|

市場調查報告書

商品編碼

2044209

泰國軟包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Thailand Flexible Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

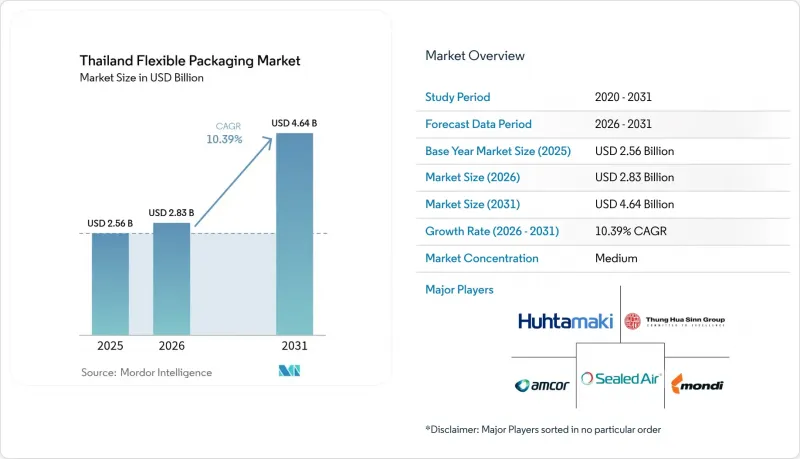

2025年泰國軟包裝市場價值為25.6億美元,預計到2031年將達到46.4億美元,而2026年為28.3億美元,預測期(2026-2031年)複合年成長率為10.39%。

強勁的電子商務物流成長、政府對生質塑膠的補貼以及「中國+1」戰略下製造地的持續轉移,正在加速對包裝袋、小袋和郵寄包裝的需求。儘管品牌所有者對可回收性的承諾正促使加工商轉向單一材料的機械取向聚乙烯(MDO-PE),但阻隔性多層複合材料在對氧氣敏感的食品中仍然發揮著至關重要的作用。泰國軟包裝市場也受益於清真認證即食食品出口的成長、旅遊業的復甦(該行業更傾向於使用獨立小袋)以及政策支持的東部經濟走廊產業投資。市場競爭依然適中,跨國加工企業投資化學回收和工業4.0生產線,而200多家中小企業在小批量生產領域保持主導地位。

泰式軟包裝市場趨勢與洞察

電子商務小包裹量的激增正在加速對輕型郵政包裝的需求。

預計2025年,泰國每日小包裹處理量將達到700萬至800萬件。這一激增推動了包裝方式從紙板轉向輕質聚乙烯郵寄包裝,從而使最後一公里配送成本降低20%至30%。私人宅配業者已採用自動化分類機來處理每日超過1,200萬件的包裹尖峰時段,這導致對自黏袋、防靜電電子設備保護套和保溫冷凍食品袋的訂單增加。加工商已將郵寄包裝的厚度降至40至60微米,在不影響抗摔性能的前提下減少了樹脂用量。在限時搶購活動中佔據主導地位的服裝和美妝品牌要求在不到一周的前置作業時間內完成定製圖案,這迫使中小企業採用快速換版柔版印刷機。儘管包裹量激增,泰國尚未實施電子商務包裝法規,因此電商平台的自願回收計畫成為推動可回收單一材料解決方案的主要動力。

泰國清真食品和即食食品的出口熱潮推動了對阻隔性包裝袋的需求。

預計到2025年,清真認證產品的出口額將達到約78億美元。這主要得益於常溫保存的咖哩和調理食品,這些產品需要使用帶有鋁箔或二氧化矽阻隔層的殺菌袋,以確保18至24個月的保存期限。清真科學中心和中央伊斯蘭委員會的認證構成了一項文件門檻,有利於擁有可追溯供應鏈的大型加工商。海灣合作理事會(GCC)的進口商越來越需要阻隔性透明薄膜來突出產品質量,這推動了對氧化鋁沉澱技術的投資。可重複密封的拉鍊和吸嘴雖然會讓價格上漲30%至40%,但卻能滿足海外都市區消費者對份量控制的需求。預計2030年,南部各州清真食品產能的擴大將提振當地對蒸煮蒸餾材料的需求。

