|

市場調查報告書

商品編碼

2072837

印度醫藥物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)India Pharmaceutical Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

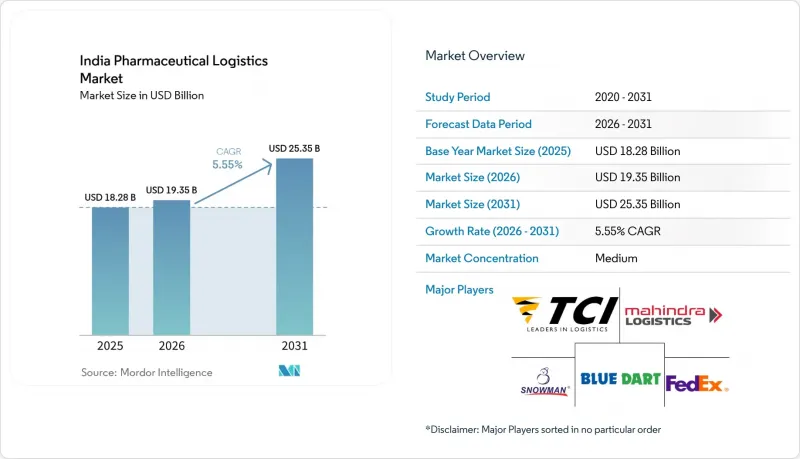

根據 Mordor Intelligence 預測,印度醫藥物流市場規模將從 2025 年的 182.8 億美元成長到 2026 年的 193.5 億美元,到 2031 年將達到 253.5 億美元,2026 年至 2031 年的複合年成長率為 5.5%。

作為全球最大的學名藥供應國,印度佔全球整體學名藥出口的20%,其作用持續擴大並加劇了國內外配送流程的規模和複雜性。本報告按物流功能(運輸、倉儲和配送、附加價值服務)、營運模式(低溫運輸、非低溫運輸)、產品類型(處方藥、成藥藥、生技藥品製劑、疫苗、臨床試驗材料、細胞和基因療法、醫療設備、動物用藥品)以及地區(北部、中部及其他地區)進行細分。市場預測以美元計價。

印度醫藥物流市場的趨勢與洞察

政府支持的生產連結獎勵計畫計劃

由於印度擴大了藥品和原料藥成分的生產連結獎勵計畫(PLI)計劃,印度醫藥物流市場需求正在成長。截至2025年12月,這些計畫下的累積投資額已達419.43億印度盧比(約46.6億美元),是最初承諾目標172.75億印度盧比(約19.2億美元)的兩倍多。兩項計畫下的累計銷售額達到3,350.36億印度盧比(約372.8億美元),涵蓋1,988種產品,其中出口額為2,152.48億印度盧比(約239.5億美元)。這表明,生產連結獎勵計畫已開始推動國內和出口通路物流量的成長。產品組合的變化更為顯著,該計劃更傾向於生物製藥、複雜學名藥和自體免疫免疫療法,這些產品對溫度和操作控制的要求比傳統口服固體製劑更為嚴格。 2026-2027會計年度聯邦預算已撥款10,000億印度盧比(約11.1億美元)用於「生物製藥SHAKTI」舉措,目標是在五年內建立1000多家獲得認證的臨床試驗機構。這表明,在可預見的未來,對專業運輸和受監管倉儲的需求將持續存在。

對需要溫度控制的生技藥品和疫苗的需求增加。

印度醫藥物流市場正受到對溫度敏感型藥品快速成長的需求所驅動。印度供應聯合國兒童基金會全球疫苗採購的60%,並滿足全球40%至70%的百白破疫苗和卡介苗需求,因此疫苗處理能力已成為物流規劃的核心要素。同時,2026年至2030年間,超過40種主要品牌藥品的專利即將到期,印度製造商正將重心轉向生物製藥、GLP-1類似物和特種注射劑,這些產品通常需要2°C至8°C的溫度控制。這給主要為大批量口服固態製劑而非高敏感療法而建立的低溫運輸帶來了壓力。為了支持原料藥和疫苗出口商,德迅集團分別於2025年12月和2026年5月在班加羅爾和海德拉巴增設了獲得HealthChain認證的交叉轉運設施。這表明物流營運商正在重新設計其資產,以適應這種新的產品組合。

