|

市場調查報告書

商品編碼

2072472

垂直農業:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Vertical Farming - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

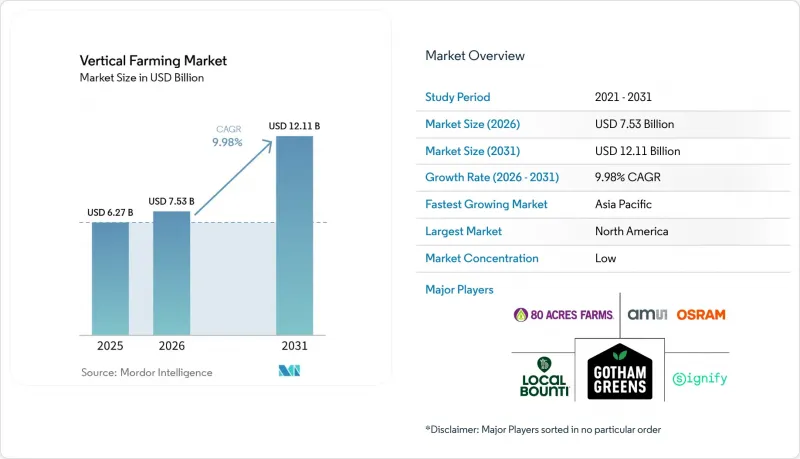

據 Mordor Intelligence 稱,2025 年垂直農業市場價值為 62.7 億美元,預計到 2031 年將達到 121.1 億美元,而 2026 年為 75.3 億美元,預測期(2026-2031 年)複合年成長率為 9.98%。

本報告按栽培方法(水耕、氣耕、魚菜共生)、農場結構(如垂直農場)、組件(如照明、氣候控制)、作物類型(如番茄、漿果、生菜和綠葉、辣椒)以及地區(例如北美、南美、歐洲)進行分類。市場預測以美元計價。

全球垂直農業市場趨勢與洞察

都市區對本地生產的、不含農藥的農產品的需求

都市區對本地種植的有機農產品的需求是垂直農業市場的重要商業性驅動力,尤其是在人口密集的大都會圈的大型食品零售商和餐飲批發商中。北美領先的可控環境農業公司 Gotham Greens 在 2026 年 2 月報告稱,其在美國室內種植的包裝沙拉、生菜和香草的市場總合已接近 10%,在截至 2026 年 1 月的 13 週零售統計期內同比成長 22%。這表明室內種植的農產品正從小眾高階產品類別轉向更廣泛的市場。這一趨勢意義重大,因為垂直農業市場不僅在「有機」標籤方面具有競爭力,而且在可預測的全年供應方面也具有優勢,這使得零售商能夠減少安全庫存並更有效地管理補貨。此外,在大都會圈消費中心附近種植農產品由於其卓越的新鮮度,在分銷方面具有優勢。更短的運輸時間延長了保存期限並降低了降價壓力。因此,垂直農業市場在零售商中越來越受歡迎,這些零售商將可靠性、來源和減少廢棄物作為一個整體來考慮,而不是將這些因素作為單獨的購買因素。

降低LED、機器人和感測器技術的成本。

設備成本的降低仍然是垂直農業市場成長最顯著的促進因素之一,提高了新安裝和升級的資本效率。 Signify於2025年6月推出了飛利浦GrowWise智慧頻譜系統,宣布該平台可透過基於即時日照條件的自動頻譜調節,實現高達6%的節能或提高作物生長。 2026年3月發表在《植物科學前沿》(Frontiers in Plant Science)上的一項研究表明,在測試條件下,持續低強度LED照明可將生菜的能源效率提高21%,並將LED運行成本降低16.5%,且不會導致產量下降。同樣在2026年3月,英國農業技術中心報告稱,其先進作物動態控制試驗透過植物主導的照明控制,將能源效率提高了21%至25%,儘管該系統仍處於早期整合階段。因此,垂直農業市場的採購經濟模式正在發生重大調整。這是因為,那些推遲採購的企業現在可以評估比以往創業投資主導的建設週期中引入的硬體和自動化系統更有效率的系統。

