|

市場調查報告書

商品編碼

2066593

光連接模組:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Optical Interconnect - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

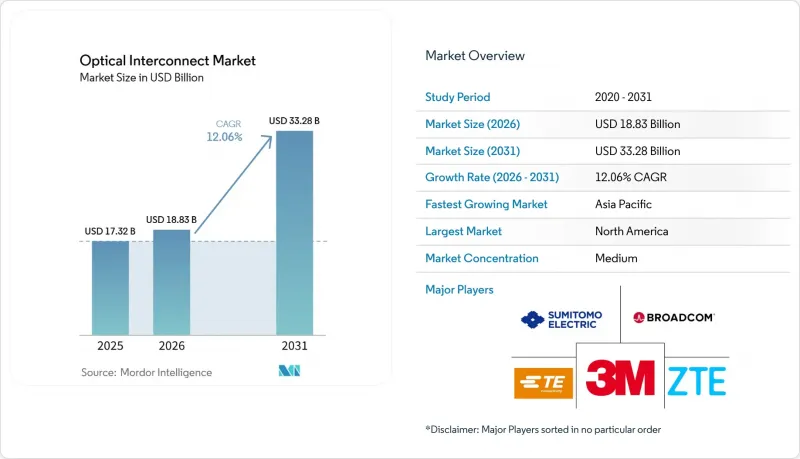

根據 Mordor Intelligence 預測,光連接模組市場規模預計將在 2025 年達到 173.2 億美元,2026 年達到 188.3 億美元,到 2031 年達到 332.8 億美元,2026 年至 2031 年的複合年成長率為 12.06%。

[1] 康寧公司,《面向人工智慧資料中心的光纖連接》,corning.com。這一成長趨勢的驅動力來自人工智慧和高效能運算工作負載日益成長的頻寬需求、從銅纜到光電的轉變,以及超超大規模資料中心業者資本投資的快速成長。本報告按產品(光收發器、光纖組件等)、互連等級(晶片間、基板間/機架級等)、光纖模式(單模光纖和多模光纖)、資料速率(低於 40 Gbps、40-100 Gbps 及其他)、應用(通訊和資料通訊)以及地區進行細分。

全球光連接模組市場趨勢與洞察

通訊頻寬需求不斷成長

生成式人工智慧叢集所需的光纖數量是傳統雲端服務的 10 到 100 倍,這使得現有銅纜互連的物理極限接近極限,並加速了向光電的過渡。 Meta 的內部架構在機架邊界處已經面臨銅纜傳輸距離的限制,這促使企業加大對光纖拓撲的投資,以支援橫向擴展領域中數百Terabit每秒的傳輸速度。高速乙太網路連接埠的出貨量預計將從 2023 年的 7,000 萬個成長到 2026 年的 2.4 億個以上,這反映了 1.6T 介面的日益普及。現代 GPU叢集指定了 200Tbps 的東西向頻寬,這意味著每個光纖鏈路需要部署超過 3000 根光纖。這種規模直接惠及提供高密度光子整合技術的供應商。持續的流量成長正在推動長距離資料中心互連 (DCI) 環境中伺服器、交換器和光連接模組組件的多年訂單。

加大對資料中心互聯的投資

光是微軟就簽署了超過80億美元的新暗纖合約,以加強其分散式雲端骨幹網路。 Dell'Oro預測,到2028年,人工智慧後端網路市場規模將超過200億美元,這意味著未來十年光連接模組的需求將超過伺服器的整體支出。超大規模資料中心業者目前正在投資建造自己的海底光纜,預計到2029年,海底光纜投資將達到98億美元。此舉將進一步擴大連貫傳輸系統的潛在市場規模。預計未來五年內,區域交換點的流量將成長六倍,光連接模組市場正受惠於來自分散式互連和骨幹網路升級的穩定需求。由於各通訊業者都在尋求最大限度地降低已鋪設光纖的每位元成本,因此能夠提供800G和1.6T光學模組的供應商預計將獲得顯著的市場佔有率。

下一代科技的商業化進程有所延遲

儘管研發方面取得了顯著進展,但由於光網際網路論壇 (OIF) 的可靠性測試和標準化流程比預期更長,共封裝光元件預計仍需數年時間才能廣泛應用。Terabit傳輸速率下的熱限制要求採用符合嚴格認證標準的新型封裝材料和散熱器,這延長了系統原始設備製造商 (OEM) 的設計週期。薄膜鈮酸鋰光電前景廣闊,但仍面臨脆性和良率方面的挑戰,導致除中國少數試點工廠外,其他地區的量產進程受阻。這些商業化進程的延遲為通訊業者必須在面向未來的發展和可靠的可靠性之間取得平衡,同時也阻礙了光連接模組市場對尖端解決方案的短期應用。

