|

市場調查報告書

商品編碼

1934802

中國工業感測器市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)China Industrial Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

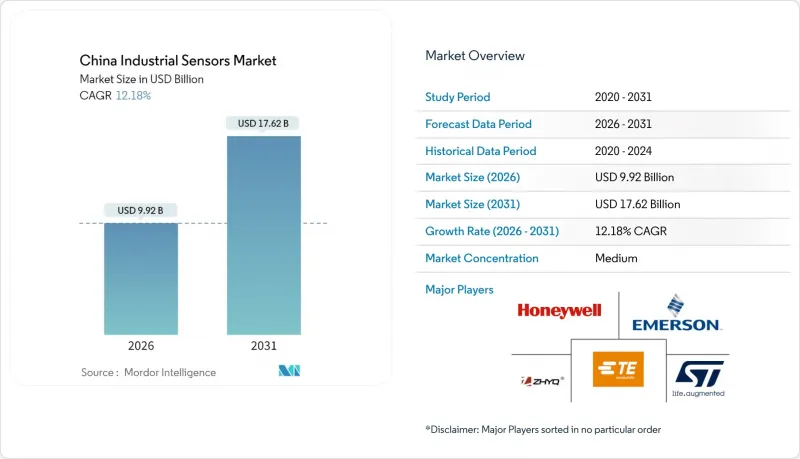

2025年中國工業感測器市場價值88.4億美元,預計2031年將達到176.2億美元,高於2026年的99.2億美元。

預測期(2026-2031 年)的複合年成長率預計為 12.18%。

這一成長動能反映了該國向智慧製造轉型、全國推行工業4.0以及為降低進口依賴而推出的廣泛在地化獎勵。在工廠數位化預算中,感測器維修的支出佔比已達15%以上,而《網路安全法》對邊緣運算的要求也推動了國產設備的普及。電動車產量激增、工業園區嚴格的碳排放管理法規以及不斷擴展的預測性維護計劃,進一步推動了汽車、流程和能源資產中多感測器技術的應用。競爭格局仍較為分散,大型外資企業為遵守採購法規而進行在地化生產,而本土新興企業則透過併購系統(MEMS)升級提升自身價值。

中國工業感測器市場趨勢及洞察

工業4.0的加速普及推動智慧工廠的感測器維修。

工廠正從獨立的自動化孤島向整合感測器網路轉型,這些網路能夠將持續資料傳輸到內部人工智慧平台。在2,000億元人民幣的公共資金中,約有15%被累計給了感測器,由此催生了一系列捆綁硬體、網路連接和分析服務的服務包。與西方工廠常見的逐步維修不同,中國製造商通常會在一次停產期內完成整條生產線的改造。網路安全法中關於邊緣運算的規定要求進行本地資料處理,這進一步推動了對國產人工智慧設備的需求。

政府激勵措施鼓勵國產感測器本地化

北京當局將感測器列為“關鍵技術”,由此帶來了補貼、稅收優惠和快速劃撥土地等一系列政策,每年採購額超過500億元。預計到2027年,中國對高階MEMS的進口依賴度將從2024年的80%以上降至50%以下。目前,國際主要製造商正紛紛成立合資企業,將核心製造流程引入中國,加速技術轉移,並提升本土人才能力。

對高階MEMS晶粒進口的高度依賴推高了元件成本。

先進的 MEMS晶粒主要來自台灣、韓國和德國,繼續佔精密級晶片供應的 70% 以上。在 2024 年半導體短缺期間,前置作業時間延長至 26 週,與完全在地採購相比,元件成本增加了 35-40%,降低了對成本敏感領域的價格競爭力。

細分市場分析

到2025年,壓力感測器將佔中國工業感測器市場26.42%的佔有率,其應用範圍廣泛,包括汽車煞車系統、石油化學管道和空調控制等。隨著關鍵設備的預測性維護計劃需要持續的壓力回饋迴路,該細分市場的收入預計將穩定成長。氣體感測器預計將以13.56%的複合年成長率快速成長,這主要得益於碳排放監測法規的實施以及先進的電化學和光聲技術在煙囪、電池工廠和廢氣洗滌設備中的應用。溫度和液位感測器在製藥、食品加工和水處理行業中保持穩定的訂單,這主要受監管部門對詳細溫度和液位記錄的要求所驅動。流量感測器和磁場感測器分別擴大應用於智慧城市供水網路和電動汽車馬達控制設備。加速感應器和橫擺角速度感測器正被整合到國內汽車製造商的自動駕駛研發流程中。