禁止進口塑膠廢料導致本地rPET/rPE供應短缺。

2025年禁止進口塑膠廢料的政策將使市場上每年減少15萬至20萬噸再生PET和PE原料,導致再生PET價格上漲25%至30%,使其相對於原生樹脂的成本優勢蕩然無存。國內PET瓶的回收量僅為可用寶特瓶的三分之一左右,而由於人工分揀的限制,軟包裝薄膜的回收量仍然非常有限。目前,食品級rPET的供應量無法滿足加工商的需求,迫使出口商要麼支付溢價購買經認證的進口顆粒,要麼冒著無法滿足歐洲再生材料含量要求的風險。 SCG Packaging和TPBI的化學回收試點計畫有望緩解這一局面,但預計要到2027年才能全面實施。隨著再生材料含量目標的日益嚴格,加工化妝品包裝袋和清潔劑補充裝的加工商面臨著最嚴重的供應短缺問題。

細分市場分析

2025年,軟包裝袋將主導泰國軟包裝市場,佔36.71%的市場佔有率,充分展現其在飲料、寵物食品和家居護理產品填充用等領域的廣泛應用。品牌商更青睞帶有吸嘴和拉鍊的垂直包裝,這種包裝相比玻璃瓶,不僅整體系統成本更低,還能在貨架上脫穎而出,並提供可調節的份量。同時,小袋和條狀包裝也以11.54%的複合年成長率成長,主要得益於消費者積極購買單份飲料、調味品和營養補充粉等產品,並透過電商平台直接配送。輕量化也是重點領域,新型線性低密度聚乙烯薄膜可在不影響抗衝擊性的前提下,將包裝袋重量減輕8-10%。

除了厚度減少之外,軟包裝袋在高附加價值蒸餾食品和寵物食品領域仍然佔據穩固地位,因為這些領域對阻隔氧氣和水分的阻隔性要求很高。同時,小袋的應用範圍正在從粉狀產品擴展到液體產品,例如使用耐熱澆鑄聚丙烯層的單次使用洗髮精。跨國飲料品牌正在試用穿孔雙條包裝,這種包裝只有在打開時才會混合益生菌和維生素,因此對設備的密封精度提出了更高的要求。生產泡麵調味料的本地中小企業依賴最小批量為1萬件的柔版印刷機,這為那些僅從事數位印刷、為網紅主導產品推廣進行小批量生產的新興企業創造了機會。整體而言,泰國的軟包裝市場仍然傾向於那些能夠在消費者便利性、輕量化物流和不斷發展的EPR(生產者延伸責任制)成本結構之間取得平衡的包裝形式。

到2025年,塑膠仍將佔據泰國軟包裝市場54.89%的佔有率。這主要歸功於聚乙烯、聚丙烯和PET的成本績效優勢。聚乙烯應用廣泛,從用於麵包袋的低密度聚乙烯到用於清潔劑包裝袋的高密度聚乙烯,加工商的年產量超過300萬噸。然而,在「生物循環綠」補貼計畫和PLA樹脂價格下降的推動下,泰國生質塑膠軟包裝市場正在快速擴張,預計將以11.36%的複合年成長率成長。生鮮食品和烘焙產品的品牌商正在轉向使用PLA基薄膜,這種薄膜既能滿足海洋公園的堆肥要求,又能確保包裝在整個8天供應鏈中的完整性。

傳統塑膠材料目前面臨雙重壓力:一是與原油價格相關的原料成本波動,二是難以回收的多層結構產品需承擔的生產者延伸責任(EPR)成本。聚丙烯(PP)因其透明性和耐熱性,在袋裝米飯和微波爆米花中仍然發揮著重要作用,但再生PP的供應鏈仍不完善,削弱了其對循環經濟的貢獻。聚對苯二甲酸乙二醇酯(PET)是金屬沉澱零食薄膜的關鍵材料,但由於廢料進口禁令導致食品級再生PET(rPET)短缺,加工商不得不頻繁地將原生材料和再生材料混合,以保持在歐洲客戶規定的25%閾值以下。在生質塑膠領域,早期PBAT共混物正在提高韌性,而非基因改造PLA等級則符合出口市場的標籤要求。掌握生物基外層和薄隔離層共擠出成型技術的加工商,在跨國快速消費品買家尋求區域產品組合脫碳的過程中,將佔據有利地位。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電子商務小包裹量的激增正在加速對輕型郵政包裝的需求。