細分市場分析

據博通公司稱,就產品級銷售額而言,光連接模組市場目前以收發器為主導,預計到2025年將佔總銷售額的36.40%。然而,嵌入式光學模組的成長速度最快,複合年成長率高達22.1%,這主要得益於ASIC設計人員持續推進交換機底盤內共封裝光元件的檢驗。傳統的主動光纜在即插即用部署中仍然很受歡迎,但由於通訊業者傾向於選擇能夠處理更長傳輸距離的隔離式光學模組,其成長速度有所放緩。光纜組件和連接器與整體光纖市場的成長保持同步,銷售穩定,且沒有整合光電那樣陡峭的成本曲線。博通公司的51.2 Tbps CPO平台與插入式光纜相比,能量損耗降低了70%,這也解釋了為什麼嵌入式模組的市佔率持續擴大。英特爾的光I/O晶片組以5 pJ/bit的功耗實現了4 Tbps的雙向吞吐量,這一突破性的能效提升表明,一旦封裝良率成熟,嵌入式設計將成為其自然的替代選擇(intel.com)。 OpenLight和Jabil等製造聯盟正在加速整合組件的上市進程,這預示著光互連市場正向嵌入式光技術進行更廣泛的轉型。

中期來看,嵌入式模組有望從插入式模組手中奪取部分市場佔有率,同時在散熱設計預算限制導致傳統外形尺寸無法採用的領域開拓新市場。許多超大規模資料中心業者將繼續並行採購嵌入式和插入式模組,直到產業互通性成熟。這將確保即使成長軸發生轉變,收發器收入也能保持穩定。同時,CPO(光纖通道模組)的變體是 1.6T 和 3.2T 光纖交換架構藍圖的核心,確保了背板光學模組的充足供應。嵌入式模組緩解了提高前面板密度的壓力,使機架設計人員能夠減少底盤深度或添加加速器來提高整體運算密度。這些產品類型之間的相互作用凸顯了為何廣泛的產品系列對於旨在保持光連接模組市場活力並確保從超大規模資料中心業者獲得設計訂單的供應商至關重要。

到2025年,闆對板和機架級鏈路將佔光連接模組市場佔有率的44.20%,這反映了當今模組化伺服器的設計趨勢。矽光電將實現繞過PCB走線的封裝內光通道,晶片對晶片鏈路的複合年成長率預計將達到26.9%。城域和長途資料中心互連(DCI)解決方案仍然至關重要,但由於引進週期較長和監管障礙,其成長速度較慢。技術要求也有所不同。晶片對晶片的光纖通訊旨在實現亞納秒延遲和每太Terabit效率,而DCI設備則致力於最佳化頻譜效率和放大器級聯。

Marvell 在 OFC 2025 上示範的 PCIe Gen 6光纖傳輸,可在 10 公尺光纖上實現 64 GT/s 的資料傳輸速率,支援 CPU 和 GPU 分離的解耦式電腦架。 Ayar Labs 的資金籌措輪凸顯了人們對單晶片式光 I/O 的日益成長的信心,這種方案能夠打破傳統的記憶體和快取層級結構。隨著共封裝光元件從原型走向量產,基板設計人員正將雷射光源放置在更靠近 ASIC 的位置,以降低插入損耗和插件面板的熱密度。然而,服務供應商仍然需要機架級鏈路來確保向後相容性,從而彌合傳統脊葉式拓撲結構與下一代光纖網路之間的差距。這些混合需求趨勢正在推動光連接模組市場各個互連層級的營收成長。

區域分析

預計到2025年,北美將引領光連接模組市場,佔據33.60%的市場佔有率,這主要得益於超大規模資料中心業者的集中以及英特爾等公司數十年來在矽光電的研究投入。對專有光纖資產的資本投資仍然強勁,例如微軟與Lumen達成的數十億美元的暗纖交易,證實了短期內對高速光纖通訊設備的需求存在穩固的下限。該地區的併購,例如AMD收購Enosemi以及諾基亞以23億美元收購Infinera,正在為總部位於美國的各公司增加設計人才和智慧財產權。根據《晶片技術創新法案》(CHIPS Act),聯邦政府持續投資於先進封裝和光電津貼,進一步增強了北美製造業的韌性,尤其是在磷化銦晶圓和異構整合領域。

