|

市場調查報告書

商品編碼

2044259

亞太地區環氧樹脂黏合劑:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Asia-Pacific Epoxy Adhesive - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

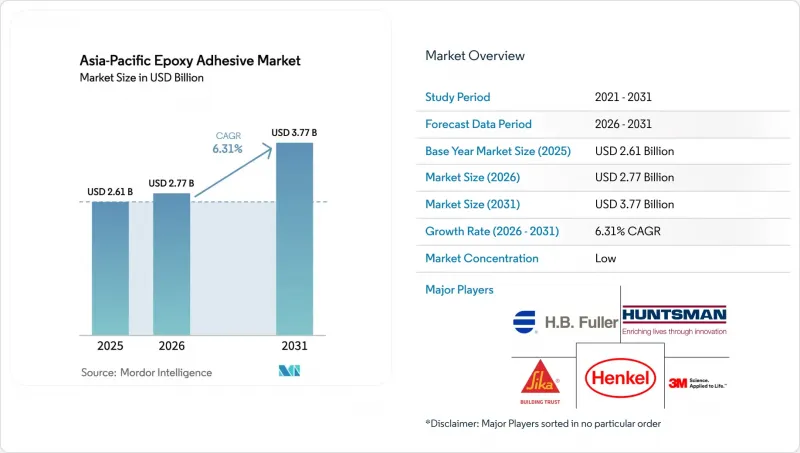

預計亞太地區環氧樹脂黏合劑市場將從 2025 年的 26.1 億美元成長到 2026 年的 27.7 億美元,然後在 2031 年達到 37.7 億美元,2026 年至 2031 年的複合年成長率為 6.31%。

交通運輸設備的穩定電氣化、半導體封裝投資的增加以及創紀錄的城市基礎設施支出,正在推動全部區域對結構性黏著劑的需求,預計這將使亞太環氧樹脂黏合劑市場增速高於全球平均水平。隨著汽車製造商採用輕質複合複合材料黏接代替焊接,雙組分反應型膠合劑的價格優勢依然強勁。同時,日益嚴格的室內空氣品質法規正促使建築項目轉向使用低VOC、可在接近室溫下固化的固化劑。大型化學企業正在擴大其區域實驗室的規模,以縮短電動車電池、光電晶片和高層建築外觀面板的配方開發週期,這使得擁有強大本地應用工程能力的公司獲得了競爭優勢。

亞太地區環氧樹脂黏合劑市場趨勢及洞察。

輕型電動車和轎車的產量迅速成長

在亞太地區,電動車 (EV) 製造工廠對黏合劑解決方案的應用日益廣泛,涵蓋電池模組、電芯到電池包 (CTP) 系統以及鋁複合材料車身面板等多種零件。隨著汽車製造商致力於將整車重量降低 15-20%,這一趨勢尤其推動了該地區環氧樹脂黏合劑市場的發展。比亞迪、現代汽車和 LG 能源解決方案等產業領導企業的大規模投資,正推動電池容量以數吉瓦時的速度成長。這些電池採用間隙填充環氧樹脂,這種環氧樹脂以其高導熱性和快速初始強度而聞名。此外,一種新近商業化的銀膠環氧樹脂,可在室溫下儲存長達六個月,正在革新碳化矽功率模組的生產方式。這項創新技術無需傳統的燒結工藝,不僅簡化了逆變器的生產流程,還能降低高達 40% 的能耗。

基礎設施快速發展和高層建築建設

預計到2025年,亞太地區各國政府將在建築領域投資超過5兆美元。快速的都市化推動了對幕牆玻璃、錨固水泥漿和修補砂漿的需求成長,而這些材料都依賴高韌性環氧樹脂。此外,新型低溫固化劑可在5度C至10度C範圍內固化,正在革新冬季混凝土澆築製程。這項創新技術在中國北方建築工地和印度高海拔鐵路項目中特別顯著,使施工人員無需使用昂貴的加熱毯。

