|

市場調查報告書

商品編碼

2072844

中國醫藥物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)China Pharmaceutical Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

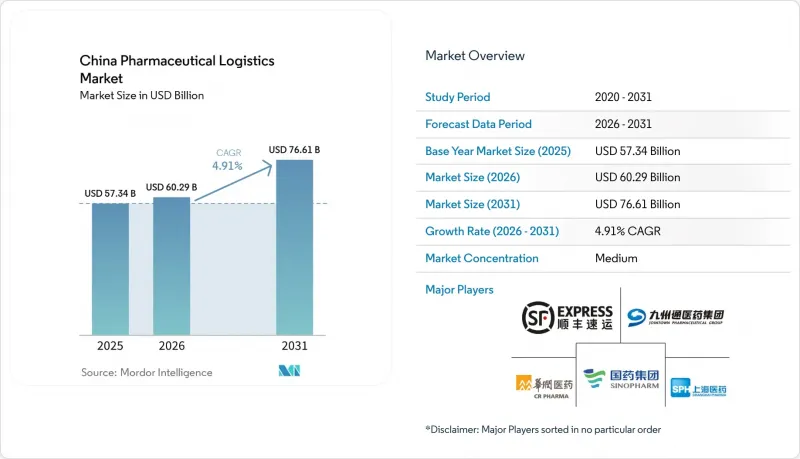

根據 Mordor Intelligence 預測,中國醫藥流市場規模預計到 2025 年將達到 573.4 億美元,到 2026 年將達到 602.9 億美元,到 2031 年將達到 766.1 億美元,2026 年至 2031 年的複合成長率為 4.91%。

人口老化帶來的穩定藥品需求、國內大規模藥品生產基地以及將分銷品質與藥品安全和服務一致性更直接掛鉤的政策框架,支撐了該市場的發展。本報告按物流功能(運輸、倉儲配送、附加價值服務)、營運模式(低溫運輸、非低溫運輸)、產品類型(處方藥、成藥、生技藥品、疫苗、臨床試驗樣本、細胞和基因療法、醫療設備、動物用藥品)以及地區(北方、東北部及其他地區)進行細分。市場預測以美元計價。

中國醫藥物流市場趨勢與洞察

擴大國家基本藥物配送網路

2025年修訂的《國家基本醫療保險藥品目錄》擴大了健保目標產品範圍,並首次新增了涵蓋創新藥物的私人醫療保險類別。這將直接增加透過核准分銷通路分銷的醫保覆蓋藥品數量。這項變化對中國醫藥物流市場意義重大,因為醫保覆蓋範圍的擴大增加了供應鏈中醫院和零售環節的藥品處理量。隨著創新療法的廣泛應用,這不僅凸顯了對常溫儲存能力的需求,也凸顯了對完善低溫運輸基礎設施的需求。 「十五」規劃的政策方向也支持大規模全國性經銷商,從而加強採購執行中的合規性、分銷管道密度和規模經濟。對於中國醫藥物流市場而言,這將導致全國物流基礎的擴大和最低服務標準的提高。因此,隨著分銷網路的擴張,那些難以投資可追溯性、序列化和溫控資產的小規模企業將面臨更大的壓力。

生物製藥和溫度控制產品的需求快速成長。

生物製藥和其他對溫度敏感的產品正在改變中國醫藥物流市場的營運重心,因為它們需要比可常溫儲存的學名藥更嚴格的管控、更完善的驗證和更穩健的異常處理機制。預計2025年,中國醫藥低溫運輸物流成本將達到267.8億元人民幣(約37.9億美元),冷藏倉庫容量將成長5.43%至452.5萬立方米,超過常溫倉庫的成長速度。這種技術轉變在細胞和基因治療領域更為顯著,某些產品的運輸溫度可能從傳統的2度C至8度C範圍轉變為-150度C至-196度C的低溫條件。這項要求使得只有擁有專用設備、檢驗的作業流程和經過培訓的員工的營運商才能進入該領域,而這些通常是普通貨運公司所不具備的。這也使得合格的供應商能夠維持比常溫採購主導物流更高的價格。在中國的醫藥物流市場,即使標準藥品分銷面臨普遍的價格壓力,這一趨勢也將導致資金流入高階低溫運輸通道。

