|

市場調查報告書

商品編碼

2066695

歐洲環氧樹脂黏合劑:市場佔有率分析、產業趨勢和統計數據、成長預測(2026-2031)Europe Epoxy Adhesive - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

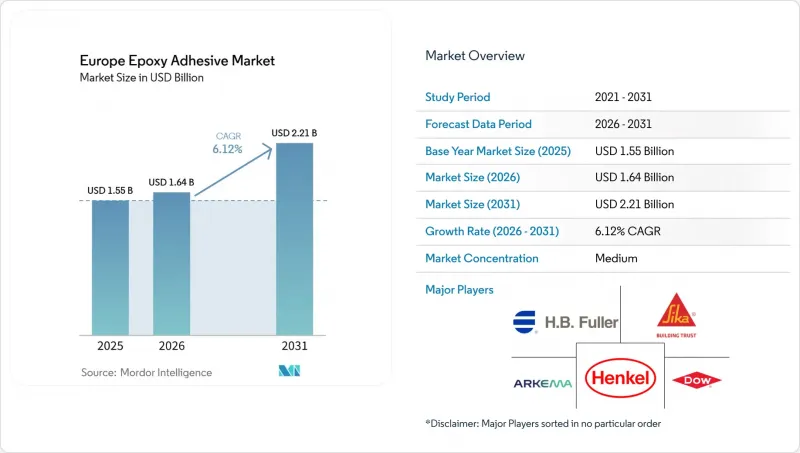

根據 Mordor Intelligence 預測,歐洲環氧樹脂黏合劑市場規模預計將在 2025 年達到 15.5 億美元,2026 年達到 16.4 億美元,到 2031 年達到 22.1 億美元,2026 年至 2031 年的複合年成長率為 6.12%。

本報告按終端用戶產業(航太與國防、汽車、船舶、電氣與電子、建築及其他終端用戶產業)、技術(反應型、溶劑型、紫外光固化型和水性)以及地區(法國、德國、義大利、俄羅斯、西班牙、英國、北歐國家及其他歐洲國家)進行細分。市場預測以美元計價。

歐洲環氧樹脂黏合劑市場的趨勢與洞察

電動車和輕型汽車結構膠合劑市場快速成長

在電池外殼、衝擊吸收結構和複合材料車身部件中,環氧樹脂黏合劑正日益取代焊接、鉚接和機械緊固件等傳統方法。添加陶瓷填料的導熱環氧樹脂的導熱係數可超過 2 W/m·K,搭接剪切強度高達 30 MPa。這種優異的性能能夠有效管理熱量,並實現模組和冷卻板之間的牢固粘合,從而承受衝擊載荷。電池形狀的多樣化,例如圓柱形、軟包形和片狀電池,對環氧樹脂黏合劑、壓敏黏著劑和間隙填充劑提出了獨特的需求。這些需求共同推動了歐洲汽車平台結構性黏著劑市場的發展。隨著汽車製造商 (OEM) 為追求輕量化而擴大採用鋁和纖維增強聚合物零件,對化學相容性黏合劑的需求也日益成長。這些黏合劑必須能夠承受 -40 度C至 80 度C的熱循環而不發生分層。西卡福斯(SikaForce)和威沃化學(WEVO-CHEMIE)等供應商目前正專注於研發用於電動車模組的矽基環氧樹脂,這些環氧樹脂的初始黏合強度超過2 MPa,導熱係數接近1.5 W/m*K。此外,採用機器人噴塗和線上紅外線固化技術的試驗生產線不僅縮短了生產週期,還有助於提高德國和法國超級工廠的採用率。基於這些趨勢,預計2026年至2028年歐洲電池應用環氧樹脂黏合劑市場將實現兩位數的銷售成長。