雙酚A和環氧氯丙烷原料的價格波動

由於季度價格波動超過20%,沒有長期樹脂合約的中型複合材料生產商正面臨利潤率壓力。為了克服這一限制,東南亞的一些加工商正在轉向生物基環氧樹脂。這些由松香和腰果酚製成的環氧樹脂價格高出30%,但玻璃化轉變溫度超過230 度C。

細分市場分析

電子和半導體應用領域正以6.58%的複合年成長率快速成長。由於新竹和居林等地湧現出眾多功率元件和光子模組製造工廠,該領域的成長速度超過了汽車產業。然而,汽車產業仍是最大的貢獻者,佔23.18%的市場。亞太地區環氧樹脂黏合劑市場在該領域持續成長,主要得益於車身結構、電池組和動力傳動系統領域的應用。

高頻氮化鎵和碳化矽元件領域對體積導熱係數超過 150 W/mK 的銀填充環氧樹脂的需求不斷成長。這一趨勢正在加強化學品供應商和基板製造商之間的研發合作。此外,建築、能源和海洋領域的需求仍然穩定。政府對基礎設施的投資主要集中在橋樑、風力渦輪機葉片和船舶船體維修等項目上,這些項目都需要高模量黏接。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電動車和汽車輕量化製造的激增

- 對基礎設施和高層建築的快速投資

- 電子設備和半導體組裝的擴張

- 國內飛機專案採用在地化的資質要求。

- 反傾銷稅促進後向整合

- 市場限制因素

- BPA和ECH原料價格波動

- 溶劑型產品需遵守嚴格的揮發性有機化合物 (VOC) 和室內空氣品質 (IAQ) 法規。

- 水性環氧樹脂的性能差異與成本溢價

- 價值鏈分析

- 分銷鏈分析

- 監理情勢

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

- 分銷通路分析

第5章 市場規模與成長預測

- 按最終用戶行業分類

- 航太/國防

- 車

- 船

- 電氣和電子

- 建造

- 能源與電力

- 其他終端用戶產業

- 透過技術

- 反應性

- 溶劑型

- 紫外線固化型

- 水溶液

- 國家

- 澳洲

- 中國

- 印度

- 印尼

- 日本

- 馬來西亞

- 新加坡

- 韓國

- 泰國

- 亞太其他地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- 3M

- Arkema

- artience Co., Ltd.

- Avery Dennison Corporation

- BASF

- Dow Inc.

- Dymax Corporation

- HB Fuller Company

- Henkel AG & Co. KGaA

- Hubei Huitian New Materials Co., Ltd.

- Huntsman Corporation

- ITW Performance Polymers

- Jowat SE

- Kangda New Materials(Group)Co., Ltd.

- NANPAO RESINS CHEMICAL GROUP

- Permabond LLC

- Pidilite Industries Ltd.

- Sika AG

第7章 市場機會與未來展望

The Asia-Pacific epoxy adhesives market size is expected to grow from USD 2.61 billion in 2025 to USD 2.77 billion in 2026 and is forecast to reach USD 3.77 billion by 2031 at 6.31% CAGR over 2026-2031. Steady electrification of transport, an upturn in semiconductor packaging investments, and record urban infrastructure spending are converging to lift structural bonding demand across the region, allowing the Asia-Pacific epoxy adhesives market to outpace global averages. Two-component reactive systems continue to command pricing power as vehicle makers replace welding with lightweight composite bonding, while stringent indoor-air-quality rules are steering construction projects toward low-VOC hardeners that cure at near-ambient temperatures. Major chemical suppliers are scaling regional laboratories to shorten formulation cycles for electric-vehicle batteries, photonics chiplets, and high-rise facade panels, a shift that tilts competitive advantage toward firms with local application-engineering depth.

