|

市場調查報告書

商品編碼

2066740

德國電動商用車電池組:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)Germany Electric Commercial Vehicle Battery Pack - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

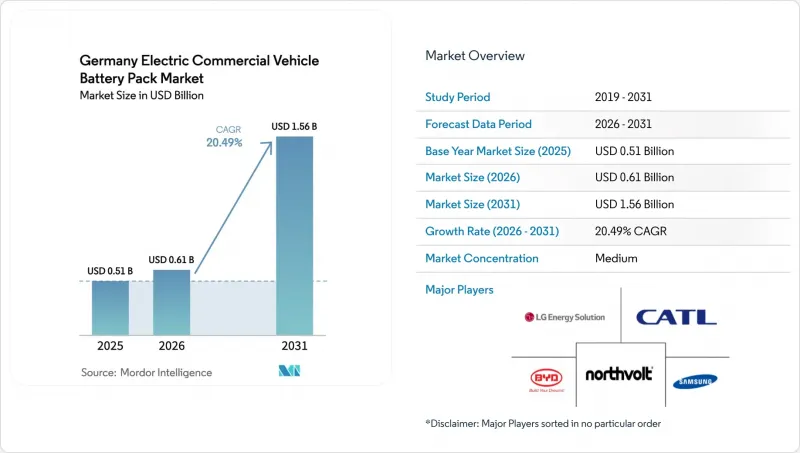

據 Mordor Intelligence 稱,德國電動商用車電池組市場預計將從 2025 年的 5.1 億美元成長到 2026 年的 6.1 億美元,到 2031 年達到 15.6 億美元,預計 2026 年至 2031 年的複合年成長率為 20.49%。

本報告按車輛類型(例如,輕型商用車)、驅動類型(例如,電池式電動車)、電池化學成分(例如,磷酸鋰鐵)、容量(例如,小於15千瓦時)、電池形狀(例如,圓柱形)、電壓、模組結構和組件進行分類。市場預測以貨幣價值(美元)和銷售(單位)兩種形式呈現。

德國電動商用車電池組市場趨勢及洞察。

聯邦政府對電動商用車(E-CV)的補貼計畫正在推動市場成長。

德國的國家獎勵計畫顯著改善了純電動卡車的經濟效益。該計劃透過降低擁有成本和加快採購進度,促進了車輛的早期轉型,使電動商用車對營運商更具吸引力。在地採購條款保護了國內供應商,並在一定程度上抵消了中國的成本優勢。該計劃重點關注40kWh及以上的電池組,從而推動了中型和重型卡車市場的需求,而這些市場目前正面臨基礎設施短缺的問題。儘管相關人員擔心該計劃將於2027年結束,可能導致需求急劇下降,從而造成“銷量斷崖”,但短期內加速訂購正在為德國電動商用車電池組市場注入動力。目前,原始設備製造商(OEM)正在加快生產進度,以最大限度地獲得補貼並確保電池配額。

歐盟重型商用車(HDV)二氧化碳排放目標

布魯塞爾方面要求到2040年將重型車輛的排放減少90%,這使得電池需求從「可選」轉變為「強制」。不符合規定的卡車將因每克超標的二氧化碳排放而被罰款,迫使德國汽車製造商暫停內燃機車輛的新研發項目。 2030年的中期目標正在加速平台重新設計,德國電動商用車電池組市場正轉向高容量電池組,而非混合動力汽車這種臨時解決方案。採購團隊現在簽訂四年期的供應契約,以降低合規風險。雖然這些法規穩定了長期需求,但也增加了短期採購壓力。

卡車充電通道短缺

由於電池組價格大幅下降,電動車在都市區配送領域日益普及,使其與柴油車更具競爭力。然而,基礎建設卻落後,尤其是大型車輛的基礎設施。快速充電站的數量未能達到預期目標,降低了長途運輸的效率。如果電動車的普及速度不能加快,未來可能會出現瓶頸。作為一項臨時措施,汽車製造商正在部署移動充電拖車;而作為一項戰略舉措,為了降低地緣政治風險,供應鏈正在將重心轉移到歐洲的電池組裝。

