|

市場調查報告書

商品編碼

2072653

印度中程配送:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)India Middle Mile Delivery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

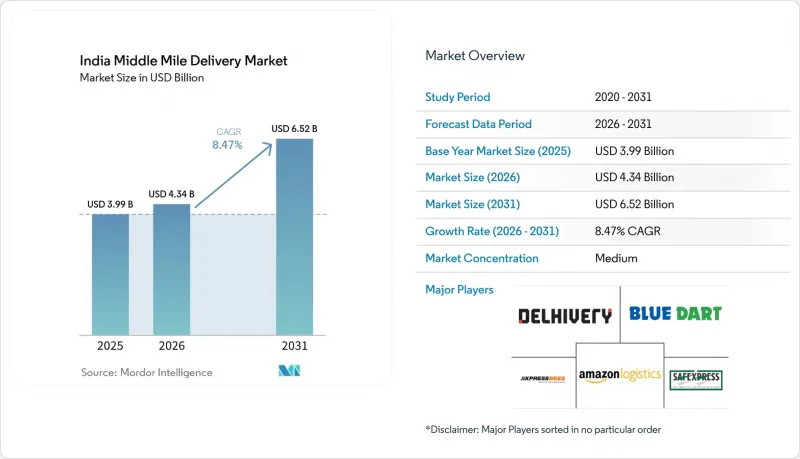

據 Mordor Intelligence 稱,2025 年印度中程配送市場價值為 39.9 億美元,預計到 2031 年將從 2026 年的 43.4 億美元成長至 65.2 億美元,預測期(2026-2031 年)複合年成長率為 8.47%。

本報告按運輸方式(公路、鐵路、航空等)、經營模式(B2B、B2C、C2C)、溫度控制(有/無溫度控制)、目的地(國內/國際)、終端用戶產業(電子商務、時尚等)和地區(北部、中部等)進行細分。市場規模和預測均以美元計價。

印度中程配送市場的趨勢與洞察

國家物流政策和“Ghati Shakti”基礎設施的推廣

印度的中程配送市場正受惠於一套將運輸走廊、產業叢集和物流樞紐整合到一個協調的公共架構中的規劃系統。 「PM Gati Shakti」整合了57個部會和超過1700個資料層,使貨物規劃能夠基於比傳統走廊決策更強大的空間基礎。 「統一物流介面平台」連接了44個政府系統,服務超過1700家註冊公司,提高了跨運輸方式貨物的即時可視性。這對於中程配送運作至關重要,因為基礎設施和資料系統朝著同一方向發展,簡化了路線規劃、交接和走廊選擇。隨著多模態和走廊連接設施的全面運作運營,沿著這些指定走廊部署樞紐和長途運輸資產的營運商有望保持成本優勢。

電子商務和快速配送蓬勃發展

印度的中程配送市場也受益於小包裹運輸規模更大、頻率更高(與幾年前相比)這一事實。電子商務和快消品的興起增加了對樞紐頻繁補貨、短週期分揀以及城際運輸的需求,這些需求需要在比傳統小包裹運輸更短的服務時限內完成。這正在改變自動化的經濟效益,因為區域城市樞紐的小包裹密度如今已足以支撐更快的分類速度和更規律的幹線運輸時刻表。此外,隨著需求擴展到最大的大都會圈之外,營運商被迫將運輸能力進一步擴展到二線和三線城市,導致網路設計發生變化。因此,如今驅動市場發展的不僅是貨運量的成長,還有透過更密集的網路運輸小規模、對時間更敏感的包裹的需求。

分散的貨運基礎設施和司機短缺

印度的中程配送市場仍面臨著與勞動力和車輛組織相關的結構性問題,這些問題限制了其在高峰期快速擴展運輸能力的能力。問題的核心不僅在於合格司機的短缺,還在於大多數車輛仍然分散在資金籌措、培訓和數位化系統獲取管道不均的小規模企業手中。因此,當運輸需求激增時,企業要麼被迫謹慎應對,要麼被迫承擔閒置資產和人事費用成本的增加,難以擴大處理能力。此外,排放氣體法規、安全系統和路線管理技術的合規性也存在滯後,而正規的托運人越來越希望將這些改進納入其服務合約。這種情況導致服務品質參差不齊,在印度中程配送市場的部分地區,運輸路線的改善並未轉化為完全可靠的營運績效。

