|

市場調查報告書

商品編碼

2072630

軟包裝數位印刷:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Digital Printing For Flexible Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

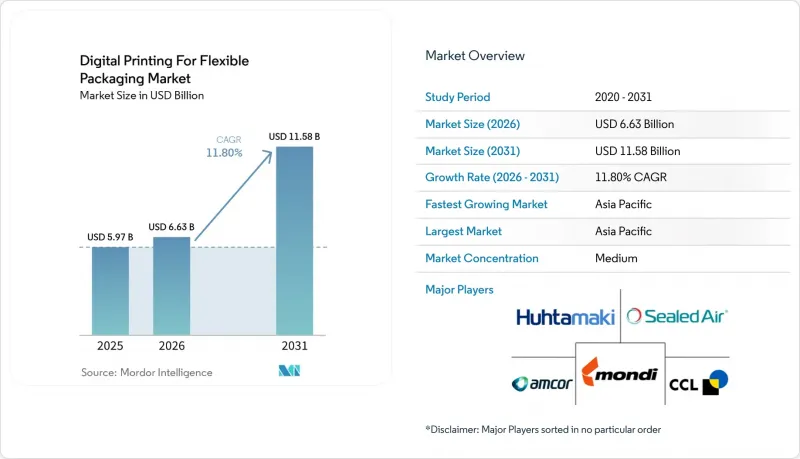

根據 Mordor Intelligence 預測,軟性包裝數位印刷市場規模預計將在 2025 年達到 59.7 億美元,2026 年達到 66.3 億美元,到 2031 年達到 115.8 億美元,2026 年至 2031 年的複合年成長率為 11.80%。

本報告按印刷技術(靜電照相、UV噴墨、水性噴墨等)、包裝類型(袋裝、條狀包裝、小袋裝等)、油墨類型(UV固化油墨等)、材料類型(紙張和紙基複合材料等)、終端用戶行業(食品、飲料等)和地區進行細分。市場預測以美元計價。

全球軟包裝數位印刷趨勢及洞察

小批量 SKU 的增加正在推動軟性包裝大規模生產的經濟效益。

SKU數量的增加已不再局限於品牌推廣活動,而是影響到軟包裝數位印刷市場的生產計畫、設備利用率和加工商投資。在2026年FTA FORUM INFOFLEX大會上,來自Siegwerk、GEW和Flint Group的演講者指出,品牌商的訂單量正在減少,但同時又要求從設計到商店的執行速度更快。這削弱了傳統凹版印刷換版的經濟效益。數位系統無需在不同作業之間更換印刷版,使加工商更容易在1萬至1.5萬件的批量範圍內保持競爭力,而這一批量範圍對於模擬設備而言越來越難以高效處理。這種轉變降低了庫存積壓的風險,並最大限度地減少了設計過時所造成的損失。此外,它還使採購團隊在比較軟包裝數位印刷市場的供應商時,能夠更清楚地整體情況總成本。訂購模式也在改變需求方向。品牌商越來越需要數位功能,而不僅僅是將其視為可選服務,而是將其視為基本供應要求。因此,轉換器的投資回收期現在取決於客戶諮詢和訂單配置的品質。

電子商務物流正在重塑區域包裝格局。

電子商務不僅改變了產品數量,也改變了軟包裝數位印刷市場必須應對的包裝種類、標籤變更和區域規格等問題。在中國,宅配的國家包裝標準促使大規模線上經銷商需要快速更新設計,而數位印刷比頻繁更換印版更適合滿足這一需求。在印度,快速零售的生鮮食品銷售模式持續推動對輕便包裝袋和小袋的需求,這就要求產品本地化為當地語言,開展本地化促銷活動,並縮短補貨週期。這一點至關重要,因為線上需求並非以單一的大量訂單形式出現,而是以眾多SKU的形式出現,這些SKU具有地域性、季節性或宣傳活動主導,印刷商必須同時管理這些需求。歐洲品牌所有者在將通用產品結構調整為符合各國語言和標籤差異方面也面臨類似的挑戰,這推動了軟包裝數位印刷技術的應用。因此,數位化敏捷性不僅是降低印刷成本的手段,也是管理供應鏈的工具。

