非有更多生產商簽訂多年契約,否則通用飼料在北美昆蟲飼料市場的滲透率將仍然有限。

細分市場分析

到2025年,黑水虻幼蟲(BSFL)將佔據北美昆蟲飼料市場61.6%的佔有率,明顯優於北美昆蟲飼料市場中的所有其他昆蟲品種。這一地位得益於其廣泛的基材適應性、最全面的監管覆蓋以及與大多數競爭品種相比更優異的自動化生產系統相容性。美國飼料管理協會(AAFCO)的T60.117批准使黑水虻幼蟲可用於鮭科魚類、家禽、豬和成犬寵物食品,從而擴大了其在美國和加拿大的商業性應用範圍。預計從2026年到2031年,穀蟲的複合年成長率將達到17.0%,這主要得益於AAFCO於2024年1月批准其用於成犬食品,為這種新型昆蟲品種打開了高階寵物食品市場的大門。

黑水虻幼蟲也受惠於北美昆蟲飼料產業生產系統的成熟,增強了買家對供應穩定性的信心。德克薩斯農工大學農業生命研究中心於2026年1月採用了取得專利的「黑水虻幼蟲飼料塊」技術。該系統可將生產率提高20-30%,並使幼蟲在室溫下儲存數週至數月。穀蟲仍然具有巨大的潛力。與黑水虻幼蟲不同,它們的價值提案更適用於高階寵物食品領域,而非大規模水產養殖。蟋蟀和家蠅雖然規模較小,但在北美昆蟲飼料市場仍佔據重要地位,其知名度、偏好或特定物種的用途推動了試驗活動。

到2025年,昆蟲飼料將佔北美昆蟲飼料市場57.6%的佔有率,並繼續保持其在北美昆蟲飼料市場最大產品形態的地位。這一主導地位源於其明確的監管地位、易於整合到現有飼料配方體系中,以及在水產養殖和畜牧業應用中的可靠證據。此外,由於昆蟲粉的氨基酸組成能夠有效滿足物種特異性配方的需求,尤其是在甲硫胺酸和離胺酸比例至關重要的情況下,因此也備受買家青睞。昆蟲油是成長最快的產品形態,預計到2031年將以16.9%的複合年成長率成長,這主要得益於人們對黑水虻(BSFL)來源脂質的興趣。黑水虻脂質富含月桂酸,其應用範圍已不再局限於簡單的熱量替代。

整隻乾燥昆蟲產品在小規模但影響力較大的零售和專賣管道仍然很受歡迎,這些管道重視產品的視覺簡潔性和直接飼餵性,尤其是在家庭家禽養殖和某些伴侶動物飼料領域。 「其他」類別包括糞便和泥狀食物泥,隨著生產設施轉向處理多種產品的營運模式,這兩種產品的商業性價值都在不斷提升。 Entosystem 的 Drummondville 工廠和 Innovafeed 的 Decatur 工廠等設計案例表明,生產商正在圍繞蛋白質、脂肪和土壤改良劑等產品而非單一產品來建造工廠。這種轉變意義重大,因為在北美昆蟲飼料產業,產品形式的多樣化(而不僅僅是飼料粉的產量)正日益成為工廠盈利的基礎。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- AAFCO 和 CFIA 的批准擴大了其在飼料中的允許使用範圍。

- 魚粉和大豆粕價格的波動正在推動替代品的採用。

- 水產飼料生產商正在尋找國產魚粉的替代品。

- 對含有低過敏性蛋白質的優質寵物食品的需求

- 透過將食品和玉米加工產品集中在同一地點生產,單位成本效益提高了。

- 透過糞便貨幣化提高工廠的整體盈利

- 市場限制因素

- 昆蟲粉價格溢價與傳統蛋白質的比較

- 按物種和生命階段分類的批准限額限制了目標需求。

- 基板在預消費階段的限制以及封裝拆卸的瓶頸。

- 大型自動化設施資金短缺

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 依昆蟲種類

- 黑果蠅

- 穀蟲

- 蒼蠅

- 蟋蟀

- 其他

- 按產品形式

- 昆蟲粉

- 昆蟲油

- 乾昆蟲(整隻)

- 其他

- 透過使用

- 水產養殖

- 家禽

- 豬

- 寵物食品

- 其他動物飼料

- 最終用戶

- 商業飼料廠

- 綜合畜牧養殖業務

- 水產養殖場及孵化場

- 寵物食品製造商及其他

- 按地區

- 美國

- 加拿大

- 墨西哥

- 其他北美國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- EnviroFlight(Darling Ingredients Inc.)

- Enterra Feed Corporation

- Innovafeed SAS

- Protix BV

- Entosystem Inc.

- Oreka Solutions Inc.

- Oberland Agriscience Inc.

- Chapul Farms

- Amera Biotech

- BSFL Solutions Inc.

- Unique Biotech Inc.