細分市場分析

到2025年,道路運輸將佔據印度中程配送市場69.73%的佔有率,顯著超越其他運輸方式。這一主導地位歸功於印度龐大的國家公路網,該公路網總長146,572公里,持續支持著工業和消費走廊之間靈活的樞紐間運輸。在印度的中程配送市場,公路運輸仍然是那些需要覆蓋範圍廣、貨物尺寸不規則或需要鐵路和航空道路運輸無法充分滿足的「門到樞紐」柔軟性的配送服務的首選運輸方式。對於短途和區域內運輸而言,這一點尤其重要,因為在這些運輸中,運輸頻率比單純的運輸速度更為關鍵。

預計到2031年,印度中程配送市場中,航空運輸的複合年成長率將達到10.10%,成為成長最快的運輸方式。這反映出市場對藥品、生鮮產品和跨境貨物的需求不斷成長,而這些貨物的時效性至關重要。鐵路運輸憑藉其可靠的營運時刻表和長途運輸的經濟優勢,在以走廊為基礎的貨運模式中佔據越來越重要的地位。隨著西部專用貨運走廊於2026年建成通車,鐵路將在那些優先考慮幹線運輸效率和緩解堵塞而非單段配送柔軟性的線路上進一步鞏固其地位。海運活動仍以港口主導,並依賴沿海產業叢集,因此其角色集中在特定區域,而非覆蓋廣泛。

預計到2025年,B2C模式將佔印度中程配送市場規模的72.03%,這反映了電子商務平台和快消業者為有組織的小包裹運輸帶來的規模優勢。此模式具有許多優勢,例如標準化包裝、固定路線、樞紐間頻繁往返,以及能夠將自動化成本分攤到大規模的貨運量上。這些營運特點使得B2C領域成為最能充分利用高密度分類網路和常規幹線運輸計畫的領域。 B2B模式仍然重要,因為它構成了製造業、日常消費品(FMCG)和正規分銷合約等穩定貨物需求的基礎,有助於營運商平衡電子商務的季節性波動。

C2C(消費者對消費者)是成長最快的經營模式,預計到2031年將以10.22%的複合年成長率成長。這一轉變與再行銷、社群化銷售和P2P小包裹遞送密切相關,這些模式正變得更加系統化,更容易透過數位網路進行路由。在印度的中程配送業,這意味著逆向物流、小批量小包裹遞送和多向遞送比以往任何時候都更加重要。那些僅以正向B2C遞送為前提建構網路的營運商可能需要重新設計其樞紐,以提高其處理退貨、分類和重新路由的能力。雖然規模仍小於B2C,但就全國小包裹網路的應用場景拓展而言,印度中程配送產業的這一細分領域佔據著重要的結構性地位。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 國家物流政策與「Ghati Shakti」基礎建設發展計劃

- 電子商務和快速配送蓬勃發展

- 專用貨運走廊可以降低鐵路運輸的成本和運輸時間。

- 利用人工智慧和物聯網的可視化和最佳化平台

- 面向中小微型企業的零擔貨運叢集商創造了新的運輸量。

- 採用可再生能源供電的低溫運輸樞紐可降低營運成本。

- 市場限制因素

- 卡車運輸業較為分散,而且司機短缺。

- 燃油價格波動給利潤率帶來了壓力。

- 多模態物流園區全面運作的瓶頸

- 不遵守低溫運輸規定會導致食品變質,並因此受到罰款。

- 法律規範

- 價值鍊和通路分析

- 技術創新前景

- 波特五力模型

- 關於倉庫和物流中心的考量

- 關於冷藏中程配送的注意事項。

- 地緣政治事件對供應鏈轉型的影響

第5章 市場規模及成長預測(價值,2026-2031 年)

- 透過運輸方式

- 路

- 鐵路

- 航空旅行

- 海洋

- 按經營模式

- Business-to-Business(B2B)

- Business-to-Consumer(B2C)

- Customer-to-Consumer(C2C)

