|

市場調查報告書

商品編碼

2071343

全球模組化包裝設備市場:成長機會、成長要素、產業趨勢分析及2026-2035年預測Global Modular Packaging Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

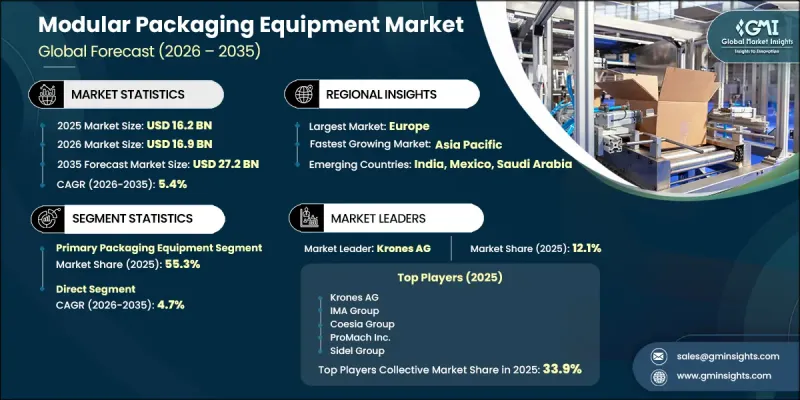

全球模組化包裝設備市場預計到 2025 年將達到 162 億美元,年複合成長率為 5.4%,到 2035 年將達到 272 億美元。

這項成長受到多種結構性因素的影響,包括產品系列日益複雜,需要快速切換能力;歐洲與包裝廢棄物減量政策相關的環境法規日趨嚴格;以及先進製造業經濟體持續存在的勞動力短缺問題。這些因素共同推動了模組化設備設計的普及,使製造商能夠在保持合規性和營運效率的同時,提高生產的靈活性。快速消費品 (FMCG) 和製藥業的需求尤其強勁,這些行業頻繁的產品變化、嚴格的品質標準和縮短的產品生命週期都要求生產基礎設施具有高度的適應性。製造商越來越重視能夠支援快速配置變更和可擴展生產能力的系統,從而更有效地應對不斷變化的市場需求。隨著生產環境持續朝向更高的柔軟性和自動化方向發展,模組化包裝設備正成為全球各產業下一代製造策略的核心要素。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 162億美元 |

| 預計金額 | 272億美元 |

| 複合年成長率 | 5.4% |

預計到2025年,初級包裝設備市佔率將達到55.3%,並在2035年之前維持5%的複合年成長率。食品、飲料和製藥業對灌裝、密封和成型系統的強勁需求,推動了該細分市場的持續主導地位。能夠處理各種產品形式的靈活生產線、嚴格的衛生要求以及不斷發展的材料標準,都在推動模組化初級包裝解決方案的普及。在製藥業,先進治療方法和特殊給藥方式的日益增多,進一步推動了對高度適應性和可重建設備系統的需求。

預計到2025年,銷售管道將佔據55.8%的市場佔有率,並在2035年之前以4.7%的複合年成長率成長。該通路包括設備製造商與最終用戶之間的直接互動,具體方式包括實施客製化系統、整合生產線解決方案和簽訂長期服務合約。對於需要客製化工程、系統驗證和持續技術支援的複雜製造設備而言,這仍然是首選模式。此外,直接採購模式能夠促進製造商和設備供應商之間更緊密的合作,從而最佳化系統效能並改善生命週期管理。

預計到2025年,北美模組化包裝設備市佔率將達到28.4%,並在2035年之前以4.3%的複合年成長率成長。該地區的需求主要由食品飲料和製藥製造業驅動,這些行業人事費用上升、監管合規要求日益嚴格以及對靈活生產能力的需求不斷成長,都推動了對模組化系統的投資。製造商擴大採用自動化和可重構包裝系統,以提高營運效率並減少與產品切換相關的停機時間,這進一步促進了該地區的市場成長。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 快速消費品和製藥業對 SKU 和快速規格轉換的需求不斷成長。