- NutraFed, LLC

- Grubbly Farms

- Fluker's Cricket Farm, Inc.

- Nellie's Black Soldier Fly Larvae

第7章 市場機會與未來趨勢

According to Mordor Intelligence, the north america insect feed market size reached USD 466.0 million in 2025 and is projected to expand from USD 505.8 million in 2026 to USD 862.2 million by 2031, registering a CAGR of 11.3% during the forecast period (2026 - 2031).

This report is Segmented by Insect Type (Black Soldier Fly, Mealworm, and More), by Product Form (Insect Meal, Insect Oil, and More), by Application (Aquaculture, Poultry, and More), by End User (Commercial Feed Mills, and More), and by Geography (United States, Canada, Mexico, and Rest of North America). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

North America Insect Feed Market Trends and Insights

AAFCO and CFIA Approvals Expanding Permitted Feed Use

The pace of regulatory approvals remains the most operationally important growth driver in the North America insect feed market. Association of American Feed Control Officials (AAFCO) approved Black Soldier Fly Larvae (BSFL) tentative definition T60.117 in February 2024, which permitted use in salmonid, poultry, swine, and adult companion-animal food, and it also approved dried mealworm meal for adult dog food in January 2024 as the first mealworm-specific feed definition. Canada then introduced the Feeds Regulations 2024 in July 2024, which updated the national framework and simplified parts of the registration process for insect ingredient submissions. Each approval creates a new round of formulation work at commercial feed mills, so adoption tends to happen through repeat procurement cycles rather than a single purchasing decision. That pattern supports steady demand building in the North America insect feed market because each species and application approval opens another defined commercial lane. Canada's Bill C-273, introduced in April 2026, adds another layer to this theme because provisional registration within 90 days for ingredients already approved in 2 or more jurisdictions could shorten commercialization timelines and strengthen Canada's regulatory position.

Fishmeal and Soybean Meal Volatility Supporting Substitution

Price volatility in conventional feed proteins is giving the North America insect feed market a stronger economic footing than it had in earlier years. Global fishmeal prices reached USD 1,992 per metric ton in March 2026, up 40.9% year on year, while soybean meal stood at USD 312 per metric ton at the same point. This gap matters because it makes insect meal more relevant as a hedge for buyers exposed to fishmeal swings, even if insect meal still carries a premium to soy in many rations. FAO documented how El Nino-related anchovy quota reductions in Peru cut catches by 28% in 2023, which showed how quickly marine protein supply can tighten under climate stress. USDA market data from May 2026 also showed soybean meal at 46.5-48% protein trading at USD 315-360 per metric ton in U.S. corn-belt markets, so the soy benchmark remains difficult for insect meal to match on price alone. As a result, larger feed buyers are increasingly treating insect meal allocations as part of supply-chain risk management, which supports broader adoption in the North America insect feed market where fishmeal exposure is high.

Insect Meal Pricing Premium Versus Conventional Proteins

The largest commercial restraint in the North America insect feed market is still the pricing premium of insect meal against conventional proteins. USDA data from May 2026 showed soybean meal at USD 315-360 per metric ton, which stayed well below the cost of commercially produced insect meal. Fishmeal inflation has improved the substitution case in aquaculture, but swine and poultry buyers usually do not face a comparable price shock that would justify broad insect meal inclusion on economics alone. The cost curve for insect production is improving through scale, breeding advances, automation, and substrate integration, but recent setbacks show that this transition remains expensive and uneven. Darling Ingredients reported USD 58.0 million in restructuring and impairment charges in February 2026 related primarily to EnviroFlight and CTH natural casing businesses, which highlighted the pressure on current economics. Until more producers lock in multi-year contracts during favorable pricing windows, the North America insect feed market will continue to face limited penetration in commodity-grade rations.

Other drivers and restraints analyzed in the detailed report include:

- Aquaculture Feed Formulators Seeking Domestic Fishmeal Alternatives

- Premium Pet Food Demand for Hypoallergenic Proteins

- Capital Scarcity for Large Automated Facilities

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Black soldier fly larvae held 61.6% of North America insect feed market share in 2025, which kept BSFL clearly ahead of all other insect types in the North America insect feed market. Its position is supported by broad substrate versatility, the widest regulatory coverage, and stronger fit with automated production systems than most competing species. AAFCO's T60.117 approval gave BSFL access to salmonid, poultry, swine, and adult companion-animal uses, which widened its commercial reach in both the United States and Canada. Mealworms are forecast to grow at a 17.0% CAGR from 2026 to 2031, helped by AAFCO's January 2024 approval for adult dog food, which opened a premium companion-animal route for a new insect species.