亞太地區以13.05%的複合年成長率成為成長最快的地區,這主要得益於中國的國家光電戰略、台灣晶圓代工廠產能的提升以及區域對端到端供應鏈的投資。由台積電主導的矽光電產業聯盟匯集了30多家企業,透過提供統一的製程設計套件,降低了製造准入門檻,縮短了新參與企業的學習曲線。中國的CHIPX中試生產線正在6吋晶圓上製造薄膜鈮酸鋰,使國內企業在下一代調變器領域擁有領先優勢。各地區政府都在為用於商業工作負載和國家研究的人工智慧運算叢集提供津貼,確保了預測期內對Terabit特級光纖通訊設備的持續需求。台灣晶圓廠與美國雲端服務供應商之間的合作進一步模糊了區域界限,最終將提升亞太地區光連接模組市場的整體需求。

到2024年,歐洲在全球光元件生產中的佔有率將降至8%以下。為此,歐盟委員會提案了《光電晶片法案》,旨在重振國內產能。儘管到2024年,歐洲光電企業在研發方面的投資超過120億歐元,但在商業化方面仍落後於北美和亞太地區。諸如「Photonics21」計畫以及德國和法國的國家計畫旨在到2027年將試點生產線的數量加倍。在企業發展趨勢方面,普睿司曼以9.5億美元收購Channell Commercial Corporation,擴大了其在北美和中東資料中心專案的光纖連接業務基礎,體現了其務實的全球化策略。儘管該地區仍然擁有技術優勢,但光連接模組市場的成長取決於合作資金籌措和更快捷的技術轉移機制,以將創新轉化為量產產品。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對通訊頻寬的需求不斷成長(雲端運算、人工智慧、高效能運算)

- 增加對資料中心互連(DCI)建置的投資

- 超大規模資料中心向 400G/800G 的快速過渡

- 矽光電收發器的商業化

- 向共封裝光元件 (CPO) 過渡到交換器專用積體電路 (ASIC)

- 薄膜鈮酸鋰(LNOI)光電在長距離鏈路的應用。

- 市場限制因素

- 下一代光連接模組技術的商業化進程有所延遲

- 800G/1.6T光學模組和先進封裝需要高額資本投入。

- CPO和整合光電中的溫度控管挑戰

- 磷化銦晶片和封裝供應瓶頸

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 依產品

- 光收發器

- 主動光纜(AOC)

- 嵌入式光學模組(EOM)

- 電纜組件

- 光纖連接器

- 互連等級

- 晶片之間

- 基板對板/機架級

- 地鐵/長途 DCI

- 光纖模式

- 單模光纖

- 多模光纖

- 按資料傳輸速度

- 低於 40 Gbps

- 40~100 Gbps

- 100~400 Gbps

- 超過 400 Gbps

- 透過使用

- 電訊

- 資料通訊

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ASEAN

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- UAE

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- 3M Company

- Amphenol Corporation

- Broadcom Inc.

- Ciena Corporation

- Cisco Systems Inc.

- Coherent Corp.(formerly II-VI)

- CommScope Holding Co.

- Corning Incorporated

- FIT Hon Teng(Molex)Ltd.

- Go!Foton Inc.

- Huawei Technologies Co. Ltd.

- Infinera Corporation

- Intel Corporation

- Lumentum Holdings Inc.

- NVIDIA Corporation

- Samtec Inc.

- Sumitomo Electric Industries Ltd.

- TE Connectivity Ltd.

- ZTE Corporation

- 其他(專注於特定領域的光子學新創公司)

第7章 市場機會與未來展望

According to Mordor Intelligence, the optical interconnect market size is projected to be USD 17.32 billion in 2025, USD 18.83 billion in 2026, and reach USD 33.28 billion by 2031, growing at a CAGR of 12.06% from 2026 to 2031.

