|

市場調查報告書

商品編碼

2073056

耐磨鋼板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)Abrasion Wear Resistant Steel Plates - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

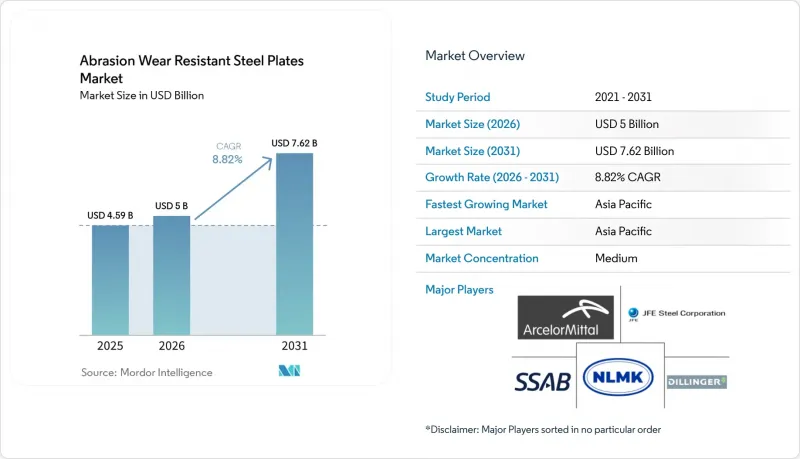

根據 Mordor Intelligence 預測,耐磨鋼板的市場規模預計將在 2025 年達到 45.9 億美元,2026 年達到 50 億美元,到 2031 年達到 76.2 億美元,2026 年至 2031 年的複合年成長率為 8.82%。

本報告按產品類型(HB 400、450 及其他)、客戶類型(OEM、分銷商、維護承包商及其他)、終端用戶行業(採礦、採石、水泥、建築、回收及其他)、板材厚度(薄(10 毫米或以下)、中(10-40 毫米)、厚(40 毫米以上)和地區(亞太地區及其他地區)進行細分。市場預測以美元計價。

全球耐磨鋼板市場趨勢及洞察

來自採礦和建築業的需求不斷成長

銅、鋰和稀土元素領域的新計畫推動了自動卸貨卡車車廂、襯板和輸送機部件的訂單成長。在亞太地區,挖土機和裝載機的產量激增,以支持交通運輸和基礎設施建設。北美原始設備製造商 (OEM) 正在採用更高硬度的鋼板,以有效應對監管規定的重量限制。作為一項策略性舉措,安賽樂米塔爾新日鐵印度公司已撥款將其產能提高三倍,旨在縮短國內交貨週期並減少對進口的依賴。礦業業者越來越傾向於使用 HB 500 以上硬度等級的鋼板。這一趨勢使得在偏遠地區延長作業間隔成為可能,因為在這些地區,停機成本遠高於更高的材料成本。因此,這一趨勢不僅導致超高硬度鋼板供應趨緊,也提高了價格穩定性。

法規主導了安全性和耐磨性標準的擴展

IS 18809:2024 和 GB/T 24186-2022 透過強制規定硬度和衝擊韌性標準、收緊 OEM競標規範以及逐步淘汰舊式低碳鋼部件,確立了新的標準。新的可追溯性法規引入了熱處理編號標記和認證檢驗報告,降低了造假風險,並鼓勵客戶選擇經過嚴格審核、資本投入高的厚鋼板製造商。美國和歐盟的安全監管機構修訂了其設備指南,將 HB 400 指定為標準。因此,HB 450 及更高硬度的鋼材越來越受到重載應用的青睞。

超高硬度牌號的生產成本很高

精細的淬火和回火製程、合金化過程中添加鉻和鉬,以及嚴格的後處理檢驗,都推高了某些產品的單位成本。 2025年,SSAB撥出巨額預算用於升級其位於奧克瑟洛松德的電弧爐(EAF),旨在維持其高階產能。同時,歐盟能源價格的上漲正給該鋼鐵廠的利潤率帶來壓力,並限制了HB 550和HB 600鋼板價格折扣的柔軟性。