- 人事費用上升和熟練技術人員短缺正在推動自動化技術的應用。

- 電子商務的發展和直接向消費者出貨的擴大,對靈活的生產線配置提出了要求。

- 產業潛在風險與挑戰

- 標準化差距-多廠商模組化組件之間的互通性

- 工業物聯網連接的模組化包裝生產線的網路安全風險

- 機會

- 亞太地區及中東和非洲(MEA)包裝產業的工業化和現代化

- 模組化即服務 (MaaS) 與設備即服務 (EaaS)經營模式的實施

- 促進因素

- 成長潛力分析

- 監理框架

- 標準和合規要求

- 區域監理框架

- 認證標準

- 關鍵市場趨勢與顛覆性因素

- 技術與創新展望

- 當前趨勢

- 新進展

- 價格分析

- 對過去價格趨勢的分析

- 依球員類型分類的定價策略(高級球員、超值球員、成本加成球員)

- 未來市場趨勢

- 貿易數據分析

- 進出口量及進口額趨勢

- 主要貿易路線及關稅的影響

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 按細分市場分類的生成式人工智慧用例和部署藍圖

- 風險、限制和監管考量

- 波特的分析

- PESTLE分析

- 生產能力和生產情況

- 設備產能:按地區和主要生產商分類

- 運轉率和擴張計劃

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 初級包裝設備

- 灌裝機

- 封口機

- 貼標機

- 編碼和標記裝置

- 二級包裝設備

- 裝盒機

- 箱包裝系統

- 收縮包裝機

- 碼垛裝置

- 三級包裝設備

- 拉伸帽系統

- 單元化和綁帶緊固系統

第6章 市場估算與預測:依自動化程度分類,2022-2035年

- 手動模組化設備

- 半自動系統

- 自動化系統

第7章 市場估計與預測:依最終用途分類,2022-2035年

- 食品/飲料

- 製藥

- 化妝品和個人護理

- 化學物質和殺蟲劑

- 電子設備

- 其他(汽車等)

第8章 市場估算與預測:依通路分類,2022-2035年

- 直接的

- 間接

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- UAE

- 沙烏地阿拉伯

- 南非

第10章:公司簡介

- 世界公司

- Coesia Group

- Business Overview

- Financial Data

- Product Landscape

- Strategic Outlook

- SWOT Analysis

- IMA Group

- Krones AG

- Multivac Group

- ProMach Inc.

- Sidel Group

- Syntegon Technology

- Coesia Group

- 當地公司

- Fuji Machinery Co., Ltd.

- Ishida Co., Ltd.

- Marchesini Group

- Optima Packaging Group

- Robopac/Aetna Group

- Truking Technology Ltd.

- ULMA Packaging

- 新興企業

- Cama Group

- Combi Packaging Systems

- Massman Companies

- Mpac Group plc

- Nichrome India Pvt. Ltd.

- Schubert Group

- TNA Solutions

The Global Modular Packaging Equipment Market was valued at USD 16.2 billion in 2025 and is estimated to grow at a CAGR of 5.4% to reach USD 27.2 billion by 2035.

Growth is shaped by multiple structural forces, including the increasing complexity of product portfolios that require rapid changeover capabilities, stricter environmental regulations linked to packaging waste reduction policies in Europe, and ongoing labor shortages in advanced manufacturing economies. These combined factors are accelerating the adoption of modular equipment designs that allow manufacturers to enhance production agility while maintaining regulatory compliance and operational efficiency. Demand is particularly strong across fast-moving consumer goods and pharmaceutical manufacturing, where frequent product variation, strict quality standards, and shorter product life cycles require highly adaptable production infrastructure. Manufacturers are increasingly prioritizing systems that support rapid configuration changes and scalable production capacity, enabling them to respond more effectively to shifting market requirements. As production environments continue to evolve toward higher flexibility and automation, modular packaging equipment is becoming a core component of next-generation manufacturing strategies across global industries.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $16.2 Billion |

| Forecast Value | $27.2 Billion |

| CAGR | 5.4% |

The primary packaging equipment segment accounted for 55.3% share in 2025 and is projected to grow at a CAGR of 5% through 2035. This segment continues to lead due to strong demand for filling, sealing, and forming systems across food, beverage, and pharmaceutical applications. The need for flexible production lines capable of handling diverse product formats, strict hygiene requirements, and evolving material standards is reinforcing the adoption of modular primary packaging solutions. In pharmaceutical manufacturing, the increasing production of advanced therapies and specialized drug delivery formats is further strengthening demand for adaptable and reconfigurable equipment systems.