細分市場分析

至2025年,輕型商用車(LCV)將佔德國電動商用車電池組市場48.18%的佔有率。這主要得益於日均行駛里程100-200公里的宅配及郵政車輛車隊。電子商務貨運量的激增也使得60-80千瓦時容量的電池組需求保持強勁。相較之下,中型和重型卡車的複合年成長率最高,達到22.38%,政策補貼仍然抵消了成本和負載容量的擔憂。聯邦政府對重型卡車的津貼正在提振訂單並加速平台推出。都市區噪音法規和低排放氣體區的設立正在推動輕型商用車(LCV)的電氣化,而歐盟的二氧化碳排放罰款則促使汽車製造商(OEM)向長途運輸的純電動驅動系統轉型。

車隊營運商正透過大量採購電芯來整合訂單,以確保優先生產名額並協商更優惠的價格。創新的重點在於模組化電池組設計,使車隊營運商能夠透過更換電池盒來最佳化續航里程。雖然輕型商用車 (LCV) 的夜間充電已成為標準配置,但對於長途卡車而言,公共高功率充電站至關重要。因此,德國電動商用車電池組市場的發展速度呈現雙軌制:輕型商用車的數量推動了初期收入的成長,而卡車平台預計將在未來實現規模化發展。

預計到2025年,電池式電動車(BEV)將佔汽車交付量的81.62%。隨著汽車製造商逐步淘汰插電式混合動力汽車(PHEV),純電動車的複合年成長率預計將達到21.21%。儘管初始成本較高,但由於法規要求廢氣零排放氣體以及動力系統維護簡便,車隊正在轉向純電動車。目前,插電式混合動力汽車僅被一些電力基礎設施不足的區域公車業者使用。監管補貼政策也正在推動純電動車的發展,進一步鞏固了其在德國電動商用車電池組市場動力解決方案領域的領先地位。

充電生態系統也不斷調整。車庫中的智慧充電軟體能夠分散充電負荷,避免尖峰時段的集中充電;兆瓦級充電樁正在萊茵-礦區走廊進行試點。零件供應商正在最佳化溫度控管系統,以實現更快的直流快充週期,從而滿足緊迫的交貨期限。隨著殘值趨於穩定,租賃公司越來越願意為純電動車隊提供融資,擴大了中小企業的購車管道。相關人員預計插電式混合動力車的市場佔有率將會下降,而電池式電動車平台將進一步鞏固其地位。

由於成本低、安全性高且供應鏈穩定,磷酸鐵鋰電池組預計到2025年將佔據45.09%的市場佔有率。由於不含鎳或鈷,磷酸鐵鋰電池組受金屬價格波動的影響較小,這使其在德國電動商用車電池組市場中具有戰略優勢。同時,液態金屬磷酸鐵鋰電池(LMFP)也呈現強勁成長勢頭,年複合成長率達22.52%,預計在不影響熱穩定性的前提下,能量密度將提高10-15%。原始設備製造商(OEM)正在高階區域卡車中採用LMFP電池組,因為其減輕的電池組重量可以提高有效負載容量。

對於需要緊湊型結構的長途面積,基於NMC的化學成分仍然至關重要,但高鎳產品更容易受到價格波動的影響。為了因應不斷變化的需求,供應商正擴大將LFP和LMFP生產線整合到同一地點。固態固態電池原型目前處於檢驗階段,但要到2029年才會投入量產。化學成分的發展趨勢正從成本驅動型轉向基於性能的分級產品組合,使車隊能夠根據自身的運作週期調整電池組的特性。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 電動汽車銷售

