|

市場調查報告書

商品編碼

2073136

校園交換器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Campus Switch - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

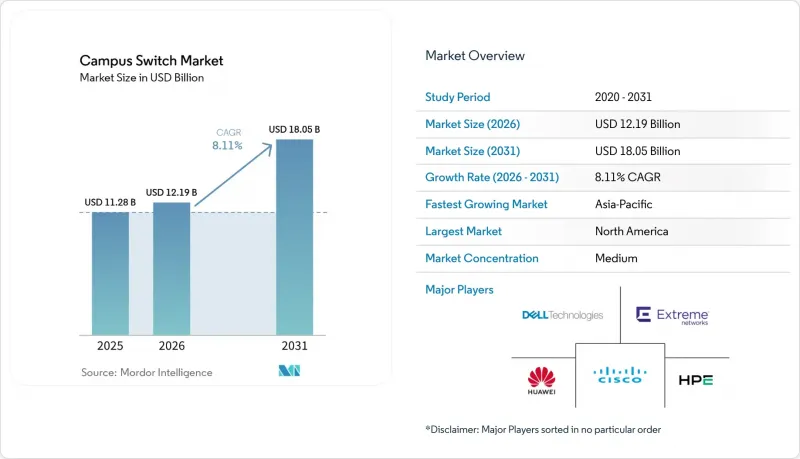

根據 Mordor Intelligence 預測,校園交換器市場規模將從 2025 年的 112.8 億美元成長到 2026 年的 121.9 億美元,然後在 2031 年達到 180.5 億美元,2026 年至 2031 年的複合年成長率為 8.1%。

本報告按交換器類型(固定配置交換器和模組化交換器)、端口速度(1 GbE 或更低、2.5/5 GbE 多千兆、10 GbE 及其他)、最終用戶企業規模(大型企業、中小企業)、最終用戶行業(教育機構、企業園區、政府和公共部門園區及其他)以及地區進行細分。市場預測以美元計價。

全球校園交換器市場趨勢與洞察

擴大Wi-Fi 6/6E和Wi-Fi 7的部署

Wi-Fi 7 的 320 MHz 頻道可提供超過 40 Gbps 的最大吞吐量,但也暴露了傳統Gigabit交換器仍然存在的存取層瓶頸。為了解決這一瓶頸問題,喬治城大學於 2025 年升級至配備 2.5/5 GbE 連接埠的 Catalyst 9000 交換器。據惠普企業 (Hewlett Packard Enterprise) 稱,目前 60% 的新款 Aruba 730 系列網路基地台都配備了多Gigabit交換機,這凸顯了有線回程傳輸需要跟上無線容量的步伐。華為在湖北大學於 2025 年推出的「光纖到辦公室 (FTOO)」計畫將 Wi-Fi 7 無線模組與 XGS-PON Pro+ 結合,實現了 10 Gbps 的邊緣頻寬。隨著越來越多的校園效仿這些案例,需求呈指數級成長,從接入層的多Gigabit端口到聚合數百個高速上行鏈路的 400 Gbps 主幹網,不一而足。因此,校園交換機市場將獲得強勁的成長動力,這種成長動力將遠遠超過最初的 Wi-Fi 7引進週期。

增加對智慧校園和教育科技領域的投資

生成式人工智慧、身臨其境型學習和整合式建築控制都依賴能夠提供服務品質 (QoS) 和千瓦級 PoE 供電的有線基礎設施。 2024 年,科羅拉多大學博爾德分校部署的 ChatGPT Edu 系統,其核心網路的日峰值流量達到 10 Tb,因此需要緊急升級到 400 Gbps 的主幹網路。伯明翰城市大學的數位轉型計畫需要 PoE++ 為安裝在每個教室的高解析度攝影機和物聯網感測器運作,這凸顯了現代教學方法與交換能力之間的緊密聯繫。阿德爾菲大學 2025 年的多千兆位元現代化改造將支援混合學習模式,為在校學生和遠距學生提供 4K影片。這些項目都體現了一個通用的認知:網路架構品質日益影響學生體驗和教育機構的競爭力,因此即使在財務謹慎的環境下,對交換器的投資也逐漸增加。