- 按類型進行溫度控制

- 無溫度控制

- 溫控型

- 目的地

- 國內的

- 國際的

- 按最終用戶行業分類

- 電子商務零售

- 時尚與生活風格

- 美容、健康和個人護理

- 住宅和家具

- 家用電子電器和家用電器

- 醫療保健和醫療用品

- 其他

- 按地區

- 北方

- 中部

- 西

- 東

- 南部

第6章 競爭情勢

- 市場集中度

- 關鍵策略趨勢

- 市佔率分析

- 公司簡介

- Delhivery

- Blue Dart Express

- Amazon Transportation Services

- XpressBees

- Safexpress

- Ekart Logistics

- TCI Express

- Gati(Allcargo Group)

- Mahindra Logistics

- DHL Supply Chain India

- VRL Logistics

- DTDC Express

- FedEx India

- TVS Supply Chain Solutions

- CJ Darcl Logistics

- Om Logistics Ltd.

- Navata Road Transport

- Nitco Logistics

- BlackBuck

- Rivigo

- LetsTransport

- ElasticRun

第7章 市場機會與未來展望

According to Mordor Intelligence, the india middle-mile delivery market size was valued at USD 3.99 billion in 2025 and is estimated to grow from USD 4.34 billion in 2026 to reach USD 6.52 billion by 2031, at a CAGR of 8.47% during the forecast period (2026-2031).

This report is Segmented by Transportation Mode (Road, Rail, Air, and More), by Business Model (B2B, B2C, and C2C), by Temperature Control (Temperature-Controlled and Non-Temperature-Controlled), by Destination (Domestic and International), by End-User Industry (E-Commerce, Fashion, and More), and by Region (North, Central, and More). The Market Size and Forecasts are Provided in Terms of Value (USD).

India Middle Mile Delivery Market Trends and Insights

National Logistics Policy and Gati Shakti Infrastructure Push

The India middle-mile delivery market is benefiting from a planning system that now links transport corridors, industrial clusters, and logistics nodes into a coordinated public framework. PM Gati Shakti integrates 57 ministries and more than 1,700 data layers, enabling freight planning with a stronger spatial basis than earlier corridor decisions. The Unified Logistics Interface Platform connects 44 government systems and serves more than 1,700 registered companies, improving real-time cargo visibility across transport modes. This matters for middle-mile operations because route planning, handoffs, and corridor selection become easier when infrastructure and data systems move in the same direction. Operators that place hubs and linehaul assets along these designated corridors are likely to maintain a cost advantage as more multimodal parks and corridor-linked facilities enter full use.

E-Commerce and Quick-Commerce Shipment Boom

The India middle-mile delivery market is also benefiting from the fact that parcel movement now occurs in larger, more frequent waves than it did a few years ago. E-commerce and quick commerce are increasing the need for repeat-hub replenishment, short-cycle sortation, and intercity transfers operating within tighter service windows than conventional parcel movement. This is changing the economics of automation because secondary-city hubs now have enough parcel density to justify faster sortation and more regular linehaul schedules. It is also shifting network design, since demand is moving beyond the largest metros and forcing operators to place capacity deeper into Tier-2 and Tier-3 corridors. As a result, the market is no longer driven only by shipment growth, but also by the need to move smaller, more time-sensitive consignments through a denser network.

Fragmented Trucking Base and Driver Shortage

The India middle-mile delivery market still faces a structural labor and fleet-organizational problem that limits how quickly capacity can scale during peak periods. The core issue is not only the shortage of qualified drivers, but also the fact that a large share of the fleet remains dispersed across small operators with uneven access to finance, training, and digital systems. That makes throughput harder to scale when shipment demand rises quickly, because operators either commit cautiously or carry higher idle-asset and labor costs. It also slows compliance upgrades in emissions, safety systems, and route technology, which organized shippers increasingly expect as part of service contracts. This keeps service quality uneven and prevents some parts of the India middle-mile delivery market from converting corridor upgrades into fully reliable operational performance.

