|

市場調查報告書

商品編碼

2073013

零售和電子商務領域的IT永續發展軟體:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031年)Retail and E-Commerce IT Sustainability Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

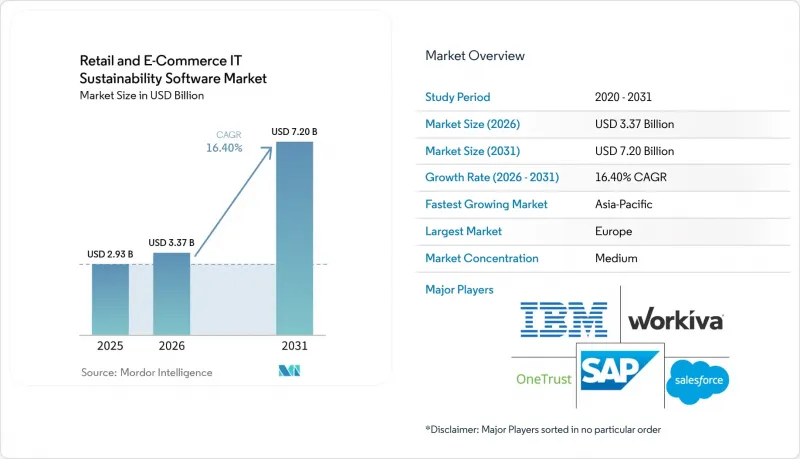

根據 Mordor Intelligence 預測,零售和電子商務 IT 永續性軟體的市場規模預計將從 2025 年的 29.3 億美元和 2026 年的 33.7 億美元成長到 2031 年的 72 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 16.40%。

本報告按交付方式(軟體和服務)、部署方式(雲端、混合等)、企業規模(大型企業和中小企業)、功能(碳計量和排放管理軟體、永續發展報告和揭露軟體等)以及地區進行細分。市場預測以價值(美元)表示。

全球零售及電子商務IT永續發展軟體市場趨勢及洞察

ESG資訊揭露與審計回應的監管合規性

在多個零售市場,監管揭露要求正迅速從自願報告轉向具有法律約束力的合規性,這項變革正在加速零售和電商IT永續發展軟體市場的平台採購。在歐洲,與《消費者權益保護指令》(CSRD)相關的修訂於2026年3月生效,維持了大型企業符合環境和社會報告準則(ESRS)的報告義務,從而維持了對基於結構化、可重複報告工作流程的資訊揭露系統的需求。下一個壓力來自消費者導向的環境聲明,因為《消費者權利指令》(CEMD)於2026年9月27日生效,其監管範圍從年度報告擴展到零售商和電商業者使用的產品頁面、包裝和運輸資訊。同樣在印度,針對大型上市公司的《商業報告準則》(BRSR)核心保證要求在2026-27會計年度進行了擴展,進一步加重了零售集團及其合作夥伴供應商的審計相關報告負擔。因此,零售和電商領域的IT永續發展軟體市場更青睞那些支援多種框架、維護文件追蹤記錄,即使同一零售商需要同時滿足不同的報告要求也能產生可用輸出的平台。依賴單一框架配置的供應商可能會減緩軟體的普及速度,因為零售商越來越需要能夠適應監管變化而無需重新實施的系統。

零售商面臨著證明其產品範圍 3 的完整性和環境足跡的壓力。

零售和電商領域的IT永續軟體市場正受益於消費者期望的直接變化,因為零售商現在需要產品層面和供應商層面的證據來支持其範圍3的計算和永續性聲明。由於許多零售價值鏈中下游供應商的透明度仍然較低,商業挑戰不僅在於收集數據,還在於從那些將上游關係視為機密的供應商那裡獲取可靠數據。 2026年2月,Worldly將其產品影響計算器擴展到涵蓋260多個消費品類別的40萬種產品,這表明產品層面的範圍3建模正從有限的試點階段過渡到更廣泛的營運階段。這項轉變意義重大,因為零售商需要原始供應商資料和商品層面的記錄,以便在數位產品護照義務開始影響特定類別之前很久就能證實其聲明的合法性。因此,在零售和電商領域的IT永續性軟體市場中,能夠檢驗、標準化和整合來自二級和三級供應商的輸入資訊的供應商比僅依賴估計值的供應商更受重視。高價合約正在從僅僅粗略計算碳足跡轉向提供工具,幫助零售商在審計和客戶評價期間佐證產品聲明。

