|

市場調查報告書

商品編碼

2072838

德國醫藥物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Germany Pharmaceutical Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

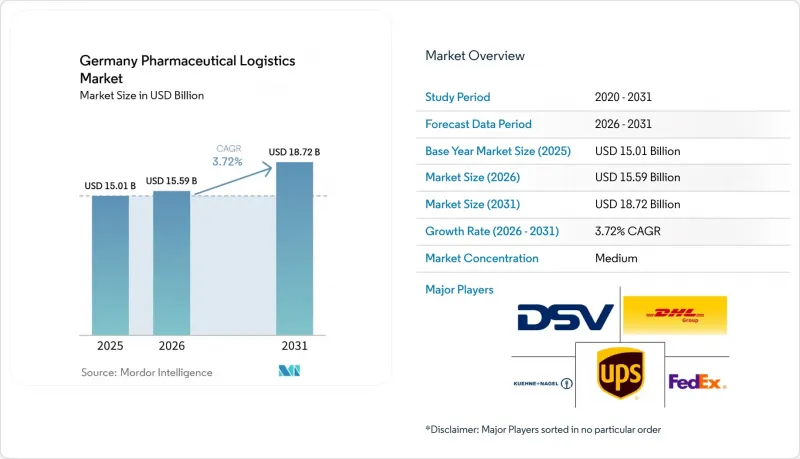

根據 Mordor Intelligence 預測,德國醫藥物流市場規模將從 2025 年的 150.1 億美元成長到 2026 年的 155.9 億美元,到 2031 年將達到 187.2 億美元,2026 年至 2031 年的複合年成長率為 3.72%。

儘管德國整體經濟成長依然疲軟,但其醫藥物流市場卻不斷擴張。預計2025年,德國GDP成長率僅0.2%,能源價格風險持續對短期工業生產構成沉重壓力。本報告按物流功能(運輸、倉儲配送、附加價值服務)、營運模式(低溫運輸物流和非低溫運輸物流)、產品類型(處方藥、成藥、生技藥品、疫苗和血液製品等)以及地區(例如北萊茵-威斯特法倫州)進行細分。市場預測以美元計價。

德國醫藥物流市場趨勢與洞察

不斷擴大的生物製藥和生物相似藥產品線

在德國醫藥物流市場,隨著生物製藥和生物相似藥更深入融入日常藥品分發流程,轉向更複雜的低溫運輸的趨勢正在加速。自2026年4月1日起,德國將在藥房實施生物相似藥替代處方框架,這提高了藥房層面精準的批次追蹤、受控配送和清晰的儲存歷史記錄的需求。這項轉變意義重大,因為它不僅增加了現有批發管道的貨物處理量,還將更多貨物轉移到小型、小規模的藥房層面,而這些貨物難以在標準網路中有效管理。因此,德國醫藥物流市場重視能夠在單一檢驗的營運模式下管理+2 度C至+8 度C溫度範圍、冷凍和低溫環境的供應商。這一點在巴伐利亞州和巴登-符騰堡州尤為明顯,這兩個州的生物製藥生產、血漿處理和特種藥品製造正在推動對更專業化的儲存和運輸服務的需求不斷成長。此外,旨在將先進療法商業化的管道標準也已提高,要求營運商遵守歐盟GDP要求,記錄所有交付情況,並證明有能力在整個運輸過程中保持溫度控制的完整性。

德國電子處方箋系統(eRezept)全國推廣

電子處方系統(eRezept)正在重塑德國醫藥物流市場。隨著處方箋配藥流程日益數位化和高效,配送至宅配和銷售管道也變得更加便利。預計到2025年10月17日,德國電子處方系統的累計使用量將突破10億次,顯示自2024年強制實施以來,數位化處方箋系統發展迅速。這種轉變導致貨運結構發生變化,從大規模、常規的批發配送轉向高頻次、小批量配送,但仍需符合GDP規範的處理流程。此外,由於藥房和處方箋資料在訂購週期中比紙本模式更早可用,需求可見度也得到提升。這種早期訊號使物流供應商和專科藥局能夠提前在高需求都市區部署庫存,並縮短補貨前置作業時間。因此,能夠將處方資料與庫存規劃、配送路線調度和溫控庫存分配相結合的倉庫管理系統在德國醫藥物流市場中的價值日益凸顯。