產品配置正從分立元件轉向將壓力、溫度和振動資料整合到單一MEMS堆疊中的封裝。供應商正與自動化廠商合作設計這些混合產品,以縮短安裝時間並簡化總線級佈線。分析訂閱服務的捆綁進一步模糊了硬體和業務收益之間的界限,為在這兩個領域都佔據主導地位的現有企業提供了永續的競爭優勢。對氣體檢測模組日益成長的需求正在推動MEMS晶粒製造商與封裝專家之間的合作,後者擁有即使在嚴苛的工業環境中也能封裝脆弱結構的先進技術。

預計到2025年,汽車產業將佔中國工業感測器市場27.35%的佔有率,反映了中國無與倫比的汽車組裝量和快速的電氣化進程。新能源汽車(NEV)配備的感測器數量約為燃油車(ICE)的2.5倍,即使總產量趨於穩定,需求依然強勁。電池溫度控管、高精度電流監測以及用於自動駕駛的慣性測量單元(IMU)是高附加價值細分市場。隨著民航業的復甦和軍事預算的增加,航太航太和國防領域的採購需求正在回升,推動了對能夠承受振動、輻射和極端溫度的堅固耐用型壓力感測器和慣性裝置的訂單激增。

醫療保健產業正以14.18%的複合年成長率快速成長,這主要得益於全國醫院數位化以及老齡化社會中遠端患者監護技術的進步。用於輸液泵的一次性MEMS壓力感測器、用於穿戴式裝置的非侵入式光學模組以及用於麻醉工作站的氣體感測器,代表日益廣泛的臨床應用。電子和半導體製造工廠正在持續推動無塵潔淨室監測的大規模採購項目。同時,發電公司正在將感測陣列整合到太陽能和風能發電設施以及併網設備中。石油天然氣、食品飲料和污水處理產業正在透過增強型感測器來改善安全和品質通訊協定,從而更好地服務其終端用戶群。

中國工業感測器市場報告按產品類型(壓力、溫度、液位等)、最終用戶(汽車、航太與軍事、化學與石化等)、感測技術(MEMS、非MEMS等)、外形規格(分離式感測器、整合模組、無線智慧節點)和地區進行細分。市場預測以美元以金額為準。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 工業4.0的引進正在加速智慧工廠感測器的維修。

- 政府激勵措施促進國內感測器生產的本地化

- 電動車產量快速成長,帶動多感測器需求增加。

- 預測性維護計劃推動了對壓力和振動感測器的需求

- 工業園區強制實施碳計量推動了對流量和氣體感測器的需求。

- 人工智慧驅動的邊緣分析為中小企業提供感測器即服務

- 市場限制

- 對高階MEMS晶粒進口的高度依賴推高了元件成本。

- 各國標準分散,使OEM認證變得複雜。

- 12吋MEMS晶圓短缺導致本地壓力晶片的大規模生產延遲。

- 歐盟新的網路安全規則增加了出口感測器的加密成本。

- 宏觀經濟因素的影響

- 產業價值鏈分析

- 監管環境

- 技術展望

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 依產品類型

- 壓力

- 溫度

- 等級

- 流動

- 磁場

- 加速度和偏航率

- 氣體

- 最終用戶

- 車

- 航太/軍事

- 化工/石油化工

- 醫療保健

- 電子和半導體

- 發電

- 石油和天然氣

- 食品/飲料

- 水和污水處理

- 其他最終用戶

- 透過檢測技術

- MEMS

- 非MEMS(散裝)

- 光學/光電

- 磁性/霍爾

- 按外形規格

- 分立感測器

- 整合模組

- 無線智慧節點

- 按地區

- 華東

- 華南

- 華北

- 華中地區

- 中國東北

- 中國西南地區

- 中國西北地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Honeywell International Inc.

- Emerson Electric Co.(Rosemount Inc.)

- STMicroelectronics NV

- TE Connectivity Ltd.(First Sensor AG)

- Shanghai Zhaohui Pressure Apparatus Co., Ltd.

- Ninghai Sendo Sensor Co., Ltd.

- TM Automation Instruments Co., Ltd.