高電力負荷和資本密集度

全封閉式生產系統依賴高能耗的照明和氣候控制基礎設施,這使得營運成本成為垂直農業市場最大的阻礙因素之一。在室內農場中,人工LED照明通常消耗最大的電力,而用於維持穩定生長環境的冷卻、通風和除濕系統也會顯著增加營運成本。在工業電價較高的地區,這些成本壓力尤其嚴峻,限制了低利潤作物的商業性可行性,並促使該行業更加專注於高階綠葉和特色產品。本地公司Bounty Corporation向美國證券交易委員會(SEC)提交的文件凸顯了資本結構在該行業的重要性。該公司計劃在2025年至2026年間重組債務並獲得成長資金,同時繼續最佳化產量和產能。因此,垂直農業市場仍面臨根本性的限制:技術可行性並不一定能轉化為財務上的永續發展。

細分市場分析

水耕法是垂直農業市場中最大的種植方式,預計到2025年將佔56.7%的市場。其主導地位源自於其在營養輸送、種植週期控制和根區管理方面長期累積的商業成功經驗,並已應用於多種室內農場模式。此外,水耕法仍是應用最廣泛的種植方式,2018年至2023年間,眾多業者的投資都基於此系統結構。這項成功經驗持續影響垂直農業產業的採購、生產者培訓和材料供應。因此,即使不斷推出新的系統改進方案,市佔率的重新分配也進展緩慢。

氣耕是成長最快的垂直農業技術,預計2026年至2031年間,其在垂直農業市場的複合年成長率將達到13.1%。此模式對那些尋求更佳根區衛生和更高節水效果的企業極具吸引力,超越了傳統循環水耕系統所能提供的標準。魚菜共生技術也日益受到關注,其循環食物系統和雙重收入來源使其儘管運作複雜性較高,但仍具有應用價值。 2025年8月,JR東日本創業平台宣布成立資本與商業聯盟,旨在將基於魚菜共生技術的循環食物生產商業化。此前,該公司已將其魚菜共生設施擴展至日本的五個地點。此舉印證了垂直農業市場正逐步向綜合食物系統轉型,而非突然放棄水耕技術的觀點。

建築型農場是垂直農業市場中最大的細分市場,預計到2025年將佔垂直農業市場規模的72.4%。這種主導地位反映了其在更大產能、更整合的氣候控制系統以及大規模吸收固定成本的優勢。此外,與許多小規模的模組化專案相比,這些專案由於其更清晰的營運模式,往往更容易吸引機構資本。實際上,規模最大的建築型設施仍是大都會圈供應鏈中垂直農業市場擴張的標竿。這種地位使得此類設施在旨在實現大規模生產的商業規劃中佔據核心地位。

貨櫃式農場是成長最快的垂直農業結構,預計2026年至2031年將以12.3%的複合年成長率成長。其吸引力在於部署迅速、地理柔軟性,並且能夠輕鬆進入供不應求的地區。 2025年7月,Freight Farms公司(旗下擁有500多個運作中的貨櫃式農場)的資產轉讓給Grocer公司,這表明即使原公司破產,對貨櫃式系統的需求依然存在。杜拜的GigaFarm計畫則代表了另一種截然不同的模式。該計畫計畫建造200座生長塔,其中首批20座的組件已於2025年交付,計畫年產量目標為3,000噸。綜上所述,這些趨勢表明,在垂直農業市場,貨櫃式農場和建築式農場不僅是替代方案,更是在市場准入和業務擴張的各個階段的互補工具。

區域分析

北美是垂直農業市場最大的區域貢獻者,預計到2025年將佔據41.8%的市場。該地區受益於密集的大都會圈零售網路、成熟的低溫運輸系統以及支持室內農業規模化發展的技術資本集中。本地企業Bounti Corporation預計2025會計年度的銷售額將達到4,837萬美元,產品將供應給約13,000家門市,顯示一些美國營運商已經實現了商業性覆蓋範圍的擴大。加拿大作為第二大中心的地位也不斷鞏固。 GoodLeaf Farms於2025年11月籌集了3,790萬美元(5,200萬加元),用於將其在亞伯達和魁北克省的工廠產能翻番,並在安大略省新建一個研發中心。

