|

市場調查報告書

商品編碼

2044199

粗鋼:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Crude Steel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

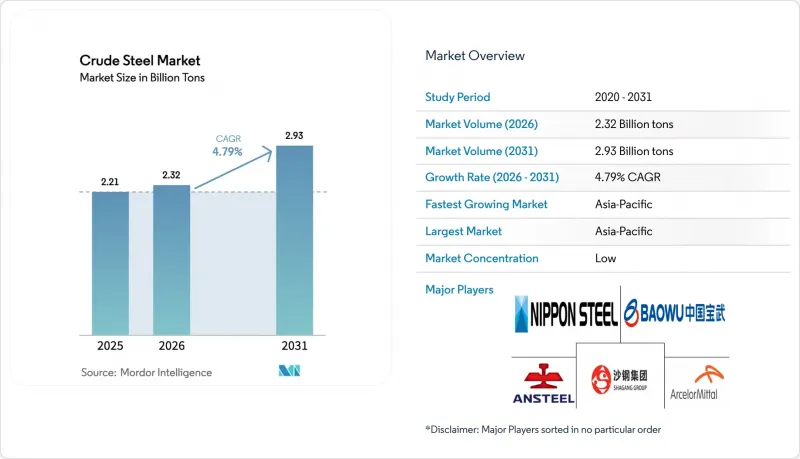

預計到 2026 年,粗鋼市場規模將達到 23.2 億噸,高於 2025 年的 22.1 億噸,預計到 2031 年將達到 29.3 億噸。

預計從 2026 年到 2031 年,其複合年成長率將達到 4.79%。

隨著更嚴格的脫碳目標、廢鋼回收系統的成熟以及再生能源價格的下降,電弧爐(EAF)技術正在取代高爐/轉爐(BOF)製程。亞太地區透過大規模城市基礎設施項目佔據了很大一部分需求,其中印度產能的擴張和東協的大型企劃正日益抵消中國房地產週期放緩的影響。從終端用戶趨勢來看,公共基礎設施和住宅佔年產量的一半以上,交通電氣化、機械現代化和可再生能源的發展都促進了產量的成長。電弧爐(EAF)投資熱潮、氫氣直接還原法試點項目以及旨在確保低碳生產系統的大規模收購正在塑造著競爭格局,這些收購是為了應對碳邊境調節稅和買方脫碳要求。因此,一體化製造商正在高爐改造、電工鋼板生產線和製程熱解決方案方面投入創紀錄的資金,以對沖未來資產擱淺和綠色溢價不確定性的風險。

全球粗鋼市場趨勢與洞察

20家主要鋼鐵製造商競相爭取與脫碳相關的資本投資

超過2000億美元已用於向低碳高爐、氫基直接還原裝置和電工鋼板生產線轉型,所有這些項目都計劃在2030年前完成。安賽樂米塔爾在阿拉巴馬州投資12億美元的電解鋼板廠和蒂森克虜伯的「tkH2Steel」計畫(旨在2030年將二氧化碳排放減少30%)凸顯了先行者的優勢。計劃於2026年初啟動的試點營運預計將證明,一旦再生能源的價格與石化燃料電力的價格持平,其成本將與傳統製造流程持平。先行者將在與渴望減少範圍3排放的汽車製造商和家電製造商的價格談判中佔據優勢,而後後進企業則將面臨高爐資產因碳關稅的加強而淪為“擱淺資產”的風險。

印度和東協建築業超級週期持續到2030年

印度計劃在2047年將粗鋼產能提升至5億噸,此目標得益於國內鐵礦石產量達到3.18億噸,為區域長材和結構鋼的蓬勃發展奠定了基礎。同時,東協其他大型企劃,例如印尼的努沙登加拉首都計畫和泰國的東部經濟走廊,總合十年將需要超過5,000萬噸的鋼鐵。以亞洲鋼鐵公司(SteelAsia)為首的區域投資者,正投資650億菲律賓披索比索建設多條電弧爐(EAF)生產線,以縮短價值鏈,並確保高附加價值加工業務的發展。持續成長依賴財政支出和外國直接投資的流入,但利率週期和原物料價格波動構成下行風險。