由於VOC/REACH法規,向高性能系統過渡。

2025年4月,歐盟委員會提案將批准期限限制為10年,並引入「必要用途」篩選機制,從而縮短傳統溶劑型系統的合規寬限期。BASF-西卡公司的胺基環氧固化劑Baxxodur EC 151an與傳統胺基體系相比,可將VOC排放降低90%,固化時間縮短三分之二,這顯示法規正在推動創新。隨著原始設備製造商(OEM)力求獲得ISO 14001認證,水性和紫外光固化化學品在家用電器、複合板和電子產品領域的應用日益廣泛。漢高收購ATP Adhesive Systems(其產品系列超過90%為水性產品),從策略上鞏固了其在歐洲環氧黏合劑市場的地位,目標客戶為汽車、電子和建築行業。這一監管趨勢表明,永續年成長率(CAGR)在整個預測期內將保持在較高水準。

雙酚A和環氧氯丙烷原料價格的波動

2025年,由於市場供應過剩,歐洲環氧樹脂價格下跌了12%,導致利潤率下降,採購的不確定性增加。 2025年6月,威斯萊克公司關閉了位於佩爾尼斯的工廠,該工廠生產環氧樹脂、雙酚A和環氧氯丙烷。隨後,英力士公司於2025年10月宣布關閉位於萊茵貝格的工廠,該工廠生產環氧氯丙烷和氯氣。同時,印度徵收反傾銷稅,導致亞洲環氧樹脂的通路轉移到歐洲,進一步加劇了價格波動。為了應對這種波動,黏合劑製造商已轉向與多家供應商簽訂契約,甚至開始引入生物基原料。儘管採取了這些措施,短期成本預測的難度仍然影響著歐洲環氧樹脂黏合劑市場的營運資金決策。

細分市場分析

預計到2025年,汽車產業將佔歐洲環氧樹脂黏合劑市場佔有率的23.18%,凸顯了環氧樹脂在提升車身剛性和衝擊吸收方面的持續優勢。隨著汽車產業的電氣化程度不斷提高,對導熱間隙填充劑、阻燃灌封樹脂和按需脫模解決方案的需求也日益成長,這些對於電池回收至關重要。由於搭接剪切強度要求達到15-23 MPa,工作溫度最高可達80 度C,每輛車的平均用量不斷增加,使得歐洲環氧樹脂黏合劑市場價格居高不下。電子業正以6.58%的複合年成長率成長,這主要得益於5G的部署和功率模組的小型化。這些發展需要導熱係數達到3 W/m*K或更高且具有高延伸率的黏合劑來解決熱膨脹係數不匹配的問題。在德國和波蘭,低黏度、室溫固化的矽凝膠正被應用於Mini-LED組裝,顯著降低了能耗。儘管家用電子電器產業週期可能出現疲軟,但在消費性電子產品、工業自動化和太陽能逆變器等多元化需求的推動下,預計銷售量將保持穩定成長。

建設產業佔環氧樹脂出貨量的第三大佔有率,歐盟的維修補貼推動了該產業的成長。這些補貼促進了低揮發性有機化合物(VOC)、高初始粘結強度的聚氨酯樹脂的使用,尤其是在外牆和保溫板的粘接方面。海洋、航太和可再生能源產業各自有著獨特的需求。例如,對一些高性能的特殊等級產品有需求,例如用於複合材料船體的耐濕甲基丙烯酸酯黏合劑和阻燃環氧樹脂。後者必須符合美國聯邦航空條例(FAR)25.853關於飛機內飾防火、防煙和防毒的標準。在能源領域,特別是離岸風力發電,優先選擇在30年使用壽命內保持25 kJ/m²或更高斷裂韌性的抗裂環氧樹脂。這些不同的細分市場共同增強了終端市場的韌性,並保護歐洲環氧樹脂黏合劑市場免受單一產業週期性波動的影響。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電動車和輕型汽車結構黏合技術蓬勃發展

- 建築和維修激增(歐盟綠色新政)