低溫運輸倉庫能源成本不斷上漲

德國醫藥物流市場持續受到能源價格飆漲的影響,因為低溫運輸倉庫的耗電量遠高於常溫設施。德國的工業用電成本位居歐洲最高之列,直接加重了冷藏和冷凍醫藥設施營運商的負擔。由於設施也需要適應冷媒轉換要求,導致對低全球暖化潛勢(GWP)系統及相關設備的升級改造需要更多資本投入,成本問題進一步加劇。一份產業報告顯示,採用包含風電購電協議(PPA)的混合電力採購模式,在一個報告期間內實現了成本節約並減少了1900噸二氧化碳排放。然而,避險和能源轉型計畫與藥品分銷標準(GDP)升級、監控系統和新建冷庫所需的資金存在競爭。因此,財務實力雄厚的供應商在德國醫藥物流市場擁有明顯的優勢,因為他們可以同時為能源適應性和合規性投資資金籌措。

細分市場分析

2025年,運輸業在德國醫藥物流市場佔有率中佔58.14%,持續維持其在德國醫藥物流市場中最大物流職能的地位。公路運輸仍然是德國藥局、醫院、批發商和生產商網路的核心,需要密集的國內覆蓋和頻繁的補貨配送。空運在運輸高價值、時效性強的貨物方面繼續發揮重要作用,例如先進療法、臨床試驗材料和保存期限短的生物製藥,這些貨物需要從機場快速運送到醫療機構。鐵路和海運在進口方面繼續發揮至關重要的作用,用於處理散裝物料和某些上游醫藥原料。

倉儲和配送維持了穩定的中游地位。這是因為沿著高速公路分佈的符合GDP認證的多溫區設施仍然是國內服務模式的核心。變化最快的領域是附加價值服務,預計將以6.55%的複合年成長率成長,並有望在2031年之前成為德國醫藥物流市場中成長最快的領域。醫藥托運人擴大將序列化整合、退貨管理、不合格產品處理、包裝設計支援和患者專用試劑盒製作等業務外包給能夠將合規系統與實際操作相結合的供應商。 DHL在醫療保健物流領域投資20億歐元(23.5億美元),凸顯了主要企業在德國醫藥物流市場大力推動臨床、生物製藥和先進治療支援服務的決心。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況及物流在製藥業中的作用

- 藥品支出趨勢

- 市場促進因素

- 擴大生物製藥和生物相似藥的研發管線

- 德國電子處方箋系統(eRezept)全國推廣

- 嚴格執行歐盟GDP 2022/993合規性審計

- 專業藥房的成長正在推動當日送達模式的發展。

- 在德國高速公路上進行氫燃料溫控卡車的示範測試

- 一個利用區塊鏈技術的序列化試點項目,超越了強制性的FMD要求。

- 市場限制因素

- 低溫運輸倉庫能源成本不斷上漲

- 都市區最後一公里配送的複雜許可流程涉及多個政府機構。

- 缺乏持有GDP認證的司機和倉庫技術人員

- 醫療無人機飛行路徑監管途徑的限制

- 法律規範

- 價值鍊與通路結構分析

- 技術創新前景

- 波特五力分析

- 藥品物流需求的變化

- 地緣政治事件對供應鏈轉型的影響

第5章 市場規模與成長預測

- 透過物流功能

- 運輸

- 道路運輸

- 航空

- 海路和內河航道

- 鐵路

- 倉儲/物流

- 附加價值服務及其他

- 運輸

- 透過操作模式

- 低溫運輸物流

- 非低溫運輸物流

- 依產品類型

- 處方藥

- 成藥

- 生物製劑和生物相似藥

- 疫苗和血液製品

- 臨床試驗材料

- 細胞和基因治療

- 醫療設備及診斷設備

- 動物醫藥

- 其他

- 按地區

- 北萊茵-威斯特法倫州

- 巴伐利亞

- 巴登-符騰堡州

- 其他州

第6章 競爭情勢

- 市場集中度

- 關鍵策略趨勢

- 市佔率分析

- 公司簡介

- DHL Group

- Kuehne+Nagel

- DSV A/S(Including DB Schenker)