[1] Corning Incorporated, "Fiber Connectivity for AI-Ready Data Centers," corning.com Rising bandwidth requirements from artificial intelligence and high-performance computing workloads, the migration from copper to photonics, and rapidly expanding hyperscaler capital expenditure underpin this growth trajectory. This report is Segmented by Product (Optical Transceivers, Cable Assemblies, and More), Interconnect Level (Chip-To-Chip, Board-To-Board / Rack-Level, and More), Fiber Mode (Single-Mode Fiber and Multi-Mode Fiber), Data-Rate ( Less Than 40 Gbps, 40-100 Gbps, and More), Application (Telecommunication and Data Communication), and Geography.

Global Optical Interconnect Market Trends and Insights

Increasing Demand for Communication Bandwidth

Generative AI clusters require 10-100 times more fiber than traditional cloud services, pushing existing copper interconnects past their physical limits and forcing an accelerated transition to photonics. Meta's internal architectures already show copper reach constraints at the rack boundary, guiding investment toward optical topologies that support hundreds of terabits per second in scale-out domains. High-speed Ethernet port shipments are projected to climb from 70 million in 2023 to more than 240 million in 2026, mirroring the ramp of 1.6 T interfaces. Modern GPU clusters now specify 200 Tbps of east-west bandwidth, translating into installations that exceed 3,000 fibers per fabric link, a scale that directly benefits vendors of dense photonic integration. This persistent traffic curve underpins multi-year orders for optical interconnect components across servers, switches, and long-haul DCI footprints.

Rising Data-Center Interconnect Investments

Microsoft alone has secured more than USD 8 billion in new dark-fiber contracts to reinforce its distributed cloud backbone. Dell'Oro projects AI back-end networks surpassing USD 20 billion by 2028, implying that optical interconnect market demand will outpace general server spending through the decade. Hyperscalers are now funding their own submarine cables, raising subsea investment to USD 9.8 billion by 2029, a move that further widens the addressable base for coherent transport systems. With traffic growth at regional exchange points expected to multiply sixfold within five years, the optical interconnect market benefits from a stable pipeline of DCI and backbone upgrades. Vendors equipped to deliver 800 G and 1.6 T optics stand to capture outsized share as operators seek to maximize cost-per-bit on each installed fiber.

Slow Commercialization of Next-Generation Technologies

Co-packaged optics remains several years away from mass adoption despite visible R&D momentum, as reliability testing and standardization through the Optical Internetworking Forum take longer than anticipated. Thermal constraints at terabit speeds require new packaging materials and heat spreaders that pass strict qualification regimes, extending design cycles for system OEMs. Thin-film lithium-niobate photonics, though promising, still faces brittleness and yield challenges, delaying the high-volume availability of the material outside a few pilot fabs in China. These commercialization lags introduce planning risk for operators that must balance future-proofing with proven reliability, tempering near-term adoption rates for bleeding-edge solutions in the optical interconnect market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid 400 G/800 G Migration

- Commercial Silicon-Photonics Adoption

- High Capital Expenditure Requirements

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The optical interconnect market size for product-level sales centers on transceivers, which held a 36.40% revenue position in 2025, according to Broadcom. Embedded optical modules, however, are growing fastest at a 22.1% CAGR as ASIC designers validate co-packaged optics inside switch chassis. Traditional active optical cables remain popular for plug-and-play deployments, but their growth moderates as operators favor separate optics that scale to longer reaches. Cable assemblies and connectors track overall fiber growth, providing steady volume without the steep cost curves of integrated photonics. Broadcom's 51.2 Tbps CPO platform shows 70% lower energy dissipation than pluggables, illustrating why embedded modules will keep gaining share. Intel's optical I/O chiplet delivers 4 Tbps bidirectional throughput at 5 pJ/bit, a power milestone that positions embedded designs as the logical successor once packaging yields mature intel.com. Manufacturing alliances such as OpenLight and Jabil shorten time-to-market for integrated parts, signaling a broader pivot toward embedded optics inside the optical interconnect market.

The medium-term outlook suggests that embedded modules will cannibalize a portion of pluggables but also open new sockets where thermal budgets forbid traditional form factors. Many hyperscalers will dual-source embedded and pluggable parts until industry-wide interoperability matures, preserving transceiver revenue even as growth shifts. Meanwhile, CPO variants sit at the center of switch roadmaps for 1.6 T and 3.2 T fabrics, guaranteeing a sizable pipeline for backplane optics. Because embedded modules reduce front-panel density pressures, rack architects can shrink chassis depth or add accelerators, improving overall compute density. The interplay among these product categories keeps the optical interconnect market dynamic and underscores why broad portfolios are critical for vendors courting hyperscaler design wins.