大額資本投資會為長期經濟可行性帶來投資回收風險。

對於軟性包裝數位印刷市場而言,資本成本仍然是短期內最大的障礙,尤其對於那些工廠車間仍保留可用類比設備的加工商而言更是如此。能夠處理多種承印物的生產型印刷機通常售價超過100萬美元,而工作流程的整合會進一步增加實現穩定產量所需的總投資。投資回報前景取決於訂單中是否有足夠的中小批量訂單,但許多加工商無法保證這樣的訂單結構,因為他們與客戶的合約是基於傳統的長期生產模式。為此,Flint Group Digital Zeicon推出了「Ecolyne」訂閱模式,該模式於2025年底率先在亞太地區推出,並於2026年推廣至全球。此模式將大額資本投資視為持續營運成本,從而降低了初始採用門檻,使加工商能夠更循序漸進地擴大規模。儘管如此,資本投資問題仍然是軟性包裝數位印刷市場普及的一大障礙,因為許多買家仍然要求提供明確的證據表明,生產配置、客戶需求和運轉率能夠保持良好狀態。

細分市場分析

預計到2025年,UV噴墨印刷將佔據軟包裝數位印刷市場30.88%的佔有率。這反映了其成熟的部署經驗、廣泛的基材相容性和完善的售後服務支援。其優勢在於能夠處理各種軟性薄膜,與現有加工商的工作流程相容,並且與一些競爭流程相比,所需的額外準備步驟更少。與靜電照相相比,UV噴墨印刷更適合PE和PP薄膜應用。在這些應用中,生產團隊需要更簡單的基材處理和可靠的黏合性能。這種操作親和性至關重要,因為加工商在擴大生產規模時,往往傾向於選擇能夠減少認證時間、操作人員再培訓和供應鏈複雜性的系統。這些實際因素使得UV噴墨印刷即使在新技術不斷湧現的情況下,仍然是軟包裝數位印刷市場的主要收入來源。

水性噴墨印刷技術在紙基應用領域也取得了長足發展。 SCREEN Europe公司的「Truepress PAC 520P」目前正在義大利薩基塔爾工廠進行大規模商業化生產,速度高達80公尺/分鐘。該系統無需印版或模具,並使用符合食品安全標準的水性油墨。混合印刷機預計到2031年將以14.38%的複合年成長率成長,成為該市場成長最快的技術類別。 Gallus Five將於2025年上市,這表明加工商正在尋求既能保持工業級處理獲利能力,又能具備處理各種作業所需的數位化柔軟性的系統。混合系統不僅可以取代老舊的數位設備,還能拓寬可訂單的專案範圍,將數位化技術的應用擴展到中型批量生產領域,而純數位設備在這些領域往往難以獲利。作為補償,加工商通常需要更有信心,相信中短期批量需求會持續存在,才會採用這種高速但資本密集的方案。

預計到2025年,軟包裝袋將佔據37.04%的市場佔有率,成為該領域最大的包裝形式,並在食品、飲料、個人護理和家居用品等應用領域發揮核心作用。這一領先地位體現了軟包裝袋在阻隔性能、商店影響力、消費者便利性和適應頻繁設計變更能力之間的平衡。立式袋尤其受益於數位印刷,品牌可以在一次宣傳活動中推出多種設計方案,而無需承擔小批量類比印刷所需的高昂滾筒成本。包裝紙和捲材在各個工業領域仍然廣泛使用,並且與模擬生產的聯繫仍然緊密,尤其是在長期食品應用中。然而,在促銷活動和限量版宣傳活動中,數位印刷的應用正在不斷增加,因為在這些活動中,上市速度往往比單位成本更為重要。

