|

市場調查報告書

商品編碼

2066733

美國工業感測器:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)United States Industrial Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

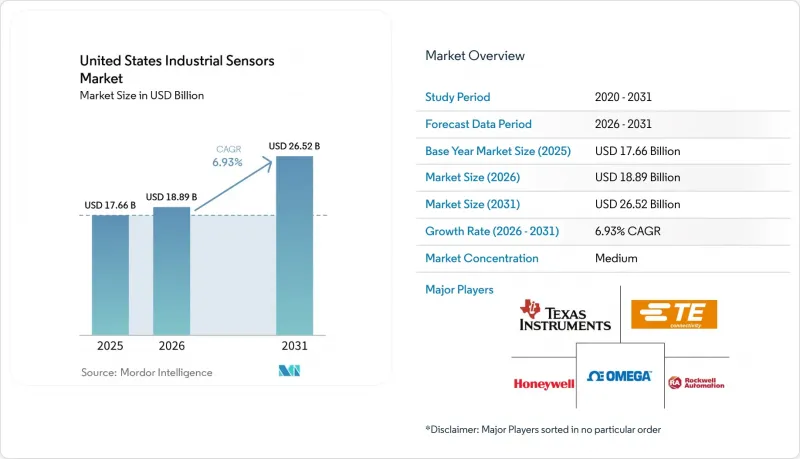

據 Mordor Intelligence 稱,2025 年美國工業感測器市場價值 176.6 億美元,預計將從 2026 年的 188.9 億美元成長到 2031 年的 265.2 億美元,2026 年至 2031 年的複合年成長率為 6.93%。

本報告按連接方式(有線和無線解決方案)、感測器類型(壓力感測器、流量感測器、溫度感測器、液位感測器等)以及終端用戶產業(石油天然氣、化學和石化、水和用水和污水處理、食品飲料、發電、汽車等)進行細分。市場預測以美元計價。

美國工業感測器市場趨勢與洞察

離散製造業和流程產業的工業物聯網應用迅速成長

製造商正在生產流程的各個階段整合感測器,以實現即時分析,從而最大限度地減少意外停機時間和缺陷率。私人 5G 網路的部署已證明振動、溫度和視覺感測器的延遲低於 10 毫秒,證實了無線技術在汽車組裝和數控加工線上的應用潛力。一家食品加工企業透過使用 LoRaWAN 閘道回程傳輸來自衛生溫度和流量感測器的數據,減少了 60% 的佈線。邊緣閘道器現在與 OPC UA 協同工作,執行時間敏感型網路處理,從而實現以前僅限於有線系統的封閉回路型控制。因此,美國工業感測器市場在現有(棕地)和新建(待開發區)工廠中都出現了感測器網路密度和安裝率的顯著提升。

增加對清潔能源基礎設施的資本投資

美國能源局的「快速併網」舉措已將併網時間縮短了一半,從而推動了風力發電機變槳控制系統中差壓感測器和併網逆變器中電流感測器的需求。到2025年,聯邦政府將投入4,400萬美元用於先進計量系統和變電站自動化,這兩項技術都依賴溫度感測器和局部放電感測器。離岸風力發電開發商正在指定符合NFPA 70第500節規定的本質安全型壓力和流量測量儀器,這些儀器適用於I類1區環境。電池儲能計畫預計到2025年將新增15吉瓦的容量,這些計畫要求配備熱失控檢測裝置,以滿足UL 9540A標準。因此,清潔能源的成長正在推動美國工業感測器市場向氣體、電流和振動感測技術轉型,這些技術有助於提高資產運轉率和合規性。

特殊MEMS晶片的供應波動仍在持續。

2024年下半年,汽車用壓阻式壓力感知器和電容式加速計的前置作業時間超過26週,導致維修工程延誤。英飛凌的「XENSIV」系列和博世Sensortec的「BMI」系列面臨最嚴格的配額限制。儘管受《晶片法案》(CHIPS Act)資助的美國本土晶圓代工廠正在擴大產能,但預計至少要到2028年才能趕上亞洲的產能,供應風險依然很高。透過改用SOI和壓電元件等替代方案或重新設計來尋求雙重採購,正在增加非重複性工程成本,並減緩美國工業感測器市場的短期成長。