中國房地產市場復甦速度慢於預期。

2024年9月中國住宅銷售量較去年同期下降37.7%,進一步抑制了住宅用鋼的需求。此前,住宅用鋼需求已較2019年的尖峰時段(2.96億噸)下降了一半。因此,中國鋼廠出口增加,導致區域價格下跌,並引發貿易摩擦,尤其是在東南亞地區。需求長期下降與人口成長停滯和空置率上升有關,顯示這是一種結構性調整,而非週期性波動。

細分市場分析

到2025年,全靜鋼將佔粗鋼市場佔有率的54.18%,這反映了其在連鑄生產線中的關鍵作用,而連鑄生產線幾乎涵蓋了所有現代鋼坯生產。鋁基和矽基脫氧劑能夠抑制氣體生成,從而最大限度地減少表面孔隙率並提高成品率。隨著汽車製造商對輕量化底盤零件的化學成分偏析控制要求日益提高,預計到2031年,半鎮靜鋼的複合年成長率將達到4.9%,高於整體市場成長水準。帶底鋼和帶頂鋼仍在一些特定的板材和帶鋼應用領域繼續使用,但隨著綜合鋼廠優先考慮成品率和潔淨度,其市場佔有率正在結構性下降。

電弧爐 (EAF) 生產商正增加窯爐鋼的指定用途,以最大限度地提高合金回收率並減少返工,從而鞏固了該領域的領先地位。同時,半窯爐鋼日益受到關注,這與汽車製造商轉向需要精確微量合金元素的高級高抗張強度鋼的趨勢不謀而合。雖然監管因素對成分選擇幾乎沒有直接影響,但從能源密集生產的角度來看,鋼廠正在加快脫氧製程的最佳化和鋁添加劑的回收,以獲得經濟效益。

《粗鋼市場報告》按成分(全靜鋼鋼和半靜鋼鋼)、製造程序(轉爐煉鋼和電弧爐煉鋼)、終端用戶行業(建築、交通運輸及其他終端用戶行業)和地區(亞太地區、北美地區、歐洲地區、南美地區以及中東和非洲地區)進行細分。市場預測以噸為單位。

區域分析

預計到2025年,亞太地區將佔全球出貨量的73.52%,並在2031年之前以4.86%的複合年成長率成長。這主要得益於印度計劃將年產能擴大至5億噸,以及東南亞國協建設項目的進展。中國住宅市場放緩主導的產能過剩正日益轉向出口市場,引發了南亞和拉丁美洲的反傾銷措施。日本和韓國在政府大力補貼的支持下,正專注於生產電工鋼板和耐氫爐等特殊產品。

在北美,受《兩黨基礎設施法案》和《通膨控制法案》的影響,需求前景較為樂觀;但供應方面,重組正在進行中,主要集中在一些大型交易上,例如日本鋼鐵住友金屬以149億美元收購美國鋼鐵公司。充足的廢鋼和再生能源為擴大電弧爐(EAF)產能提供了有利條件;加拿大正在利用其水力發電網路;墨西哥隨著生產回流,正在獲得汽車用鋼的訂單。

在歐洲,能源價格飆升帶來的不利影響正透過提高能源效率、歐盟鋼鐵基金津貼以及徵收碳邊境調節稅來應對,以提升進口產品的價格競爭力。在南美、中東和非洲,基於基礎設施和資源加工廠的建設,預計鋼鐵業將實現中等個位數的成長,但由於資金籌措限制,專案儲備有限。運費上漲和供應鏈區域化(由範圍3排放計算引發)是影響全球鋼鐵廠位置和產品組合決策的通用因素。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 排名前 20 名的鋼鐵製造商在脫碳相關資本投資方面展開競爭。