預計到2031年,條狀包裝和小袋的複合年成長率將達到12.74%,成為所有包裝形式中成長最快的。這一成長與單份膳食補充劑、便捷型個人保健產品以及需要緊湊包裝和頻繁更換包裝圖案的電商履約模式的需求相吻合。製藥業的需求也在不斷成長,因為一些非處方藥正在轉向小袋,並且需要對每單位產品進行可變數據處理,以實現可追溯性和患者資訊管理。為了滿足序列化需求和包裝柔軟性之間的這種交匯點,Domino Printec India在2025年印度國際包裝展(CPHI)和印度包裝製造及電子展(PMEC)上推出了K300可變數據印刷系統,其印刷速度高達250米/分鐘。雖然袋裝和其他包裝形式仍然很重要,但由於它們依賴通用產品和散裝應用,傳統的大批量印刷在這些領域仍然具有更高的經濟優勢。

區域分析

預計到2025年,亞太地區將佔據全球軟包裝數位印刷市場35.95%的佔有率,並將以13.06%的複合年成長率持續成長至2031年。該地區擁有最大的生產基地和最快的成長速度,這種罕見的組合表明,包裝需求與電子商務、快速消費品(FMCG)的規模以及區域產品差異密切相關。中國仍然是該市場的核心,因為線上零售活動的活性化、包裝的頻繁更新以及標準化需求,自然地催生了小批量數位印刷的需求。印度也正在成為重要的成長中心,因為藥品序列化、快速零售推動的食品雜貨銷售成長以及食品接觸材料監管的日益嚴格,都促使加工商需要更快、更靈活的包裝形式。在2026年上海國際塑膠包裝展覽會(Chinaplas 2026)上,BOBST與中國加工商合作,展示了數位化和永續的軟包裝解決方案,凸顯了這項需求對該地區的重要性。

截至2026年,北美和歐洲在軟包裝數位印刷市場擁有最成熟的技術基礎,儘管該報告並未單獨列出各市場的市場佔有率。在北美,ePac於2026年3月在鳳凰城開設了一家新工廠,並擴大了亞特蘭大、費城和溫哥華的產能,這表明數位軟包裝正在從孤立的區域擴張轉向更廣泛的網路部署。在歐洲,隨著PPWR 2025/40和德國印刷油墨條例對油墨和基材認證標準的選擇產生影響,在更嚴格的合規條件下,該行業仍在取得進展。此外,ePac在謝菲爾德工廠引進了歐洲、中東和非洲地區首台HP Indigo 200K印刷機,顯示區域規模化正從試點階段邁向更商業性的階段。

在南美、中東、非洲和其他一些小規模的市場,即使到了2025年,數位印刷技術的應用仍將處於起步階段,其發展主要取決於包裝現代化和本地品牌建設,而非目前數位設備的普及程度。巴西是南美市場成長潛力最大的國家。這是因為隨著品牌食品和飲料需求的成長,市場對高品質圖像、產品種類多樣化和快速上市的需求也隨之增加,而這些需求難以透過傳統的大量生產系統來滿足。在阿拉伯聯合大公國和沙烏地阿拉伯,針對高階食品和個人保健產品的包裝方案正在推廣,這些方案適用於在地化的新產品推出和小批量生產。南非、奈及利亞和埃及還有進一步的成長空間,隨著軟包裝數位印刷市場擴展到當前主要地區之外,這些國家的發展速度將取決於加工商的投資、材料供應和電子商務基礎設施。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 軟包裝小批量SKU數量增加

- 電子商務驅動的區域包裝需求

- 品牌對可變數據和大規模客製化的需求

- 採用混合式數位印刷機,減少切換過程中的浪費和前置作業時間。

- 在受監管的包裝中採用低遷移、食品安全油墨

- 用於微型倉配和個人化醫療的直接到轉換器數位印刷

- 市場限制因素

- 與傳統的大量印刷相比,這涉及較高的資本投入和投資回收風險。

- 特種油墨和薄膜基材的價格波動

- 某些數位墨水系統的食品接觸性和可回收性認證有其限制。

- 互聯列印生產線的網路安全和工作流程中斷風險

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 透過印刷技術

- 靜電照相術

- UV噴墨

- 水性噴墨

- 混合式印刷機

- 其他印刷技術

- 按包裝類型

- 小袋

- 條狀包裝和小袋

- 包裝和卷材

- 包包

- 標籤

- 其他包裝類型

- 按墨水類型

- UV固化油墨

- 水性油墨

- 溶劑型油墨

- 電子束(EB)墨水

- 材料類型

- 塑膠薄膜(PET、PE、PP)

- 紙和紙基層壓板

- 鋁箔

- 可堆肥薄膜

- 其他材料類型

- 按最終用戶行業分類

- 食物

- 飲料

- 製藥

- 個人護理化妝品

- 家

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 泰國

- 印尼

- 其他亞太國家

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- HP Inc.