- 泰國清真食品和即食食品出口的蓬勃發展,推動了對具有阻隔性的包裝袋的需求增加。

- 根據生物循環綠色(BCG)政策,津貼以提高生質塑膠薄膜的生產能力。

- 重視可回收性的品牌擁有者正在轉向使用單一材料的MDO-PE薄膜。

- 工業 4.0 標準的柔版印刷機的引進提高了中小企業小批量生產的獲利能力。

- 作為「中國+1」策略的一部分,國際快速消費品生產向泰國進行近岸外包。

- 市場限制因素

- 禁止進口塑膠廢料導致國內rPET/rPE供應短缺。

- 生產者延伸責任制(EPR)法案將推高合規成本。

- 先進印刷和加工領域技術純熟勞工短缺

- 原物料價格波動對加工企業的利潤率帶來了壓力。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 當前地緣政治局勢對市場的影響

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

- 主要產業的供應商部署狀況

- 投資分析

第5章 市場規模與成長預測

- 依產品類型

- 小袋

- 包包

- 薄膜包裝

- 小包裝/條狀包裝

- 標籤和封套

- 軟性儲槽及其他產品類型

- 材料

- 塑膠

- 聚乙烯(PE)

- 聚丙烯(PP)

- 聚對苯二甲酸乙二醇酯(PET)

- 聚氯乙烯(PVC)

- 其他塑膠

- 紙

- 鋁箔

- 生質塑膠

- 多層屏障結構

- 塑膠

- 按最終用戶行業分類

- 食物

- 飲料

- 個人護理和化妝品

- 製藥和醫療保健

- 寵物食品和動物飼料

- 家用和工業用途

- 電子商務與物流

- 按層級構造

- 單材料結構

- 多層阻隔層壓板

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Amcor plc

- Thung Hua Sinn Group

- Huhtamaki Oyj

- Sealed Air Corporation

- T. Tarutani Pack Co Ltd

- SCG Packaging Public Co Ltd

- Mondi plc

- JR Pack Co Ltd

- Thai Artec Co Ltd

- TPBI Public Co Ltd

- Innopack Industry Co Ltd

- Scientex Packaging(Ayer Keroh)Berhad

- Kim Pai Co Ltd

- Print Master Co Ltd

- South East Packaging Industry Co Ltd

- LLH Printing and Packaging

- Majend Macks Co Ltd

- Fuji Seal International Inc.

- Royal Meiwa Pax Co Ltd

- Craftz Co Ltd

- Alpla(Thailand)Co Ltd

- Shrinkflex(Thailand)Public Co Ltd

第7章 市場機會與未來展望

The Thailand flexible packaging market size was valued at USD 2.56 billion in 2025 and estimated to grow from USD 2.83 billion in 2026 to reach USD 4.64 billion by 2031, at a CAGR of 10.39% during the forecast period (2026-2031).

Solid e-commerce logistics growth, government bioplastic subsidies, and a steady wave of China-plus-one manufacturing relocations are accelerating demand across pouch, sachet, and mailer formats. Brand-owner commitments to recyclability are nudging converters toward mono-material, machine-direction-oriented polyethylene (MDO-PE), even as high-barrier multilayer laminates retain their critical role for oxygen-sensitive foods. The Thailand flexible packaging market is also benefiting from rising halal ready-to-eat exports, a revitalized tourism sector that favors portion-controlled sachets, and policy-backed industrial investments in the Eastern Economic Corridor. Competitive intensity remains moderate, with multinational converters investing in chemical recycling and Industry 4.0 lines while more than 200 small and medium-sized enterprises (SMEs) retain leadership in short-run jobs.