- 印度和東協建築業超級週期持續到2030年

- 對輕量化汽車的需求正在恢復對高附加價值扁鋼板的需求。

- 綠氫能計畫的管道將降低長期電力成本。

- 小型模組化爐在製程加熱領域的應用迅速擴展。

- 市場限制因素

- 中國房地產市場復甦速度慢於預期。

- 貿易救濟措施的增加阻礙了跨國資本流動。

- 圍繞綠色總理的不確定性導致購電協議的簽署被推遲。

- 價值鏈分析

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭程度

- 供應分析

- 監理政策分析

- 貿易分析

- 價格趨勢分析

- 生產成本分析

第5章 市場規模和成長預測(價值和數量)

- 按成分

- 全靜鋼

- 半靜鋼

- 透過製造程序

- 鹼性氧氣轉爐(BOF)

- 電弧爐(EAF)

- 按最終用戶行業分類

- 建築/施工

- 運輸

- 工具/機器

- 能源

- 消費品

- 其他終端用戶產業

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- ArcelorMittal

- China Ansteel Group Corporation Limited

- China BaoWu Steel Group Corporation Limited

- Fangda Special Steel Technology

- HBIS Group

- Hunan Valin Iron and Steel Co., Ltd.

- Hyundai Steel

- JFE Steel Corporation

- Jiangsu Shagang Group

- JSW

- Nippon Steel Corporation

- NLMK Group

- Nucor Corporation

- POSCO HOLDINGS

- Rizhao Steel Holding Group CO., LTD.

- SAIL

- Tata Steel

- Techint Group

- United States Steel Corporation

第7章 市場機會與未來展望

Crude Steel market size in 2026 is estimated at 2.32 billion tons, growing from 2025 value of 2.21 billion tons with 2031 projections showing 2.93 billion tons, growing at 4.79% CAGR over 2026-2031.

Electric-arc-furnace (EAF) technology is steadily displacing blast-furnace/basic-oxygen-furnace (BOF) routes as decarbonization targets tighten, scrap collection systems mature, and renewable electricity becomes more affordable. Asia-Pacific commands the bulk of demand through large-scale urban infrastructure programs, while India's capacity expansion and ASEAN mega-projects increasingly counterbalance China's easing property cycle. End-user trends show public infrastructure and housing absorbing more than half of annual volume, with transportation electrification, machinery upgrades, and renewable-energy build-outs adding incremental tonnage. Competitive dynamics are shaped by a wave of EAF investments, hydrogen-based direct-reduction pilots, and headline acquisitions that aim to secure low-carbon production footprints in anticipation of carbon-border levies and buyer decarbonization mandates. Integrated producers therefore channel record capital into furnace conversions, electrical-steel lines, and process-heat solutions to hedge against future asset stranding and green-premium uncertainty.

Global Crude Steel Market Trends and Insights

Decarbonization-Linked Capex Race Among Top 20 Steelmakers

More than USD 200 billion has been earmarked for low-carbon furnace conversions, hydrogen-based direct-reduction units, and electrical-steel lines scheduled for completion before 2030. ArcelorMittal's USD 1.2 billion electrical-steel plant in Alabama and thyssenkrupp's tkH2Steel program targeting a 30% CO2 cut by 2030 highlight the first-mover premium. Pilot operations scheduled for early 2026 are expected to validate cost parity with conventional routes once renewable electricity prices converge with fossil alternatives. Early adopters gain price-negotiation leverage with automotive and appliance buyers eager to shrink Scope 3 emissions, while late movers risk stranded blast-furnace assets under tightening carbon-border taxes.