亞太地區是垂直農業市場成長最快的區域,預計2026年至2031年將以12.8%的複合年成長率成長。土地稀缺、食品安全期望的提高以及日本、中國、新加坡和韓國政府對保護性農業的大力主導,是推動這一成長的主要因素。中國2026年的政策指導方針正式支持保護性農業的現代化,並更廣泛地應用人工智慧、物聯網、機器人和無人機等技術,從而鞏固了該地區的長期發展基礎。中東在垂直農業市場也佔有重要的戰略地位,Bustanica計畫在2026年將業務拓展至零售、旅館和大型餐飲領域。非洲和南美洲的垂直農業市場仍處於起步階段,專案活動有限,初期更有可能採用都市區營養供應和模組化部署模式,而非立即進行大規模商業擴張。

歐洲垂直農業市場錯綜複雜,消費者對本地種植的室內農產品需求強勁,但同時也面臨不斷上漲的電力成本和日益嚴格的資金籌措條件。儘管Ocado集團多次提供資金支持,Jones Food Company Limited仍於2025年4月進入破產管理程序。這表明,在盈利無法得到保障的情況下,成本壓力會如何阻礙企業規模擴張。另一方面,歐洲在技術發展方面仍然具有重要影響力,尤其是在照明、控制系統和工程平台領域,荷蘭、義大利和英國擁有強大的實力。思科於2026年4月與Planet Farms Holding SpA達成合作,顯示歐洲在自主室內農業基礎設施領域正積極發展,並計劃將業務拓展至英國和北歐市場。因此,歐洲對垂直農業市場仍然至關重要,但與其他一些地區相比,其成長路徑將更容易受到能源成本和嚴格的資本管理的影響。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 都市區對本地生產的、不含農藥的農產品的需求

- 降低LED、機器人和感測技術的成本。

- 全年生產,適應氣候變遷

- 政府為保障糧食安全和發展農業技術提供獎勵和資金支持

- 透過排碳權和ESG溢價累積收入

- 結合廢熱和低成本電力帶來的經濟效益。

- 市場限制因素

- 高電力負荷和資本密集度

- 在大規模種植中,具有經濟效益的作物種類是有限的。

- 該行業崩潰後,貸款機構和保險公司收緊了信貸標準。

- 食品安全和生物風險保險保費上漲。

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 透過生長機制

- 水耕法

- 氣耕

- 水耕法

- 按農場結構

- 建築型垂直農場

- 貨櫃式垂直農場

- 按組件

- 照明系統

- 氣候控制系統

- 感測器和監控設備

- 灌溉和施肥系統

- 軟體和控制平台

- 農場建築材料及栽培架

- 按作物類型

- 生菜和綠葉蔬菜

- 草藥

- 番茄

- 莓果

- 黃瓜

- 青椒

- 微型菜苗

- 其他作物

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 其他北美國家

- 歐洲

- 德國

- 英國

- 法國

- 荷蘭

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 新加坡

- 韓國

- 澳洲

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美國家

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 以色列

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 肯亞

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- 80 Acres Farms Inc.

- Gotham Greens Holdings LLC

- Local Bounti Corporation

- Crop One Holdings Inc.

- Oishii Farm Corporation

- GrowUp Farms Limited

- Planet Farms Holding SpA

- Jones Food Company Limited

- Intelligent Growth Solutions Limited

- Urban Crop Solutions BV

- Signify NV

- ams-OSRAM AG

- Heliospectra AB

- Green Sense Farms Holdings, Inc.

- Vertical Future Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the vertical farming market size was valued at USD 6.27 billion in 2025 and estimated to grow from USD 7.53 billion in 2026 to reach USD 12.11 billion by 2031, at a CAGR of 9.98% during the forecast period (2026-2031).

This report is Segmented by Growing Mechanism (Hydroponics, Aeroponics, and Aquaponics), by Farm Structure (Building-Based Vertical Farms and More), by Components (Lighting, Climate Control, and More), by Crop Type (Tomato, Berries, Lettuce and Leafy Greens, Pepper, and More), and by Geography (North America, South America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Vertical Farming Market Trends and Insights

Urban Demand for Local Pesticide-Free Produce

Urban demand for locally grown, pesticide-free produce has become a significant commercial driver for the vertical farming market, particularly among large grocery retailers and foodservice distributors in densely populated metropolitan areas. Gotham Greens, a major controlled-environment agriculture operator in North America, reported in February 2026 that the combined United States market share for indoor-grown packaged salads, lettuce, and herbs reached nearly 10%, with a 22% year-over-year increase during the 13-week retail measurement period ending January 2026. This indicates that indoor produce is transitioning from a niche premium shelf category to a broader market presence. This trend is important because the vertical farming market competes not only on pesticide-free labeling but also on predictable, year-round delivery, enabling retailers to reduce safety stock and manage replenishment more efficiently. Additionally, freshness offers a distribution advantage when produce is grown near metropolitan consumption hubs, as shorter transport times extend shelf life and reduce markdown pressures. As a result, the vertical farming market is gaining traction in retail accounts where reliability, provenance, and waste reduction are prioritized collectively rather than as separate purchasing factors.