分散地區的最後一公里基礎設施

農村地區「最後一公里」配送的脆弱性仍然是中國醫藥物流市場面臨的最突出的營運限制因素之一。儘管預計到2025年,中國醫藥運輸車隊規模將達到4,6416輛,但投資仍集中在主要都市區路線,導致農村市場認證運輸能力短缺,路線冗餘度有限。這種不平衡在西部和山區省份尤為突出,這些地區僅靠公路運輸可能無法滿足溫度穩定性要求或對補貨時間要求。發表在《公共衛生前沿》(Frontiers in Public Health)上的一項2025年研究也表明,基本藥物的可及性仍然存在區域差異,儘管政策層面做出了許多努力,但社會經濟狀況仍然影響著藥物的實際供應。在農村地區擁有集中採購合約的供應商往往低估了「最後一公里」的成本,導致用於資產升級和服務擴展的資金減少。雖然海南、雲南、新疆和重慶的無人機運作顯示這些限制因素可以得到緩解,但中國醫藥流市場在許多內陸挑戰性路線上仍然缺乏廣泛的商業性覆蓋。

細分市場分析

到2025年,運輸環節將佔中國醫藥物流市場佔有率的52.46%,成為整個營運鏈中最大的功能環節。這一環節的規模反映了道路運輸在城際運輸、都市區補給、醫院配送和藥局補貨等的核心角色。空運將繼續在緊急生技藥品、高價值樣本以及某些對速度和溫控要求高於成本的臨床運輸中發揮關鍵作用。內河航運和海運將繼續支持某些運輸路線上的常溫散裝貨物運輸,這些路線的交貨時間要求相對寬鬆,且單位運費經濟性有利於大批量運輸。到2025年,倉儲總容量將達到9,381.6萬立方米,顯示運輸環節將繼續與國內大規模倉儲基地緊密合作。

在這一領域的後半段,情況呈現出不同的態勢。預計到2031年,附加價值服務將以7.74%的複合年成長率成長,並正成為關鍵的差異化因素。製藥公司越來越傾向於將序列化、符合GDP標準的溫控、DTP(直接面向患者)藥房履約以及「低溫運輸即服務」等任務外包給第三方,而不是自行建造。這種轉變正在改變中國醫藥物流產業的經濟結構,因為利潤來源正從純粹的運輸收入轉向以合規性為重點的增值服務。順豐控股於2025年下半年正式成立生命科學和醫藥供應鏈業務集團,正是這種重組的體現,也是該領域銷售額成長超過20%的驅動力。因此,儘管倉儲和配送作為穩定的中階仍然重要,但成長越來越依賴數位整合、檢驗的處理以及豐富的外包服務,而不僅僅是儲存空間。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況及物流在製藥業中的作用

- 藥品支出趨勢

- 市場促進因素

- 擴大全國基本藥物配送網路

- 生物製藥的快速成長和對溫度控制的需求

- 網路藥局的興起以及人們對24小時送達的期望

- 更嚴格執行GDP審計和許可製度

- 集中採購中心正在促進區域整合。

- 在西部州的中距離路線上測試無人機和自動駕駛車輛

- 市場限制因素

- 農村地區最後一公里基礎設施的碎片化

- 碳排放上限政策下低溫運輸能源成本飆漲

- 關於mRNA疫苗用乾冰供應的規定

- 由於都市區醫院的交通管制,送餐時間會受到限制。

- 法律規範

- 價值鍊和分銷管道的結構分析

- 技術創新的前景

- 波特五力分析

- 藥品物流需求的變化

- 地緣政治事件對供應鏈轉型的影響

第5章 市場規模與成長預測

- 透過物流功能

- 運輸

- 道路運輸

- 航空

- 海路和內河航道

- 鐵路

- 倉儲/物流

- 附加價值服務及其他

- 運輸

- 透過操作模式

- 低溫運輸物流

- 非低溫運輸物流

- 依產品類型

- 處方藥

- 成藥

- 生物製劑和生物相似藥

- 疫苗和血液製品

- 臨床試驗材料

- 細胞和基因治療

- 醫療設備及診斷設備

- 動物醫藥

- 其他

- 按地區

- 北

- 東北

- 東方

- 中心

- 南

- 西南

- 西北

第6章 競爭情勢

- 市場集中度

- 關鍵策略趨勢

- 市佔率分析

- 公司簡介

- Sinopharm Logistics

- SF Express

- JD Logistics

- DHL Group

- United Parcel Service of America, Inc.(UPS)