- 由於VOC和REACH法規的限制,向高性能系統過渡勢在必行。

- 用於離岸風力發電的大型葉片

- 在組裝中引入機器人點膠技術

- 市場限制因素

- 雙酚A和環氧氯丙烷原料價格的波動

- 雙酚A的毒理學和監管重新分類

- 生物基和混合型替代品的興起

- 價值鏈分析

- 監理情勢

- 波特五力分析

- 分銷通路分析

第5章 市場規模與成長預測

- 按最終用戶行業分類

- 航太/國防

- 車

- 海上

- 電氣和電子設備

- 建造

- 能源與電力

- 其他終端用戶產業

- 透過技術

- 反應型

- 溶劑型

- 紫外線固化

- 水性塗料

- 國家

- 法國

- 德國

- 義大利

- 俄羅斯

- 西班牙

- 英國

- 北歐國家

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- 3M

- Arkema

- BASF

- Beardow Adams

- DELO Industrial Adhesives

- Dow Inc.

- HB Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- ITW Performance Polymers

- Jowat SE

- MAPEI SpA

- Momentive Performance Materials

- PARKER HANNIFIN CORP

- Sika AG

- Soudal Holding NV

- tesa Tapes(India)Private Limited

- ThreeBond Europe

- Wacker Chemie AG

第7章 市場機會與未來展望

According to Mordor Intelligence, the europe epoxy adhesives market size is projected to be USD 1.55 billion in 2025, USD 1.64 billion in 2026, and reach USD 2.21 billion by 2031, growing at a CAGR of 6.12% from 2026 to 2031.

This report is Segmented by End-User Industry (Aerospace and Defense, Automotive, Marine, Electrical and Electronics, Construction, and Other End-User Industries), Technology (Reactive, Solvent-Borne, UV-Cured, and Water-Borne), and Geography (France, Germany, Italy, Russia, Spain, United Kingdom, NORDIC Countries, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

Europe Epoxy Adhesive Market Trends and Insights

Electric Vehicle and Lightweight-Vehicle Structural Bonding Boom

In battery housings, crash structures, and mixed-material body components, epoxy adhesives are increasingly supplanting traditional methods like welds, rivets, and mechanical fasteners. Modified with ceramic fillers, thermally conductive epoxies achieve a thermal conductivity of >=2 W/m*K and lap-shear strengths of up to 30 MPa. This capability facilitates module-to-cooling-plate interfaces that effectively manage heat and endure crash loads. The diversity in cell formats, such as cylindrical, pouch, and blade, drives a distinct demand for epoxies, pressure-sensitive tapes, and gap-fillers. This collective demand is expanding the footprint of the European structural adhesives market in vehicle platforms. As lightweighting trends push OEMs towards aluminum and fiber-reinforced polymer parts, the need arises for chemically compatible adhesives. These adhesives must withstand thermal cycling from -40 °C to 80 °C without delaminating. Supplier portfolios, including SikaForce and WEVO-CHEMIE, now highlight silicone grades with initial adhesion exceeding 2 MPa and thermal conductivities approaching 1.5 W/m*K, specifically for EV modules. Furthermore, pilot lines that incorporate robotic metering and in-line infrared curing are not only reducing takt times but also enhancing adoption rates in German and French gigafactories. Given these trends, the European epoxy adhesives market for battery applications is poised for double-digit volume growth from 2026 to 2028.

VOC/REACH-Driven Shift to High-Performance Systems

In April 2025, the European Commission proposed capping authorizations at 10 years and implementing an "essential use" filter, tightening the compliance window for legacy solvent-borne systems. BASF-Sika's Baxxodur EC 151an, an amine-based epoxy hardener, boasts 90% lower VOC emissions compared to traditional amine systems and reduces cure time by two-thirds, showcasing how regulation drives innovation. As OEMs chase ISO 14001 certifications, water-borne and UV-cured chemistries are winning more designs in appliances, engineered wood, and electronics. Henkel's acquisition of ATP Adhesive Systems, with a portfolio over 90% water-based, strategically boosts Henkel's foothold in Europe's epoxy adhesives market, targeting the automotive, electronics, and construction sectors. This regulatory trend suggests a sustained CAGR premium for sustainable grades throughout the forecast period.