Other drivers and restraints analyzed in the detailed report include:

- Dedicated Freight Corridors Cut Rail Transit Cost/Time

- AI-/IoT-Enabled Visibility and Optimization Platforms

- Fuel-Price Volatility Squeezing Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Roadways held 69.73% of the India middle-mile delivery market share in 2025, leaving them far ahead of other transport modes. That leadership came from the scale of India's national highway system, which reached 146,572 km and continues to support flexible hub-to-hub movement across industrial and consumption corridors. In the Indian middle-mile delivery market, road remains the default mode for shipments that require broad geographic reach, irregular consignment sizes, or door-to-hub flexibility that rail and air cannot match with the same ease. This is especially relevant for short-haul and intra-regional transfers, where shipment frequency matters more than pure corridor speed.

Airways is set to record the fastest India middle-mile delivery market size CAGR at 10.10% through 2031, reflecting stronger demand from pharmaceutical, perishable, and cross-border freight that places a premium on time certainty. Railways are gaining ground where schedule reliability and long-haul economics now favor corridor-based freight movement. The completion of the Western dedicated freight corridor in 2026 gives rail a stronger role on routes where linehaul efficiency and less congestion matter more than one-leg delivery flexibility. Maritime activity remains tied to port-led and coastal industrial clusters, so its role is concentrated rather than broad.

B2C accounted for 72.03% of the India middle-mile delivery market size in 2025, reflecting the scale that e-commerce platforms and quick-commerce players now bring to organized parcel movement. This model benefits from standardized packaging, repeat routes, frequent inter-hub runs, and the ability to spread automation cost across very large shipment pools. Those operating features make B2C the segment that most clearly rewards dense sortation networks and repeat linehaul schedules. B2B remains important because it anchors steady freight demand from manufacturing, FMCG, and formal distribution contracts, helping operators balance e-commerce seasonality.

C2C is the fastest-growing business model and is projected to expand at a 10.22% CAGR through 2031. The change is tied to recommerce, social selling, and peer-to-peer parcel movement, which are becoming more formal and easier to route through digital networks. In the India middle-mile delivery industry, that means reverse flows, small-batch parcel transfers, and mixed-direction movement are becoming more relevant than before. Operators that built networks only around forward B2C movement may need to redesign hubs to handle more returns, grading, and rerouting capacity. This part of the India middle-mile delivery industry is still smaller than B2C, but it is structurally important because it widens the use cases for national parcel networks.

Complete Report Scope:

- By Transportation Mode

- Roadways

- Railways

- Airways

- Maritime

- By Business Model

- Business-to-Business (B2B)

- Business-to-Consumer (B2C)

- Customer-to-Consumer (C2C)

- By Temperature Control

- Non-Temperature Controlled

- Temperature Controlled

- By Destination

- Domestics

- International

- By End User Industry

- E-commerce Retail

- Fashion and Lifestyle

- Beauty, Wellness and Personal Care

- Home and Furniture

- Consumer Electronics and Appliances

- Healthcare and Medical Supplies

- Others

- By Region

- North

- Central

- West

- East

- South

List of Companies Covered in this Report:

- Delhivery

- Blue Dart Express

- Amazon Transportation Services

- XpressBees

- Safexpress

- Ekart Logistics

- TCI Express

- Gati (Allcargo Group)

- Mahindra Logistics

- DHL Supply Chain India

- VRL Logistics

- DTDC Express

- FedEx India

- TVS Supply Chain Solutions

- CJ Darcl Logistics

- Om Logistics Ltd.

- Navata Road Transport

- Nitco Logistics

- BlackBuck

- Rivigo

- LetsTransport

- ElasticRun

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 National Logistics Policy and Gati Shakti Infrastructure Push

- 4.2.2 E-Commerce and Quick-Commerce Shipment Boom

- 4.2.3 Dedicated Freight Corridors Cut Rail Transit Cost/Time

- 4.2.4 AI-/IoT-Enabled Visibility and Optimization Platforms

- 4.2.5 MSME LTL Cluster Aggregators Unlocking New Volumes

- 4.2.6 Renewable-Powered Cold-Chain Hubs Lowering OPEX

- 4.3 Market Restraints

- 4.3.1 Fragmented Trucking Base and Driver Shortage

- 4.3.2 Fuel-Price Volatility Squeezing Margins

- 4.3.3 Ramp-Up Bottlenecks at Multimodal Logistics Parks

- 4.3.4 Cold-Chain Compliance Gaps Causing Spoilage Penalties

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Technology Innovations Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Rivalry Among Competitors