細分市場分析

預計到2025年,HB 450將佔總銷售額的34.39%,已成為礦業和自動卸貨卡車應用領域的領先產品。耐磨鋼板市場,尤其是HB等級高於500的產品市場,預計在2026年至2031年的預測期內將以10.47%的複合年成長率穩步成長。這一成長歸功於礦業公司採用更硬、更薄的襯板來最佳化卡車的負載容量,同時又不影響其耐用性。 2026年3月,SSAB公司發布了Hardox HiAce,這是一款創新產品,它結合了HB 450的硬度和高達400攝氏度的耐腐蝕性。這項進步將使其應用範圍擴展到更廣泛的領域,包括水泥冷卻器和廢棄物箱。

超硬鋼材受益於數位雙胞胎分析,該分析證實,延長維護週期可以抵消此類鋼材較高的價格。然而,挑戰依然存在。焊接工藝的複雜性和合金附加費的增加導致其價格與HB 400鋼材相比有顯著差異。遵循IS 18809:2024化學成分標準的鋼廠難以平衡硼和碳的當量值,以確保鋼材的韌性。應對這項挑戰需要投資線上淬火設備和自動化檢測工具。儘管如此,礦業承包商已從中受益。改用「Hardox 500 Tuf」鋼材後,卡車重量減輕了500多公斤,從而顯著節省了燃油成本。這不僅增強了其在總擁有成本(TCO)方面的優勢,也提升了人們對該領域成長的信心。

到2025年,分銷商將佔全球銷售額的48.47%,凸顯了售後市場的細分特性,而快速決策在該市場至關重要。同時,OEM廠商直接採購耐磨鋼板的市佔率正在擴大,預計在2026年至2031年的預測期內,OEM市場規模將以9.66%的複合年成長率成長。這一成長主要得益於設備製造商在結構模擬和生命週期碳排放評估中日益重視鋼板的選擇。此外,為確保2027年推出的所有卡車從鋼鐵廠到生產線的供應鏈,相關合約的簽署也印證了這項轉變。

鋼廠擁有的服務網路進一步強化了原始設備製造商 (OEM) 的影響力。 SSAB 旗下擁有 550 家門市的「Hardox Wearparts」連鎖店提供隔日送達的配件包,幫助 OEM 減少庫存積壓並簡化保固追蹤。雖然分銷商在緊急維修和小批量訂單方面仍然發揮作用,但其重要性正在下降。鋼廠和製造商之間日益增多的開發數據、軟體介面和性能診斷資訊共用,也印證了這一趨勢。

區域分析

到2025年,亞太地區將佔全球銷售額的58.53%,佔據主導地位,預計在2026年至2031年的預測期內,其複合年成長率將達到9.49%,超過其他所有地區。中國的GB/T 24186-2022標準已成為國內OEM競標的基礎,並顯著降低了中國對進口的依賴。同時,印度的IS 18809:2024標準正使國內生產與國際標準接軌,使「印度製造」採購團隊能夠縮短前置作業時間。安賽樂米塔爾新日鐵印度公司正按計畫推進產能擴張,目標是在2030年前實現產能擴張,從而確保鋼板的穩定供應,以滿足國內外市場需求,特別是挖土機和自動卸貨卡車的需求。

雖然北美並非主要參與企業,但它正利用在採礦業的投資,尤其是在內華達州和安大略省的電池金屬領域。作為一項政策主導的在地化舉措,加拿大政府正向泰特斯鋼鐵公司提供補貼,以加強其供應鏈,以應對可能出現的運輸中斷。在美國,設備製造商正轉向使用低碳鋼板。這項轉變受到各州採購法規的影響,這些法規已採用範圍3會計準則。這項轉變為「SSAB Zero」產品的交付鋪平了道路,這些產品將儲存在愛荷華州的一個新堆場。