BPA and Epichlorohydrin Feedstock Price Volatility

In 2025, European epoxy resin prices fell by 12% due to market oversupply, leading to tighter margins and heightened procurement uncertainties. Westlake shut down its Pernis facility, which produced epoxy resins, BPA, and epichlorohydrin, in June 2025. This was soon followed by Ineos's announcement in October 2025 to close its Rheinberg units for epichlorohydrin and chlorine. Meanwhile, India's imposition of anti-dumping duties shifted Asian epoxy flows towards Europe, exacerbating price fluctuations. To navigate this volatility, adhesive formulators are turning to multi-vendor contracts and are even delving into bio-based feedstocks. Despite these measures, the unpredictability of near-term costs continues to impact working-capital decisions in the European epoxy adhesives market.

Other drivers and restraints analyzed in the detailed report include:

- Offshore Wind Blade Upsizing

- Robotic Dispensing Adoption in Assembly Lines

- Toxicological/Regulatory Re-classification of BPA

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, the automotive sector accounted for 23.18% of Europe's epoxy adhesives market, highlighting a consistent preference for epoxies in enhancing body stiffness and crash absorption. As the industry electrifies, there's a growing demand for thermally conductive gap-fillers, flame-retardant potting resins, and debond-on-demand solutions, all pivotal for battery recycling. With lap-shear strength requirements set between 15-23 MPa and service temperatures reaching up to 80 °C, the average value per vehicle sees a boost, allowing the European epoxy adhesives market to maintain its premium pricing. The electronics sector is on a 6.58% CAGR trajectory, driven by 5G rollouts and the miniaturization of power modules. These advancements necessitate adhesives boasting thermal conductivity of >=3 W/m*K and high elongation to counter thermal mismatches. In Germany and Poland, assembly lines for Mini-LEDs are now opting for low-viscosity silicone gels that cure at room temperature, a move that slashes energy consumption. A diverse demand spanning consumer devices, industrial automation, and photovoltaic inverters ensures steady volume growth, even amidst potential softening in consumer electronics cycles.

Construction, ranking third in volume, is buoyed by EU renovation subsidies. These subsidies promote the use of low-VOC, high-grab polyurethanes, especially for bonding facades and insulation panels. The marine, aerospace, and renewable-energy sectors each have their unique demands. For instance, they seek niche high-performance grades, such as moisture-tolerant methacrylate adhesives for composite hulls and flame-retardant epoxies. The latter must adhere to FAR 25.853 standards concerning fire, smoke, and toxicity in aircraft interiors. Energy applications, particularly in offshore wind, prioritize crack-resistant epoxies, ensuring they maintain a fracture toughness of >=25 kJ/m2 over a 30-year lifecycle. Together, these diverse segments bolster end-market resilience, shielding the European epoxy adhesives market from the cyclical fluctuations of any single sector.

List of Companies Covered in this Report:

- 3M

- Arkema

- BASF

- Beardow Adams

- DELO Industrial Adhesives

- Dow Inc.

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- ITW Performance Polymers

- Jowat SE

- MAPEI S.p.A.

- Momentive Performance Materials

- PARKER HANNIFIN CORP

- Sika AG

- Soudal Holding N.V.