- Xeikon NV

- Canon Solutions America, Inc.

- EFI Electronics For Imaging, Inc.

- Durst Group AG

- Heidelberger Druckmaschinen AG

- Landa Digital Printing Ltd.

- Domino Printing Sciences plc

- Eastman Kodak Company

- CCL Industries Inc.

- Amcor plc

- Mondi plc

- Huhtamaki Oyj

- Sealed Air Corporation

- ePac Holdings, LLC

- Bobst Group SA

- Konica Minolta, Inc.

- SCREEN Graphic Solutions Co., Ltd.

- Fujifilm Holdings Corporation

- Agfa-Gevaert NV

- Flint Group

第7章 市場機會與未來展望

According to Mordor Intelligence, the digital printing for flexible packaging market size is projected to be USD 5.97 billion in 2025, USD 6.63 billion in 2026, and reach USD 11.58 billion by 2031, growing at a CAGR of 11.80% from 2026 to 2031.

This report is Segmented by Printing Technology (Electrophotography, UV Inkjet, Water-Based Inkjet, and More), Packaging Type (Pouches, Stick Packs and Sachets, and More), Ink Type (UV-Curable Inks, and More), Material Type (Paper and Paper-Based Laminates, and More), End-User Industry (Food, Beverages, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Digital Printing For Flexible Packaging Market Trends and Insights

Short-Run SKU Proliferation Drives Volume Economics in Flexible Packs

SKU growth has moved beyond branding activity and now affects production planning, asset use, and converter investment in the digital printing for flexible packaging market. At FTA FORUM INFOFLEX 2026, speakers from Siegwerk, GEW, and Flint Group said brands were placing smaller orders while also asking for faster design-to-shelf execution, which weakens the economics of conventional gravure changeovers. Digital systems avoid physical print forms between jobs, helping converters stay competitive in the run-length range of 10,000 to 15,000 units, which has become harder for analog assets to serve efficiently. That same shift lowers overstock risk, reduces write-offs from obsolete designs, and gives procurement teams a clearer total-cost picture when they compare suppliers in the digital printing for flexible packaging market. The ordering pattern is also changing the direction of demand, as brands are increasingly requiring digital capability as a supply requirement rather than treating it as an optional service. As a result, converter payback periods are being influenced as much by customer pull and order mix quality as by the hardware itself.

E-Commerce Logistics Reshape Regional Pack Formats

E-commerce is changing not only volume but also the number of pack versions, labeling changes, and regional formats that the digital printing for flexible packaging market must support. In China, national packaging standards for express shipments have heightened the need for rapid design updates across a large online seller base, which aligns better with digital production than repeated cylinder changes. In India, quick-commerce grocery models are driving repeat demand for lightweight pouches and sachets that require regional language support, local promotions, and short refill cycles. This matters because online demand does not flow as a single, large order stream; instead, it breaks into many geography-specific, seasonal, and campaign-led SKUs that one converter has to manage simultaneously. European brand owners face a similar issue when aligning common product structures with country-level language and labeling differences, which supports wider adoption of digital printing for flexible packaging. Digital agility, therefore, acts as a supply chain control tool, not only as a print cost tool.

High Capital Expenditure Creates Payback Risk Against Long-Run Economics

Capital cost remains the clearest short-term barrier in the digital printing for flexible packaging market, especially for converters that still have usable analog assets on the floor. Production-grade presses that can run across a broad substrate range commonly cost more than USD 1 million, and workflow integration further increases the total commitment before stable output is achieved. The payback profile depends on having enough short- and medium-run orders in the order book, and many converters cannot guarantee that mix when their customer contracts were built around longer, conventional production. Flint Group Digital Xeikon has responded with its Ecolyne subscription model, which was launched globally in 2026 after its initial Asia-Pacific introduction in late 2025. The model lowers the upfront entry point by treating a large capital commitment as a recurring operating cost and allowing converters to scale more gradually. Even so, the capex question continues to slow adoption in the digital printing for flexible packaging market because many buyers still need clear proof that run mix, customer demand, and utilization will remain favorable.