公立教育機構的預算限制

根據經合組織的數據,預計2023年至2024年間,高等教育生均實際支出將下降3%,這將對用於IT升級的可支配預算帶來壓力。加州在2025-2026會計年度削減了5億美元的社區學院經費,迫使各學區推遲部署多Gigabit平台,並延長已有10年歷史的交換機的使用壽命。世界銀行的統計數據顯示,在低收入國家,數位基礎建設目前僅佔教育支出的不到10%。這導致了兩極化:資金雄厚的私立大學正在加快升級週期,而公立院校則推遲升級,儘管設備老化,但交付速度卻十分緩慢。

細分市場分析

到 2025 年,固定配置交換器將佔據校園交換器市場 84.16% 的佔有率。由於中小學和分校的機架端口數很少超過 48 個,預計固定配置交換器將繼續主導接入櫃市場直至 2031 年。思科 Catalyst 9300 等產品提供的堆疊功能允許邏輯聚合多達 8 個單元,從而在不增加底盤複雜性的前提下提供一定程度的擴充性。然而,堆疊線會引入單點故障,而模組化背板可以避免這個問題,這種細微差別在技術評估中日益受到重視。因此,頂尖大學的採購團隊正在採用底盤方案,為匯聚層和核心層指定基於機箱的交換機,而為邊緣層保留固定配置交換器。這種方案既保持了模組化交換器的成長勢頭,又避免了徹底的替換。

儘管模組化交換器在2025年的銷售額佔比很小,但預計到2031年將以9.72%的年均成長率成長,超過整個園區交換器市場的表現。擁有數萬個終端的教育機構可以透過部署部分配置的底盤,並隨著學生人數和物聯網密度的增加擴展線路卡,從而提高投資回報率(ROIC)。瞻博網路(Juniper)的QFX5250在一個16插槽的機架中提供102.4 Tbps的處理能力,但管理員可以透過僅啟用必要的連接埠來降低初始投資。同樣,Extreme Networks的7830支援未來的800 Gbps光學模組,無需更換底盤。相較之下,固定配置型號在中小企業中仍然很受歡迎,因為這些企業更注重的是簡易性和快速部署,而不是插槽的柔軟性。

預計到 2025 年,1 GbE 及較慢的連接埠將佔出貨量的 44.82%,但隨著Gigabit上行鏈路被 Wi-Fi 6E 和 Wi-Fi 7 飽和,其佔有率正在下降。 2.5/5 GbE 多千兆埠預計將以 12.48% 的年成長率在所有速度等級中成長最快,並有望推動校園交換器接取層硬體市場的整體規模成長。 Juniper 的 EX4000 所有連接埠均支援多千兆和 PoE++,使教育機構能夠使用單一 SKU 實現從機房到核心的標準化。 Juniper 的無風扇 710XP 型號適用於對噪音敏感的圖書館和小規模教室,這表明多千兆功能不再是高階特性。

儘管 10Gigabit埠在伺服器上行鏈路中仍然發揮著至關重要的作用,但 25/40 千兆乙太網路主要局限於資料中心的葉層。隨著脊交換機需要聚合數百個上行Gigabit流量,對 100/400 Gbps 聚合的需求絕對值正在成長,但其在園區交換器市場的佔有率仍然有限。預計到 2028 年,Gigabit埠將應用於語音電話和傳統感測器,而多Gigabit將成為新建專案和大型維修的標準配置,這將改變供應商必須考慮的功率預算、散熱要求和價格範圍。

區域分析

亞太地區是成長最快的地區,預計複合年成長率將達到9.68%,這主要得益於各國人工智慧戰略對光纖密集型校園骨幹網的大力投入。在日本,SINET6升級至400Gbps引發了整個網路的需求激增,推動了100Gbps分配交換器的大量採購。在中國,學生宿舍升級到XGS-PON Pro+正在加速多Gigabit部署,消除了銅纜的限制。同時,在印度,隨著AirTrunk叢集12億美元收購Lumina CloudInfra,資料中心擴張叢集。