ERP、PIM、POS 和供應鏈系統之間的高整合成本。

零售和電商領域的IT永續發展軟體市場仍面臨許多挑戰。其中包括將永續發展平台與零售商已用於產品、貿易、供應商、庫存和物流的系統連接起來的成本。許多全通路零售商經營5-7個關鍵的企業系統,如果資料模型不一致,協調這些環境的成本可能接近軟體授權本身的價值。雖然雲端技術的普及改善了底層基礎設施,但並未消除跨供應商生態系統進行API標準化和資料結構協調所需的工作。 SAP更新的2026年永續發展控制塔藍圖強調了嵌入式報告功能和廣泛的ERP連接的重要性,這反映出買家仍然非常重視能夠從源頭上減輕整合負擔的系統。這種負擔在中型企業市場最為嚴重,因為傳統架構和小規模部署團隊會導致更長的引進週期和合規性實現的延遲。隨著供應商開始提供認證連接器和預先建置的零售工作流程,消除每個階段的客製化整合需求,零售和電商領域的IT永續發展軟體市場預計將會加速發展。

細分市場分析

2025年,軟體在零售和電商IT永續發展軟體市場中佔了69.45%的佔有率。這證實了平台層在碳計量、ESG資訊揭露、供應鏈分析和情境建模等領域的支出仍然至關重要。這種集中度源自於大型零售商首先需要一個管治的“記錄系統”,然後才能向供應商索取資料、建立資訊揭露文件或在多個業務部門推廣永續發展計畫。軟體層也與企業採購的早期階段相吻合,當時零售商優先考慮平台選擇、內部資料結構和報告管理,而非長期營運服務。從這個意義上講,零售和電商IT永續發展軟體市場遵循了以往企業軟體週期中的模式,即底層平台吸引了第一波預算分配。然而,軟體在早期階段佔據主導並不意味著服務就處於次要地位,因為下一階段的買家需求將越來越關注部署品質、審計支援和跨系統配置。

預計2026年至2031年間,服務市場將以16.92%的複合年成長率成長,顯示零售和電商領域的IT永續發展軟體市場正從授權模式轉向日常營運模式。希望擺脫以電子表格主導的ESG工作流程的零售商,通常需要資料遷移、連接器設定、管治設計以及初始彙報週期等方面的支持,才能自信地利用平台。隨著合規框架的不斷發展,零售商需要定期更新其工作流程邏輯、控制措施和文件標準,這增加了他們對持續支援的需求。 Workiva在多框架報告和自動化方面的優勢清晰地表明,隨著客戶從初始部署過渡到定期報告週期,為何將軟體與綜合服務結合的供應商具有優勢。因此,零售和電商領域的IT永續發展軟體產業正在轉型為一個更加注重關係的市場,託管支援和諮詢服務在合約續約和提升銷售決策中發揮著越來越重要的作用。隨著時間的推移,那些在其平台之外建立高度擴充性服務團隊的供應商,更有可能在持續的合規相關支出中佔據更大的佔有率。

預計到2025年,雲端採用率將佔市場佔有率的66.12%,反映出SaaS交付與現代零售商和電子商務企業採用的分散式營運模式高度契合。雲端系統易於跨國家、業務部門和報告團隊擴展,並能快速適應揭露範本、包裝規則或報告邏輯的變化。因此,對於希望建立跨國報告系統而無需等待長期本地基礎設施項目的零售商而言,雲端已成為切實可行的首選。雲端在零售和電商IT永續發展軟體市場持續佔據領先地位,因為企業負責人仍優先考慮集中管理、降低維護負擔以及輕鬆取得新功能。然而,當供應商記錄、自有品牌資料或特定司法管轄區的管治要求需要更嚴格的資料管理時,僅靠雲端並不總是足夠。