- Kuehne+Nagel

- DSV A/S(Including DB Schenker)

- FedEx

- Cencora

- CJ Rokin Logistics

- Nippon Express Holdings

- Yamato Holdings

- ZTO Express

- YTO Express

- STO Express

- China Post EMS

- Cainiao Smart Logistics Network

- CMA CGM Group(Including CEVA Logistics)

- DCH Auriga

- Sinotrans Limited

- China Resources Pharmaceutical Commercial

- Jointown Pharmaceutical Group

第7章 市場機會與未來展望

According to Mordor Intelligence, the china pharmaceutical logistics market size is projected to be USD 57.34 billion in 2025, USD 60.29 billion in 2026, and reach USD 76.61 billion by 2031, growing at a CAGR of 4.91% from 2026 to 2031.

The market is supported by steady demand for medicines from an aging population, a large domestic pharmaceutical production base, and a policy system that links distribution quality more directly to drug safety and service consistency. This report is Segmented by Logistics Function (Transportation, Warehousing and Distribution, Value-Added Services), by Mode of Operation (Cold-Chain, Non-Cold-Chain), by Product Type (Prescription Drugs, OTC, Biologics, Vaccines, Clinical Trial Materials, Cell and Gene Therapies, Medical Devices, Veterinary Medicine), and by Region (North, Northeast, and More). The Market Forecasts are in Value (USD).

China Pharmaceutical Logistics Market Trends and Insights

Expansion of the National Essential-Drug Distribution Network

The updated 2025 National Basic Medical Insurance Drug Directory widened the reimbursed product base and, for the first time, added a commercial health insurance category for innovative drugs, which directly increases the flow of covered medicines through licensed distribution channels. That change matters for the China pharmaceutical logistics market because reimbursed access expands throughput at both the hospital and retail ends of the chain. It underscores the need for additional ambient capacity, but also for qualified cold-chain infrastructure as innovative therapies enter broader circulation. The policy direction under the 15th Five-Year Plan also supports larger national distributors, which strengthens scale advantages in compliance, route density, and procurement execution. For the China pharmaceutical logistics market, the result is a larger national flow base paired with a higher minimum service standard. Smaller operators that cannot fund traceability, serialization, and temperature-controlled assets are therefore under more pressure as the distribution network broadens.

Rapid Growth in Biologics and Temperature-Controlled Demand

Biologics and other temperature-sensitive products are shifting the operating center of the China pharmaceutical logistics market, as they require tighter controls, stronger validation, and more robust exception management than ambient generics. Pharmaceutical cold-chain logistics costs in China reached CNY 26.78 billion (USD 3.79 billion) in 2025, while cold storage capacity rose 5.43% to 4.525 million cubic meters, a faster rate than growth in ambient warehousing. The technical shift is even greater in the cell and gene therapy lanes, where transport can shift from the established 2 °C to 8 °C range toward cryogenic conditions of -150 °C to -196 °C for certain products. That requirement narrows the field to operators with specialized equipment, validated handling protocols, and staff training that general freight firms do not usually maintain. It also allows qualified providers to defend higher pricing than they can in ambient, procurement-led flows. In the China pharmaceutical logistics market, this pushes capital toward premium cold-chain corridors even when broader price pressure affects standard medicine distribution.

Fragmented Rural Last-Mile Infrastructure

Rural last-mile weakness remains one of the clearest operating limits in the China pharmaceutical logistics market. China's pharmaceutical vehicle fleet reached 46,416 units in 2025, but investment still clustered around stronger urban corridors, which left lower-tier markets with thinner certified capacity and less route redundancy. That imbalance matters more in western and mountainous provinces, where road-only delivery can conflict with temperature stability windows and time-sensitive replenishment needs. A 2025 Frontiers in Public Health study also showed that access to essential medicines still varies across regions, with socio-economic conditions continuing to shape actual availability despite broad policy efforts. Providers serving centralized procurement contracts in rural areas often face underpriced last-mile costs, which reduces the funds available for asset upgrades and service expansion. Drone pilots in Hainan, Yunnan, Xinjiang, and Chongqing show that the constraint can be reduced, but the China pharmaceutical logistics market still lacks broad commercial coverage in many difficult inland routes.