- 汽車製造商的電動車銷量

- 熱門電動車款

- 偏好特定電池化學系統的原始設備製造商

- 電池組價格

- 電池材料成本

- 電池化學物質價格比較

- 電動車電池容量和效率

- 即將推出的電動車車型

- 電池和封裝的生產能力和運轉率

- 法律規範

- 型式認可和包裝安全標準

- 市場進入:獎勵、在地採購和貿易

- 二手產品:生產者責任延伸、二次利用及回收義務

- 價值鍊和通路分析

- 技術展望

- 波特五力模型

- 市場促進因素

- 聯邦政府對電動車的補貼計畫推動了市場成長

- 歐盟重型車輛(HDV)二氧化碳排放目標

- 磷酸鐵鋰電池組的成本低於100美元/kWh

- 夜間城市物流噪音管制條例

- 過渡到 800V 總線平台

- 電池即服務公車合約

- 市場限制因素

- 一條走廊,兩側零星分佈著一些卡車充電站。

- 人們普遍認為柴油車的初始成本較高,而且與柴油車相比成本較高。

- 石墨廠授權延誤

- LMFP許可證費用的波動性

第5章 市場規模及成長預測(價值:美元,數量:單位)

- 車輛類型

- 輕型商用車

- 中型和大型卡車

- 公車

- 依推進類型

- 電池式電動車

- 插電式混合動力電動車

- 電池化學成分

- 磷酸鋰鐵(LFP)

- LMFP(磷酸錳鋰鐵)

- NMC(鎳錳鈷氧化物)

- NCA(鎳鈷鋁氧化物)

- LTO(鈦酸鋰)

- 其他(LCO、LMO、NMX、新興電池技術等)

- 按產能

- 小於 15 千瓦時

- 15~40 kWh

- 40~60 kWh

- 60~80 kWh

- 80~100 kWh

- 100~150 kWh

- 150度或以上

- 依電池類型

- 圓柱形

- 袋式

- 棱鏡型

- 電壓等級

- 低於 400 伏特(48-350 伏特)

- 400~600 V

- 600~800 V

- 800伏特或以上

- 模組化結構

- 電池到模組(CTM)

- 細胞到包裝(CTP)

- 模組到包裝 (MTP)

- 按組件

- 陽極

- 陰極

- 電解

- 分離器

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Akasol AG(Borgwarner Inc.)

- Automotive Cells Company(ACC)

- BYD Company Ltd.

- Contemporary Amperex Technology Co. Ltd.(CATL)

- Samsung SDI Co. Ltd.

- LG Energy Solution Ltd.

- Northvolt AB

- Panasonic Holdings Corp.

- Microvast Holdings, Inc.

- BMZ Germany GmbH

- Webasto SE

- Forsee Power

- Liacon GmbH

- Super B

- SK On Co., Ltd.

- Ebusco Holding NV

- Saft Groupe SA

第7章 市場機會與未來展望

第8章:電動車電池組公司執行長面臨的關鍵策略挑戰

第9章:誰向誰供貨? (OEM廠商層級圖)

第10章:本地化和成本結構

- 貨幣銀行細分(美元/度)

- 在地採購內容和進口內容

- 轉嫁關稅和補貼

第11章 生產能力與運轉率追蹤器

- 電池容量(GWh)(已安裝/正在建造)

- 運轉率和瓶頸

- 新電廠計劃

第12章:貿易流量與進口依賴度

第13章:回收與第二生命生態系統

According to Mordor Intelligence, the german electric commercial vehicle battery pack market size is expected to increase from USD 0.51 billion in 2025 to USD 0.61 billion in 2026 and reach USD 1.56 billion by 2031, growing at a CAGR of 20.49% over 2026-2031.

This report is Segmented by Vehicle Type (Light Commercial Vehicle, and More), Propulsion Type (Battery Electric Vehicle, and More), Battery Chemistry (Lithium Iron Phosphate, and More), Capacity (Below 15 KWh, and More), Battery Form (Cylindrical, and More), Voltage, Module Architecture, Component. The Market Forecasts are Provided in Terms of Value (USD) and Volume in Units.