BSFL also benefits from a more mature production profile in the North America insect feed industry, which gives buyers greater confidence in continuity of supply. Texas A&M AgriLife introduced the patented BSF Billet technology in January 2026, and the system points to 20-30% productivity gains along with room-temperature larval storage for weeks to months. Mealworms still have a meaningful opening because their value proposition is different from BSFL and more closely tied to premium pet nutrition than to bulk aquaculture volume. Crickets and houseflies remain smaller in scale, but they retain relevance where familiarity, palatability, or species-specific use cases support trial activity in the North America insect feed market.

Insect meal accounted for 57.6% of the North America insect feed market size in 2025, which kept protein concentrate as the largest product form in the North America insect feed market. This lead reflects its clearer regulatory standing, easier fit with existing feed formulation systems, and stronger evidence base across aquaculture and livestock uses. Buyers also value insect meal because its amino acid profile can work well in species-specific formulas where methionine and lysine balance matter. Insect oil is the fastest-growing product form with a 16.9% CAGR through 2031, supported by interest in BSFL lipids that are rich in lauric acid and are now being used for more than simple caloric substitution.

Whole dried insects still serve smaller but visible retail and specialty channels where visual simplicity and direct feeding matter, especially in backyard poultry and some companion-animal formats. The others category includes frass and puree, and both are becoming more commercially relevant as facilities move toward multi-output operating models. Entosystem's Drummondville site and Innovafeed's Decatur design both show that producers are structuring plants around protein, oil, and soil amendment rather than one output alone. That shift matters because the North America insect feed industry is increasingly rewarding product-form diversification, not just meal volume, as the basis for plant-level profitability.

Complete Report Scope:

- By Insect Type

- Black Soldier Fly

- Mealworms

- Houseflies

- Crickets

- Others

- By Product Form

- Insect Meal

- Insect Oil

- Whole Dried Insects

- Others

- By Application

- Aquaculture

- Poultry

- Swine

- Pet Food

- Other Animal Feed

- By End User

- Commercial Feed Mills

- Integrated Livestock Producers

- Aquaculture Farms and Hatcheries

- Pet Food Manufacturers and Others

- By Geography

- United States

- Canada

- Mexico

- Rest of North America

List of Companies Covered in this Report:

- EnviroFlight (Darling Ingredients Inc.)

- Enterra Feed Corporation

- Innovafeed SAS

- Protix B.V.

- Entosystem Inc.

- Oreka Solutions Inc.

- Oberland Agriscience Inc.

- Chapul Farms

- Amera Biotech

- BSFL Solutions Inc.

- Unique Biotech Inc.

- NutraFed, LLC

- Grubbly Farms

- Fluker's Cricket Farm, Inc.

- Nellie's Black Soldier Fly Larvae

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AAFCO and CFIA approvals expanding permitted feed use

- 4.2.2 Fishmeal and soybean meal volatility supporting substitution

- 4.2.3 Aquaculture feed formulators seeking domestic fishmeal alternatives

- 4.2.4 Premium pet food demand for hypoallergenic proteins

- 4.2.5 Co-location with food and corn-processing side streams improving unit economics

- 4.2.6 Frass monetization improving full-plant returns

- 4.3 Market Restraints

- 4.3.1 Insect meal pricing premium versus conventional proteins

- 4.3.2 Species and life-stage approval limits capping addressable demand

- 4.3.3 Preconsumer substrate restrictions and depackaging bottlenecks

- 4.3.4 Capital scarcity for large automated facilities

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Insect Type

- 5.1.1 Black Soldier Fly

- 5.1.2 Mealworms

- 5.1.3 Houseflies

- 5.1.4 Crickets

- 5.1.5 Others

- 5.2 By Product Form

- 5.2.1 Insect Meal

- 5.2.2 Insect Oil

- 5.2.3 Whole Dried Insects

- 5.2.4 Others

- 5.3 By Application

- 5.3.1 Aquaculture

- 5.3.2 Poultry

- 5.3.3 Swine

- 5.3.4 Pet Food

- 5.3.5 Other Animal Feed

- 5.4 By End User

- 5.4.1 Commercial Feed Mills

- 5.4.2 Integrated Livestock Producers

- 5.4.3 Aquaculture Farms and Hatcheries

- 5.4.4 Pet Food Manufacturers and Others

- 5.5 By Geography

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

- 5.5.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 EnviroFlight (Darling Ingredients Inc.)

- 6.4.2 Enterra Feed Corporation

- 6.4.3 Innovafeed SAS

- 6.4.4 Protix B.V.

- 6.4.5 Entosystem Inc.

- 6.4.6 Oreka Solutions Inc.

- 6.4.7 Oberland Agriscience Inc.

- 6.4.8 Chapul Farms

- 6.4.9 Amera Biotech

- 6.4.10 BSFL Solutions Inc.

- 6.4.11 Unique Biotech Inc.

- 6.4.12 NutraFed, LLC

- 6.4.13 Grubbly Farms

- 6.4.14 Fluker's Cricket Farm, Inc.

- 6.4.15 Nellie's Black Soldier Fly Larvae