混合部署預計將在2026年至2031年間以16.78%的複合年成長率成長,這表明企業買家越來越傾向於柔軟性而非「非此即彼」的架構。零售商可以利用雲端來擴展報告和協作,同時將商業性敏感記錄保留在管治的本地或內部環境中。 SAP 對其永續發展控制塔的2026年更新凸顯了這種模式日益成長的受歡迎程度。該公司強調了可審計的報告、人工智慧支援以及對各種ERP環境的廣泛覆蓋,而不是狹隘的單一堆堆疊配置。在零售和電子商務的IT永續發展軟體市場,混合部署的擴展也推動了相關服務需求的成長。這是因為零售商需要跨系統的中間件、編配和受控資料處理歷程。未來,對於既需要擴展報告又需要嚴格控制敏感供應商資訊的大規模全通路營運商而言,混合模式很可能成為最具吸引力的選擇。沒有可靠混合方案的供應商或許在較簡單的用例中仍然具有價值,但在更複雜的企業專案中可能面臨失去訂單的風險。

區域分析

2025年,歐洲佔據了零售和電商IT永續發展軟體市場34.56%的佔有率,成為同期最大的區域收入貢獻者。這一區域地位主要得益於眾多永續發展法規的存在,這些法規同時影響零售報告、包裝義務以及面向消費者的環境聲明。 2026年,與《企業永續性報告指令》(CSRD)相關的變更持續推進,而《包裝和包裝廢棄物法規》和《消費者權利指令》則加大了營運壓力,涵蓋了從年度報告到產品溝通和電商標籤等各個方面。在英國,對誤導性環境聲明的審查力度加大,持續推動了市場需求,同時,服務於歐洲消費者的零售商在管治和文件方面的要求仍然很高。在此背景下,零售和電商IT永續發展軟體市場的規模不僅得益於大型跨國公司,也得益於那些必須滿足因與客戶和供應商關係而產生的合規要求的中型企業。

預計2026年至2031年,亞太地區將以17.12%的複合年成長率成長,成為零售和電子商務領域IT永續發展軟體市場成長最快的地區。這一成長得益於包括日本、澳洲、韓國、新加坡、中國和印度在內的多個主要經濟體在2025年至2027年間幾乎同步實施符合ISSB標準或擴展後的永續發展資訊揭露要求。此外,由於該地區是許多全球零售供應鏈的重要生產中心,因此對軟體的需求不僅受到國內上市公司監管的驅動,也受到出口依賴和主導對供應商的要求的影響。這種雙重壓力正在亞太地區創造更廣泛的應用基礎,因為製造商、採購合作夥伴和零售集團都被整合到同一合規資料鏈中。

北美在零售和電商IT永續發展軟體市場仍具有重要的商業性地位,即便其市場佔有率和成長率並非該地區最高。 2026年,在聯邦層級不確定性日益加劇的情況下,加州的氣候資訊揭露框架依然至關重要,推動了在該州營運的大型零售商對軟體的持續需求。南美洲是零售和電商IT永續發展軟體市場中規模較小但同樣活躍的地區,尤其是在巴西,企業越來越關注與出口相關的永續發展預期以及遵守當地的報告規範。 SAP於2025年底將其永續發展足跡管理(Sustainability Footprint Management)擴展到巴西聖保羅AWS區域,正反映了對本地最佳化碳計量基礎設施日益成長的需求。在中東,隨著大型零售集團和國家永續發展政策推動更完善的ESG資料基礎設施的發展,人們對該領域的興趣也日益濃厚。另一方面,非洲仍處於起步階段,目前主要集中在出口導向上市公司。在全部區域,零售和電子商務的 IT 永續性軟體市場正在擴大,但其普及速度仍然很大程度上取決於監管執行的嚴格程度以及大型零售商在多大程度上確保將數據要求納入其供應商合約中。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- ESG資訊揭露與審計回應的監管合規性