大都會圈以外地區低溫運輸基礎設施分散

印度醫藥物流市場的擴張仍受到低溫運輸基礎設施分佈不均的限制,這些基礎設施必須符合相關標準。目前,冷鍊網路仍集中在少數大都會圈和製造地,而二、三線城市和農村地區的溫控運輸和倉儲服務則嚴重不足。儘管印度擁有超過3,500家低溫運輸營運商,但只有8%到10%符合世界衛生組織藥品生產品質管理規範(WHO-GDP)的標準,大部分網路仍達不到處理敏感藥品所需的品質標準。 2026年,Bluedart公司國內業務負責人表示,即使生物製藥、胰島素和疫苗開始在都市區需求中心以外的地區流通,二、三線城市和農村地區的溫控運輸和倉儲仍然十分有限。規模小規模的本地業者往往無力承擔驗證、緊急電源和持續監控系統的成本,這阻礙了主要運輸路線以外地區網路品質的提升。

細分市場分析

到2025年,運輸業將佔印度醫藥物流市場的54.07%,證實了公路貨運仍是國內醫藥分銷的核心運輸方式。印度擁有630萬公里的公路網,覆蓋超過750個地區,在這些地區,直接運輸比其他運輸方式更為重要,因此卡車運輸仍然不可或缺。空運雖然運輸量較小,但對於生物製藥、臨床試驗材料和緊急原料藥(API)的運輸而言,其每公斤收益卻顯著更高。這一趨勢在出口美國、歐洲和東協市場的航線上尤其明顯。由於運輸時間長,且難以維持必要的溫度控制和監測標準,海運和內河航運在醫藥領域的應用仍然有限。

預計附加價值服務將以8.38%的複合年成長率實現最快成長,這表明印度醫藥物流行業正在超越單純的運輸和倉儲合約。醫藥客戶擴大將包裝、套件組裝、序列化支援、逆向物流和文件管理整合到一體化合約中。倉儲和配送營運也變得更加活躍,濕度控制、批次分離、溫度映射和符合GDP標準的SOP實施不再是可選服務,而是日常營運的一部分。雖然鐵路運輸規模仍然較小,但馬士基聯合貨運公司(Maersk Concor)於2026年5月開通的海得拉巴至納瓦舍瓦的每週冷藏運輸線路表明,在貨物密度足夠高的地區,醫藥專用鐵路運輸線路可以有效運作。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況及物流在製藥業中的作用

- 藥品支出趨勢

- 市場促進因素

- 國內醫藥製造群的成長

- 政府支持的生產連結獎勵計畫(PLI)計劃

- 對需要溫度控制的生技藥品和疫苗的需求不斷成長。

- 線上藥局和D2C藥品分銷的擴張

- CDSCO強制要求使用RFID進行追蹤和追溯。

- 由於需要遵守保存期限規定,逆向物流需求激增。

- 市場限制因素

- 大都會圈以外地區低溫運輸基礎設施分散

- GDP審計演變帶來的高昂合規成本

- 鐵路沿線藥品級倉庫短缺

- 未來對柴油冷藏貨櫃車輛碳排放稅

- 法律規範

- 價值鍊與通路結構分析

- 技術創新的前景

- 波特五力分析

- 藥品物流需求的變化

- 地緣政治事件對供應鏈轉型的影響

第5章 市場規模與成長預測

- 透過物流功能

- 運輸

- 道路運輸

- 航空

- 海路和內河航道

- 鐵路

- 倉儲/物流

- 附加價值服務及其他

- 運輸

- 透過操作模式

- 低溫運輸物流

- 非低溫運輸物流

- 依產品類型

- 處方藥

- 成藥

- 生物製劑和生物相似藥

- 疫苗和血液製品

- 臨床試驗材料

- 細胞和基因治療

- 醫療設備及診斷設備

- 動物醫藥

- 其他

- 按地區

- 北

- 中心

- 西方

- 東方

- 南

第6章 競爭情勢

- 市場集中度

- 關鍵策略趨勢

- 市佔率分析

- 公司簡介

- DHL Group

- Kuehne+Nagel

- DSV A/S(Including DB Schenker)

- FedEx

- United Parcel Service of America, Inc.(UPS)

- Blue Dart Express Pvt. Ltd.