Other drivers and restraints analyzed in the detailed report include:

- Brand Demand for Variable Data and Mass Customization Accelerates Converter Migration

- Hybrid Digital Presses Resolve the Changeover-Speed Trade-Off at Scale

- Specialty Ink and Film Substrate Price Volatility Compresses Converter Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

UV inkjet held 30.88% of the digital printing market share for flexible packaging in 2025, reflecting a mature installed base, broad substrate qualification, and well-developed service support. Its strength has come from how it handles a wide range of flexible films while also fitting existing converter workflows, with fewer extra preparation steps than some competing processes. Compared with electrophotography, UV inkjet is better aligned with PE and PP film applications, where production teams want simpler substrate handling and dependable adhesion. That operational familiarity matters because converters tend to favor systems that reduce qualification time, operator retraining, and supply chain complexity when they scale output. In the digital printing for flexible packaging market, those practical factors have helped UV inkjet remain the main revenue anchor even as newer technologies expand.

Water-based inkjet is also advancing in paper-based applications, and SCREEN Europe's Truepress PAC 520P is now in full commercial production at Sacchital in Italy at 80 m/min, using food-safety-compliant water-based inks without plates or tooling. Hybrid presses are projected to grow at a 14.38% CAGR through 2031, which makes them the fastest moving technology category in this market. The Gallus Five launch in 2025 showed how converters are looking for systems that preserve industrial throughput while also adding digital flexibility for mixed job streams. Hybrid systems extend digital reach into medium-run work that pure digital assets often struggle to serve profitably, so they widen the usable order mix rather than simply replacing older digital units. The tradeoff is that converters usually need stronger confidence in sustained short-to-medium run demand before they commit to this faster but more capital-intensive option.

Pouches held a 37.04% share in 2025, making them the largest format in the segment and confirming their central role across food, beverage, personal care, and household applications. Their lead reflects the balance they offer between barrier performance, shelf impact, consumer convenience, and the ability to support frequent design changes. Stand-up pouches have especially benefited from digital printing, as brands can carry multiple design variants in a single campaign without absorbing the cylinder costs that make small analog runs unattractive. Wraps and rollstock still serve a broad industrial base and remain more closely linked to analog production, particularly in long-run food applications. Even so, promotional overwraps and limited-edition campaigns are drawing more digital activity because launch speed often matters more than unit cost in those programs.

Stick packs and sachets are projected to grow at a 12.74% CAGR through 2031, which gives them the strongest pace among packaging formats. Their growth aligns with single-serve nutrition, convenience-led personal care, and e-commerce fulfillment models that require compact formats and frequent artwork changes. Pharmaceutical demand is also expanding as some over-the-counter products shift to sachet-based delivery and require unit-level variable data for traceability and patient information. Domino Printech India launched the K300 variable data printing system at CPHI and PMEC 2025 for this exact intersection of serialization demand and packaging format flexibility, with speeds up to 250 m/min. Bags and other packaging types remain relevant, but their heavier exposure to commodity and bulk applications means conventional long-run print still holds a stronger economic position there.

Complete Report Scope:

- By Printing Technology

- Electrophotography

- UV Inkjet

- Water-based Inkjet

- Hybrid Presses

- Other Printing Technologies

- By Packaging Type

- Pouches

- Stick Packs and Sachets

- Wraps and Rollstock

- Bags

- Labels

- Other Packaging Types

- By Ink Type

- UV-curable Inks

- Water-based Inks

- Solvent-based Inks

- Electron-beam (EB) Inks

- By Material Type

- Plastic Films (PET, PE, PP)