- 零售商面臨著證明其產品範圍 3 的完整性和碳足跡的壓力。

- 從基於電子表格的工作流程遷移到企業永續發展資料平台

- 人工智慧驅動的永續發展報告和異常檢測

- 全通路零售的日益複雜化正在推動可追溯性的需求。

- 供應商評分卡在永續採購和自有品牌風險管理的應用

- 市場限制因素

- ERP、PIM、POS 和供應鏈系統整合成本高。

- 二級和三級供應商網路中供應商資料的分散化和可追溯性差。

- 零售業永續發展分析師與ESG管理階層短缺

- 報告標準的變更需要進行重組和合規措施審查。

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 報價

- 軟體

- 服務

- 不同的發展

- 雲

- 現場

- 混合

- 按公司規模

- 大公司

- 小型企業

- 功能性別

- 碳計量與排放管理軟體

- 永續發展報告及揭露軟體

- 供應鏈中的ESG和供應商永續管理

- 永續性分析、預測和情境建模

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- SAP SE

- Salesforce, Inc.

- IBM Corporation

- Workiva Inc.

- OneTrust, LLC

- Diligent Corporation

- EcoVadis SAS

- Sphera Solutions, Inc.

- Enablon SA

- Intelex Technologies ULC

- Cority Software Inc.

- Persefoni AI, Inc.

- Novisto Inc.

- Greenstone Limited

- Datamaran Limited

- Benchmark Digital Partners LLC

- UL LLC

- Wolters Kluwer NV

- Watershed

- Position Green

第7章 市場機會與未來展望

According to Mordor Intelligence, the retail and e-commerce IT sustainability software market size is projected to expand from USD 2.93 billion in 2025 and USD 3.37 billion in 2026 to USD 7.20 billion by 2031, registering a CAGR of 16.40% between 2026 and 2031.

This report is Segmented by Offering (Software, and Services), Deployment (Cloud, Hybrid, and More), Enterprise Size (Large Enterprises, and Small and Medium-Sized Enterprises), Functionality (Carbon Accounting and Emissions Management Software, Sustainability Reporting and Disclosure Software, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Retail and E-Commerce IT Sustainability Software Market Trends and Insights

Regulatory Compliance for ESG Disclosure and Audit Readiness

Regulatory disclosure requirements have moved from voluntary reporting into binding compliance across several retail markets within a short period, and that shift is accelerating platform purchases in the retail and e-commerce IT sustainability software market. In Europe, CSRD-related amendments entered into force in March 2026 and maintained ESRS-aligned reporting obligations for large in-scope companies, thereby preserving demand for disclosure systems built on structured, repeatable reporting workflows. The next layer of pressure comes from consumer-facing environmental claims, as the Empowering Consumers Directive takes effect on September 27, 2026, and extends scrutiny from annual reports to product pages, packaging, and delivery communications used by retailers and e-commerce operators. India also expanded BRSR Core assurance requirements for large listed companies for the fiscal year 2026-27, which adds another audit-driven reporting burden for retail groups and suppliers tied to those issuers. As a result, the retail and e-commerce IT sustainability software market is favoring platforms that can support multiple frameworks, preserve documentation trails, and produce outputs that remain usable when the same retailer must satisfy different reporting regimes simultaneously. Vendors that rely on single-framework configurations face slower adoption, as retailers increasingly need systems that can absorb regulatory changes without restarting implementation work.

Retailer Pressure to Prove Scope 3 and Product Footprint Integrity

The retail and e-commerce IT sustainability software market is benefiting from a direct shift in buyer expectations, as retailers now need product- and supplier-level evidence to support Scope 3 accounting and sustainability claims. Lower-tier supplier visibility remains weak across many retail value chains, so the commercial problem is not only collecting data but also securing reliable data from suppliers that view their upstream relationships as sensitive. Worldly expanded its Product Impact Calculator to 400,000 products across more than 260 consumer goods categories in February 2026, which shows that product-level Scope 3 modeling is moving beyond narrow pilots and into broader operational use. That change matters because retailers need primary supplier data and defensible item-level records well before Digital Product Passport obligations begin affecting selected categories. The retail and e-commerce IT sustainability software market is, therefore, rewarding vendors that can validate, normalize, and link Tier 2 and Tier 3 supplier inputs rather than relying solely on broad spend-based estimates. Premium contract value is shifting toward tools that help retailers defend product claims during audits and customer reviews, not just calculate a high-level carbon footprint.

