|

市場調查報告書

商品編碼

2072466

義大利可再生能源:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)Italy Renewable Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

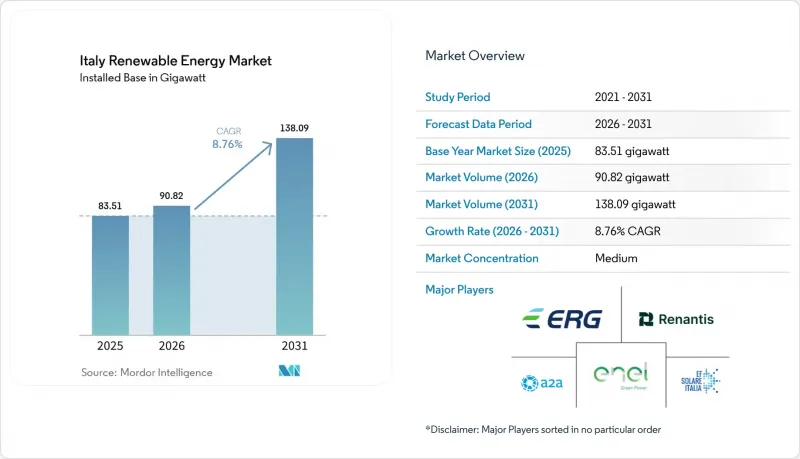

根據 Mordor Intelligence 估計,到 2026 年,義大利可再生能源市場規模將達到 90.82 吉瓦,高於 2025 年的 83.51 吉瓦,預計到 2031 年將達到 138.09 吉瓦。

預計從 2026 年到 2031 年,其複合年成長率將達到 8.76%。

本報告按技術(太陽能、風能、水力發電、生質能源、地熱能和海洋能)和最終用戶(公用事業公司、工商業用戶和住宅)進行細分。市場規模和預測以裝置容量(吉瓦)為單位。

義大利可再生能源市場趨勢與洞察

透過NRRP擴大財政支持。

國家再生能源轉型計畫(NRRP)已直接撥款253.6億歐元用於能源轉型項目,透過競爭性競標和優惠津貼的方式提供資金,從而降低了新計畫的加權平均資本成本。 2023年12月發布的《再生能源電力歐盟補充協議》(REPowerEU Addendum)又追加了29億歐元,用於電網數位化和大型可再生能源專案。迄今為止,NRRP已向計畫發起人撥款430億歐元,佔其總資金的22%。隨著授權制度改革逐步解決停滯項目,預計2026年截止日期前,支出將加速成長。歷史投資不足導致電網出現缺口,而這些缺口目前恰好位於義大利陽光最充足的地區,因此南部省份和島嶼地區優先獲得發展機會。因此,當專案開發商在經濟發展受限的地區位置專案時,可以在競標中獲得優惠估值。

歐盟的「適合55歲人士」指令

「Fit-for-55」一攬子計畫要求義大利到2030年將其最終能源消耗中可再生能源的佔比提高到40.5%。這相當於約131吉瓦的發電裝置容量,其中80吉瓦為光伏發電,進一步鞏固了太陽能發電的成長動能。具有法律約束力的里程碑事件將投資期限延長至超出典型企劃案融資的水平,並對未能達成目標的情況處以罰款,從而確保了積極的建設進度。再生能源將加速供暖、製冷和交通運輸領域的脫碳進程,使發電企業能夠從跨多個行業的原產地保證和碳定價機制中獲益。 2024年,再生能源將佔義大利國內需求的41%,目前義大利正在探索利用與奧地利和斯洛維尼亞新建的聯網線路達成跨境電力出口協議。

授權延誤和鄰避效應

環境審核通常需要3到5年,是歐盟建議的24個月期限的兩倍。地方文化遺產管理部門經常要求進行景觀影響評估,民間團體也曾對旅遊路線附近的風力渦輪機提起訴訟。 2025年的一項法令豁免了10兆瓦以下太陽能發電工程的環境影響評估要求,但各地的反應並不一致,不確定性依然存在。儘管最近的一項法院裁決推翻了一項全面的土地使用禁令,表明情況正在逐步改善,但開發商仍有約80吉瓦的項目等待最終核准。