- Allcargo Logistics Pvt. Ltd.

- TCI Express

- Mahindra Logistics, Ltd.

- Snowman Logistics

- ColdEx Logistics

- Safexpress Pvt. Ltd.

- Gati-KWE

- FM Logistic

- CMA CGM Group(Including CEVA Logistics)

- NYK Line(Including Yusen Logistics)

- TVS Supply Chain Solutions

- Stellar Value Chain Solutions

- Crystal Logistic Cool Chain

- ColdStar Logistics

- Celcius Logistics

- Life Care Logistic

第7章 市場機會與未來展望

According to Mordor Intelligence, the india pharmaceutical logistics market size is expected to increase from USD 18.28 billion in 2025 to USD 19.35 billion in 2026 and reach USD 25.35 billion by 2031, growing at a CAGR of 5.55% over 2026-2031.

India's role as the world's largest supplier of generic medicines, accounting for 20% of global generic drug exports by volume, continues to expand the scale and complexity of domestic and export distribution flows. This report is Segmented by Logistics Function (Transportation, Warehousing and Distribution, Value-Added Services), by Mode of Operation (Cold-Chain, Non-Cold-Chain), by Product Type (Prescription Drugs, OTC, Biologics, Vaccines, Clinical Trial Materials, Cell and Gene Therapies, Medical Devices, Veterinary Medicine), and by Region (North, Central, and More). The Market Forecasts are in Value (USD).

India Pharmaceutical Logistics Market Trends and Insights

Government Production-Linked Incentive Schemes

India pharmaceutical logistics market demand is rising with the scale-up created by the pharmaceutical and bulk drug PLI programs. As of December 2025, cumulative investment under these schemes reached INR 41,943 crores (USD 4.66 billion) and was more than double the initial commitment target of INR 17,275 crores (USD 1.92 billion). Cumulative sales under both schemes reached INR 3,35,036 crores (USD 37.28 billion) across 1,988 products, including exports worth INR 2,15,248 crores (USD 23.95 billion), indicating that production-linked incentives are already driving higher logistics volumes across domestic and export channels. The more important shift is in the product mix, as the program favors biopharmaceuticals, complex generics, and autoimmune therapies that require tighter thermal and handling controls than conventional oral solids. Union Budget 2026-27 also backed the Biopharma SHAKTI initiative with INR 10,000 crores (USD 1.11 billion) over 5 years and a target of more than 1,000 accredited clinical trial sites, which points to a longer cycle of specialized transport and compliant warehousing demand.

Rising Demand for Temperature-Controlled Biologics and Vaccines

India's pharmaceutical logistics market is being driven by a faster shift toward temperature-sensitive medicines. India supplies 60% of UNICEF's global vaccine procurement and meets 40%-70% of global demand for DPT and BCG vaccines, keeping vaccine handling capacity central to logistics planning. At the same time, the patent cliff for more than 40 major branded drugs between 2026 and 2030 is steering Indian manufacturers toward biologics, GLP-1 analogs, and specialty injectables that usually require 2 °C-8 °C control. This is putting pressure on a cold chain built primarily for bulk oral solids rather than for sensitive therapies. Kuehne+Nagel added HealthChain-certified cross-docks in Bengaluru in December 2025 and in Hyderabad in May 2026 to support API and vaccine exporters, indicating that providers are redesigning assets around this new mix.