High Integration Cost Across ERP, PIM, POS, and Supply Chain Systems

The retail and e-commerce IT sustainability software market still faces a significant barrier: the cost of connecting sustainability platforms to the systems retailers already use for products, transactions, suppliers, inventory, and logistics. Many omnichannel retailers operate across 5 to 7 major enterprise systems, and the cost of linking those environments can approach the value of the software license itself when data models do not align. Stronger cloud adoption has improved baseline infrastructure, but it has not removed the work needed to standardize APIs and reconcile data structures across vendor ecosystems. SAP's 2026 roadmap updates for Sustainability Control Tower also highlighted the importance of embedded reporting and broad ERP connectivity, which reflects how much buyers still value systems that reduce integration effort at the source. This burden is heaviest in the mid-market, where legacy architecture and smaller implementation teams lengthen deployment cycles and delay compliance gains. The retail and e-commerce IT sustainability software market is likely to see faster adoption as vendors offer certified connectors and prebuilt retail workflows, rather than requiring custom integration at each step.

Other drivers and restraints analyzed in the detailed report include:

- Shift From Spreadsheet Workflows to Enterprise Sustainability Data Platforms

- AI-Enabled Sustainability Reporting and Exception Detection

- Fragmented Supplier Data and Low Traceability in Tier 2 and Tier 3 Networks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 69.45% of the retail and e-commerce IT sustainability software market in 2025, which confirmed that the platform layer remained the center of spending across carbon accounting, ESG disclosure, supply chain analytics, and scenario modeling. This concentration developed because large retailers first needed a governed system of record before they could scale supplier data requests, disclosure preparation, or sustainability planning across multiple business units. The software layer also aligns with the first phase of enterprise buying, where retailers prioritized platform selection, internal data structure, and reporting controls over longer-term operational services. In that sense, the retail and e-commerce IT sustainability software market followed a pattern seen in earlier enterprise software cycles, where foundational platforms attracted the first wave of budget allocation. Even so, the early software lead does not mean services are secondary, because the next stage of buyer demand is increasingly focused on implementation quality, audit support, and cross-system configuration.

Services are projected to grow at a 16.92% CAGR from 2026 to 2031, indicating that the retail and e-commerce IT sustainability software market is shifting from license acquisition to everyday operational use. Retailers moving away from spreadsheet-led ESG workflows often need support for data migration, connector setup, governance design, and first-cycle reporting before they can rely on the platform with confidence. The need for recurring support is also rising as compliance frameworks continue to evolve, requiring retailers to regularly update workflow logic, controls, and documentation standards. Workiva's strength in multi-framework reporting and automation illustrates why providers that pair software with service depth are positioned well as customers move from initial deployment into repeat reporting cycles. The retail and e-commerce IT sustainability software industry is therefore becoming more relationship-driven, with managed support and advisory execution playing a larger role in renewal and upsell decisions. Vendors that build scalable services teams alongside the platform are likely to capture a greater share of recurring compliance spending over time.

Cloud deployment captured a 66.12% share in 2025, reflecting the strong fit between SaaS delivery and the distributed operating model used by modern retailers and e-commerce groups. Cloud systems are easier to scale across countries, business units, and reporting teams, and they support faster updates when disclosure templates, packaging rules, or reporting logic change. That made cloud a practical first choice for retailers looking to set up multi-country reporting without waiting for lengthy local infrastructure projects. The retail and e-commerce IT sustainability software market size for cloud remained ahead because enterprise buyers still value centralized administration, lower maintenance burden, and easier access to new features. At the same time, pure cloud is not always sufficient when supplier records, private-label data, or jurisdiction-specific governance requirements require tighter data control.

Hybrid deployment is projected to expand at a 16.78% CAGR from 2026 to 2031, which signals that enterprise buyers increasingly want flexibility rather than an all-or-nothing architecture. Retailers can use the cloud for reporting scale and collaboration while keeping commercially sensitive records in governed, local, or on-premises environments. SAP's 2026 Sustainability Control Tower updates showed why this model is gaining traction: the company emphasized audit-ready reporting, AI support, and broader coverage across different ERP environments rather than a narrow, single-stack setup. The retail and e-commerce IT sustainability software market is also seeing adjacent service demand rise as hybrid adoption increases, since retailers need middleware, orchestration, and controlled data lineage across systems. Over time, hybrid will appeal most to large omnichannel operators that need both reporting scale and tighter handling of supplier-sensitive information. Vendors without credible hybrid options may remain relevant in simpler use cases, but they risk losing more complex enterprise programs.