儘管歐洲經濟成長軌跡已穩定在個位數中段水平,但由於環境附加費等原因,高價依然存在。 SSAB即將啟動的項目,例如奧克瑟松德電弧爐(EAF)和呂勒奧小型鋼廠的運作,預計將在未來十年內顯著降低範圍1排放。這使得歐洲產鋼材成為優先考慮經檢驗的低碳含量的汽車和建築設備製造商的理想選擇。此外,北約成員國對特種產品的需求也在不斷成長,尤其是在國防裝備維修,例如裝甲車輛的地板。

儘管寶鋼在南美和中東及非洲(MENA)地區的市場佔有率仍然不高,但這兩個地區均呈現強勁的中個位數成長。這一成長主要得益於智利和秘魯銅礦的擴張,以及沙烏地阿拉伯紅海沿岸正在進行的大型企劃。寶鋼位於拉斯蓋爾的先進鋼板廠採用經濟高效的天然氣直接還原鐵(DRI)生產,預計將成為中東及北非(MENA)地區礦山和造船廠的主要鋼板供應商。這種在地化生產不僅將簡化沿岸地區礦業承包商的採購流程,還將緩解重型鋼板運輸帶來的物流挑戰。

貿易緊張局勢仍構成緊迫威脅。浦項鋼鐵正積極加大對美國和印度下游資產的投資,以策略性地應對北美可能出現的高額進口關稅。這些策略性舉措,加上各地區的具體法規和產能投資,凸顯了影響耐磨鋼板市場的複雜動態。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 採礦和建築業需求增加

- 由於法規要求,安全和穿著標準有所擴展。

- 用於將供應鏈本地化到重型設備中心的獎勵

- 循環經濟中對再生耐磨鋼板原料的需求

- 數位雙胞胎可實現預測性磨損最佳化。

- 市場限制因素

- 超高硬度等級產品的製造成本很高

- 硬度值超過 500 的鋼種在加工和焊接柔軟性方面有其限制

- 耐磨合金焊接熟練工人短缺

- 價值鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 依產品類型

- HB 400

- HB 450

- HB 500

- HB 500 或以上

- 依客戶類型

- OEM

- 銷售代理

- 維修承包商

- 其他

- 按最終用戶行業分類

- 礦業

- 採石業

- 水泥

- 建造

- 回收利用

- 其他

- 按板材厚度

- 薄板(10毫米或更薄)

- 中等厚度板材(10-40毫米)

- 厚板(40毫米或更厚)

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ASEAN

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- AG der Dillinger Huttenwerke

- ArcelorMittal

- Baosteel Co., Ltd.

- Bisalloy Steel Group

- CMC(Commercial Metals Co.)

- Eckhardt Steel & Alloy

- Hbis Steel Group

- JFE Steel Corporation

- NIPPON STEEL CORPORATION

- NLMK Group

- Nucor Corporation

- POSCO India PC

- Salzgitter Mannesmann

- SIJ Slovenian Steel Group dd

- SSAB

- Tata Steel Nederland BV

- voestalpine Stahl GmbH

第7章 市場機會與未來展望

According to Mordor Intelligence, the abrasion wear resistant steel plates market size is projected to be USD 4.59 billion in 2025, USD 5 billion in 2026, and reach USD 7.62 billion by 2031, growing at a CAGR of 8.82% from 2026 to 2031.

This report is Segmented by Product Type (HB 400, 450, and More), Customer Type (OEMs, Distributors, Maintenance Contractors, and Others), End-User Industry (Mining, Quarrying, Cement, Construction, Recycling, and Others), Plate Thickness (Thin <=10 Mm, Medium 10-40 Mm, and Thick (more Than 40 Mm)), and Geography (Asia-Pacific, and More). The Market Forecasts are Provided in Value (USD).