The direct distribution channel represented 55.8% share in 2025 and is expected to grow at a CAGR of 4.7% through 2035. This channel includes direct engagement between equipment manufacturers and end users through customized system deployment, integrated production line solutions, and long-term service agreements. It remains the preferred model for complex manufacturing installations that require tailored engineering, system validation, and ongoing technical support. Direct procurement structures also enable closer collaboration between manufacturers and equipment providers, improving system performance optimization and lifecycle management.

North America Modular Packaging Equipment Market held a 28.4% share in 2025 and is projected to grow at a CAGR of 4.3% through 2035. Demand in the region is primarily driven by food and beverage as well as pharmaceutical manufacturing sectors, where investment in modular systems is supported by increasing labor costs, strict regulatory compliance requirements, and rising demand for flexible production capabilities. Manufacturers are increasingly adopting automated and reconfigurable packaging systems to improve operational efficiency and reduce downtime associated with product changeovers, further supporting regional market growth.

Key companies operating in the Global Modular Packaging Equipment Market include Coesia Group, Syntegon Technology, Krones AG, Multivac Group, IMA Group, Schubert Group, ProMach Inc., Sidel Group, Optima Packaging Group, Ishida Co., Ltd., ULMA Packaging, Marchesini Group, Robopac / Aetna Group, Fuji Machinery Co., Ltd., TNA Solutions, Mpac Group plc, Nichrome India Pvt. Ltd., Combi Packaging Systems, Massman Companies, Truking Technology Ltd., and Cama Group. Companies operating in the modular packaging equipment market are focusing on advanced automation integration, system modularity enhancement, and digitalization of packaging operations to strengthen their competitive position. Manufacturers are investing in smart equipment technologies, predictive maintenance capabilities, and IoT-enabled production monitoring systems to improve efficiency and reduce downtime. Strategic partnerships with end-use industries are enabling the co-development of customized packaging solutions tailored to specific production requirements. Companies are also expanding global service networks and aftermarket support capabilities to enhance customer retention and lifecycle value. In addition, firms are emphasizing sustainability-driven innovation, including energy-efficient machinery designs and reduced material waste systems, to align with evolving environmental regulations.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.2.1 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Region

- 2.2.2 Type

- 2.2.3 Automation Level

- 2.2.4 End Use

- 2.2.5 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising SKU proliferation & demand for rapid format changeover across FMCG & pharma

- 3.2.1.2 Labor cost escalation & skilled technician shortages driving automation adoption

- 3.2.1.3 Growth of e-commerce & direct-to-consumer fulfillment requiring flexible line configurations

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Standardization gaps- interoperability between multi-vendor modular components

- 3.2.2.2 Cybersecurity risks in IIoT-connected modular packaging lines

- 3.2.3 Opportunities

- 3.2.3.1 Industrialization & packaging modernization in Asia Pacific & MEA

- 3.2.3.2 Modular-as-a-service (MaaS) & equipment-as-a-service (EaaS) business model adoption

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory framework

- 3.4.1 Standards & Compliance Requirements

- 3.4.2 Regional Regulatory Frameworks

- 3.4.3 Certification Standards

- 3.5 Major market trends and disruptions

- 3.6 Technology/innovation landscape

- 3.6.1 Current trends

- 3.6.2 Emerging trends

- 3.7 Pricing Analysis (driven by primary research)

- 3.7.1 Historical price trend analysis (driven by primary research)

- 3.7.2 Pricing strategy by player type (premium / value / cost-plus) (driven by primary research)

- 3.8 Future market trends

- 3.9 Trade data analysis (driven by paid database) (HS Code-8422)

- 3.9.1 Import/export volume & value trends (driven by primary research)

- 3.9.2 Key trade corridors & tariff impact (driven by primary research)

- 3.10 Impact of AI & Generative AI on the Market

- 3.10.1 AI-driven disruption of existing business models

- 3.10.2 Gen-AI use cases & adoption roadmap by segment

- 3.10.3 Risks, limitations & regulatory considerations

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

- 3.13 Capacity & production landscape (driven by primary research)

- 3.13.1 Installed capacity by region & key producer (driven by primary research)