- Xi'an UTOP Measurement Instrument Co., Ltd.

- Ericco International Limited

- Henan Hanwei Electronics Co., Ltd.

- Amphenol Advanced Sensors

- All Sensors Corporation

- Pepperl+Fuchs SE

- SICK AG

- Keyence Corporation

- Omron Corporation

- Yikoo Intelligent Technology Co., Ltd.

- Sodilong Automation Co., Ltd.

- ABB Ltd.

- Siemens AG(Process Instrumentation)

- Baumer Group

- Infineon Technologies AG

- Bosch Sensortec GmbH

第7章 市場機會與未來展望

The China industrial sensors market was valued at USD 8.84 billion in 2025 and estimated to grow from USD 9.92 billion in 2026 to reach USD 17.62 billion by 2031, at a CAGR of 12.18% during the forecast period (2026-2031).

This momentum reflects the country's pivot toward smart manufacturing, its nationwide Industry 4.0 roll-outs, and wide-ranging localization incentives that reduce import exposure. Factory digitization budgets increasingly earmark 15% of total spending for sensor retrofits, while edge-processing mandates under the Cybersecurity Law favor domestically built devices. Surging electric-vehicle (EV) output, strict carbon accounting rules at industrial parks, and expansive predictive maintenance programs further raise multi-sensor penetration across automotive, process, and energy assets. Competitive dynamics remain moderately fragmented as foreign majors localize production to comply with procurement rules and domestic challengers ascend the value curve through mergers, acquisitions, and MEMS upgrades.

China Industrial Sensors Market Trends and Insights

Industry 4.0 Deployment Accelerates Smart-Factory Sensor Retrofits

Factories are replacing stand-alone automation islands with unified sensor networks that stream continuous data to in-house AI platforms. Public funding of CNY 200 billion earmarked for smart upgrades reserves roughly 15% for sensors, creating a wave of bulk contracts that bundle hardware, connectivity, and analytics subscriptions. Unlike gradual retrofits common in Western plants, Chinese manufacturers often re-equip entire lines in a single shutdown window. Edge computing clauses in the Cybersecurity Law require local data processing, channeling demand toward domestically produced, AI-ready devices.

Government Incentives for Domestic Sensor Localization

Beijing's classification of sensors as a "critical technology" unlocks subsidies, tax breaks, and fast-track land allotments worth more than CNY 50 billion in annual procurement volume. The import dependence for high-end MEMS is expected to decline from over 80% in 2024 to below 50% by 2027. Foreign leaders are now pursuing joint ventures that embed core fabrication stages within China, accelerating technology transfer and scaling local workforce capabilities.

High Import Dependence for High-End MEMS Dies Inflates BOM Costs

Advanced MEMS dies, largely sourced from Taiwan, South Korea, and Germany, continue to account for more than 70% of the precision-grade supply. Lead times stretched to 26 weeks during the 2024 chip crunch, increasing the bill of materials by 35-40% compared to fully localized alternatives, and dampening price competitiveness in cost-sensitive sectors.

Other drivers and restraints analyzed in the detailed report include:

- EV Production Surge Increases Multi-Sensor Demand

- Predictive-Maintenance Programs Boost Pressure and Vibration Sensors

- 12-Inch MEMS Wafer Shortages Delay Localized Pressure-Chip Ramp-Up

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Pressure devices claimed a 26.42% share of the Chinese industrial sensors market in 2025, underscoring their cross-sector ubiquity in automotive braking, petrochemical pipelines, and HVAC controls. Segment revenue is expected to climb steadily as predictive-maintenance schemes mandate continuous pressure feedback loops in critical assets. Gas sensors, driven by carbon-monitoring laws, are projected to deliver the swiftest ascent at a 13.56% CAGR, incorporating sophisticated electrochemical and photoacoustic designs into smokestacks, battery plants, and waste-gas scrubbers. Temperature and level sensors consistently sustain orders from pharmaceuticals, food processing, and water treatment, where regulatory regimes require granular thermal and fill-level logging. Flow and magnetic field sensors are experiencing rising allocations in smart-city water grids and EV motor controllers, respectively, while acceleration and yaw-rate units are being integrated into autonomous-driving R&D cycles among domestic OEMs.