細分市場分析

到2025年,有線解決方案將佔據美國工業感測器市場73.82%的佔有率,這主要得益於數十年來對4-20 mA和HART迴路的投資。這些迴路對於NFPA 85和API 670標準規定的5毫秒以下停機操作仍然至關重要。然而,受5G私有網路、LoRaWAN和乙太網路APL等技術的普及應用所推動,無線節點預計到2031年將以8.45%的複合年成長率成長。新建設的半導體工廠正在透過無線回程傳輸部署數千個IO-Link溫度感測器,以保持無塵室的柔軟性,而乙太網路APL則有助於滿足碳氫化合物區域的本質安全標準。美國工業感測器市場正朝著混合架構發展,其中有線迴路負責安全功能,而無線層則提供診斷功能。

在一家汽車工廠進行的專用蜂窩網路試點部署表明,減少電纜安裝成本可降低 40%,這為離散製造業採用無線技術提供了強力的論點。同時,在現有的化工廠中,由於頻段許可和閘道器硬體的成本削弱了無線技術的提案,有線維修往往得以保留。像艾默生和Honeywell這樣的供應商現在提供整合資產管理套件,可以聚合有線和無線資料流,這表明混合連接將如何支援美國工業感測器市場的下一階段成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 離散產業和流程產業對工業物聯網 (IIoT) 的採用率迅速提高

- 增加對清潔能源基礎設施的資本投資

- 美國半導體製造廠的擴張正在推動先進製造業對感測器的需求。

- 2025年起加速推進預測性維護計劃

- 聯邦政府獎勵措施,吸引關鍵產業回流我國

- 隨著氫能經濟的發展,對新型壓力感測器和氣體感測器的需求日益成長。

- 市場限制因素

- 專用MEMS晶片的供應波動仍在持續。

- 網路安全風險阻礙無線感測器的普及

- 在爆炸環境中,本質安全型感測器的總擁有成本較高

- 工業通訊協定標準的碎片化

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 透過連接方式

- 有線解決方案

- 無線解決方案

- 依感測器類型

- 壓力感測器

- 流量感測器

- 溫度感測器

- 液位感測器

- 氣體感測器

- 接近感測器和光電感測器

- 振動感測器

- 其他感測器

- 按最終用戶行業分類

- 石油和天然氣

- 化工/石油化工

- 水和污水處理

- 食品/飲料

- 發電

- 車

- 製藥和生命科學

- 航太/國防

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- ABB Ltd

- Analog Devices, Inc.

- Banner Engineering Corp.

- Bosch Sensortec GmbH

- Endress+Hauser AG

- Emerson Electric Co.

- Honeywell International Inc.

- IFM Efector, Inc.

- Infineon Technologies AG

- Keyence Corporation of America

- Omega Engineering Inc.

- Omron Corporation

- Pepperl+Fuchs, Inc.

- Rockwell Automation, Inc.

- Sensata Technologies, Inc.

- Sick AG

- TE Connectivity Ltd.

- Texas Instruments Incorporated

- The Krohne Group

- Vega Grieshaber KG

- Yokogawa Electric Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the united states industrial sensors market size was valued at USD 17.66 billion in 2025 and is estimated to grow from USD 18.89 billion in 2026 to USD 26.52 billion by 2031, growing at a CAGR of 6.93% from 2026 to 2031.

This report is Segmented by Connectivity (Wired Solutions, and Wireless Solutions), Sensor Type (Pressure Sensors, Flow Sensors, Temperature Sensors, Level Sensors, and More), and End-User Industry (Oil and Gas, Chemicals and Petrochemicals, Water and Wastewater, Food and Beverage, Power Generation, Automotive, and More). The Market Forecasts are Provided in Terms of Value (USD).

United States Industrial Sensors Market Trends and Insights

Surge in IIoT Adoption Across Discrete and Process Industries

Manufacturers are embedding sensors at every production node to enable real-time analytics that minimize unplanned downtime and scrap rates. Private 5G deployments demonstrate sub-10 millisecond latency for vibration, temperature, and vision sensors, validating wireless performance on automotive assembly and CNC machining lines. Food processors have reduced cabling work by 60% using LoRaWAN gateways to backhaul data from hygienic temperature and flow sensors. Edge gateways now run time-sensitive networking in concert with OPC UA, allowing closed-loop control that was previously limited to wired systems. As a result, the United States industrial sensors market is witnessing denser sensor grids and higher attach rates in both brownfield and greenfield facilities.