Complete Report Scope:

- By Offering

- Software

- Services

- By Deployment

- Cloud

- On-Premises

- Hybrid

- By Enterprise Size

- Large Enterprises

- Small and Medium-Sized Enterprises

- By Functionality

- Carbon Accounting and Emissions Management Software

- Sustainability Reporting and Disclosure Software

- Supply Chain ESG and Supplier Sustainability Management

- Sustainability Analytics, Forecasting and Scenario Modeling

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

Europe accounted for 34.56% of the retail and e-commerce IT sustainability software market in 2025, making it the leading regional contributor to revenue during the period. The region's position stems from the density of sustainability rules that affect retail reporting, packaging obligations, and consumer-facing environmental claims simultaneously. CSRD-related changes remained active in 2026, while the Packaging and Packaging Waste Regulation and the Empowering Consumers Directive added operational pressure that extends from annual reporting into product communication and e-commerce presentation. The United Kingdom also continued to shape demand by tightening oversight of misleading environmental claims, which kept governance and documentation requirements high for retailers serving European consumers. Within this setting, the retail and e-commerce IT sustainability software market size remains supported not only by large multinationals but also by mid-market operators that must respond to compliance expectations flowing through their customer and supplier relationships.

Asia-Pacific is projected to grow at a 17.12% CAGR from 2026 to 2031, which makes it the fastest-growing region in the retail and e-commerce IT sustainability software market. Growth is being supported by a near-concurrent rollout of ISSB-aligned or expanded sustainability disclosure requirements across several major economies, including Japan, Australia, South Korea, Singapore, China, and India, during the 2025 to 2027 window. The region's role as the main production base for many global retail supply chains also means software demand is driven by export exposure and retailer-led supplier requests, not solely by domestic listed company regulation. That dual pressure gives Asia-Pacific a broader adoption base, as manufacturers, sourcing partners, and retail groups are drawn into the same compliance data chain.

North America remains commercially important, even though the retail and e-commerce IT sustainability software market is not the regional leader in either share or growth rate. California's climate disclosure pathway continued to matter in 2026, even as federal uncertainty increased, helping preserve software demand among large retailers doing business in the state. South America is a smaller but active part of the retail and e-commerce IT sustainability software market, with Brazil standing out as a region where companies align with export-linked sustainability expectations and local reporting practices. SAP's extension of Sustainability Footprint Management into the Brazil Sao Paulo AWS region in late 2025 reflected this growing demand for localized carbon accounting infrastructure. The Middle East is seeing rising interest as large retail groups and national sustainability agendas push for better ESG data infrastructure, while Africa remains earlier stage, with adoption centered on export-oriented and listed entities. Across these geographies, the retail and e-commerce IT sustainability software market is expanding in scope, but adoption speed still depends heavily on the strength of regulatory enforcement and on how firmly large retailers embed data requirements in supplier contracts.

- SAP SE

- Salesforce, Inc.

- IBM Corporation

- Workiva Inc.

- OneTrust, LLC

- Diligent Corporation

- EcoVadis SAS

- Sphera Solutions, Inc.

- Enablon SA

- Intelex Technologies ULC

- Cority Software Inc.

- Persefoni AI, Inc.

- Novisto Inc.

- Greenstone Limited

- Datamaran Limited

- Benchmark Digital Partners LLC

- UL LLC

- Wolters Kluwer N.V.