Germany Electric Commercial Vehicle Battery Pack Market Trends and Insights

Federal E-CV Subsidy Program Driving the Market Growth

Germany's national incentive program is significantly improving the economics of battery-electric trucks. By reducing ownership costs and accelerating procurement timelines, the scheme enables faster fleet transitions and makes electric commercial vehicles more attractive to operators . Local-content clauses shield domestic suppliers and partially neutralize Chinese cost advantages. The program focuses on packs above 40 kWh, catalyzing demand in medium and heavy-duty classes facing infrastructure gaps. Stakeholders voice concern that the 2027 sunset could create a volume cliff, yet near-term pull-forward orders lend momentum to the German electric commercial vehicle battery pack market. OEMs are now front-loading production schedules to maximize grant capture and lock in cell allocations.

EU HDV CO2 Targets

Brussels' requirement for a 90% cut in heavy-duty vehicle emissions by 2040 converts battery demand from optional to obligatory. Non-compliant trucks will attract penalties per gram of excess CO2, forcing German OEMs to cease new internal-combustion programs. Interim 2030 targets accelerate platform redesign, pushing the German electric commercial vehicle battery pack market toward higher-capacity packs over hybrid stopgaps. Procurement teams now secure four-year supply contracts to de-risk compliance. The regulation stabilizes long-run demand but intensifies short-term sourcing pressure.

Sparse Truck-Charging Corridors

Major logistics firms are increasingly turning to electric urban delivery fleets due to a significant drop in battery pack prices, making them competitive with diesel. Yet, the infrastructure hasn't kept pace, particularly for heavy-duty vehicles. The number of fast-charging points falls short of targets, curtailing long-haul efficiency and potentially leading to future bottlenecks if the rollout doesn't speed up. As a stopgap, OEMs are deploying mobile charging trailers, and in a strategic move to mitigate geopolitical risks, supply chains are pivoting towards European cell assembly.

Other drivers and restraints analyzed in the detailed report include:

- LFP Pack Cost Drops Below USD 100/kWh

- Battery-as-a-Service Bus Contracts

- Graphite-Plant Permitting Delays

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Light commercial vehicles (LCVs) held 48.18% of Germany's electric commercial vehicle battery pack market share in 2025, underpinned by courier and postal fleets operating 100-200 km daily routes. Shipment surges in e-commerce sustain baseline pack demand in the 60-80 kWh bracket. In contrast, medium and heavy trucks show the swiftest 22.38% CAGR as policy subsidies override lingering cost and payload concerns. Federal grants for heavy trucks have expedited orders and hastened platform launches. Urban noise regulations and low-emission zones are bolstering the electrification of light commercial vehicles (LCVs), while EU CO2 penalties are steering original equipment manufacturers (OEMs) towards battery-electric drivetrains for long hauls.

Fleet operators are consolidating orders to gain priority production slots and negotiate better pricing on bulk cells. The focus of innovation is on modular pack designs that enable fleets to interchange cartridges for optimized range. While overnight depot charging is standard for LCVs, public high-power stations are essential for trucks on long routes. As a result, the German market for electric commercial vehicle battery packs is charting a dual-speed path: LCV volumes are driving early revenues, while truck platforms are poised to achieve scale in the future.

Battery-electric vehicles captured 81.62% of 2025 deliveries and will log a 21.21% CAGR as OEMs phase out plug-in hybrids. Zero-tailpipe-emission rules and simpler driveline maintenance tilt fleets toward BEVs despite higher initial prices. PHEVs are only found in regional bus operators that lack depot power upgrades. Regulatory credit systems also incentivize pure BEVs, deepening their advantage in the German electric commercial vehicle battery pack market for propulsion solutions.

Charging ecosystems are adapting: depot smart-charging software staggers load to avoid peak tariffs, while megawatt chargers are piloting along the Rhine-Main corridor. Component suppliers now tune thermal systems to enable quicker DC fast-charge cycles to meet tight delivery windows. With residual values stabilizing, leasing companies are increasingly open to underwriting BEV fleets, thereby broadening access for SMEs. Stakeholders anticipate that PHEV market share will decline, further solidifying the momentum behind battery-electric platforms.