Construction Super-Cycle in India and ASEAN Through 2030

India's target of boosting installed crude-steel capacity to 500 million tons by 2047 anchors a regional boom in long and structural steel, underpinned by domestic iron-ore output that rose to 318 million tons in 2025. Parallel ASEAN megaprojects-such as Indonesia's Nusantara capital and Thailand's Eastern Economic Corridor-collectively require more than 50 million tons in the current decade. Regional investors led by SteelAsia are deploying PHP 65 billion across multiple EAF lines to shorten supply chains and capture value-added fabrication. Sustained growth rests on continued fiscal spending and foreign-direct-investment inflows, although interest-rate cycles and raw-material price swings pose downside risk.

Slower-Than-Expected Chinese Real-Estate Recovery

Monthly new-home sales in China fell 37.7% year-on-year in September 2024, trimming residential-steel demand that had already halved from its 2019 peak of 296 million tons. The resulting export push by Chinese mills depresses regional prices and sparks trade friction, particularly in Southeast Asia. Long-term demand destruction is tied to demographic plateauing and higher vacancy rates, pointing to a structural rather than cyclical adjustment.

Other drivers and restraints analyzed in the detailed report include:

- Automotive Lightweighting Push Reviving Value-Added Flat Steel

- Green-Hydrogen Project Pipelines Lowering Long-Run Power Cost

- Trade-Remedy Proliferation Hampering Cross-Border Flows

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Killed steel captured 54.18% of the crude steel market share in 2025, reflecting its indispensability to continuous casting lines that account for nearly all modern slab production. Aluminum and silicon deoxidizers suppress gas evolution, which minimizes surface voids and improves yield. Semi-killed grades are expected to outpace overall growth at a 4.9% CAGR through 2031 as automakers seek controlled chemical segregation for lightweight chassis components. Rimmed and capped steels continue to serve niche sheet and strip use cases but remain in structural decline as integrated mills prioritize yield and cleanliness.

EAF operators increasingly specify killed grades to maximize alloy recovery and reduce rework, reinforcing the segment's predominance. Meanwhile, semi-killed steel's rising profile aligns with automakers' transition to advanced high-strength steels requiring precise micro-alloying. Regulatory factors exert minimal direct influence on composition choice, though energy-intensity considerations encourage mills to streamline deoxidation practices and recover aluminum additions for economic gain.

The Crude Steel Market Report is Segmented by Composition (Killed Steel and Semi-Killed Steel), Manufacturing Process (Basic Oxygen Furnace (BOF) and Electric Arc Furnace (EAF)), End-User Industry (Building and Construction, Transportation, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific accounted for 73.52% of 2025 shipments and is projected to grow at 4.86% CAGR to 2031, supported by India's planned scale-up to 500 million tons of annual capacity and ASEAN construction pipelines. China's housing-driven soft patch generates a surplus that increasingly targets export markets, prompting anti-dumping actions across South Asia and Latin America. Japan and South Korea shift focus to electrical-steel specialisms and hydrogen-ready furnaces backed by strong governmental subsidies.

North America's demand outlook brightens under the Bipartisan Infrastructure Law and the Inflation Reduction Act, though the region's supply side is consolidating around headline deals such as Nippon Steel's USD 14.9 billion take-over of U.S. Steel. Abundant scrap and renewable electricity create fertile ground for EAF capacity, with Canada leveraging hydro-powered grids and Mexico capturing reshoring-induced auto-steel orders.

Europe combats energy-price headwinds via efficiency upgrades, EU steel fund grants, and carbon-border tariffs aimed at leveling imports. South America and Middle East-Africa present mid-single-digit growth rooted in infrastructure and resource-processing plants, though financing constraints limit project pipelines. Regionalization of supply chains, triggered by freight-cost inflation and Scope 3 accounting, is a unifying theme influencing mill location and product-mix decisions worldwide.

- ArcelorMittal

- China Ansteel Group Corporation Limited

- China BaoWu Steel Group Corporation Limited

- Fangda Special Steel Technology

- HBIS Group

- Hunan Valin Iron and Steel Co., Ltd.

- Hyundai Steel

- JFE Steel Corporation

- Jiangsu Shagang Group

- JSW

- Nippon Steel Corporation

- NLMK Group

- Nucor Corporation

- POSCO HOLDINGS

- Rizhao Steel Holding Group CO., LTD.