Other drivers and restraints analyzed in the detailed report include:

- Rise of E-Commerce Pharmacies and 24-Hr Delivery Expectations

- Stricter GDP Audit and Licensing Enforcement

- Escalating Cold-Chain Energy Costs Under Carbon Caps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation held 52.46% of the China pharmaceutical logistics market share in 2025, making it the largest functional segment across the operating chain. The segment's scale reflects the central role of road movement in intercity transfers, urban replenishment, hospital delivery, and pharmacy restocking. Air freight remains relevant for urgent biologics, high-value samples, and selected clinical shipments where speed and temperature control matter more than cost. Inland waterway and sea transport still support bulk ambient flows in selected corridors where delivery windows are less strict, and unit economics favor larger-volume movement. Total warehousing capacity reached 93.816 million cubic meters in 2025, which shows that the transport layer continues to work in close coordination with a large national storage base.

The second half of this segment tells a different story, because value-added services are forecast to grow at a 7.74% CAGR through 2031 and are now becoming central to differentiation. Pharmaceutical manufacturers increasingly want third parties to handle serialization, GDP-compliant temperature monitoring, DTP pharmacy fulfillment, and cold-chain-as-a-service instead of building those capabilities alone. That shift changes the economics of the China pharmaceutical logistics industry, because margins move away from pure transport yield and toward compliance-heavy service overlays. SF Holding's formal creation of a supply chain business group for life sciences and pharmaceuticals in late 2025 reflects that repositioning and helped drive more than 20% revenue growth in the vertical. Warehousing and distribution therefore remain important as a stable middle layer, but growth is increasingly tied to digital integration, validated handling, and outsourced service depth rather than storage space alone.

Complete Report Scope:

- By Logistics Function

- Transportation

- Road

- Air

- Sea and Inland Waterways

- Rail

- Warehousing and Distribution

- Value-added Services and Others

- Transportation

- By Mode of Operation

- Cold-Chain Logistics

- Non-Cold-Chain Logistics

- By Product Type

- Prescription Drugs

- OTC Drugs

- Biologics and Biosimilars

- Vaccines and Blood Products

- Clinical Trail Materials

- Cell and Gene Therapies

- Medical Devices and Diagnostics

- Veterinary Medicine

- Others

- By Region

- North

- Northeast

- East

- Central

- South

- Southwest

- Northwest

List of Companies Covered in this Report:

- Sinopharm Logistics

- SF Express

- JD Logistics

- DHL Group

- United Parcel Service of America, Inc. (UPS)

- Kuehne+Nagel

- DSV A/S (Including DB Schenker)

- FedEx

- Cencora

- CJ Rokin Logistics

- Nippon Express Holdings

- Yamato Holdings

- ZTO Express

- YTO Express

- STO Express

- China Post EMS

- Cainiao Smart Logistics Network

- CMA CGM Group (Including CEVA Logistics)

- DCH Auriga

- Sinotrans Limited

- China Resources Pharmaceutical Commercial

- Jointown Pharmaceutical Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview and Role of Logistics in Pharmaceutical

- 4.2 Pharmaceutical Spending Trends

- 4.3 Market Drivers

- 4.3.1 Expansion of the National Essential-Drug Distribution Network

- 4.3.2 Rapid Growth in Biologics and Temperature-Controlled Demand

- 4.3.3 Rise of E-Commerce Pharmacies and 24-Hr Delivery Expectations

- 4.3.4 Stricter GDP Audit and Licensing Enforcement

- 4.3.5 Centralized-Procurement Hubs Drive Regional Consolidation

- 4.3.6 Pilots of Drones/AVs for Western-Province Mid-Mile Routes

- 4.4 Market Restraints

- 4.4.1 Fragmented Rural Last-Mile Infrastructure

- 4.4.2 Escalating Cold-Chain Energy Costs Under Carbon Caps

- 4.4.3 Dry-Ice Supply Rules for MRNA Vaccines

- 4.4.4 Urban Hospital Traffic-Control Delivery Curfews

- 4.5 Regulatory Framework

- 4.6 Value Chain and Distribution Channel Architecture Analysis

- 4.7 Technology Innovations Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Rivalry Among Competitors