Falling LED, Robotics, and Sensing Costs

Falling equipment costs remain one of the clearest growth supports for the vertical farming market because they improve the capital efficiency of new installations and upgrades. Signify launched its Philips GrowWise smart spectrum system in June 2025 and stated that the platform can deliver up to 6% energy savings or crop growth improvement through automatic spectral adjustment based on real-time sunlight conditions. A March 2026 study in Frontiers in Plant Science found that continuous, low-intensity LED lighting improved energy use efficiency by 21% and reduced LED application costs by 16.5% for lettuce, without yield loss under the tested conditions. The United Kingdom Agri-Tech Center also reported in March 2026 that its Advanced Crop Dynamic Control trial improved energy efficiency by 21% to 25% through plant-led lighting control, even while the system remained at an early stage of integration. As a result, the vertical farming market is seeing a practical reset in procurement economics, as operators who delayed purchases can now evaluate more efficient hardware and automation systems than those installed during the earlier venture-heavy build cycle.

High Electricity Load and Capital Intensity

Operating economics remain one of the largest constraints in the vertical farming market because fully enclosed production systems depend on energy-intensive lighting and climate-control infrastructure. Artificial LED lighting typically accounts for the largest electricity load in indoor farms, while cooling, ventilation, and dehumidification systems add substantial operating costs to maintain stable growing conditions. These cost pressures are especially challenging in regions with high industrial electricity prices, limiting the commercial viability of lower-margin crop categories and reinforcing industry focus on premium leafy greens and specialty produce. Local Bounti Corporation's filings with the U.S. Securities and Exchange Commission (SEC) underline how capital structure remains critical in this space, with the company reshaping debt and adding growth capital during 2025 and 2026 while continuing to optimize yields and capacity . The vertical farming market, therefore, continues to face a fundamental constraint: technical feasibility does not always translate into financially sustainable deployment.

Other drivers and restraints analyzed in the detailed report include:

- Climate-Resilient Year-Round Production

- Government Food-Security Incentives and Ag-Tech Funding

- Limited Economically Viable Crop Basket at Scale

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hydroponics was the largest growing mechanism in the vertical farming market, with a 56.7% share in 2025. Its lead came from a long commercial record in nutrient delivery, crop-cycle control, and root-zone management across several indoor farm formats. The hydroponic installed base also remained the deepest because many operator investments made between 2018 and 2023 were built around this system architecture. That installed base still shapes procurement, grower training, and input sourcing in the vertical farming industry. As a result, share rebalancing remains gradual even as newer systems improve.

Aeroponics is the fastest-growing technology and is projected to expand at a 13.1% CAGR during 2026-2031 in the vertical farming market. The model appeals to operators seeking better root-zone hygiene and additional water savings beyond those offered by standard recirculating hydroponic systems. Aquaponics is also gaining attention, where circular food systems and dual revenue streams can justify more operational complexity. JR East Startup and Platform announced a capital and business alliance in August 2025 to commercialize aquaponics-based circular food production, as its aquaponics facilities expanded to 5 sites across Japan. That supports the view that the vertical farming market is slowly expanding into integrated food systems rather than moving away from hydroponics all at once.

Building-based farms were the largest segment, accounting for 72.4% if the vertical farming market size in 2025. Their lead reflects a larger productive capacity, more integrated climate systems, and better fixed-cost absorption at a commercial scale. These projects also tend to attract institutional capital more easily because their operating models are clearer than in many smaller modular deployments. In practice, the largest building-based assets still set the benchmark for how the vertical farming market scales in metropolitan supply chains. That position has kept this structure at the center of high-volume commercial planning.