LFP packs commanded a 45.09% share in 2025 due to their lower costs, safety, and stable supply chains. The absence of nickel and cobalt shields prices from metal volatility, giving LFP a strategic edge in the German electric commercial vehicle battery pack market. LMFP, however, posts a brisk 22.52% CAGR, promising an energy density 10-15% higher without compromising thermal stability. OEMs earmark LMFP for premium regional trucks, where pack-weight savings enable extra payload.

NMC chemistries remain essential for long-range buses that require compact footprints, yet high-nickel blends are subject to price swings. Suppliers are increasingly co-locating LFP and LMFP lines to hedge against demand shifts. Solid-state prototypes are entering validation but will not influence volume before 2029. Chemistries are evolving from cost-driven dominance toward performance-tiered portfolios that let fleets match pack characteristics to duty cycles.

List of Companies Covered in this Report:

- Akasol AG (Borgwarner Inc.)

- Automotive Cells Company (ACC)

- BYD Company Ltd.

- Contemporary Amperex Technology Co. Ltd. (CATL)

- Samsung SDI Co. Ltd.

- LG Energy Solution Ltd.

- Northvolt AB

- Panasonic Holdings Corp.

- Microvast Holdings, Inc.

- BMZ Germany GmbH

- Webasto SE

- Forsee Power

- Liacon GmbH

- Super B

- SK On Co., Ltd.

- Ebusco Holding N.V.

- Saft Groupe S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Electric Vehicle Sales

- 4.2 Electric Vehicle Sales By OEMs

- 4.3 Best-selling EV Models

- 4.4 OEMs With Preferable Battery Chemistry

- 4.5 Battery Pack Price

- 4.6 Battery Material Cost

- 4.7 Battery Chemistry Price Comparison

- 4.8 EV Battery Capacity and Efficiency

- 4.9 Upcoming EV Models

- 4.10 Cell and Pack Capacity vs Utilization

- 4.11 Regulatory Framework

- 4.12 Type Approval and Pack Safety Standards

- 4.13 Market Access: Incentives, Local Content and Trade

- 4.14 End-of-Life: EPR, Second-Life and Recycling Mandates

- 4.15 Value Chain and Distribution Channel Analysis

- 4.16 Technological Outlook

- 4.17 Porter's Five Forces

- 4.17.1 Threat of New Entrants

- 4.17.2 Bargaining Power of Suppliers

- 4.17.3 Bargaining Power of Buyers

- 4.17.4 Threat of Substitutes

- 4.17.5 Competitive Rivalry

- 4.18 Market Drivers

- 4.18.1 Federal E-CV Subsidy Program Driving Market Growth

- 4.18.2 EU HDV CO2 Targets

- 4.18.3 LFP Pack Cost Drops Below USD 100/kWh

- 4.18.4 Night-Time City-Logistics Noise Caps

- 4.18.5 Shift To 800 V Coach Platforms

- 4.18.6 Battery-As-A-Service Bus Contracts

- 4.19 Market Restraints

- 4.19.1 Sparse Truck-Charging Corridors

- 4.19.2 Up-Front Cost Premium Vs Diesel

- 4.19.3 Graphite-Plant Permitting Delays

- 4.19.4 LMFP License-Fee Volatility

5 Market Size and Growth Forecasts (Value in USD and Volume in Units)

- 5.1 By Vehicle Type

- 5.1.1 Light Commercial Vehicle

- 5.1.2 Medium and Heavy Duty Truck

- 5.1.3 Bus

- 5.2 By Propulsion Type

- 5.2.1 Baterry Electric Vehicle

- 5.2.2 Plug-in Hybrid Electric Vehicle

- 5.3 By Battery Chemistry

- 5.3.1 LFP (Lithium Iron Phosphate)

- 5.3.2 LMFP (Lithium Manganese Iron Phosphate)

- 5.3.3 NMC (Nickel Manganese Cobalt Oxide)

- 5.3.4 NCA (Nickel Cobalt Aluminum Oxide)

- 5.3.5 LTO (Lithium Titanium Oxide)

- 5.3.6 Others (LCO, LMO, NMX, Emerging Battery Technologies, etc.)