The product mix is shifting from discrete components toward integrated packages that consolidate pressure, temperature, and vibration data in a single MEMS stack. Suppliers co-design these hybrids with automation vendors to shorten installation time and simplify bus-level wiring. Bundled analytics subscriptions further blur the line between hardware and service revenue, giving incumbents that master both domains an enduring advantage. The growing appeal of gas-sensing modules encourages partnerships between MEMS die makers and packaging specialists who can encapsulate fragile structures for harsh industrial atmospheres.

Automotive lines absorbed 27.35% of the Chinese industrial sensors market size in 2025, reflecting the nation's unrivaled vehicle assembly volume and its rapid electrification curve. New-energy vehicles embed roughly 2.5X more sensors than internal-combustion models, boosting demand even as total unit output plateaus. Battery thermal management, high-precision current monitoring, and inertial measurement units for autonomy represent the highest-value niches. Aerospace and defense procurements are reviving as commercial flights rebound and military budgets expand, channeling orders for ruggedized pressure and inertial devices that withstand vibration, radiation, and extreme temperatures.

Medical applications, advancing at a 14.18% CAGR, benefit from nationwide hospital digitization and remote-patient monitoring for an aging population. Disposable MEMS pressure sensors in infusion pumps, non-invasive optical modules in wearables, and gas sensors in anesthetic workstations illustrate a widening clinical scope. Electronics and semiconductor fabs continue sizable purchasing programs for particle-free clean-room monitoring, while power-generation utilities integrate sensing arrays across solar, wind, and grid-balancing equipment. Oil, gas, food, beverage, and wastewater sectors modernize with sensor-enhanced safety and quality protocols, rounding out the end-user spectrum.

The China Industrial Sensors Market Report is Segmented by Product Type (Pressure, Temperature, Level, and More), End User (Automotive, Aerospace and Military, Chemical and Petrochemical, and More), Sensing Technology (MEMS, Non-MEMS, and More), Form Factor (Discrete Sensors, Integrated Modules, and Wireless Smart Nodes), and Region. The Market Forecasts are Provided in Terms of Value USD.

List of Companies Covered in this Report:

- Honeywell International Inc.

- Emerson Electric Co. (Rosemount Inc.)

- STMicroelectronics N.V.

- TE Connectivity Ltd. (First Sensor AG)

- Shanghai Zhaohui Pressure Apparatus Co., Ltd.

- Ninghai Sendo Sensor Co., Ltd.

- TM Automation Instruments Co., Ltd.

- Xi'an UTOP Measurement Instrument Co., Ltd.

- Ericco International Limited

- Henan Hanwei Electronics Co., Ltd.

- Amphenol Advanced Sensors

- All Sensors Corporation

- Pepperl+Fuchs SE

- SICK AG

- Keyence Corporation

- Omron Corporation

- Yikoo Intelligent Technology Co., Ltd.

- Sodilong Automation Co., Ltd.

- ABB Ltd.

- Siemens AG (Process Instrumentation)

- Baumer Group

- Infineon Technologies AG

- Bosch Sensortec GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Industry 4.0 deployment accelerates smart-factory sensor retrofits

- 4.2.2 Government incentives for domestic sensor localization

- 4.2.3 EV production surge increases multi-sensor demand

- 4.2.4 Predictive-maintenance programs boost pressure and vibration sensors

- 4.2.5 Mandated carbon-accounting at industrial parks drives flow and gas sensors

- 4.2.6 AI-enabled edge analytics makes sensor-as-a-service viable for SMEs

- 4.3 Market Restraints

- 4.3.1 High import dependence for high-end MEMS dies inflates BOM costs

- 4.3.2 Fragmented national standards complicate OEM qualification

- 4.3.3 12-inch MEMS wafer shortages delay localized pressure-chip ramp-up

- 4.3.4 New EU cybersecurity rules add encryption cost to export-grade sensors

- 4.4 Impact of Macroeconomic Factors

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Pressure

- 5.1.2 Temperature

- 5.1.3 Level

- 5.1.4 Flow

- 5.1.5 Magnetic Field

- 5.1.6 Acceleration and Yaw Rate

- 5.1.7 Gas

- 5.2 By End User

- 5.2.1 Automotive

- 5.2.2 Aerospace and Military

- 5.2.3 Chemical and Petrochemical

- 5.2.4 Medical

- 5.2.5 Electronics and Semiconductor

- 5.2.6 Power Generation

- 5.2.7 Oil and Gas

- 5.2.8 Food and Beverage

- 5.2.9 Water and Wastewater

- 5.2.10 Other End Users

- 5.3 By Sensing Technology

- 5.3.1 MEMS

- 5.3.2 Non-MEMS (Bulk)