Fragmented Cold-Chain Infrastructure Beyond Metros

India pharmaceutical logistics market expansion is still limited by the uneven spread of compliant cold infrastructure. The network remains concentrated in a small group of metros and manufacturing hubs, while Tier 2, Tier 3, and rural corridors stay underserved for temperature-controlled transport and storage. More than 3,500 cold-chain operators exist in India, yet only 8%-10% meet WHO-GDP standards, leaving a large share of the network below the quality level required for sensitive pharmaceutical handling. Blue Dart's National Operations Head stated in 2026 that temperature-controlled transport and storage remain limited across Tier II, Tier III, and rural regions, even as biologics, insulin, and vaccines move beyond urban demand centers. Smaller regional operators often cannot absorb the cost of validation, backup power, and continuous monitoring systems, which slows network quality improvement outside the main corridors.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of E-Pharmacy and D2C Drug Distribution

- RFID-Based Track-and-Trace Mandates by CDSCO

- High Compliance Cost of Evolving GDP Audits

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation accounted for 54.07% of the India pharmaceutical logistics market share in 2025, which confirms that road freight remains the core movement layer for domestic pharmaceutical distribution. Trucks remain essential because India's 6.3 million km of road network supports deliveries to more than 750 districts, where direct reach matters more than modal substitution. Air freight carries lower volume but earns much higher revenue per kilogram for biologics, clinical trial materials, and urgent API shipments, especially on export lanes to the United States, Europe, and ASEAN markets. Sea and inland waterways remain limited for pharmaceutical use because long transit windows make temperature control and monitoring harder to sustain at the required standards.

Value-added services are projected to record the fastest growth at 8.38% CAGR, which shows that the India pharmaceutical logistics industry is moving beyond pure transport and storage contracts. Pharmaceutical customers are increasingly combining packaging, kitting, serialization support, reverse logistics, and documentation management inside integrated agreements. Warehousing and distribution is also becoming more active because humidity control, batch segregation, temperature mapping, and GDP-compliant SOP execution are now part of routine operations rather than optional services. Rail remains small, but the weekly Maersk-CONCOR reefer corridor from Hyderabad to Nhava Sheva launched in May 2026 shows that dedicated pharma rail routes can work where shipment density is high enough.

Complete Report Scope:

- By Logistics Function

- Transportation

- Road

- Air

- Sea and Inland Waterways

- Rail

- Warehousing and Distribution

- Value-added Services and Others

- Transportation

- By Mode of Operation

- Cold-Chain Logistics

- Non-Cold-Chain Logistics

- By Product Type

- Prescription Drugs

- OTC Drugs

- Biologics and Biosimilars

- Vaccines and Blood Products

- Clinical Trail Materials

- Cell and Gene Therapies

- Medical Devices and Diagnostics

- Veterinary Medicine

- Others

- By Region

- North

- Central

- West

- East

- South

List of Companies Covered in this Report:

- DHL Group

- Kuehne+Nagel

- DSV A/S (Including DB Schenker)

- FedEx

- United Parcel Service of America, Inc. (UPS)

- Blue Dart Express Pvt. Ltd.

- Allcargo Logistics Pvt. Ltd.

- TCI Express

- Mahindra Logistics, Ltd.

- Snowman Logistics

- ColdEx Logistics

- Safexpress Pvt. Ltd.

- Gati-KWE

- FM Logistic

- CMA CGM Group (Including CEVA Logistics)

- NYK Line (Including Yusen Logistics)

- TVS Supply Chain Solutions

- Stellar Value Chain Solutions

- Crystal Logistic Cool Chain

- ColdStar Logistics

- Celcius Logistics

- Life Care Logistic

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview and Role of Logistics in Pharmaceutical

- 4.2 Pharmaceutical Spending Trends

- 4.3 Market Drivers

- 4.3.1 Growth of Domestic Pharmaceutical Manufacturing Clusters

- 4.3.2 Government Production-Linked Incentive (PLI) Schemes

- 4.3.3 Rising Demand for Temperature-Controlled Biologics and Vaccines

- 4.3.4 Expansion of E-Pharmacy and D2C Drug Distribution

- 4.3.5 RFID-Based Track-and-Trace Mandates by CDSCO

- 4.3.6 Surge in Reverse Logistics Due to Expiry-Date Compliance

- 4.4 Market Restraints

- 4.4.1 Fragmented Cold-Chain Infrastructure Beyond Metros

- 4.4.2 High Compliance Cost of Evolving GDP Audits

- 4.4.3 Scarcity of Rail-Side Pharma-Grade Warehouses

- 4.4.4 Prospective Carbon-Tax on Diesel Reefer Fleets

- 4.5 Regulatory Framework

- 4.6 Value Chain and Distribution Channel Architecture Analysis

- 4.7 Technology Innovations Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Rivalry Among Competitors