- Watershed

- Position Green

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory Compliance for ESG Disclosure and Audit Readiness

- 4.2.2 Retailer Pressure to Prove Scope 3 and Product Footprint Integrity

- 4.2.3 Shift From Spreadsheet Workflows to Enterprise Sustainability Data Platforms

- 4.2.4 AI-Enabled Sustainability Reporting and Exception Detection

- 4.2.5 Omnichannel Retail Complexity Increasing Traceability Demand

- 4.2.6 Supplier Scorecarding for Sustainable Procurement and Private Label Risk Control

- 4.3 Market Restraints

- 4.3.1 High Integration Cost Across ERP, PIM, POS, and Supply Chain Systems

- 4.3.2 Fragmented Supplier Data and Low Traceability in Tier 2 and Tier 3 Networks

- 4.3.3 Shortage of Retail Sustainability Analytics Talent and ESG Control Owners

- 4.3.4 Reporting Standard Volatility Causing Reconfiguration and Compliance Rework

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-Sized Enterprises

- 5.4 By Functionality

- 5.4.1 Carbon Accounting and Emissions Management Software

- 5.4.2 Sustainability Reporting and Disclosure Software

- 5.4.3 Supply Chain ESG and Supplier Sustainability Management

- 5.4.4 Sustainability Analytics, Forecasting and Scenario Modeling

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Salesforce, Inc.

- 6.4.3 IBM Corporation

- 6.4.4 Workiva Inc.

- 6.4.5 OneTrust, LLC

- 6.4.6 Diligent Corporation

- 6.4.7 EcoVadis SAS

- 6.4.8 Sphera Solutions, Inc.

- 6.4.9 Enablon SA

- 6.4.10 Intelex Technologies ULC

- 6.4.11 Cority Software Inc.

- 6.4.12 Persefoni AI, Inc.

- 6.4.13 Novisto Inc.

- 6.4.14 Greenstone Limited

- 6.4.15 Datamaran Limited

- 6.4.16 Benchmark Digital Partners LLC

- 6.4.17 UL LLC

- 6.4.18 Wolters Kluwer N.V.

- 6.4.19 Watershed

- 6.4.20 Position Green

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

全球人工智慧資料中心市場分析與預測(2026-2032):技術、基礎設施、部署與營運趨勢

全球人工智慧資料中心市場分析與預測(2026-2032):技術、基礎設施、部署與營運趨勢 亞太地區人工智慧(AI)最佳化資料中心:市場佔有率分析、產業趨勢與統計及成長預測(2025-2030 年)

亞太地區人工智慧(AI)最佳化資料中心:市場佔有率分析、產業趨勢與統計及成長預測(2025-2030 年) 資料中心銅纜市場規模、佔有率和趨勢分析報告:按應用、類型、地區和細分市場分類(2026-2033 年)

資料中心銅纜市場規模、佔有率和趨勢分析報告:按應用、類型、地區和細分市場分類(2026-2033 年) 資料中心基礎設施最佳化:市場規模、溫度控管與能源消耗 - 市場數據概覽(2026 年第二季)人工智慧資料中心市場:全球產業分析、市場規模、市場佔有率及2026年至2033年預測(按服務產品、資料中心類型、部署模式、應用、最終用戶、國家和地區分類)

資料中心基礎設施最佳化:市場規模、溫度控管與能源消耗 - 市場數據概覽(2026 年第二季)人工智慧資料中心市場:全球產業分析、市場規模、市場佔有率及2026年至2033年預測(按服務產品、資料中心類型、部署模式、應用、最終用戶、國家和地區分類) 2026年全球網路基礎設施即代碼(IaC)市場報告

2026年全球網路基礎設施即代碼(IaC)市場報告 2026-2030年全球人工智慧資料中心市場

2026-2030年全球人工智慧資料中心市場 全球人工智慧資料中心市場:按產品/服務、資料中心類型、部署方式、應用領域、最終用戶和地區分類-預測至2032年

全球人工智慧資料中心市場:按產品/服務、資料中心類型、部署方式、應用領域、最終用戶和地區分類-預測至2032年 全球人工智慧資料中心市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球人工智慧資料中心市場:市場規模、佔有率和趨勢分析(按組件、資料中心類型、部署方式、人工智慧應用領域、產業和地區分類),細分市場預測(2026-2033 年)

全球人工智慧資料中心市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球人工智慧資料中心市場:市場規模、佔有率和趨勢分析(按組件、資料中心類型、部署方式、人工智慧應用領域、產業和地區分類),細分市場預測(2026-2033 年)