Asia-Pacific Epoxy Adhesive Market Trends and Insights

Surging EV And Lightweight Automotive Output

In the Asia-Pacific region, electric vehicle plants are increasingly turning to adhesive solutions for various components, including battery modules, cell-to-pack systems, and aluminum-composite body panels. This trend is bolstering the region's epoxy adhesives market, especially as original-equipment manufacturers aim to reduce curb weight by 15-20%. Major investments from industry giants like BYD, Hyundai, and LG Energy Solution are driving a multi-gigawatt-hour battery capacity. These batteries rely on gap-filling epoxies known for their high thermal conductivity and rapid green strength. Additionally, a newly commercialized silver-paste epoxy, which can be stored at room temperature for up to six months, is revolutionizing the production of silicon-carbide power modules. By eliminating the traditional sintering steps, this innovation not only streamlines inverter production but also reduces energy consumption by as much as 40%.

Rapid Infrastructure And High-Rise Construction

In 2025, governments across the Asia-Pacific region invested over USD 5 trillion in construction. This surge in urbanization heightened the demand for products like facade glazing, anchor grouts, and repair mortars, all of which depend on high-toughness epoxies. Additionally, a newly introduced low-temperature hardener, capable of curing between 5 °C and 10 °C, is revolutionizing winter concreting. This innovation is particularly beneficial for northern China's construction and India's high-altitude rail projects, eliminating the need for expensive heating blankets.

Volatility In Bisphenol A And Epichlorohydrin Feedstocks

Mid-tier mixers, lacking long-term resin contracts, face margin compression due to quarterly price swings exceeding 20%. As a restraint, several processors in Southeast Asia are turning to bio-based epoxies. These epoxies, sourced from rosin and cardanol, boast glass-transition temperatures surpassing 230 °C, albeit at a 30% price premium.

Other drivers and restraints analyzed in the detailed report include:

- Expansion Of Electronics And Semiconductor Assembly

- Anti-Dumping Tariffs Spurring Backward Integration

- Stringent VOC And Indoor-Air-Quality Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Electronics and semiconductor applications are expanding at a rate of 6.58% CAGR. This segment is surpassing the automotive sector as fabs for power devices and photonic modules emerge across regions, including Hsinchu and Kulim. The automotive sector, however, remains the largest contributor, holding a 23.18% share. The Asia-Pacific epoxy adhesives market within this segment continues to grow, driven by applications in vehicle structures, battery packs, and powertrains.

The high-frequency gallium-nitride and silicon-carbide devices segment is fueling demand for silver-filled epoxies with bulk thermal conductivity exceeding 150 W/m-K. This trend is strengthening R&D collaborations between chemical suppliers and substrate manufacturers. Additionally, the construction, energy, and marine segments collectively maintain steady demand. Government investments in infrastructure are focusing on projects such as bridges, wind blades, and hull refurbishments, all of which require high-modulus bonding.

The Asia-Pacific Epoxy Adhesives Market Report is Segmented by End-User Industry (Aerospace and Defense, Automotive, Electrical and Electronics, Construction, Other End-User Industries), Technology (Reactive, Solvent-Borne, UV-Cured, Water-Borne), and Geography (Australia, China, India, Indonesia, Japan, Malaysia, Singapore, South Korea, Thailand, Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- 3M

- Arkema

- artience Co., Ltd.

- Avery Dennison Corporation

- BASF

- Dow Inc.

- Dymax Corporation

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Hubei Huitian New Materials Co., Ltd.

- Huntsman Corporation

- ITW Performance Polymers

- Jowat SE

- Kangda New Materials (Group) Co., Ltd.

- NANPAO RESINS CHEMICAL GROUP

- Permabond LLC

- Pidilite Industries Ltd.