Thailand Flexible Packaging Market Trends and Insights

Surging E-Commerce Parcel Volumes Accelerating Demand for Lightweight Mailing Packs

Daily parcel throughput climbed to 7-8 million in 2025, a jump that converted corrugated shippers into lighter polyethylene mailers, enabling them to save 20-30% on last-mile freight costs. Private couriers installed automated sorters to handle peak loads of more than 12 million parcels per day, pulling in orders for peel-and-seal pouches, anti-static electronics sleeves, and insulated frozen-food bags. Converters trimmed mailer gauges to 40-60 microns, lowering resin usage without sacrificing drop resistance. Apparel and beauty brands, which dominate flash-sale events, are requesting custom graphics within one-week lead times, pressuring SMEs to adopt quick-change flexo presses. Despite the volume spike, Thailand has not imposed e-commerce packaging regulations, so voluntary take-back programs by marketplaces are the main nudge toward recyclable mono-material solutions.

Boom in Thailand's Halal and Ready-to-Eat Food Exports Requiring High-Barrier Pouches

Halal-certified exports reached roughly USD 7.8 billion in 2025, anchored by shelf-stable curries and ready meals that demand retort pouches with aluminum-foil or silicon-oxide barriers capable of 18-24 month shelf life. Certification by the Halal Science Center and the Central Islamic Council creates documentation hurdles that favor large converters with traceable supply chains. Gulf Cooperation Council importers increasingly request high-barrier, transparent films to showcase product quality, spurring investment in aluminum oxide vapor deposition. Resealable zippers and spouts command a 30-40% price premium but deliver portion control sought by urban consumers abroad. Expected expansion of halal capacity in Southern provinces is set to lift local demand for retort-grade laminates through 2030.

Ban on Imported Plastic Scrap Tightening Local rPET/rPE Availability

The 2025 prohibition on imported plastic scrap removed 150,000-200,000 t/y of recycled PET and PE feedstock, inflating recycled PET prices by 25-30% and eroding the cost edge over virgin resin. Domestic collection accounts for only a third of available PET bottles, while flexible film recovery remains negligible due to manual sorting constraints. Food-grade rPET supply now meets less than half of converter demand, pushing exporters to pay premiums for certified imported pellets or risk failing recycled-content mandates in Europe. Chemical recycling pilots by SCG Packaging and TPBI promise relief but are unlikely to reach scale before 2027. Converters serving cosmetic sachets and detergent refill packs face the sharpest squeeze as recycled-content targets tighten.

Other drivers and restraints analyzed in the detailed report include:

- Bio-Circular-Green Policy Subsidising Bioplastic Film Capacity Additions

- Brand-Owner Shifts to Mono-Material MDO-PE Film for Recyclability

- Extended Producer Responsibility Draft Law Raising Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Pouches accounted for a commanding 36.71% of the Thai flexible packaging market in 2025, underscoring their versatility for beverages, pet food, and home-care refills. Brands prefer stand-up formats with spouts or zippers that lend billboard-like shelf presence and enable portion control at a lower total system cost than glass jars. In parallel, sachets and stick packs are growing at an 11.54% CAGR as on-the-go consumers snap up single-serve beverages, condiments, and nutraceutical powders delivered directly via e-commerce. Weight reduction is also a focal point; new linear low-density polyethylene films cut pouch gram weight by 8-10% without compromising drop resistance.

Down-gauging aside, pouches hold firm in value-added retort meals and pet food where oxygen and moisture barriers are non-negotiable. Sachets, on the other hand, are moving beyond powders into liquids such as single-dose shampoos using heat-resistant cast polypropylene layers. Multinational beverage brands are trialing perforated twin-stick formats that mix probiotic cultures with vitamins only when opened, placing extra sealing accuracy demands on equipment. Local SMEs that serve instant noodle condiments rely on flexo presses with 10,000-unit minimums, creating an opportunity for digital-only newcomers serving micro-batches for influencer-led product launches. Overall, the Thailand flexible packaging market continues to favor formats that balance consumer convenience, lightweight logistics, and evolving EPR cost structures.