Global Abrasion Wear Resistant Steel Plates Market Trends and Insights

Rising Demand from Mining and Construction Sectors

New projects in the copper, lithium, and rare-earth sectors are driving up orders for dump-truck bodies, liners, and conveyor components. In the Asia-Pacific region, the production of excavators and loaders has surged to support transport and infrastructure initiatives. North-American OEMs are adopting higher-hardness plates to navigate regulatory weight constraints effectively. In a strategic move, ArcelorMittal Nippon Steel India has allocated funds to triple its capacity, aiming for faster domestic deliveries and reduced reliance on imports. Mining operators are increasingly favoring HB 500 and grades above 500. This preference enables them to extend operational intervals in remote sites, where downtime costs significantly exceed material premiums. As a result, this trend not only tightens the supply of ultra-hard grades but also reinforces price stability.

Regulation-Driven Safety and Wear Standards Expansion

IS 18809:2024 and GB/T 24186-2022 set new benchmarks by mandating hardness and impact-toughness criteria, tightening OEM bid specifications, and phasing out older mild-steel components. New regulations on traceability introduced heat-number stamping and certified test reports, which reduced counterfeiting risks and directed orders to rigorously audited high-capex plate mills. Safety agencies in the United States and the European Union updated equipment guidelines, designating HB 400 as the standard. As a result, heavy-duty applications increasingly favor HB 450 and harder variants.

High Production Costs of Ultra-Hardness Grades

The meticulous quench-and-temper protocols, the incorporation of chromium and molybdenum during alloying, and rigorous post-treatment inspections have driven up unit costs for certain products. In 2025, SSAB earmarked a substantial budget to upgrade its Oxelosund EAF with the aim of maintaining its premium capacity. At the same time, rising energy prices in the European Union have tightened mill margins, limiting the discounting flexibility for HB 550 and HB 600 plates.

Other drivers and restraints analyzed in the detailed report include:

- Supply-Chain Localization Incentives in Heavy-Equipment Hubs

- Circular-Economy Demand for Recycled Wear-Plate Feedstock

- Limited Fabrication and Welding Flexibility at HB grades greater than 500

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

HB 450, which is projected to account for 34.39% of 2025's revenue, establishes its position as a key player in the mining and dump-body applications. The market for abrasion wear-resistant steel plates, particularly those with HB grades exceeding 500, is poised for robust growth at a 10.47% CAGR during the forecast period of 2026-2031. This growth is attributed to mines adopting harder, thinner liners that optimize truck payloads without compromising durability. In March 2026, SSAB unveiled Hardox HiAce, an innovation that combines the hardness of HB 450 with corrosion resistance up to 400 degrees Celsius. This advancement opens doors to wider applications, such as cement coolers and waste-handling bins.

Ultra-hard grades are benefiting from digital-twin analytics, which confirm that longer service intervals can offset the premium costs of these plates. However, challenges persist: complexities in welding and increased alloy surcharges lead to a notable price gap when compared to HB 400. Mills operating under IS 18809:2024 chemistry standards grapple with balancing boron and carbon-equivalent values to ensure toughness. This challenge necessitates investments in in-line quench equipment and automated inspection tools. Still, mining contractors are reaping the rewards. By switching to Hardox 500 Tuf, truck bodies have shed over 500 kilograms, translating to significant fuel savings. This not only strengthens the cost-of-ownership argument but also boosts confidence in the segment's growth.

In 2025, distributors accounted for 48.47% of global revenue, underscoring the fragmented nature of the aftermarket, where swift decisions are crucial. Meanwhile, the market share for OEM direct purchases of abrasion wear-resistant steel plates is increasing, with OEMs growing at a CAGR of 9.66% in the forecast period of 2026-2031. This growth is attributed to equipment builders increasingly factoring plate selection into their structural simulations and life-cycle carbon assessments. A testament to this shift is the agreement that secures a mill-to-line supply chain for all trucks debuting in 2027.