- 4.9 Evolution of Pharmaceutical Logistics Requirements

- 4.10 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size and Growth Forecasts

- 5.1 By Logistics Function

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Air

- 5.1.1.3 Sea and Inland Waterways

- 5.1.1.4 Rail

- 5.1.2 Warehousing and Distribution

- 5.1.3 Value-added Services and Others

- 5.1.1 Transportation

- 5.2 By Mode of Operation

- 5.2.1 Cold-Chain Logistics

- 5.2.2 Non-Cold-Chain Logistics

- 5.3 By Product Type

- 5.3.1 Prescription Drugs

- 5.3.2 OTC Drugs

- 5.3.3 Biologics and Biosimilars

- 5.3.4 Vaccines and Blood Products

- 5.3.5 Clinical Trail Materials

- 5.3.6 Cell and Gene Therapies

- 5.3.7 Medical Devices and Diagnostics

- 5.3.8 Veterinary Medicine

- 5.3.9 Others

- 5.4 By Region

- 5.4.1 North

- 5.4.2 Northeast

- 5.4.3 East

- 5.4.4 Central

- 5.4.5 South

- 5.4.6 Southwest

- 5.4.7 Northwest

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Sinopharm Logistics

- 6.4.2 SF Express

- 6.4.3 JD Logistics

- 6.4.4 DHL Group

- 6.4.5 United Parcel Service of America, Inc. (UPS)

- 6.4.6 Kuehne+Nagel

- 6.4.7 DSV A/S (Including DB Schenker)

- 6.4.8 FedEx

- 6.4.9 Cencora

- 6.4.10 CJ Rokin Logistics

- 6.4.11 Nippon Express Holdings

- 6.4.12 Yamato Holdings

- 6.4.13 ZTO Express

- 6.4.14 YTO Express

- 6.4.15 STO Express

- 6.4.16 China Post EMS

- 6.4.17 Cainiao Smart Logistics Network

- 6.4.18 CMA CGM Group (Including CEVA Logistics)

- 6.4.19 DCH Auriga

- 6.4.20 Sinotrans Limited

- 6.4.21 China Resources Pharmaceutical Commercial

- 6.4.22 Jointown Pharmaceutical Group

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

印度醫藥物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)德國醫藥物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

印度醫藥物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)德國醫藥物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 生物製藥物流市場-全球產業規模、佔有率、趨勢、機會、預測:按服務、營運類型、地區和競爭格局分類,2021-2031年

生物製藥物流市場-全球產業規模、佔有率、趨勢、機會、預測:按服務、營運類型、地區和競爭格局分類,2021-2031年 全球醫藥物流市場:依服務類型、類型、產品類型、最終用戶和地區分類

全球醫藥物流市場:依服務類型、類型、產品類型、最終用戶和地區分類 醫藥物流市場規模、佔有率及成長分析:依運輸方式、服務類型、物流類型、產品類型、最終用戶、應用及地區分類-2026-2033年產業預測

醫藥物流市場規模、佔有率及成長分析:依運輸方式、服務類型、物流類型、產品類型、最終用戶、應用及地區分類-2026-2033年產業預測 醫藥物流市場:按類型、產品類型、組件、運輸方式和最終用戶分類-2026-2032年全球市場預測生物製藥物流市場:依產品類型、服務類型、運輸方式、溫度需求及最終用戶分類-2026-2032年全球市場預測生物製藥物流市場:按類型、服務類型、應用和地區分類

醫藥物流市場:按類型、產品類型、組件、運輸方式和最終用戶分類-2026-2032年全球市場預測生物製藥物流市場:依產品類型、服務類型、運輸方式、溫度需求及最終用戶分類-2026-2032年全球市場預測生物製藥物流市場:按類型、服務類型、應用和地區分類 2026年全球生物製藥物流市場報告

2026年全球生物製藥物流市場報告 全球醫藥物流市場規模、佔有率、趨勢及成長分析報告(2026-2034)

全球醫藥物流市場規模、佔有率、趨勢及成長分析報告(2026-2034)