- 5.3.3 Optical / Photoelectric

- 5.3.4 Magnetic / Hall

- 5.4 By Form Factor

- 5.4.1 Discrete Sensors

- 5.4.2 Integrated Modules

- 5.4.3 Wireless Smart Nodes

- 5.5 By Region

- 5.5.1 East China

- 5.5.2 South China

- 5.5.3 North China

- 5.5.4 Central China

- 5.5.5 Northeast China

- 5.5.6 Southwest China

- 5.5.7 Northwest China

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Honeywell International Inc.

- 6.4.2 Emerson Electric Co. (Rosemount Inc.)

- 6.4.3 STMicroelectronics N.V.

- 6.4.4 TE Connectivity Ltd. (First Sensor AG)

- 6.4.5 Shanghai Zhaohui Pressure Apparatus Co., Ltd.

- 6.4.6 Ninghai Sendo Sensor Co., Ltd.

- 6.4.7 TM Automation Instruments Co., Ltd.

- 6.4.8 Xi'an UTOP Measurement Instrument Co., Ltd.

- 6.4.9 Ericco International Limited

- 6.4.10 Henan Hanwei Electronics Co., Ltd.

- 6.4.11 Amphenol Advanced Sensors

- 6.4.12 All Sensors Corporation

- 6.4.13 Pepperl+Fuchs SE

- 6.4.14 SICK AG

- 6.4.15 Keyence Corporation

- 6.4.16 Omron Corporation

- 6.4.17 Yikoo Intelligent Technology Co., Ltd.

- 6.4.18 Sodilong Automation Co., Ltd.

- 6.4.19 ABB Ltd.

- 6.4.20 Siemens AG (Process Instrumentation)

- 6.4.21 Baumer Group

- 6.4.22 Infineon Technologies AG

- 6.4.23 Bosch Sensortec GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need assessment

工業感測器和自動化市場預測至2034年—按感測器類型、技術、產業、應用、最終用戶和地區分類的全球分析

工業感測器和自動化市場預測至2034年—按感測器類型、技術、產業、應用、最終用戶和地區分類的全球分析 工業感測器市場-全球市場規模、佔有率、趨勢、機會和預測:按產品、應用、地區和競爭對手分類,2021-2031年

工業感測器市場-全球市場規模、佔有率、趨勢、機會和預測:按產品、應用、地區和競爭對手分類,2021-2031年 美國工業感測器:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

美國工業感測器:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年) 工業感測器市場規模、佔有率和趨勢分析報告:按感測器類型、技術、最終用途、地區和細分市場預測(2025-2033 年)

工業感測器市場規模、佔有率和趨勢分析報告:按感測器類型、技術、最終用途、地區和細分市場預測(2025-2033 年) 工業感測器市場:2026-2032年全球市場預測(按感測器類型、技術、通訊協定、應用和銷售管道)

工業感測器市場:2026-2032年全球市場預測(按感測器類型、技術、通訊協定、應用和銷售管道) 工業感測器市場:按檢測方法、終端用戶產業和地區分類

工業感測器市場:按檢測方法、終端用戶產業和地區分類 工業感測器市場機會、成長要素、產業趨勢分析及2026年至2035年預測

工業感測器市場機會、成長要素、產業趨勢分析及2026年至2035年預測 半導體氣體感測器市場分析及預測至 2035 年:按類型、產品、技術、應用、材料類型、最終用戶、功能和安裝類型分類。工業感測器市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、最終用戶、功能、安裝類型、設備及解決方案分類

半導體氣體感測器市場分析及預測至 2035 年:按類型、產品、技術、應用、材料類型、最終用戶、功能和安裝類型分類。工業感測器市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、最終用戶、功能、安裝類型、設備及解決方案分類 日本工業自動化感測器市場規模、佔有率、趨勢及預測(按感測器類型、類型、自動化模式、最終用戶和地區分類,2026-2034年)

日本工業自動化感測器市場規模、佔有率、趨勢及預測(按感測器類型、類型、自動化模式、最終用戶和地區分類,2026-2034年)