北美地區在2025年貢獻了37.82%的收入,這主要得益於Wi-Fi 7的早期部署和PoE的積極擴張。然而,隨著部署基礎日趨成熟和更新周期延長,成長速度正在放緩。聯邦政府為促進數位股權而採取的獎勵策略支撐了短期支出,但州和地方政府層面的財政壓力抑制了擴張,尤其是在社區大學和中小學學區。歐洲仍然是一個重要的市場,但受到財政緊縮措施的限制。

英國和德國的教育機構正在大力推行「數位化優先」課程,但跨境採購流程的複雜性阻礙了計畫的實施。南美洲的支出主要集中在巴西和阿根廷,但宏觀經濟波動阻礙了多年期計畫的進展。在中東,多元化的資金正投入新建的智慧校園建設中,並優先採用最新的交換技術。非洲的實施仍處於起步階段,主要集中在南非和奈及利亞,由於擔心電力供應的可靠性和貨幣疲軟,計畫在捐助資金的配合下謹慎推進。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章 執行概要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- Wi-Fi 6/6E 和 Wi-Fi 7 的廣泛應用

- 增加對智慧校園和教育科技領域的投資

- 學生和教職員的數據流量增加

- 校園內支援 PoE 供電的物聯網邊緣設備激增

- 校園網路安全韌性需求日益成長

- 推廣廠商中立的開放網路(SONiC、NOS 解耦)

- 市場限制因素

- 公立教育機構的預算限制

- 資本投資的更新周期較長(7-10年)。

- 缺乏網路自動化和軟體定義網路(SDN)的技能

- ASIC和光元件的供應鏈波動

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按開關類型

- 固定配置交換機

- 模組化開關

- 連接埠速度

- 1 GbE 或更低

- 2.5/5 GbE 多千兆以太網

- 10 GbE

- 25/40 GbE

- 100 GbE

- 400 GbE 或更高

- 按最終用戶公司規模分類

- 大公司

- 小型企業

- 最終用戶

- 教育(K-12 和高等教育)

- 企業及企業園區

- 政府及公共部門園區

- 其他最終用戶

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Cisco Systems, Inc.

- Huawei Technologies Co., Ltd.

- Hewlett Packard Enterprise Company

- Arista Networks, Inc.

- Dell Technologies Inc.

- Alcatel-Lucent Enterprise International SAS

- Extreme Networks, Inc.

- Fortinet, Inc.

- NETGEAR, Inc.

- TP-Link Technologies Co., Ltd.

- D-Link Corporation

- Ubiquiti Inc.

- Edgecore Networks Corporation

- Allied Telesis Holdings Corporation

- Ruijie Networks Co., Ltd.

- Nokia Corporation

- Cambium Networks

- Ruckus Networks

- Byezzy Tech

- Zyxel Communications Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the campus switch market size is projected to grow from USD 11.28 billion in 2025 to USD 12.19 billion in 2026 and is forecast to reach USD 18.05 billion by 2031 at a CAGR of 8.1% from 2026 to 2031.

This report is Segmented by Switch Type (Fixed Configuration Switches, and Modular Switches), Port Speed (1 GbE and Below, 2. 5/5 GbE Multi-Gig, 10 GbE, and More), End-User Enterprise Size (Large Enterprises, and SMEs), End-User Industry (Education, Enterprise and Corporate Campuses, Government and Public Sector Campuses, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Campus Switch Market Trends and Insights