- Sika AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in EV and lightweight automotive manufacturing

- 4.2.2 Rapid infrastructure and high-rise construction spending

- 4.2.3 Expansion of electronics and semiconductor assembly

- 4.2.4 Domestic aircraft programs adopt localized qualifications

- 4.2.5 Anti-dumping tariffs spurring backward integration

- 4.3 Market Restraints

- 4.3.1 Volatile BPA and ECH feedstock prices

- 4.3.2 Stringent VOC and IAQ regulations on solvent systems

- 4.3.3 Performance gap and cost premium of water-borne epoxies

- 4.4 Value Chain Analysis

- 4.5 Distribution Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Distribution Channel Analysis

5 Market Size & Growth Forecasts (Value)

- 5.1 By End-User Industry

- 5.1.1 Aerospace and Defense

- 5.1.2 Automotive

- 5.1.3 Marine

- 5.1.4 Electrical and Electronics

- 5.1.5 Construction

- 5.1.6 Energy and Power

- 5.1.7 Other End-User Industries

- 5.2 By Technology

- 5.2.1 Reactive

- 5.2.2 Solvent-borne

- 5.2.3 UV-Cured

- 5.2.4 Water-borne

- 5.3 By Country

- 5.3.1 Australia

- 5.3.2 China

- 5.3.3 India

- 5.3.4 Indonesia

- 5.3.5 Japan

- 5.3.6 Malaysia

- 5.3.7 Singapore

- 5.3.8 South Korea

- 5.3.9 Thailand

- 5.3.10 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 artience Co., Ltd.

- 6.4.4 Avery Dennison Corporation

- 6.4.5 BASF

- 6.4.6 Dow Inc.

- 6.4.7 Dymax Corporation

- 6.4.8 H.B. Fuller Company

- 6.4.9 Henkel AG & Co. KGaA

- 6.4.10 Hubei Huitian New Materials Co., Ltd.

- 6.4.11 Huntsman Corporation

- 6.4.12 ITW Performance Polymers

- 6.4.13 Jowat SE

- 6.4.14 Kangda New Materials (Group) Co., Ltd.

- 6.4.15 NANPAO RESINS CHEMICAL GROUP

- 6.4.16 Permabond LLC

- 6.4.17 Pidilite Industries Ltd.

- 6.4.18 Sika AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

環氧樹脂黏合劑市場報告:按產品類型、分銷管道、終端用戶產業和地區分類(2026-2034 年)

環氧樹脂黏合劑市場報告:按產品類型、分銷管道、終端用戶產業和地區分類(2026-2034 年) 雙組分環氧樹脂黏合劑市場規模、佔有率和成長分析:按樹脂類型、配方類型、固化機制、基材類型、應用、終端用戶產業、分銷管道和地區分類-2026-2033年產業預測

雙組分環氧樹脂黏合劑市場規模、佔有率和成長分析:按樹脂類型、配方類型、固化機制、基材類型、應用、終端用戶產業、分銷管道和地區分類-2026-2033年產業預測 環氧樹脂黏合劑市場:全球市場預測(依樹脂類型、技術、形態、應用和最終用途產業分類)-2026-2032年

環氧樹脂黏合劑市場:全球市場預測(依樹脂類型、技術、形態、應用和最終用途產業分類)-2026-2032年 全球環氧樹脂黏合劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)可注射錨固環氧樹脂市場(按最終用戶、應用和產品形式分類),全球預測,2026-2032年全球雙組分環氧樹脂粘合劑市場規模、佔有率、趨勢及成長分析報告(2026-2034)

全球環氧樹脂黏合劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)可注射錨固環氧樹脂市場(按最終用戶、應用和產品形式分類),全球預測,2026-2032年全球雙組分環氧樹脂粘合劑市場規模、佔有率、趨勢及成長分析報告(2026-2034) 2026年全球環氧樹脂粘合劑市場報告2026年全球純環氧樹脂注射式化學錨定劑市場報告2026年全球高強度環氧樹脂黏合劑市場報告環氧彩色砂漿市場按包裝類型、最終用途產業、應用和分銷管道分類-2026-2032年全球預測

2026年全球環氧樹脂粘合劑市場報告2026年全球純環氧樹脂注射式化學錨定劑市場報告2026年全球高強度環氧樹脂黏合劑市場報告環氧彩色砂漿市場按包裝類型、最終用途產業、應用和分銷管道分類-2026-2032年全球預測