- 4.8 Insights on Warehousing & Distribution Centers

- 4.9 Insights on Refrigerated Middle-Mile Delivery

- 4.10 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size & Growth Forecasts (Value, 2026-2031)

- 5.1 By Transportation Mode

- 5.1.1 Roadways

- 5.1.2 Railways

- 5.1.3 Airways

- 5.1.4 Maritime

- 5.2 By Business Model

- 5.2.1 Business-to-Business (B2B)

- 5.2.2 Business-to-Consumer (B2C)

- 5.2.3 Customer-to-Consumer (C2C)

- 5.3 By Temperature Control

- 5.3.1 Non-Temperature Controlled

- 5.3.2 Temperature Controlled

- 5.4 By Destination

- 5.4.1 Domestics

- 5.4.2 International

- 5.5 By End User Industry

- 5.5.1 E-commerce Retail

- 5.5.2 Fashion and Lifestyle

- 5.5.3 Beauty, Wellness and Personal Care

- 5.5.4 Home and Furniture

- 5.5.5 Consumer Electronics and Appliances

- 5.5.6 Healthcare and Medical Supplies

- 5.5.7 Others

- 5.6 By Region

- 5.6.1 North

- 5.6.2 Central

- 5.6.3 West

- 5.6.4 East

- 5.6.5 South

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Delhivery

- 6.4.2 Blue Dart Express

- 6.4.3 Amazon Transportation Services

- 6.4.4 XpressBees

- 6.4.5 Safexpress

- 6.4.6 Ekart Logistics

- 6.4.7 TCI Express

- 6.4.8 Gati (Allcargo Group)

- 6.4.9 Mahindra Logistics

- 6.4.10 DHL Supply Chain India

- 6.4.11 VRL Logistics

- 6.4.12 DTDC Express

- 6.4.13 FedEx India

- 6.4.14 TVS Supply Chain Solutions

- 6.4.15 CJ Darcl Logistics

- 6.4.16 Om Logistics Ltd.

- 6.4.17 Navata Road Transport

- 6.4.18 Nitco Logistics

- 6.4.19 BlackBuck

- 6.4.20 Rivigo

- 6.4.21 LetsTransport

- 6.4.22 ElasticRun

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

全球資料中心物流市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球資料中心物流市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 數位航運市場規模、佔有率和成長分析:按解決方案、部署基礎設施、供應鏈功能、最終用戶產業和地區分類-2026-2033年產業預測

數位航運市場規模、佔有率和成長分析:按解決方案、部署基礎設施、供應鏈功能、最終用戶產業和地區分類-2026-2033年產業預測 裝卸整平機市場規模、佔有率和成長分析:按操作方式、核心材料成分、最終用途產業、分銷管道和地區分類-2026-2033年產業預測

裝卸整平機市場規模、佔有率和成長分析:按操作方式、核心材料成分、最終用途產業、分銷管道和地區分類-2026-2033年產業預測 美國中程配送:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)全球物流市場:市場規模、佔有率、趨勢和成長分析(2026-2034)

美國中程配送:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)全球物流市場:市場規模、佔有率、趨勢和成長分析(2026-2034) 2026年全球智慧物流市場報告

2026年全球智慧物流市場報告 智慧物流自動化市場預測至2034年—全球解決方案、運輸方式、組件、技術、應用、最終用戶和區域分析

智慧物流自動化市場預測至2034年—全球解決方案、運輸方式、組件、技術、應用、最終用戶和區域分析 資料中心物流市場規模、佔有率和趨勢分析報告:按設備類型、資料中心規模、服務、最終用途、地區和細分市場預測(2026-2033 年)航運和海事資訊通訊技術:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

資料中心物流市場規模、佔有率和趨勢分析報告:按設備類型、資料中心規模、服務、最終用途、地區和細分市場預測(2026-2033 年)航運和海事資訊通訊技術:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) 2026-2030年全球物流市場

2026-2030年全球物流市場