- SAIL

- Tata Steel

- Techint Group

- United States Steel Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Decarbonisation-Linked Capex Race Among Top 20 Steelmakers

- 4.2.2 Construction Super-Cycle in India and ASEAN Through 2030

- 4.2.3 Automotive Lightweighting Push Reviving Value-Added Flat Steel

- 4.2.4 Green-Hydrogen Project Pipelines Lowering Long-Run Power Cost

- 4.2.5 Rapid Build-Out of Small Modular Reactors for Process Heat

- 4.3 Market Restraints

- 4.3.1 Slower-Than-Expected Chinese Real-Estate Recovery

- 4.3.2 Trade-Remedy Proliferation Hampering Cross-Border Flows

- 4.3.3 Green-Premia Uncertainty Delaying Offtake Agreements

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

- 4.6 Supply Analysis

- 4.7 Regulatory Policy Analysis

- 4.8 Trade Analysis

- 4.9 Price Trend Analysis

- 4.10 Production Cost Analysis

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Composition

- 5.1.1 Killed Steel

- 5.1.2 Semi-killed Steel

- 5.2 By Manufacturing Process

- 5.2.1 Basic Oxygen Furnace (BOF)

- 5.2.2 Electric Arc Furnace (EAF)

- 5.3 By End-user Industry

- 5.3.1 Building and Construction

- 5.3.2 Transportation

- 5.3.3 Tools and Machinery

- 5.3.4 Energy

- 5.3.5 Consumer Goods

- 5.3.6 Other End-user Industries

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Russia

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ArcelorMittal

- 6.4.2 China Ansteel Group Corporation Limited

- 6.4.3 China BaoWu Steel Group Corporation Limited

- 6.4.4 Fangda Special Steel Technology

- 6.4.5 HBIS Group

- 6.4.6 Hunan Valin Iron and Steel Co., Ltd.

- 6.4.7 Hyundai Steel

- 6.4.8 JFE Steel Corporation

- 6.4.9 Jiangsu Shagang Group

- 6.4.10 JSW

- 6.4.11 Nippon Steel Corporation

- 6.4.12 NLMK Group

- 6.4.13 Nucor Corporation

- 6.4.14 POSCO HOLDINGS

- 6.4.15 Rizhao Steel Holding Group CO., LTD.

- 6.4.16 SAIL

- 6.4.17 Tata Steel

- 6.4.18 Techint Group

- 6.4.19 United States Steel Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

粗鋼市場-2026-2032年全球市場預測

粗鋼市場-2026-2032年全球市場預測 2026年全球高磁感應強度定向矽鋼市場報告

2026年全球高磁感應強度定向矽鋼市場報告 液壓鋼骨加工機械市場規模、佔有率和成長分析:按噸位、工作站配置、工作站類型、驅動系統、最終用途產業和地區分類-2026-2033年產業預測

液壓鋼骨加工機械市場規模、佔有率和成長分析:按噸位、工作站配置、工作站類型、驅動系統、最終用途產業和地區分類-2026-2033年產業預測 耐磨鋼板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

耐磨鋼板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年) 粗鋼市場規模、佔有率和成長分析:按製造流程、產品類型、最終用途產業和地區分類-2026-2033年產業預測

粗鋼市場規模、佔有率和成長分析:按製造流程、產品類型、最終用途產業和地區分類-2026-2033年產業預測 層壓鋼板市場:依產品、終端用途產業及地區分類耐磨鋼板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)合金鋼市場:依產品類型、應用和地區分類

層壓鋼板市場:依產品、終端用途產業及地區分類耐磨鋼板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)合金鋼市場:依產品類型、應用和地區分類 全球馬氏體時效鋼市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球馬氏體時效鋼市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026-2030年全球鋼鐵製造市場

2026-2030年全球鋼鐵製造市場