- United Parcel Service of America, Inc.(UPS)

- FedEx

- World Courier

- NYK Line(Including Yusen Logistics)

- CMA CGM Group(Including CEVA Logistics)

- GEODIS

- DACHSER

- Hellmann Worldwide Logistics

- Fiege Logistics

- Cencora

- LOXXESS Pharma

- UNITAX-PHARMALOGISTIK GMBH

- PharmLog Pharma Logistik GmbH

- Transpharm Logistik GmbH

- Pharmaserv GmbH and Co. KG

- Arvato SE

- Lufthansa Cargo

- Noerpel Group

第7章 市場機會與未來展望

According to Mordor Intelligence, the germany pharmaceutical logistics market size is expected to increase from USD 15.01 billion in 2025 to USD 15.59 billion in 2026 and reach USD 18.72 billion by 2031, growing at a CAGR of 3.72% over 2026-2031.

The Germany pharmaceutical logistics market is expanding in a period when Germany's wider economy remains subdued, with GDP rising only 0.2% in 2025 and energy price risks still weighing on near-term industrial output. This report is Segmented by Logistics Function (Transportation, Warehousing and Distribution, and Value-Added Services), by Mode of Operation (Cold-Chain Logistics and Non-Cold-Chain Logistics), by Product Type (Prescription Drugs, OTC Drugs, Biologics, Vaccines and Blood Products, and More), and by Region (North Rhine-Westphalia, and More). The Market Forecasts are Provided in Value (USD).

Germany Pharmaceutical Logistics Market Trends and Insights

Expanding Biologics and Biosimilars Pipeline Adoption

The Germany pharmaceutical logistics market is seeing a sharper shift toward cold-chain complexity as biologics and biosimilars move deeper into routine dispensing. Germany's pharmacy substitution framework for biosimilars took effect from April 1, 2026, which increased the need for precise lot tracking, controlled handovers, and clear chain-of-custody records at the pharmacy level. That change matters because it does not simply add volume to established wholesale lanes, it shifts more shipments into smaller and more frequent pharmacy-level consignments that are harder to manage with standard networks. The Germany pharmaceutical logistics market is therefore rewarding providers that can manage +2 °C to +8 °C, frozen, and cryogenic ranges inside one validated operating model. This is especially relevant in Bavaria and Baden-Wurttemberg, where biologics production, plasma handling, and specialty manufacturing are pushing demand for more specialized storage and transport. The commercial pipeline for advanced therapies is also raising the bar, as operators must demonstrate they can document every handoff and maintain temperature integrity throughout the full route in line with EU GDP requirements.

Nation-Wide Roll-Out of Germany's E-Prescription System (eRezept)

The Germany pharmaceutical logistics market is being reshaped by eRezept because prescription fulfillment is now more digital, faster, and easier to route into home delivery and mail-order channels. Germany crossed 1 billion cumulative eRezept redemptions on October 17, 2025, demonstrating how quickly the digital prescription system had scaled since the mandatory rollout began in 2024. This shift is changing the mix of shipments from larger scheduled wholesale drops toward higher-frequency parcel flows that still need GDP-compliant handling. It is also improving demand visibility because pharmacy and prescription data are now available much earlier in the ordering cycle than they were in the paper-based model. That earlier signal allows logistics operators and specialty pharmacies to pre-position stock nearer to high-demand urban districts and reduce replenishment lead times. The Germany pharmaceutical logistics market is therefore seeing stronger value in warehouse management systems that can connect prescription data with stock planning, route scheduling, and temperature-specific inventory allocation.

Escalating Energy Costs for Cold-Chain Warehousing

The Germany pharmaceutical logistics market remains exposed to high energy prices because cold-chain warehouses consume far more electricity than ambient facilities. Germany continues to have some of the highest industrial power costs in Europe, placing a direct burden on operators of refrigerated and frozen pharmaceutical sites. This cost issue is becoming more serious as facilities also prepare for refrigerant transition requirements, which add capital spending for low-GWP systems and related equipment upgrades. A reported example from the sector showed that switching to a blended power procurement model with wind PPA exposure reduced costs and avoided 1,900 tons of CO2 in one reporting period. Even so, hedging and energy transition programs compete for the same capital that operators need for GDP upgrades, monitoring systems, and new cold rooms. The Germany pharmaceutical logistics market, therefore, gives a clear edge to providers with stronger balance sheets, because they can fund energy adaptation and compliance investment at the same time.