Shipping-container-based farms were the fastest-growing structure and are projected to grow at a 12.3% CAGR during 2026-2031. Their appeal comes from rapid deployment, geographic flexibility, and lower commitment for operators entering undersupplied regions. The July 2025 transfer of Freight Farms assets to Growcer, which included more than 500 active container farm locations, showed that demand for container-based systems persisted even after the original company failed. The Dubai GigaFarm project also highlights the other end of the scale spectrum, with the first components for the initial 20 of 200 planned growth towers shipped in 2025, and full project output targeted at 3,000 metric tons annually. Taken together, these patterns show that the vertical farming market uses container and building-based formats less as substitutes and more as complementary tools for different stages of market entry and scale-up.

Complete Report Scope:

- By Growing Mechanism

- Hydroponics

- Aeroponics

- Aquaponics

- By Farm Structure

- Building-based Vertical Farms

- Shipping-container-based Vertical Farms

- By Component

- Lighting Systems

- Climate Control Systems

- Sensors and Monitoring Devices

- Irrigation and Fertigation Systems

- Software and Control Platforms

- Farm Structure Materials and Growing Racks

- By Crop Type

- Lettuce and Leafy Greens

- Herbs

- Tomatoes

- Berries

- Cucumbers

- Peppers

- Microgreens

- Other Crops

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- France

- Netherlands

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Singapore

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Middle East

- United Arab Emirates

- Saudi Arabia

- Israel

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Kenya

- Egypt

- Rest of Africa

- North America

Geography Analysis

North America was the largest regional contributor to the vertical farming market, accounting for 41.8% of the market share in 2025. The region benefits from dense metropolitan retail networks, established cold-chain systems, and a concentration of technology capital that supports the scale of indoor farming. Local Bounti Corporation reported FY2025 sales of USD 48.37 million and serves around 13,000 retail doors, demonstrating the commercial reach already achieved by some United States operators. Canada continues to strengthen its position as a secondary hub, with GoodLeaf Farms raising USD 37.9 million (CAD 52 million) in November 2025, to double capacity at its Alberta and Quebec sites and to build a new research and development center in Ontario.

Asia-Pacific was the fastest-growing regional segment in the vertical farming market and is projected to grow at a 12.8% CAGR during 2026-2031. Land scarcity, food safety expectations, and stronger state-backed support for facility agriculture across Japan, China, Singapore, and South Korea are shaping growth. China's 2026 policy direction formally supports upgrades in facility agriculture and the broader use of artificial intelligence, the Internet of Things, robots, and drones, which strengthens the region's long-term deployment base. The Middle East also carries strong strategic weight in the vertical farming market, with Bustanica broadening its commercial reach into retail, hospitality, and large-scale catering in 2026. Africa and South America remain early-stage opportunities in the vertical farming market, with project activity still more limited and more likely to build first through smaller urban nutrition and modular deployment models than through immediate large-scale commercial rollouts.

Europe presents a more mixed picture in the vertical farming market, as strong consumer demand for local indoor produce sits alongside elevated electricity costs and tighter financing conditions. Jones Food Company Limited entered administration in April 2025 after repeated rounds of funding support from Ocado Group, illustrating how cost pressure can overwhelm scale ambition when profitability remains out of reach. At the same time, the region remains influential in technology development, especially through lighting, control systems, and engineering platforms tied to the Netherlands, Italy, and the United Kingdom. Cisco's April 2026 work with Planet Farms Holding S.p.A. signals that Europe remains active in autonomous indoor farming infrastructure and in planned geographic expansion to the United Kingdom and Nordic markets. Europe, therefore, remains important to the vertical farming market, but its growth path depends more tightly on energy costs and capital discipline than in some other regions.

- 80 Acres Farms Inc.

- Gotham Greens Holdings LLC

- Local Bounti Corporation

- Crop One Holdings Inc.

- Oishii Farm Corporation

- GrowUp Farms Limited

- Planet Farms Holding S.p.A.

- Jones Food Company Limited

- Intelligent Growth Solutions Limited

- Urban Crop Solutions BV

- Signify N.V.

- ams-OSRAM AG

- Heliospectra AB

- Green Sense Farms Holdings, Inc.