- tesa Tapes (India) Private Limited

- ThreeBond Europe

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Electric Vehicle and Lightweight-Vehicle Structural Bonding Boom

- 4.2.2 Construction Renovation Surge (EU Green Deal)

- 4.2.3 VOC/REACH-Driven Shift to High-Performance Systems

- 4.2.4 Offshore Wind Blade Upsizing

- 4.2.5 Robotic Dispensing Adoption in Assembly Lines

- 4.3 Market Restraints

- 4.3.1 BPA and Epichlorohydrin Feedstock Price Volatility

- 4.3.2 Toxicological/Regulatory Re-classification of BPA

- 4.3.3 Rise of Bio-based and Hybrid Alternatives

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

- 4.7 Distribution Channel Analysis

5 Market Size and Growth Forecasts (Value)

- 5.1 By End-User Industry

- 5.1.1 Aerospace and Defense

- 5.1.2 Automotive

- 5.1.3 Marine

- 5.1.4 Electrical and Electronics

- 5.1.5 Construction

- 5.1.6 Energy and Power

- 5.1.7 Other End-User Industries

- 5.2 By Technology

- 5.2.1 Reactive

- 5.2.2 Solvent-borne

- 5.2.3 UV-Cured

- 5.2.4 Water-borne

- 5.3 By Country

- 5.3.1 France

- 5.3.2 Germany

- 5.3.3 Italy

- 5.3.4 Russia

- 5.3.5 Spain

- 5.3.6 United Kingdom

- 5.3.7 NORDIC Countries

- 5.3.8 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/ Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 BASF

- 6.4.4 Beardow Adams

- 6.4.5 DELO Industrial Adhesives

- 6.4.6 Dow Inc.

- 6.4.7 H.B. Fuller Company

- 6.4.8 Henkel AG & Co. KGaA

- 6.4.9 Huntsman International LLC

- 6.4.10 ITW Performance Polymers

- 6.4.11 Jowat SE

- 6.4.12 MAPEI S.p.A.

- 6.4.13 Momentive Performance Materials

- 6.4.14 PARKER HANNIFIN CORP

- 6.4.15 Sika AG

- 6.4.16 Soudal Holding N.V.

- 6.4.17 tesa Tapes (India) Private Limited

- 6.4.18 ThreeBond Europe

- 6.4.19 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

環氧樹脂黏合劑市場報告:按產品類型、分銷管道、終端用戶產業和地區分類(2026-2034 年)

環氧樹脂黏合劑市場報告:按產品類型、分銷管道、終端用戶產業和地區分類(2026-2034 年) 雙組分環氧樹脂黏合劑市場規模、佔有率和成長分析:按樹脂類型、配方類型、固化機制、基材類型、應用、終端用戶產業、分銷管道和地區分類-2026-2033年產業預測

雙組分環氧樹脂黏合劑市場規模、佔有率和成長分析:按樹脂類型、配方類型、固化機制、基材類型、應用、終端用戶產業、分銷管道和地區分類-2026-2033年產業預測 環氧樹脂黏合劑市場:全球市場預測(依樹脂類型、技術、形態、應用和最終用途產業分類)-2026-2032年

環氧樹脂黏合劑市場:全球市場預測(依樹脂類型、技術、形態、應用和最終用途產業分類)-2026-2032年 亞太地區環氧樹脂黏合劑:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

亞太地區環氧樹脂黏合劑:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 全球環氧樹脂黏合劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)可注射錨固環氧樹脂市場(按最終用戶、應用和產品形式分類),全球預測,2026-2032年全球雙組分環氧樹脂粘合劑市場規模、佔有率、趨勢及成長分析報告(2026-2034)

全球環氧樹脂黏合劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)可注射錨固環氧樹脂市場(按最終用戶、應用和產品形式分類),全球預測,2026-2032年全球雙組分環氧樹脂粘合劑市場規模、佔有率、趨勢及成長分析報告(2026-2034) 2026年全球環氧樹脂粘合劑市場報告2026年全球純環氧樹脂注射式化學錨定劑市場報告2026年全球高強度環氧樹脂黏合劑市場報告

2026年全球環氧樹脂粘合劑市場報告2026年全球純環氧樹脂注射式化學錨定劑市場報告2026年全球高強度環氧樹脂黏合劑市場報告