Expansion of Wi-Fi 6/6E and Wi-Fi 7 Adoption

Wi-Fi 7's 320 MHz channels deliver headline throughput above 40 Gbps, exposing access-layer bottlenecks wherever legacy gigabit switching persists. Georgetown University upgraded to Catalyst 9000 switches with 2.5/5 GbE ports in 2025 to remove that choke point. Hewlett Packard Enterprise reports that 60% of new Aruba 730 series access points now ship with multi-gig switches, underscoring that the wired backhaul must keep pace with wireless capacity. Huawei's 2025 fiber-to-the-office project at Hubei University pairs Wi-Fi 7 radios with XGS-PON Pro+ to deliver 10 Gbps of edge bandwidth. As more campuses emulate these examples, demand cascades from access-layer multi-gig ports to 400 Gbps spines that aggregate hundreds of high-speed uplinks. The campus switch market, therefore, gains a durable growth engine that extends well beyond the initial Wi-Fi 7 refresh cycle.

Growth in Smart Campus and EdTech Investments

Generative AI, immersive learning, and converged building controls all ride on wired infrastructure that can enforce quality of service and deliver PoE power budgets measured in kilowatts. University of Colorado Boulder's ChatGPT Edu launch in 2024 drove daily peak traffic to 10 Tb across the core, forcing emergency upgrades to 400 Gbps spines. Birmingham City University's digital-transformation program required PoE++ to run high-definition cameras and IoT sensors in every classroom, highlighting that modern pedagogy intertwines with switching capabilities. Adelphi University's 2025 multi-gig refresh aligns with hybrid learning models that stream 4K video to on-campus and remote students. These projects share the thesis that network fabric quality increasingly influences student experience and institutional competitiveness, which, in turn, fuels incremental switch spending even in fiscally cautious environments.

Budgetary Constraints in Public Educational Institutions

OECD data show that real per-student tertiary spending fell 3% between 2023 and 2024, squeezing discretionary budgets for IT upgrades. California cut community-college funding by USD 500 million for fiscal 2025-2026, prompting districts to extend the service life of decade-old switches rather than adopt multi-gig platforms. World Bank figures indicate that lower-income countries now devote under 10% of education outlays to digital infrastructure. The result is a bifurcation: well-endowed private universities advance refresh cycles, while public institutions defer, dampening unit shipments even as the installed base ages.

Other drivers and restraints analyzed in the detailed report include:

- Rising Data Traffic per Student and Staff Device

- Surge in PoE-Powered IoT Edge Devices on Campuses

- Lengthy Cap-Ex Refresh Cycles (7-10 Years)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fixed Configuration Switches held 84.16% of the campus switch market share in 2025. Fixed configuration switches will still dominate access closets through 2031 because K-12 and branch offices rarely exceed 48 ports per rack. Stacking options, such as Cisco Catalyst 9300, allow logical aggregation of up to 8 units, offering some scale without chassis complexity. However, stacking cables introduces single-point failure domains that modular backplanes avoid, a nuance increasingly acknowledged in technical evaluations. Consequently, procurement teams at flagship universities specify chassis for distribution and core layers while retaining fixed models at the edge, a hybrid approach that tempers absolute displacement but sustains modular growth momentum.

Modular switches captured a modest slice of revenue in 2025 but are forecast to grow 9.72% annually through 2031, outstripping the broader campus switch market. Institutions with tens of thousands of endpoints can install a partially populated chassis and scale line cards as enrollment or IoT density increases, thereby improving return on invested capital. Juniper's QFX5250 delivers 102.4 Tbps in a 16-slot frame, yet administrators can light only the ports they need, reducing upfront cash outlay. Extreme Networks' 7830 likewise supports future 800 Gbps optics without requiring a chassis replacement. In contrast, fixed configuration models remain popular in SMEs, where simplicity and rapid deployment matter more than slot flexibility.

In 2025, 1 GbE and slower ports held 44.82% of shipments, but their share is sliding as Wi-Fi 6E and Wi-Fi 7 saturate gigabit uplinks. The 2.5/5 GbE multi-gig tier is projected to expand 12.48% annually, the fastest of any speed class, lifting the overall campus switch market size for access-layer hardware. Juniper's EX4000 delivers multi-gig and PoE++ across every port, enabling institutions to standardize on a single SKU from the closet to the core. Arista's fanless 710XP caters to noise-sensitive libraries and small classrooms, underscoring that multi-gig is no longer a premium feature.