Plastic retained a 54.89% share of the Thailand flexible packaging market in 2025, thanks to polyethylene, polypropylene, and PET winning on cost-performance metrics. Polyethylene's broad toolkit, from low-density grades for bread bags to high-density grades for detergent pouches, anchors converter production volumes exceeding 3 million t/y. Yet the Thailand flexible packaging market size for bioplastics is expanding quickly and is forecast to grow at an 11.36% CAGR, catalyzed by the Bio-Circular-Green subsidy scheme and falling PLA resin prices. Brand owners in fresh produce and bakery lines have switched to PLA-based films that meet marine park compostability requirements while maintaining pack integrity throughout an eight-day supply chain.

Conventional plastic stalwarts now face dual pressures: volatile crude-linked feedstock costs and EPR fees that penalize difficult-to-recycle multilayer structures. Polypropylene's clarity and heat resistance keep it relevant for boil-in-bag rice and microwave popcorn, but recycled PP streams remain underdeveloped, hurting circularity claims. PET stays critical for metallized snack films, yet shortages of food-grade rPET after the scrap-import ban mean converters often blend virgin and recycled content below the 25% thresholds specified by European customers. On the bioplastic front, early-stage PBAT blends enhance toughness, while GMO-free PLA grades answer export market labeling requirements. Converters that master coextrusion of bio-based outer layers with thin barrier tie layers are well positioned to capture premium positions as multinational FMCG buyers seek to decarbonize their regional portfolios.

The Thailand Flexible Packaging Market Report is Segmented by Product Type (Pouches, Bags, Films and Wraps, Sachets and Stick Packs, Labels and Sleeves, Flexitanks and Other Product Types), Material (Plastic, Aluminum Foil, Bioplastics, and More), End-User Industry (Food, Beverage, and More), Layer Structure (Mono-Material Structures, and Multilayer Barrier Laminates). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Amcor plc

- Thung Hua Sinn Group

- Huhtamaki Oyj

- Sealed Air Corporation

- T. Tarutani Pack Co Ltd

- SCG Packaging Public Co Ltd

- Mondi plc

- JR Pack Co Ltd

- Thai Artec Co Ltd

- TPBI Public Co Ltd

- Innopack Industry Co Ltd

- Scientex Packaging (Ayer Keroh) Berhad

- Kim Pai Co Ltd

- Print Master Co Ltd

- South East Packaging Industry Co Ltd

- LLH Printing and Packaging

- Majend Macks Co Ltd

- Fuji Seal International Inc.

- Royal Meiwa Pax Co Ltd

- Craftz Co Ltd

- Alpla (Thailand) Co Ltd

- Shrinkflex (Thailand) Public Co Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging E-commerce Parcel Volumes Accelerating Demand for Lightweight Mailing Packs

- 4.2.2 Boom in Thailand's Halal and Ready-to-Eat Food Exports Requiring High-Barrier Pouches

- 4.2.3 Bio-Circular-Green (BCG) Policy Subsidising Bioplastic Film Capacity Additions

- 4.2.4 Brand-Owner Shift to Mono-Material MDO-PE Film for Recyclability

- 4.2.5 Adoption of Industry 4.0 Flexo Presses Improving Short-Run Economics for SMEs

- 4.2.6 International FMCG Near-Shoring to Thailand amid China+1 Strategy

- 4.3 Market Restraints

- 4.3.1 Ban on Imported Plastic Scrap Tightening Local rPET/rPE Availability

- 4.3.2 Extended Producer Responsibility Draft Law Raising Compliance Costs

- 4.3.3 Skilled-Labour Shortage in Advanced Printing and Converting

- 4.3.4 Volatile Feedstock Prices Eroding Converter Margins

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Impact of Current Geo-Political Scenarios on the Market

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Buyers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitutes

- 4.9.5 Intensity of Competitive Rivalry

- 4.10 Vendor Level Presence in Major Verticals

- 4.11 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Pouches

- 5.1.2 Bags

- 5.1.3 Films and Wraps

- 5.1.4 Sachets and Stick Packs

- 5.1.5 Labels and Sleeves

- 5.1.6 Flexitanks and Other Product Types

- 5.2 By Material

- 5.2.1 Plastic

- 5.2.1.1 Polyethylene (PE)