- 5.4 By Capacity

- 5.4.1 Below 15 kWh

- 5.4.2 15-40 kWh

- 5.4.3 40-60 kWh

- 5.4.4 60-80 kWh

- 5.4.5 80-100 kWh

- 5.4.6 100-150 kWh

- 5.4.7 Above 150 kWh

- 5.5 By Battery Form

- 5.5.1 Cylindrical

- 5.5.2 Pouch

- 5.5.3 Prismatic

- 5.6 By Voltage Class

- 5.6.1 Below 400 V (48-350 V)

- 5.6.2 400-600 V

- 5.6.3 600-800 V

- 5.6.4 Above 800 V

- 5.7 By Module Architecture

- 5.7.1 Cell-to-Module (CTM)

- 5.7.2 Cell-to-Pack (CTP)

- 5.7.3 Module-to-Pack (MTP)

- 5.8 By Component

- 5.8.1 Anode

- 5.8.2 Cathode

- 5.8.3 Electrolyte

- 5.8.4 Separator

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Akasol AG (Borgwarner Inc.)

- 6.4.2 Automotive Cells Company (ACC)

- 6.4.3 BYD Company Ltd.

- 6.4.4 Contemporary Amperex Technology Co. Ltd. (CATL)

- 6.4.5 Samsung SDI Co. Ltd.

- 6.4.6 LG Energy Solution Ltd.

- 6.4.7 Northvolt AB

- 6.4.8 Panasonic Holdings Corp.

- 6.4.9 Microvast Holdings, Inc.

- 6.4.10 BMZ Germany GmbH

- 6.4.11 Webasto SE

- 6.4.12 Forsee Power

- 6.4.13 Liacon GmbH

- 6.4.14 Super B

- 6.4.15 SK On Co., Ltd.

- 6.4.16 Ebusco Holding N.V.

- 6.4.17 Saft Groupe S.A.

7 Market Opportunities and Future Outlook

8 Key Strategic Questions for EV Battery Pack CEOs

9 Who Supplies Whom (OEM-Tier Map)

10 Localization and Cost Stack

- 10.1 BoM Split (USD/kWh)

- 10.2 Local vs Imported Content

- 10.3 Tariff/Subsidy Pass-Through

11 Capacity and Utilization Tracker

- 11.1 Cell GWh (Installed/Under-Build)

- 11.2 Utilization and Bottlenecks

- 11.3 New Plant Pipeline

12 Trade Flow and Import Dependence

13 Recycling and Second-Life Ecosystem

高密度電動車電池組設計市場-策略洞察與預測(2026-2031年)

高密度電動車電池組設計市場-策略洞察與預測(2026-2031年) 電動汽車電池組市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

電動汽車電池組市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 中國電動車電池組:市場佔有率分析、產業趨勢與統計、成長預測(2025-2029 年)亞太地區電動汽車電池組:市場佔有率分析、產業趨勢與統計、成長預測(2025-2029 年)北美電動車電池組:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)印度電動車電池組:市場佔有率分析、行業趨勢和統計、成長預測(2025-2029 年)德國電動車電池組:市場佔有率分析、產業趨勢與統計、成長預測(2025-2029 年)日本電動車電池組:市場佔有率分析、產業趨勢與統計、成長預測(2025-2029 年)東協電動車電池組:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)歐洲電動車電池組:市場佔有率分析、產業趨勢與統計、成長預測(2025-2029 年)

中國電動車電池組:市場佔有率分析、產業趨勢與統計、成長預測(2025-2029 年)亞太地區電動汽車電池組:市場佔有率分析、產業趨勢與統計、成長預測(2025-2029 年)北美電動車電池組:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)印度電動車電池組:市場佔有率分析、行業趨勢和統計、成長預測(2025-2029 年)德國電動車電池組:市場佔有率分析、產業趨勢與統計、成長預測(2025-2029 年)日本電動車電池組:市場佔有率分析、產業趨勢與統計、成長預測(2025-2029 年)東協電動車電池組:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)歐洲電動車電池組:市場佔有率分析、產業趨勢與統計、成長預測(2025-2029 年)