Ten-gigabit ports remain relevant for server uplinks, while 25/40 GbE remain mostly confined to data-center leaf roles. Demand for 100/400 Gbps aggregation climbs in absolute terms because spines must funnel hundreds of multi-gig flows upstream, but their share within the campus switch market remains modest. By 2028, gigabit ports are expected to serve voice handsets and legacy sensors, whereas multi-gigabit becomes the default across new construction and major renovations, changing the mix of power budgets, cooling requirements, and price bands that vendors must target.

Complete Report Scope:

- By Switch Type

- Fixed Configuration Switches

- Modular Switches

- By Port Speed

- 1 GbE and Below

- 2.5/5 GbE Multi-Gig

- 10 GbE

- 25/40 GbE

- 100 GbE

- 400 GbE and Above

- By End-user Enterprise Size

- Large Enterprises

- SMEs

- By End-User

- Education (K-12 and Higher Education)

- Enterprise and Corporate Campuses

- Government and Public Sector Campuses

- Other End-Users

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

Asia-Pacific is the fastest-growing region at a projected 9.68% CAGR, fueled by national AI strategies that bankroll fiber-rich campus backbones. Japan's SINET6 400 Gbps upgrade cascades demand across the network, prompting bulk purchases of 100 Gbps distribution switches. China's leapfrog to XGS-PON Pro+ in student housing eliminates copper limitations and accelerates multi-gig adoption, while India's data-center build-out following AirTrunk's USD 1.2 billion acquisition of Lumina CloudInfra requires 400 Gbps spines to marry compute and storage clusters.

North America held 37.82% of 2025 revenue on the strength of early Wi-Fi 7 deployments and aggressive PoE rollouts. Growth, however, decelerates as the installed base matures and refresh cycles lengthen. Federal stimulus tied to digital equity sustains near-term spending, but fiscal pressure at state and local levels tempers expansion, especially in community colleges and K-12 districts. Europe remains significant yet constrained by austerity budgets.

Institutions in the United Kingdom and Germany pursue digital-first curricula, but cross-border procurement complexity slows velocity. South America's spending centers on Brazil and Argentina, but macroeconomic volatility hampers multi-year projects. The Middle East channels diversification funds into greenfield smart campuses, favoring the latest switching technology. Africa's nascent adoption concentrates in South Africa and Nigeria, where power reliability and currency depreciation dictate cautious rollouts aligned with donor financing.

- Cisco Systems, Inc.

- Huawei Technologies Co., Ltd.

- Hewlett Packard Enterprise Company

- Arista Networks, Inc.

- Dell Technologies Inc.

- Alcatel-Lucent Enterprise International SAS

- Extreme Networks, Inc.

- Fortinet, Inc.

- NETGEAR, Inc.

- TP-Link Technologies Co., Ltd.

- D-Link Corporation

- Ubiquiti Inc.

- Edgecore Networks Corporation

- Allied Telesis Holdings Corporation

- Ruijie Networks Co., Ltd.

- Nokia Corporation

- Cambium Networks

- Ruckus Networks

- Byezzy Tech

- Zyxel Communications Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTON

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of Wi-Fi 6/6E and Wi-Fi 7 Adoption

- 4.2.2 Growth in Smart Campus and EdTech Investments

- 4.2.3 Rising Data Traffic per Student and Staff Device

- 4.2.4 Surge in PoE-Powered IoT Edge Devices on Campuses

- 4.2.5 Increasing Campus Cyber-Resilience Requirements

- 4.2.6 Vendor Neutral Open-Networking Push (SONiC, NOS Disaggregation)

- 4.3 Market Restraints

- 4.3.1 Budgetary Constraints in Public Educational Institutions

- 4.3.2 Lengthy Cap-Ex Refresh Cycles (7-10 Years)