細分市場分析

2025年,太陽能發電將佔義大利總發電量的48.10%,成為義大利可再生能源市場中佔比最大的能源。預計到2031年,該領域將以13.45%的複合年成長率成長,這主要得益於雙面太陽能組件的普及,它們能夠在不增加土地佔用的情況下提高發電量。儘管太陽能發電廠發揮主導作用,但由於直射陽光不足,聚光型太陽熱能發電仍然微乎其微。陸域風電佔總發電量的18.05%,但由於普利亞和西西里島的風位置已接近飽和,開發人員正將重心轉向更高輸出功率的改造計畫。海上漂浮式風電能夠開發深海域,預計2030年將新增2.1吉瓦的裝置容量。水力發電(包括阿爾卑斯山的抽水蓄能電站)佔總發電量的21.25%,在間歇性電源日益增加的情況下,水力發電持續為穩定電網頻率做出貢獻。先進的地熱系統、小規模水力發電和生質能源能完善了義大利的能源結構。義大利水力發電市場規模預計將基本保持穩定,但新增抽水蓄能裝置容量可望提高發電計畫的柔軟性。生質能源營運商正將原料轉向農業廢棄物,以滿足歐盟更嚴格的永續性標準。托斯卡納的地熱發電受惠於利用冷儲存的雙回圈升級改造,而海洋能仍處於示範階段。採用張力腿式和半潛式設計的浮動式風力發電平台正在拓展技術選擇,並幫助義大利擺脫對太陽能的過度依賴,實現能源來源多元化。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 增加自然資源恢復計畫的撥款

- 歐盟的「適合55歲」計劃

- 產消者能源社區

- 海上漂浮式風力發電區

- 儲存託管獎勵

- 太陽能發電的平準化電成本下降

- 市場限制因素

- 授權延誤和鄰避效應

- 電網擁塞和發電限制

- 土地利用競爭(農光互補)

- 對導入模組的依賴

- 供應鏈分析

- 監理展望

- 技術展望

- 波特五力模型

- PESTLE分析

第5章 市場規模與成長預測

- 透過技術

- 太陽能(光伏和聚光太陽能)

- 風力發電(陸上和海上)

- 水力發電(小規模、大型、抽水蓄能)

- 生質能源

- 地熱

- 海洋能源(潮汐能和波浪能)

- 最終用戶

- 公用事業

- 商業和工業用途

- 住宅

第6章 競爭情勢

- 市場集中度

- 策略性措施(併購、合資、資金籌措、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- Enel Green Power SpA

- ERG SpA

- EF Solare Italia SpA

- Vestas Wind Systems AS

- Siemens Gamesa Renewable Energy SA

- Edison SpA

- Gruppo STG Srl

- Peimar Srl

- Falck Renewables(Renantis)SpA

- A2A Rinnovabili SpA

- ACEA Energia SpA

- Sorgenia SpA

- Statkraft Italia Srl

- RWE Renewables Italia

- Engie Italia SpA

- Italgen SpA

- FERA(Fri-El Green Power)SpA

- RTR Rete Rinnovabile

- Terna Plus Srl

- Plenitude(Eni Renewables)

- Enfinity Global Italy

- BayWa re Italia Srl

- Lightsource bp Italy Srl

- GreenGo Srl

第7章 市場機會與未來展望

According to Mordor Intelligence, italy renewable energy market size in 2026 is estimated at 90.82 gigawatt, growing from 2025 value of 83.51 gigawatt with 2031 projections showing 138.09 gigawatt, growing at 8.76% CAGR over 2026-2031.

This report is Segmented by Technology (Solar Energy, Wind Energy, Hydropower, Bioenergy, Geothermal, and Ocean Energy) and End-User (Utilities, Commercial and Industrial, and Residential). The Market Sizes and Forecasts are Provided in Terms of Installed Capacity (GW).

Italy Renewable Energy Market Trends and Insights

NRRP Funding Boost

The NRRP allocates EUR 25.36 billion directly to energy transition projects, disbursing funds through competitive auctions and concessional grants that reduce the weighted-average cost of capital for new projects. The December 2023 REPowerEU addendum adds another EUR 2.9 billion, earmarked for grid digitalization and utility-scale renewables. To date, EUR 43 billion, or 22% of the total NRRP resources, has been allocated to project sponsors, with spending expected to accelerate until the 2026 deadline as permitting reforms clear backlogs. Southern provinces and islands are prioritized because historical under-investment created transmission gaps that now coincide with Italy's highest solar irradiation. Project developers thus gain preferential scoring in auctions when siting assets in regions with constrained economic development.