- 5.2.1.2 Polypropylene (PP)

- 5.2.1.3 Polyethylene Terephthalate (PET)

- 5.2.1.4 Polyvinyl Chloride (PVC)

- 5.2.1.5 Other Plastics

- 5.2.2 Paper

- 5.2.3 Aluminum Foil

- 5.2.4 Bioplastics

- 5.2.5 Multilayer Barrier Structures

- 5.2.1 Plastic

- 5.3 By End-User Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Pharmaceuticals and Healthcare

- 5.3.5 Pet Food and Animal Feed

- 5.3.6 Home-Care and Industrial

- 5.3.7 E-Commerce and Logistics

- 5.4 By Layer Structure

- 5.4.1 Mono-Material Structures

- 5.4.2 Multilayer Barrier Laminates

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Amcor plc

- 6.4.2 Thung Hua Sinn Group

- 6.4.3 Huhtamaki Oyj

- 6.4.4 Sealed Air Corporation

- 6.4.5 T. Tarutani Pack Co Ltd

- 6.4.6 SCG Packaging Public Co Ltd

- 6.4.7 Mondi plc

- 6.4.8 JR Pack Co Ltd

- 6.4.9 Thai Artec Co Ltd

- 6.4.10 TPBI Public Co Ltd

- 6.4.11 Innopack Industry Co Ltd

- 6.4.12 Scientex Packaging (Ayer Keroh) Berhad

- 6.4.13 Kim Pai Co Ltd

- 6.4.14 Print Master Co Ltd

- 6.4.15 South East Packaging Industry Co Ltd

- 6.4.16 LLH Printing and Packaging

- 6.4.17 Majend Macks Co Ltd

- 6.4.18 Fuji Seal International Inc.

- 6.4.19 Royal Meiwa Pax Co Ltd

- 6.4.20 Craftz Co Ltd

- 6.4.21 Alpla (Thailand) Co Ltd

- 6.4.22 Shrinkflex (Thailand) Public Co Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

軟性包裝市場:按材料類型、包裝形式、技術、結構、最終用戶和分銷管道分類-全球市場預測(2026-2032 年)

軟性包裝市場:按材料類型、包裝形式、技術、結構、最終用戶和分銷管道分類-全球市場預測(2026-2032 年) 軟包裝數位印刷:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

軟包裝數位印刷:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 2034年環保軟包裝市場預測-全球材料、包裝類型、永續性類型、應用、最終用戶和地區分析

2034年環保軟包裝市場預測-全球材料、包裝類型、永續性類型、應用、最終用戶和地區分析 全球模組化包裝設備市場:成長機會、成長要素、產業趨勢分析及2026-2035年預測2034年全球軟包裝市場預測-按材料、產品類型、印刷技術、包裝形式、應用和地區分類的分析

全球模組化包裝設備市場:成長機會、成長要素、產業趨勢分析及2026-2035年預測2034年全球軟包裝市場預測-按材料、產品類型、印刷技術、包裝形式、應用和地區分類的分析 軟性包裝貼合黏劑市場:按產品類型、最終用戶和地區分類軟性鋁箔包裝市場:依包裝類型、材料類型、終端用戶產業及地區分類永續軟性包裝市場預測至2034年—按材料、包裝類型、應用、最終用戶和地區分類的全球分析紙本保護包裝市場預測至2034年-全球產品類型、材料類型、包裝形式、功能、分銷管道、最終用戶和區域分析軟性包裝市場:依材料、產品類型、應用、地區分類

軟性包裝貼合黏劑市場:按產品類型、最終用戶和地區分類軟性鋁箔包裝市場:依包裝類型、材料類型、終端用戶產業及地區分類永續軟性包裝市場預測至2034年—按材料、包裝類型、應用、最終用戶和地區分類的全球分析紙本保護包裝市場預測至2034年-全球產品類型、材料類型、包裝形式、功能、分銷管道、最終用戶和區域分析軟性包裝市場:依材料、產品類型、應用、地區分類