Rising Capital Expenditure on Clean-Energy Infrastructure

The Department of Energy's Speed to Power initiative halves interconnection timelines, spurring demand for differential pressure sensors in wind-turbine pitch systems and current sensors inside grid-tied inverters. A USD 44 million federal outlay in 2025 targeted advanced metering and substation automation, both of which rely on temperature and partial-discharge sensors. Offshore wind developers specify intrinsically safe pressure and flow devices rated for Class I Division 1 environments under NFPA 70 Article 500.Battery storage projects, which added 15 GW in 2025, mandate thermal-runaway detection to meet UL 9540A standards. Clean-energy growth, therefore, tilts the United States industrial sensors market toward gas, current, and vibration sensing technologies that support asset availability and regulatory compliance.

Persistent Chip-Supply Volatility for Specialty MEMS Dies

Lead times for automotive-grade piezoresistive pressure dies and capacitive accelerometers extended beyond 26 weeks in late 2024, delaying retrofit programs. Infineon's XENSIV and Bosch Sensortec's BMI families faced the steepest allocation constraints. Domestic foundries funded by the CHIPS Act are ramping up production but are not expected to match Asian manufacturing capacity until at least 2028, keeping supply risks elevated. Dual sourcing and redesigns around SOI and piezoelectric alternatives increase non-recurring engineering costs, tempering near-term growth of the United States industrial sensors market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of the United States Semiconductor Fabs Driving Sensor Demand

- Acceleration of Predictive-Maintenance Programs Post-2025

- Cybersecurity Risks Inhibiting Wireless Sensor Roll-Outs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Wired solutions captured 73.82% of the United States industrial sensors market share in 2025 due to decades-long investment in 4-20 mA and HART loops. They remain indispensable for sub-5 millisecond shutdown tasks mandated by NFPA 85 and API 670. However, wireless nodes are forecast to grow at an 8.45% CAGR through 2031 on the back of private 5G, LoRaWAN, and Ethernet-APL adoption. Greenfield semiconductor fabs deploy thousands of IO-Link temperature sensors over wireless backhaul to preserve cleanroom flexibility, while Ethernet-APL supports intrinsic-safety compliance in hydrocarbon zones. The USAindustrial sensors market is converging toward hybrid architectures in which wired loops handle safety functions and wireless layers add diagnostics.

Private cellular pilots at automotive plants show that reducing cable pulls can lower installation budgets by 40%, creating a compelling case for wireless deployment in discrete manufacturing. Conversely, brownfield chemical sites often retain wired retrofits because spectrum licenses and gateway hardware dilute the wireless value proposition. Vendors such as Emerson and Honeywell now offer unified asset-management suites that aggregate both wired and wireless data streams, demonstrating how hybrid connectivity will underpin the next growth phase of the US industrial sensors market.

List of Companies Covered in this Report:

- ABB Ltd

- Analog Devices, Inc.

- Banner Engineering Corp.

- Bosch Sensortec GmbH

- Endress+Hauser AG

- Emerson Electric Co.

- Honeywell International Inc.

- IFM Efector, Inc.

- Infineon Technologies AG

- Keyence Corporation of America

- Omega Engineering Inc.

- Omron Corporation

- Pepperl+Fuchs, Inc.

- Rockwell Automation, Inc.

- Sensata Technologies, Inc.

- Sick AG

- TE Connectivity Ltd.

- Texas Instruments Incorporated

- The Krohne Group

- Vega Grieshaber KG

- Yokogawa Electric Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in IIoT Adoption Across Discrete and Process Industries

- 4.2.2 Rising Capital Expenditure on Clean-Energy Infrastructure

- 4.2.3 Expansion of the United States Semiconductor Fabs Driving Sensor Demand in Advanced Manufacturing

- 4.2.4 Acceleration of Predictive-Maintenance Programs Post-2025

- 4.2.5 Federal Incentives for Reshoring Critical Industries

- 4.2.6 Growth of Hydrogen Economy Requiring Novel Pressure and Gas Sensors

- 4.3 Market Restraints

- 4.3.1 Persistent Chip-Supply Volatility for Specialty MEMS Dies

- 4.3.2 Cyber-Security Risks Inhibiting Wireless Sensor Roll-Outs

- 4.3.3 High Total Cost of Ownership for Intrinsically Safe Sensors in Explosive Zones