EU Fit-for-55 Mandate

The Fit-for-55 package requires Italy to achieve a 40.5% renewable share in final energy consumption by 2030, equivalent to approximately 131 GW of capacity, including 80 GW of PV, reinforcing the growth trajectory of solar energy. Binding milestones extend investment horizons beyond typical project finance tenures and penalize non-compliance, ensuring aggressive build-out schedules. Because renewable electricity fuels decarbonization in heating, cooling, and transport, generators can monetize guarantees of origin and carbon prices across multiple sectors. With renewable electricity already accounting for 41% of national demand in 2024, Italy is now exploring cross-border power export contracts that leverage upcoming interconnectors to Austria and Slovenia.

Permitting Delays & NIMBYism

Environmental approvals typically take 3 to 5 years, which is double the EU-recommended 24-month ceiling. Local heritage offices often require visual-impact studies, while citizen groups litigate against turbines near tourism corridors. A 2025 decree waived the environmental impact assessment requirement for PV projects below 10 MW; however, regional compliance varies, prolonging uncertainty. Courts have recently annulled blanket land-use bans, signaling a gradual improvement, but developer pipelines still carry roughly 80 GW of projects awaiting final signatures.

Other drivers and restraints analyzed in the detailed report include:

- Prosumer Energy Communities

- Offshore Floating Wind Zones

- Grid Congestion & Curtailment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solar installations held 48.10% of capacity in 2025, giving them the largest slice of the Italy renewable energy market share. The segment is projected to rise at a 13.45% CAGR through 2031, supported by bifacial modules that lift output without inflating land use. Photovoltaic plants lead, while concentrated solar power remains negligible due to lower direct normal irradiance. Onshore wind provided 18.05% of the capacity, but sites in Apulia and Sicily are almost saturated, so developers are pivoting to higher-output repowering. Offshore floating wind unlocks deep-water zones and is set to add 2.1 GW by 2030. Hydropower at 21.25% of capacity, including pumped-storage hydro in the Alps, continues to stabilize frequency as intermittent assets climb.Enhanced geothermal systems, small hydro, and bioenergy round out the mix. The Italy renewable energy market size for hydropower is expected to stay largely flat, but new pumped-storage capacity will lengthen the dispatch stack. Bioenergy operators are shifting their feedstock toward agricultural waste to meet stricter EU sustainability criteria. Geothermal in Tuscany benefits from binary-cycle upgrades that tap lower-temperature reservoirs, and ocean energy remains in the pilot stage. Floating wind platforms, utilizing tension-leg and semi-submersible designs, expand the technological palette and help Italy diversify away from heavy reliance on solar energy.

Complete Report Scope:

- By Technology

- Solar Energy (PV and CSP)

- Wind Energy (Onshore and Offshore)

- Hydropower (Small, Large, PSH)

- Bioenergy

- Geothermal

- Ocean Energy (Tidal and Wave)

- By End-User

- Utilities

- Commercial and Industrial

- Residential

List of Companies Covered in this Report:

- Enel Green Power SpA

- ERG SpA

- EF Solare Italia SpA

- Vestas Wind Systems AS

- Siemens Gamesa Renewable Energy SA

- Edison SpA

- Gruppo STG Srl

- Peimar Srl

- Falck Renewables (Renantis) SpA

- A2A Rinnovabili SpA

- ACEA Energia SpA

- Sorgenia SpA

- Statkraft Italia Srl

- RWE Renewables Italia

- Engie Italia SpA

- Italgen SpA

- FERA (Fri-El Green Power) SpA

- RTR Rete Rinnovabile

- Terna Plus Srl

- Plenitude (Eni Renewables)