OEM influence is reinforced by mill-owned service networks. SSAB's 550-member Hardox Wearparts chain delivers next-day kits, helping OEMs eliminate buffer inventory and simplifying warranty tracking. While distributors will continue to play a role in addressing repair emergencies and small-lot orders, their significance is waning. This decline is evident as mills and builders increasingly share ownership of development data, software interfaces, and performance diagnostics.

Complete Report Scope:

- By Product Type

- HB 400

- HB 450

- HB 500

- HB grades greater than 500

- By Customer Type

- OEMs

- Distributors

- Maintenance Contractors

- Other Customer Types

- By End-User Industry

- Mining

- Quarrying

- Cement Industry

- Construction

- Recycling Industry

- Other End-user Industries

- By Plate Thickness

- Thin Plates (<=10 mm)

- Medium Plates (10-40 mm)

- Thick Plates (more than 40 mm)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Nordic Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- United Arab Emirates

- Rest of Middle-East and Africa

- Asia-Pacific

Geography Analysis

In 2025, the Asia-Pacific region commanded a dominant 58.53% share of global revenue and is set to outpace all other regions with a CAGR of 9.49% projected through the forecast period of 2026-2031. China's GB/T 24186-2022 standard has become the cornerstone for domestic OEM tenders, significantly reducing the nation's dependence on imports. Concurrently, India's IS 18809:2024 standard is harmonizing local production with international benchmarks, allowing "Make in India" procurement teams to shorten lead times. ArcelorMittal Nippon Steel India is on track to expand its capacity by 2030, ensuring a consistent supply of flat plates to meet the demands of both domestic and export markets, particularly for excavators and tippers.

North America, though not the dominant player, is capitalizing on mining investments, especially in battery-metal initiatives in Nevada and Ontario. Highlighting a policy-driven localization effort, the Canadian government has granted Titus Steel a subsidy, aiming to fortify supply chains against shipping disruptions. In the United States, equipment manufacturers are pivoting towards low-carbon plates, a shift influenced by state procurement rules adopting Scope 3 accounting. This transition paves the way for SSAB Zero deliveries, which are slated to be housed in a new yard in Iowa.

Europe's growth trajectory may be stabilizing at mid-single digits, yet it commands premium pricing, in part due to environmental surcharges. SSAB's forthcoming projects, such as the Oxelosund EAF start-up and the Lulea mini-mill, are poised to make significant cuts to Scope 1 emissions over the next decade. This positions European tonnage as a preferred choice for automotive and construction OEMs that prioritize verified low-carbon content. Moreover, NATO member states are ramping up their demand for specialty products, especially in defense retrofits like armored-vehicle floor plates.

While South America and the Middle-East and Africa maintain modest market shares, both regions are experiencing robust mid-single-digit growth rates. This expansion is primarily fueled by copper pit enlargements in Chile and Peru, coupled with ambitious infrastructure megaprojects along the Saudi Red Sea coast. Baosteel's state-of-the-art plate mill in Ras Al-Khair, utilizing cost-effective natural gas DRI, is set to become a key supplier of plates to MENA mines and shipyards. This localized production not only simplifies procurement for Gulf mining contractors but also alleviates freight challenges tied to transporting heavy plates.

Trade tensions remain a looming threat. In a proactive stance, POSCO is making substantial investments in downstream assets across the United States and India, strategically positioning itself to counter potential hefty import tariffs in North America. These strategic moves, combined with region-specific regulations and capacity investments, underscore the intricate dynamics shaping the abrasion wear-resistant steel plates market.

- AG der Dillinger Huttenwerke

- ArcelorMittal

- Baosteel Co., Ltd.

- Bisalloy Steel Group

- CMC (Commercial Metals Co.)

- Eckhardt Steel & Alloy

- Hbis Steel Group

- JFE Steel Corporation

- NIPPON STEEL CORPORATION

- NLMK Group

- Nucor Corporation

- POSCO India PC

- Salzgitter Mannesmann

- SIJ Slovenian Steel Group d.d.