- 4.3.3 Skills Shortage in Network Automation and SDN

- 4.3.4 Supply-Chain Volatility for ASICs and Optics

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Switch Type

- 5.1.1 Fixed Configuration Switches

- 5.1.2 Modular Switches

- 5.2 By Port Speed

- 5.2.1 1 GbE and Below

- 5.2.2 2.5/5 GbE Multi-Gig

- 5.2.3 10 GbE

- 5.2.4 25/40 GbE

- 5.2.5 100 GbE

- 5.2.6 400 GbE and Above

- 5.3 By End-user Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 SMEs

- 5.4 By End-User

- 5.4.1 Education (K-12 and Higher Education)

- 5.4.2 Enterprise and Corporate Campuses

- 5.4.3 Government and Public Sector Campuses

- 5.4.4 Other End-Users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Cisco Systems, Inc.

- 6.4.2 Huawei Technologies Co., Ltd.

- 6.4.3 Hewlett Packard Enterprise Company

- 6.4.4 Arista Networks, Inc.

- 6.4.5 Dell Technologies Inc.

- 6.4.6 Alcatel-Lucent Enterprise International SAS

- 6.4.7 Extreme Networks, Inc.

- 6.4.8 Fortinet, Inc.

- 6.4.9 NETGEAR, Inc.

- 6.4.10 TP-Link Technologies Co., Ltd.

- 6.4.11 D-Link Corporation

- 6.4.12 Ubiquiti Inc.

- 6.4.13 Edgecore Networks Corporation

- 6.4.14 Allied Telesis Holdings Corporation

- 6.4.15 Ruijie Networks Co., Ltd.

- 6.4.16 Nokia Corporation

- 6.4.17 Cambium Networks

- 6.4.18 Ruckus Networks

- 6.4.19 Byezzy Tech

- 6.4.20 Zyxel Communications Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2034年中等教育市場預測-按教育機構類型、學習形式、課程類型、所有權和地區分類的全球分析國際教育市場預測至2034年-按教育程度、學習形式、課程類型、學生類型、資金來源和地區分類的全球分析教育考試服務市場預測至2034年-按考試類型、交付方式、服務類型、最終用戶和地區分類的全球分析2034年教育市場預測-按教育程度、機構類型、資金籌措模式、服務類型、所有權、交付環境和地區分類的全球分析STEM機器人教育市場預測至2034年—按組件、部署模式、機器人類型、組織規模、應用、最終用戶和地區分類的全球分析課堂管理軟體市場預測至2034年-按組件、部署模式、功能、設備類型、最終用戶和地區分類的全球分析2034 年前高階主管認知能力發展輔導市場預測:按服務類型、交付方式、輔導形式、平台、應用、最終用戶和地區分類的全球分析

2034年中等教育市場預測-按教育機構類型、學習形式、課程類型、所有權和地區分類的全球分析國際教育市場預測至2034年-按教育程度、學習形式、課程類型、學生類型、資金來源和地區分類的全球分析教育考試服務市場預測至2034年-按考試類型、交付方式、服務類型、最終用戶和地區分類的全球分析2034年教育市場預測-按教育程度、機構類型、資金籌措模式、服務類型、所有權、交付環境和地區分類的全球分析STEM機器人教育市場預測至2034年—按組件、部署模式、機器人類型、組織規模、應用、最終用戶和地區分類的全球分析課堂管理軟體市場預測至2034年-按組件、部署模式、功能、設備類型、最終用戶和地區分類的全球分析2034 年前高階主管認知能力發展輔導市場預測:按服務類型、交付方式、輔導形式、平台、應用、最終用戶和地區分類的全球分析 2026-2030年全球幼兒教育市場

2026-2030年全球幼兒教育市場 2026年全球領導力發展專案市場報告

2026年全球領導力發展專案市場報告 留學申請平台市場:按服務提供者、應用類型、經營模式和地區分類

留學申請平台市場:按服務提供者、應用類型、經營模式和地區分類