- Paper and Paper-based Laminates

- Aluminum Foil

- Compostable Films

- Other Material Types

- By End user Industry

- Food

- Beverages

- Pharmaceuticals

- Personal Care and Cosmetics

- Household

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Thailand

- Indonesia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Geography Analysis

Asia-Pacific accounted for 35.95% share of the digital printing for flexible packaging market size in 2025 and is projected to expand at a 13.06% CAGR through 2031. The region combines the strongest volume base with the fastest growth, an uncommon combination that shows how closely packaging demand is tied to e-commerce scale, fast-moving consumer goods, and regional product variation. China remains central because online retail activity, fast pack updates, and standardization needs create a natural case for short-run digital output. India is also becoming a major growth center as pharmaceutical serialization, quick-commerce grocery expansion, and food-contact oversight push converters toward faster, more flexible packaging formats. BOBST underscored the regional importance of this demand by showcasing digital and sustainable flexible packaging solutions alongside Chinese converters at Chinaplas 2026 in Shanghai.

North America and Europe formed the most mature technology base for the digital printing for flexible packaging market in 2026, even though the input did not provide separate regional shares for each market. In North America, ePac opened a new facility in Phoenix in March 2026 and added capacity in Atlanta, Philadelphia, and Vancouver, showing that digital flexible packaging is moving into broader network deployment rather than isolated local expansion. Europe is advancing under tighter compliance conditions because PPWR 2025/40 and the German Printing Ink Ordinance are both influencing ink and substrate qualification choices. The first HP Indigo 200K installation in EMEA at ePac's Sheffield site also showed that regional scaling is moving into a more commercial stage rather than staying in pilot mode.

South America, the Middle East and Africa, and other smaller markets remained at earlier adoption stages in 2025, and their progress depended more on packaging modernization and local brand development than on current installed digital depth. Brazil leads the South American opportunity because growing branded food and beverage demand favors better graphics, more SKU variety, and shorter launch cycles than long-run conventional systems handle well. The United Arab Emirates and Saudi Arabia are supporting more premium food and personal care packaging programs, which fit localized launches and shorter production runs. South Africa, Nigeria, and Egypt offer a longer runway, and their pace will depend on converter investment, substrate availability, and e-commerce infrastructure as the digital printing for flexible packaging market expands beyond its current core regions.

- HP Inc.

- Xeikon N.V.

- Canon Solutions America, Inc.

- EFI Electronics For Imaging, Inc.

- Durst Group AG

- Heidelberger Druckmaschinen AG

- Landa Digital Printing Ltd.

- Domino Printing Sciences plc

- Eastman Kodak Company

- CCL Industries Inc.

- Amcor plc

- Mondi plc

- Huhtamaki Oyj

- Sealed Air Corporation

- ePac Holdings, LLC

- Bobst Group SA

- Konica Minolta, Inc.

- SCREEN Graphic Solutions Co., Ltd.

- Fujifilm Holdings Corporation

- Agfa-Gevaert N.V.

- Flint Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Short-Run SKU Proliferation in Flexible Packs

- 4.2.2 E-Commerce-Driven Regionalized Packaging Demand

- 4.2.3 Brand Demand for Variable Data and Mass Customization

- 4.2.4 Hybrid Digital Presses Reducing Changeover Waste and Lead Times

- 4.2.5 Low-Migration and Food-Safe Ink Adoption in Regulated Packs

- 4.2.6 Direct-To-Converter Digital Printing for Micro-Fulfillment and Personalized Medicine

- 4.3 Market Restraints

- 4.3.1 High Capex and Payback Risk Versus Conventional Long-Run Printing

- 4.3.2 Specialty Ink and Film Substrate Price Volatility

- 4.3.3 Limited Food-Contact and Recyclability Qualification for Some Digital Ink Systems

- 4.3.4 Cybersecurity and Workflow Downtime Risks in Connected Print Lines

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Printing Technology

- 5.1.1 Electrophotography

- 5.1.2 UV Inkjet

- 5.1.3 Water-based Inkjet

- 5.1.4 Hybrid Presses

- 5.1.5 Other Printing Technologies

- 5.2 By Packaging Type

- 5.2.1 Pouches

- 5.2.2 Stick Packs and Sachets

- 5.2.3 Wraps and Rollstock

- 5.2.4 Bags

- 5.2.5 Labels

- 5.2.6 Other Packaging Types

- 5.3 By Ink Type

- 5.3.1 UV-curable Inks

- 5.3.2 Water-based Inks

- 5.3.3 Solvent-based Inks

- 5.3.4 Electron-beam (EB) Inks

- 5.4 By Material Type

- 5.4.1 Plastic Films (PET, PE, PP)