Other drivers and restraints analyzed in the detailed report include:

- Stringent Enforcement of EU GDP 2022/993 Compliance Audits

- Growth of Specialty Pharmacies Pushing Same-Day Delivery Models

- Shortage of GDP-Certified Drivers and Warehouse Technicians

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation held 58.14% of Germany pharmaceutical logistics market share in 2025, which kept it as the largest logistics function in the Germany pharmaceutical logistics market. Road distribution remained the core because Germany's pharmacy, hospital, wholesale, and manufacturing networks require dense domestic coverage and frequent replenishment runs. Air freight kept its role in high-value and time-critical shipments such as advanced therapies, clinical trial materials, and short-stability biologics that need rapid airport-to-care-site movement. Rail and sea-linked flows remained more relevant for import-side handling of bulk materials and selected upstream pharmaceutical inputs.

Warehousing and distribution continued to hold a stable middle position because GDP-certified multi-temperature sites near Autobahn corridors are still central to national service design. The fastest shift came from value-added services, which are projected to expand at a 6.55% CAGR and therefore show the fastest growth in the Germany pharmaceutical logistics market through 2031. Pharmaceutical shippers are increasingly outsourcing serialization aggregation, returns control, deviation handling, artwork support, and patient-specific kitting to providers that can combine compliance systems with physical handling. DHL's EUR 2 billion (USD 2.35 billion) investment in the health logistics underlined how strongly large operators are backing clinical, biopharma, and advanced therapy support services inside the Germany pharmaceutical logistics market.

Complete Report Scope:

- By Logistics Function

- Transportation

- Road

- Air

- Sea and Inland Waterways

- Rail

- Warehousing and Distribution

- Value-added Services and Others

- Transportation

- By Mode of Operation

- Cold-Chain Logistics

- Non-Cold-Chain Logistics

- By Product Type

- Prescription Drugs

- OTC Drugs

- Biologics and Biosimilars

- Vaccines and Blood Products

- Clinical Trail Materials

- Cell and Gene Therapies

- Medical Devices and Diagnostics

- Veterinary Medicine

- Others

- By Region

- North Rhine-Westphalia

- Bavaria (Bayern)

- Baden-Wurttemberg

- Rest of States

List of Companies Covered in this Report:

- DHL Group

- Kuehne+Nagel

- DSV A/S (Including DB Schenker)

- United Parcel Service of America, Inc. (UPS)

- FedEx

- World Courier

- NYK Line (Including Yusen Logistics)

- CMA CGM Group (Including CEVA Logistics)

- GEODIS

- DACHSER

- Hellmann Worldwide Logistics

- Fiege Logistics

- Cencora

- LOXXESS Pharma

- UNITAX-PHARMALOGISTIK GMBH

- PharmLog Pharma Logistik GmbH

- Transpharm Logistik GmbH

- Pharmaserv GmbH and Co. KG

- Arvato SE

- Lufthansa Cargo

- Noerpel Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview and Role of Logistics in Pharmaceutical

- 4.2 Pharmaceutical Spending Trends

- 4.3 Market Drivers

- 4.3.1 Expanding Biologics and Biosimilars Pipeline Adoption

- 4.3.2 Nation-Wide Roll-Out of Germany's E-Prescription System (eRezept)

- 4.3.3 Stringent Enforcement of EU GDP 2022/993 Compliance Audits

- 4.3.4 Growth of Specialty Pharmacies Pushing Same-Day Delivery Models

- 4.3.5 Hydrogen-Powered Temperature-Controlled Truck Pilots on Autobahn

- 4.3.6 Blockchain-Enabled Serialization Pilots Beyond FMD Mandates

- 4.4 Market Restraints

- 4.4.1 Escalating Energy Costs for Cold-Chain Warehousing

- 4.4.2 Complex Multi-Agency Permitting for Last-Mile Urban Deliveries

- 4.4.3 Shortage of GDP-Certified Drivers and Warehouse Technicians

- 4.4.4 Limited Regulatory Pathways for Medical-Grade Drone Corridors

- 4.5 Regulatory Framework

- 4.6 Value Chain and Distribution Channel Architecture Analysis

- 4.7 Technology Innovations Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Rivalry Among Competitors