- 4.3.4 Standards Fragmentation Across Industrial Communications Protocols

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Connectivity

- 5.1.1 Wired Solutions

- 5.1.2 Wireless Solutions

- 5.2 By Sensor Type

- 5.2.1 Pressure Sensors

- 5.2.2 Flow Sensors

- 5.2.3 Temperature Sensors

- 5.2.4 Level Sensors

- 5.2.5 Gas Sensors

- 5.2.6 Proximity and Photoelectric Sensors

- 5.2.7 Vibration Sensors

- 5.2.8 Other Types of Sensors

- 5.3 By End-User Industry

- 5.3.1 Oil and Gas

- 5.3.2 Chemicals and Petrochemicals

- 5.3.3 Water and Wastewater

- 5.3.4 Food and Beverage

- 5.3.5 Power Generation

- 5.3.6 Automotive

- 5.3.7 Pharmaceutical and Life Sciences

- 5.3.8 Aerospace and Defense

- 5.3.9 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ABB Ltd

- 6.4.2 Analog Devices, Inc.

- 6.4.3 Banner Engineering Corp.

- 6.4.4 Bosch Sensortec GmbH

- 6.4.5 Endress+Hauser AG

- 6.4.6 Emerson Electric Co.

- 6.4.7 Honeywell International Inc.

- 6.4.8 IFM Efector, Inc.

- 6.4.9 Infineon Technologies AG

- 6.4.10 Keyence Corporation of America

- 6.4.11 Omega Engineering Inc.

- 6.4.12 Omron Corporation

- 6.4.13 Pepperl+Fuchs, Inc.

- 6.4.14 Rockwell Automation, Inc.

- 6.4.15 Sensata Technologies, Inc.

- 6.4.16 Sick AG

- 6.4.17 TE Connectivity Ltd.

- 6.4.18 Texas Instruments Incorporated

- 6.4.19 The Krohne Group

- 6.4.20 Vega Grieshaber KG

- 6.4.21 Yokogawa Electric Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

工業感測器和自動化市場預測至2034年—按感測器類型、技術、產業、應用、最終用戶和地區分類的全球分析

工業感測器和自動化市場預測至2034年—按感測器類型、技術、產業、應用、最終用戶和地區分類的全球分析 工業感測器市場-全球市場規模、佔有率、趨勢、機會和預測:按產品、應用、地區和競爭對手分類,2021-2031年

工業感測器市場-全球市場規模、佔有率、趨勢、機會和預測:按產品、應用、地區和競爭對手分類,2021-2031年 工業感測器市場規模、佔有率和趨勢分析報告:按感測器類型、技術、最終用途、地區和細分市場預測(2025-2033 年)

工業感測器市場規模、佔有率和趨勢分析報告:按感測器類型、技術、最終用途、地區和細分市場預測(2025-2033 年) 工業感測器市場:2026-2032年全球市場預測(按感測器類型、技術、通訊協定、應用和銷售管道)

工業感測器市場:2026-2032年全球市場預測(按感測器類型、技術、通訊協定、應用和銷售管道) 工業感測器市場:按檢測方法、終端用戶產業和地區分類

工業感測器市場:按檢測方法、終端用戶產業和地區分類 工業感測器市場機會、成長要素、產業趨勢分析及2026年至2035年預測

工業感測器市場機會、成長要素、產業趨勢分析及2026年至2035年預測 半導體氣體感測器市場分析及預測至 2035 年:按類型、產品、技術、應用、材料類型、最終用戶、功能和安裝類型分類。工業感測器市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、最終用戶、功能、安裝類型、設備及解決方案分類

半導體氣體感測器市場分析及預測至 2035 年:按類型、產品、技術、應用、材料類型、最終用戶、功能和安裝類型分類。工業感測器市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、最終用戶、功能、安裝類型、設備及解決方案分類 中國工業感測器市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

中國工業感測器市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 日本工業自動化感測器市場規模、佔有率、趨勢及預測(按感測器類型、類型、自動化模式、最終用戶和地區分類,2026-2034年)

日本工業自動化感測器市場規模、佔有率、趨勢及預測(按感測器類型、類型、自動化模式、最終用戶和地區分類,2026-2034年)