- SSAB

- Tata Steel Nederland B.V.

- voestalpine Stahl GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand from mining and construction sectors

- 4.2.2 Regulation-driven safety and wear standards expansion

- 4.2.3 Supply-chain localisation incentives in heavy-equipment hubs

- 4.2.4 Circular-economy demand for recycled wear-plate feedstock

- 4.2.5 Digital twins enabling predictive wear optimisation

- 4.3 Market Restraints

- 4.3.1 High production costs of ultra-hardness grades

- 4.3.2 Limited fabrication and welding flexibility at HB grades greater than 500

- 4.3.3 Scarcity of skilled welders for wear-resistant alloys

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 HB 400

- 5.1.2 HB 450

- 5.1.3 HB 500

- 5.1.4 HB grades greater than 500

- 5.2 By Customer Type

- 5.2.1 OEMs

- 5.2.2 Distributors

- 5.2.3 Maintenance Contractors

- 5.2.4 Other Customer Types

- 5.3 By End-User Industry

- 5.3.1 Mining

- 5.3.2 Quarrying

- 5.3.3 Cement Industry

- 5.3.4 Construction

- 5.3.5 Recycling Industry

- 5.3.6 Other End-user Industries

- 5.4 By Plate Thickness

- 5.4.1 Thin Plates (<=10 mm)

- 5.4.2 Medium Plates (10-40 mm)

- 5.4.3 Thick Plates (more than 40 mm)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Nordic Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 AG der Dillinger Huttenwerke

- 6.4.2 ArcelorMittal

- 6.4.3 Baosteel Co., Ltd.

- 6.4.4 Bisalloy Steel Group

- 6.4.5 CMC (Commercial Metals Co.)

- 6.4.6 Eckhardt Steel & Alloy

- 6.4.7 Hbis Steel Group

- 6.4.8 JFE Steel Corporation

- 6.4.9 NIPPON STEEL CORPORATION

- 6.4.10 NLMK Group

- 6.4.11 Nucor Corporation

- 6.4.12 POSCO India PC

- 6.4.13 Salzgitter Mannesmann

- 6.4.14 SIJ Slovenian Steel Group d.d.

- 6.4.15 SSAB

- 6.4.16 Tata Steel Nederland B.V.

- 6.4.17 voestalpine Stahl GmbH

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

粗鋼市場規模、佔有率和成長分析:按製造流程、產品類型、最終用途產業和地區分類-2026-2033年產業預測

粗鋼市場規模、佔有率和成長分析:按製造流程、產品類型、最終用途產業和地區分類-2026-2033年產業預測 層壓鋼板市場:依產品、終端用途產業及地區分類

層壓鋼板市場:依產品、終端用途產業及地區分類 耐磨鋼板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

耐磨鋼板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年) 粗鋼市場:2026-2032年全球市場預測(依產品類型、鋼種、製造流程、應用、形狀及塗層分類)合金鋼市場:依產品類型、應用和地區分類

粗鋼市場:2026-2032年全球市場預測(依產品類型、鋼種、製造流程、應用、形狀及塗層分類)合金鋼市場:依產品類型、應用和地區分類 全球馬氏體時效鋼市場規模、佔有率、趨勢和成長分析報告(2026-2034年)粗鋼:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

全球馬氏體時效鋼市場規模、佔有率、趨勢和成長分析報告(2026-2034年)粗鋼:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026-2030年全球鋼鐵製造市場

2026-2030年全球鋼鐵製造市場 2026年全球鍍鋅鋼板市場研究報告

2026年全球鍍鋅鋼板市場研究報告 2026年至2034年鋼鐵市場規模、佔有率、趨勢及預測(按類型、產品類型、應用及地區分類)

2026年至2034年鋼鐵市場規模、佔有率、趨勢及預測(按類型、產品類型、應用及地區分類)