- 5.4.2 Paper and Paper-based Laminates

- 5.4.3 Aluminum Foil

- 5.4.4 Compostable Films

- 5.4.5 Other Material Types

- 5.5 By End user Industry

- 5.5.1 Food

- 5.5.2 Beverages

- 5.5.3 Pharmaceuticals

- 5.5.4 Personal Care and Cosmetics

- 5.5.5 Household

- 5.5.6 Other End-user Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Thailand

- 5.6.4.7 Indonesia

- 5.6.4.8 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Egypt

- 5.6.5.2.4 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 HP Inc.

- 6.4.2 Xeikon N.V.

- 6.4.3 Canon Solutions America, Inc.

- 6.4.4 EFI Electronics For Imaging, Inc.

- 6.4.5 Durst Group AG

- 6.4.6 Heidelberger Druckmaschinen AG

- 6.4.7 Landa Digital Printing Ltd.

- 6.4.8 Domino Printing Sciences plc

- 6.4.9 Eastman Kodak Company

- 6.4.10 CCL Industries Inc.

- 6.4.11 Amcor plc

- 6.4.12 Mondi plc

- 6.4.13 Huhtamaki Oyj

- 6.4.14 Sealed Air Corporation

- 6.4.15 ePac Holdings, LLC

- 6.4.16 Bobst Group SA

- 6.4.17 Konica Minolta, Inc.

- 6.4.18 SCREEN Graphic Solutions Co., Ltd.

- 6.4.19 Fujifilm Holdings Corporation

- 6.4.20 Agfa-Gevaert N.V.

- 6.4.21 Flint Group

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2034年環保軟包裝市場預測-全球材料、包裝類型、永續性類型、應用、最終用戶和地區分析

2034年環保軟包裝市場預測-全球材料、包裝類型、永續性類型、應用、最終用戶和地區分析 全球模組化包裝設備市場:成長機會、成長要素、產業趨勢分析及2026-2035年預測2034年全球軟包裝市場預測-按材料、產品類型、印刷技術、包裝形式、應用和地區分類的分析

全球模組化包裝設備市場:成長機會、成長要素、產業趨勢分析及2026-2035年預測2034年全球軟包裝市場預測-按材料、產品類型、印刷技術、包裝形式、應用和地區分類的分析 軟性鋁箔包裝市場:依包裝類型、材料類型、終端用戶產業及地區分類永續軟性包裝市場預測至2034年—按材料、包裝類型、應用、最終用戶和地區分類的全球分析紙本保護包裝市場預測至2034年-全球產品類型、材料類型、包裝形式、功能、分銷管道、最終用戶和區域分析

軟性鋁箔包裝市場:依包裝類型、材料類型、終端用戶產業及地區分類永續軟性包裝市場預測至2034年—按材料、包裝類型、應用、最終用戶和地區分類的全球分析紙本保護包裝市場預測至2034年-全球產品類型、材料類型、包裝形式、功能、分銷管道、最終用戶和區域分析 軟性包裝市場:按材料、包裝形式、技術、結構、最終用戶和分銷管道分類-2026-2032年全球市場預測軟性包裝市場:依材料、產品類型、應用、地區分類軟性工業包裝市場:按材料、產品類型、包裝形式、最終用途和分銷管道分類-2026-2032年全球市場預測

軟性包裝市場:按材料、包裝形式、技術、結構、最終用戶和分銷管道分類-2026-2032年全球市場預測軟性包裝市場:依材料、產品類型、應用、地區分類軟性工業包裝市場:按材料、產品類型、包裝形式、最終用途和分銷管道分類-2026-2032年全球市場預測 泰國軟包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

泰國軟包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)