- Vertical Future Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Urban demand for local pesticide-free produce

- 4.2.2 Falling LED, robotics, and sensing costs

- 4.2.3 Climate-resilient year-round production

- 4.2.4 Government food-security incentives and ag-tech funding

- 4.2.5 Carbon-credit and ESG premium revenue stacking

- 4.2.6 Waste-heat and low-cost power co-location economics

- 4.3 Market Restraints

- 4.3.1 High electricity load and capital intensity

- 4.3.2 Limited economically viable crop basket at scale

- 4.3.3 Tighter lender and insurer underwriting after sector failures

- 4.3.4 Food-safety and biologic-risk insurance inflation

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Growing Mechanism

- 5.1.1 Hydroponics

- 5.1.2 Aeroponics

- 5.1.3 Aquaponics

- 5.2 By Farm Structure

- 5.2.1 Building-based Vertical Farms

- 5.2.2 Shipping-container-based Vertical Farms

- 5.3 By Component

- 5.3.1 Lighting Systems

- 5.3.2 Climate Control Systems

- 5.3.3 Sensors and Monitoring Devices

- 5.3.4 Irrigation and Fertigation Systems

- 5.3.5 Software and Control Platforms

- 5.3.6 Farm Structure Materials and Growing Racks

- 5.4 By Crop Type

- 5.4.1 Lettuce and Leafy Greens

- 5.4.2 Herbs

- 5.4.3 Tomatoes

- 5.4.4 Berries

- 5.4.5 Cucumbers

- 5.4.6 Peppers

- 5.4.7 Microgreens

- 5.4.8 Other Crops

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Netherlands

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Singapore

- 5.5.3.5 South Korea

- 5.5.3.6 Australia

- 5.5.3.7 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Chile

- 5.5.4.4 Rest of South America

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Israel

- 5.5.5.4 Turkey

- 5.5.5.5 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Kenya

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 80 Acres Farms Inc.

- 6.4.2 Gotham Greens Holdings LLC

- 6.4.3 Local Bounti Corporation

- 6.4.4 Crop One Holdings Inc.

- 6.4.5 Oishii Farm Corporation

- 6.4.6 GrowUp Farms Limited

- 6.4.7 Planet Farms Holding S.p.A.

- 6.4.8 Jones Food Company Limited

- 6.4.9 Intelligent Growth Solutions Limited

- 6.4.10 Urban Crop Solutions BV

- 6.4.11 Signify N.V.

- 6.4.12 ams-OSRAM AG

- 6.4.13 Heliospectra AB

- 6.4.14 Green Sense Farms Holdings, Inc.

- 6.4.15 Vertical Future Ltd.

7 Market Opportunities and Future Outlook

美國垂直農業:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

美國垂直農業:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年) 垂直農業市場機會、成長要素、產業趨勢分析及2026-2035年預測

垂直農業市場機會、成長要素、產業趨勢分析及2026-2035年預測 垂直農業市場分析與預測(至2035年):按類型、產品、服務、技術、組件、應用、最終用戶、安裝方法、設備和解決方案分類

垂直農業市場分析與預測(至2035年):按類型、產品、服務、技術、組件、應用、最終用戶、安裝方法、設備和解決方案分類 垂直漿果種植市場預測至2034年—全球分析(按漿果類型、栽培技術、組件、自動化程度、設施類型、應用、最終用戶、分銷管道和地區分類)

垂直漿果種植市場預測至2034年—全球分析(按漿果類型、栽培技術、組件、自動化程度、設施類型、應用、最終用戶、分銷管道和地區分類) 垂直農業市場:2026-2032年全球市場預測(依產品形式、照明類型、作物類型、系統、安裝形式和最終用戶分類)

垂直農業市場:2026-2032年全球市場預測(依產品形式、照明類型、作物類型、系統、安裝形式和最終用戶分類) 垂直農業市場報告:按組成部分、結構、成長要素、應用和地區分類(2026-2034 年)

垂直農業市場報告:按組成部分、結構、成長要素、應用和地區分類(2026-2034 年) 2026年全球垂直農業市場報告2034年室內農業產品市場預測-按產品類型、種植方法、設施類型、種植規模、最終用戶和地區分類的全球分析

2026年全球垂直農業市場報告2034年室內農業產品市場預測-按產品類型、種植方法、設施類型、種植規模、最終用戶和地區分類的全球分析 垂直農業市場:依種植方法、結構、組件、作物、地區分類全球超當地語系化垂直農場市場預測至2034年:按農場類型、種植機制、組成部分、部署形式、作物類型、經營模式、最終用戶和地區分類的分析

垂直農業市場:依種植方法、結構、組件、作物、地區分類全球超當地語系化垂直農場市場預測至2034年:按農場類型、種植機制、組成部分、部署形式、作物類型、經營模式、最終用戶和地區分類的分析