- 4.9 Evolution of Pharmaceutical Logistics Requirements

- 4.10 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size and Growth Forecasts

- 5.1 By Logistics Function

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Air

- 5.1.1.3 Sea and Inland Waterways

- 5.1.1.4 Rail

- 5.1.2 Warehousing and Distribution

- 5.1.3 Value-added Services and Others

- 5.1.1 Transportation

- 5.2 By Mode of Operation

- 5.2.1 Cold-Chain Logistics

- 5.2.2 Non-Cold-Chain Logistics

- 5.3 By Product Type

- 5.3.1 Prescription Drugs

- 5.3.2 OTC Drugs

- 5.3.3 Biologics and Biosimilars

- 5.3.4 Vaccines and Blood Products

- 5.3.5 Clinical Trail Materials

- 5.3.6 Cell and Gene Therapies

- 5.3.7 Medical Devices and Diagnostics

- 5.3.8 Veterinary Medicine

- 5.3.9 Others

- 5.4 By Region

- 5.4.1 North Rhine-Westphalia

- 5.4.2 Bavaria (Bayern)

- 5.4.3 Baden-Wurttemberg

- 5.4.4 Rest of States

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 Kuehne+Nagel

- 6.4.3 DSV A/S (Including DB Schenker)

- 6.4.4 United Parcel Service of America, Inc. (UPS)

- 6.4.5 FedEx

- 6.4.6 World Courier

- 6.4.7 NYK Line (Including Yusen Logistics)

- 6.4.8 CMA CGM Group (Including CEVA Logistics)

- 6.4.9 GEODIS

- 6.4.10 DACHSER

- 6.4.11 Hellmann Worldwide Logistics

- 6.4.12 Fiege Logistics

- 6.4.13 Cencora

- 6.4.14 LOXXESS Pharma

- 6.4.15 UNITAX-PHARMALOGISTIK GMBH

- 6.4.16 PharmLog Pharma Logistik GmbH

- 6.4.17 Transpharm Logistik GmbH

- 6.4.18 Pharmaserv GmbH and Co. KG

- 6.4.19 Arvato SE

- 6.4.20 Lufthansa Cargo

- 6.4.21 Noerpel Group

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

中國醫藥物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印度醫藥物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

中國醫藥物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印度醫藥物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 生物製藥物流市場-全球產業規模、佔有率、趨勢、機會、預測:按服務、營運類型、地區和競爭格局分類,2021-2031年

生物製藥物流市場-全球產業規模、佔有率、趨勢、機會、預測:按服務、營運類型、地區和競爭格局分類,2021-2031年 全球醫藥物流市場:依服務類型、類型、產品類型、最終用戶和地區分類

全球醫藥物流市場:依服務類型、類型、產品類型、最終用戶和地區分類 醫藥物流市場規模、佔有率及成長分析:依運輸方式、服務類型、物流類型、產品類型、最終用戶、應用及地區分類-2026-2033年產業預測

醫藥物流市場規模、佔有率及成長分析:依運輸方式、服務類型、物流類型、產品類型、最終用戶、應用及地區分類-2026-2033年產業預測 醫藥物流市場:按類型、產品類型、組件、運輸方式和最終用戶分類-2026-2032年全球市場預測生物製藥物流市場:依產品類型、服務類型、運輸方式、溫度需求及最終用戶分類-2026-2032年全球市場預測生物製藥物流市場:按類型、服務類型、應用和地區分類

醫藥物流市場:按類型、產品類型、組件、運輸方式和最終用戶分類-2026-2032年全球市場預測生物製藥物流市場:依產品類型、服務類型、運輸方式、溫度需求及最終用戶分類-2026-2032年全球市場預測生物製藥物流市場:按類型、服務類型、應用和地區分類 2026年全球生物製藥物流市場報告

2026年全球生物製藥物流市場報告 全球醫藥物流市場規模、佔有率、趨勢及成長分析報告(2026-2034)

全球醫藥物流市場規模、佔有率、趨勢及成長分析報告(2026-2034)