- 3.13.2 Capacity utilization rates & expansion pipelines(driven by primary research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Primary Packaging Equipment

- 5.2.1 Filling Machines

- 5.2.2 Sealing Machines

- 5.2.3 Labeling Machines

- 5.2.4 Coding & Marking Equipment

- 5.3 Secondary Packaging Equipment

- 5.3.1 Cartoning Machines

- 5.3.2 Case Packing Systems

- 5.3.3 Shrink Wrapping Machines

- 5.3.4 Palletizing Equipment

- 5.4 Tertiary Packaging Equipment

- 5.4.1 Stretch Hooding Systems

- 5.4.2 Unitizing & Strapping Systems

Chapter 6 Market Estimates and Forecast, By Automation Level, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Manual modular equipment

- 6.3 Semi-automatic systems

- 6.4 Automatic systems

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Food and beverage

- 7.3 Pharmaceuticals

- 7.4 Cosmetics and personal care

- 7.5 Chemical and agrochemical

- 7.6 Electronics

- 7.7 Others (automotive, etc.)

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Direct

- 8.3 Indirect

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 U.K.

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Global Companies

- 10.1.1 Coesia Group

- 10.1.1.1 Business Overview

- 10.1.1.2 Financial Data

- 10.1.1.3 Product Landscape

- 10.1.1.4 Strategic Outlook

- 10.1.1.5 SWOT Analysis

- 10.1.2 IMA Group

- 10.1.3 Krones AG

- 10.1.4 Multivac Group

- 10.1.5 ProMach Inc.

- 10.1.6 Sidel Group

- 10.1.7 Syntegon Technology

- 10.1.1 Coesia Group

- 10.2 Regional Companies

- 10.2.1 Fuji Machinery Co., Ltd.

- 10.2.2 Ishida Co., Ltd.

- 10.2.3 Marchesini Group

- 10.2.4 Optima Packaging Group

- 10.2.5 Robopac / Aetna Group

- 10.2.6 Truking Technology Ltd.

- 10.2.7 ULMA Packaging

- 10.3 Emerging Companies

- 10.3.1 Cama Group

- 10.3.2 Combi Packaging Systems

- 10.3.3 Massman Companies

- 10.3.4 Mpac Group plc

- 10.3.5 Nichrome India Pvt. Ltd.

- 10.3.6 Schubert Group

- 10.3.7 TNA Solutions

軟包裝數位印刷:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

軟包裝數位印刷:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 2034年環保軟包裝市場預測-全球材料、包裝類型、永續性類型、應用、最終用戶和地區分析2034年全球軟包裝市場預測-按材料、產品類型、印刷技術、包裝形式、應用和地區分類的分析

2034年環保軟包裝市場預測-全球材料、包裝類型、永續性類型、應用、最終用戶和地區分析2034年全球軟包裝市場預測-按材料、產品類型、印刷技術、包裝形式、應用和地區分類的分析 軟性鋁箔包裝市場:依包裝類型、材料類型、終端用戶產業及地區分類永續軟性包裝市場預測至2034年—按材料、包裝類型、應用、最終用戶和地區分類的全球分析紙本保護包裝市場預測至2034年-全球產品類型、材料類型、包裝形式、功能、分銷管道、最終用戶和區域分析

軟性鋁箔包裝市場:依包裝類型、材料類型、終端用戶產業及地區分類永續軟性包裝市場預測至2034年—按材料、包裝類型、應用、最終用戶和地區分類的全球分析紙本保護包裝市場預測至2034年-全球產品類型、材料類型、包裝形式、功能、分銷管道、最終用戶和區域分析 軟性包裝市場:按材料、包裝形式、技術、結構、最終用戶和分銷管道分類-2026-2032年全球市場預測軟性包裝市場:依材料、產品類型、應用、地區分類軟性工業包裝市場:按材料、產品類型、包裝形式、最終用途和分銷管道分類-2026-2032年全球市場預測泰國軟包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

軟性包裝市場:按材料、包裝形式、技術、結構、最終用戶和分銷管道分類-2026-2032年全球市場預測軟性包裝市場:依材料、產品類型、應用、地區分類軟性工業包裝市場:按材料、產品類型、包裝形式、最終用途和分銷管道分類-2026-2032年全球市場預測泰國軟包裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)