- Enfinity Global Italy

- BayWa r.e. Italia Srl

- Lightsource bp Italy Srl

- GreenGo Srl

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 NRRP funding boost

- 4.2.2 EU Fit-for-55 mandate

- 4.2.3 Prosumer energy communities

- 4.2.4 Offshore floating wind zones

- 4.2.5 Storage co-location incentives

- 4.2.6 Falling PV LCOE

- 4.3 Market Restraints

- 4.3.1 Permitting delays & NIMBYism

- 4.3.2 Grid congestion & curtailment

- 4.3.3 Land-use conflict (agrivoltaic)

- 4.3.4 Imported module dependency

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Competitive Rivalry

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of New Entrants

- 4.7.5 Threat of Substitutes

- 4.8 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Technology

- 5.1.1 Solar Energy (PV and CSP)

- 5.1.2 Wind Energy (Onshore and Offshore)

- 5.1.3 Hydropower (Small, Large, PSH)

- 5.1.4 Bioenergy

- 5.1.5 Geothermal

- 5.1.6 Ocean Energy (Tidal and Wave)

- 5.2 By End-User

- 5.2.1 Utilities

- 5.2.2 Commercial and Industrial

- 5.2.3 Residential

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, JVs, Funding, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Products & Services, Recent Developments)

- 6.4.1 Enel Green Power SpA

- 6.4.2 ERG SpA

- 6.4.3 EF Solare Italia SpA

- 6.4.4 Vestas Wind Systems AS

- 6.4.5 Siemens Gamesa Renewable Energy SA

- 6.4.6 Edison SpA

- 6.4.7 Gruppo STG Srl

- 6.4.8 Peimar Srl

- 6.4.9 Falck Renewables (Renantis) SpA

- 6.4.10 A2A Rinnovabili SpA

- 6.4.11 ACEA Energia SpA

- 6.4.12 Sorgenia SpA

- 6.4.13 Statkraft Italia Srl

- 6.4.14 RWE Renewables Italia

- 6.4.15 Engie Italia SpA

- 6.4.16 Italgen SpA

- 6.4.17 FERA (Fri-El Green Power) SpA

- 6.4.18 RTR Rete Rinnovabile

- 6.4.19 Terna Plus Srl

- 6.4.20 Plenitude (Eni Renewables)

- 6.4.21 Enfinity Global Italy

- 6.4.22 BayWa r.e. Italia Srl

- 6.4.23 Lightsource bp Italy Srl

- 6.4.24 GreenGo Srl

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

西班牙可再生能源:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

西班牙可再生能源:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年) 企業購電協議 (PPA) 平台市場預測至 2034 年—按合約類型、合約期限、能源來源、買方類型、平台模式和地區分類的全球分析海洋溫差發電(OTEC)市場預測—按組件、安裝地點、技術、應用、最終用戶和地區分類的全球分析—2034年農業用電動推進器市場預測至2034年-按系統類型、組件、技術、應用、最終用戶和地區分類的全球分析可再生能源保險:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)

企業購電協議 (PPA) 平台市場預測至 2034 年—按合約類型、合約期限、能源來源、買方類型、平台模式和地區分類的全球分析海洋溫差發電(OTEC)市場預測—按組件、安裝地點、技術、應用、最終用戶和地區分類的全球分析—2034年農業用電動推進器市場預測至2034年-按系統類型、組件、技術、應用、最終用戶和地區分類的全球分析可再生能源保險:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年) 可再生能源市場-全球產業規模、佔有率、趨勢、機會與預測:按類型、最終用途產業、地區和競爭格局分類,2021-2031年混合電池市場-全球產業規模、佔有率、趨勢、機會和預測:按產品類型、額定功率、最終用戶、連接方式、地區和競爭格局分類,2021-2031年東亞可再生能源:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)

可再生能源市場-全球產業規模、佔有率、趨勢、機會與預測:按類型、最終用途產業、地區和競爭格局分類,2021-2031年混合電池市場-全球產業規模、佔有率、趨勢、機會和預測:按產品類型、額定功率、最終用戶、連接方式、地區和競爭格局分類,2021-2031年東亞可再生能源:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年) 可再生能源領域的人工智慧市場:按組件、能源類型、部署模式、最終用戶、國家和地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測西歐可再生能源:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

可再生能源領域的人工智慧市場:按組件、能源類型、部署模式、最終用戶、國家和地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測西歐可再生能源:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)