- 4.9 Evolution of Pharmaceutical Logistics Requirements

- 4.10 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size and Growth Forecasts

- 5.1 By Logistics Function

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Air

- 5.1.1.3 Sea and Inland Waterways

- 5.1.1.4 Rail

- 5.1.2 Warehousing and Distribution

- 5.1.3 Value-added Services and Others

- 5.1.1 Transportation

- 5.2 By Mode of Operation

- 5.2.1 Cold-Chain Logistics

- 5.2.2 Non-Cold-Chain Logistics

- 5.3 By Product Type

- 5.3.1 Prescription Drugs

- 5.3.2 OTC Drugs

- 5.3.3 Biologics and Biosimilars

- 5.3.4 Vaccines and Blood Products

- 5.3.5 Clinical Trail Materials

- 5.3.6 Cell and Gene Therapies

- 5.3.7 Medical Devices and Diagnostics

- 5.3.8 Veterinary Medicine

- 5.3.9 Others

- 5.4 By Region

- 5.4.1 North

- 5.4.2 Central

- 5.4.3 West

- 5.4.4 East

- 5.4.5 South

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 Kuehne+Nagel

- 6.4.3 DSV A/S (Including DB Schenker)

- 6.4.4 FedEx

- 6.4.5 United Parcel Service of America, Inc. (UPS)

- 6.4.6 Blue Dart Express Pvt. Ltd.

- 6.4.7 Allcargo Logistics Pvt. Ltd.

- 6.4.8 TCI Express

- 6.4.9 Mahindra Logistics, Ltd.

- 6.4.10 Snowman Logistics

- 6.4.11 ColdEx Logistics

- 6.4.12 Safexpress Pvt. Ltd.

- 6.4.13 Gati-KWE

- 6.4.14 FM Logistic

- 6.4.15 CMA CGM Group (Including CEVA Logistics)

- 6.4.16 NYK Line (Including Yusen Logistics)

- 6.4.17 TVS Supply Chain Solutions

- 6.4.18 Stellar Value Chain Solutions

- 6.4.19 Crystal Logistic Cool Chain

- 6.4.20 ColdStar Logistics

- 6.4.21 Celcius Logistics

- 6.4.22 Life Care Logistic

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

中國醫藥物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)德國醫藥物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

中國醫藥物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)德國醫藥物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 生物製藥物流市場-全球產業規模、佔有率、趨勢、機會、預測:按服務、營運類型、地區和競爭格局分類,2021-2031年

生物製藥物流市場-全球產業規模、佔有率、趨勢、機會、預測:按服務、營運類型、地區和競爭格局分類,2021-2031年 全球醫藥物流市場:依服務類型、類型、產品類型、最終用戶和地區分類

全球醫藥物流市場:依服務類型、類型、產品類型、最終用戶和地區分類 醫藥物流市場規模、佔有率及成長分析:依運輸方式、服務類型、物流類型、產品類型、最終用戶、應用及地區分類-2026-2033年產業預測

醫藥物流市場規模、佔有率及成長分析:依運輸方式、服務類型、物流類型、產品類型、最終用戶、應用及地區分類-2026-2033年產業預測 醫藥物流市場:按類型、產品類型、組件、運輸方式和最終用戶分類-2026-2032年全球市場預測生物製藥物流市場:依產品類型、服務類型、運輸方式、溫度需求及最終用戶分類-2026-2032年全球市場預測生物製藥物流市場:按類型、服務類型、應用和地區分類

醫藥物流市場:按類型、產品類型、組件、運輸方式和最終用戶分類-2026-2032年全球市場預測生物製藥物流市場:依產品類型、服務類型、運輸方式、溫度需求及最終用戶分類-2026-2032年全球市場預測生物製藥物流市場:按類型、服務類型、應用和地區分類 2026年全球生物製藥物流市場報告

2026年全球生物製藥物流市場報告 全球醫藥物流市場規模、佔有率、趨勢及成長分析報告(2026-2034)

全球醫藥物流市場規模、佔有率、趨勢及成長分析報告(2026-2034)