Board-to-board and rack-level links accounted for 44.20% of optical interconnect market share in 2025, reflecting today's modular server designs. Silicon photonics now enables on-package optical lanes that bypass PCB traces, driving chip-to-chip links to a 26.9% CAGR outlook. Metro and long-haul DCI solutions remain essential yet grow at a steadier clip because of longer deployment cycles and regulatory hurdles. The technology needs differ: chip-to-chip optics target sub-nanosecond latency and watt-per-terabit efficiencies, whereas DCI equipment optimizes spectral efficiency and amplifier cascades.

PCIe Gen 6 over optics, demonstrated by Marvell at OFC 2025, sends 64 GT/s traffic across 10 m fibers, enabling disaggregated compute racks that decouple CPUs and GPUs. Ayar Labs' funding round underscores confidence in monolithic optical I/O that can break traditional memory and cache hierarchies. As co-packaged optics migrates from prototypes to volume switches, board designers will place laser sources near ASICs, lowering insertion loss and reducing pluggable face-plate thermal density. However, service providers still require rack-level links for backwards compatibility, bridging the transition from legacy spine-leaf topologies to next-generation fabrics. This hybrid demand profile supports incremental revenue across all interconnect levels in the optical interconnect market.

Geography Analysis

North America led the optical interconnect market with a 33.60% share in 2025 thanks to hyperscaler concentration and decades-long silicon-photonics research programs by firms such as Intel. Capital spending on proprietary fiber assets remains robust, seen in Microsoft's multibillion-dollar dark-fiber contracts with Lumen, underlining a strong near-term demand floor for high-speed optics. Regional merger activity, including AMD's acquisition of Enosemi and Nokia's USD 2.3 billion purchase of Infinera, adds both design talent and intellectual property to domestically headquartered firms. Continued Federal investment in advanced packaging and CHIPS Act photonics grants further strengthens North American manufacturing resilience, particularly for indium-phosphide wafers and heterogeneous integration.

Asia Pacific is the fastest-growing region at a 13.05% CAGR, driven by China's national photonics strategy, Taiwan's foundry leverage, and regional investments in end-to-end supply chains. The Silicon Photonics Industry Alliance organized by TSMC includes over 30 companies and offers unified process design kits, lowering fabrication barriers and shortening learning curves for new entrants. China's CHIPX pilot lines manufacture thin-film lithium-niobate on 6-inch wafers, giving domestic players a head start in next-generation modulators. Regional governments subsidize AI computing clusters that serve both commercial workloads and national research, ensuring sustained demand for terabit-scale optics over the forecast window. Collaboration between Taiwanese fabs and US cloud providers further blurs regional boundaries but ultimately inflates aggregate Asia-Pacific volumes in the optical interconnect market.

Europe's optical production slipped below 8% of global share by 2024, prompting the European Commission to propose a Photonics Chips Act aimed at revitalizing domestic capacity. European photonics firms collectively spent more than EUR 12 billion on R&D in 2024, yet commercialization gaps persist relative to North America and Asia Pacific. Initiatives from Photonics21 and national programs in Germany and France pledge to double the number of pilot lines by 2027. On the corporate front, Prysmian's USD 950 million acquisition of Channell Commercial Corporation expands the group's fiber-connectivity footprint in North American and Middle-East data-center projects, reflecting a pragmatic globalization strategy. While the region remains technologically capable, its optical interconnect market growth depends on coordinated funding and faster technology-transfer pipelines to scale innovations into volume products.

- 3M Company

- Amphenol Corporation

- Broadcom Inc.

- Ciena Corporation

- Cisco Systems Inc.

- Coherent Corp. (formerly II-VI)

- CommScope Holding Co.

- Corning Incorporated

- FIT Hon Teng (Molex) Ltd.

- Go!Foton Inc.

- Huawei Technologies Co. Ltd.

- Infinera Corporation

- Intel Corporation

- Lumentum Holdings Inc.

- NVIDIA Corporation

- Samtec Inc.

- Sumitomo Electric Industries Ltd.

- TE Connectivity Ltd.

- ZTE Corporation

- Others (additional niche photonic start-ups)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing demand for communication bandwidth (cloud, AI, HPC)

- 4.2.2 Rising investments in data-center interconnect (DCI) build-outs

- 4.2.3 Rapid 400G/800G migration across hyperscale data centres

- 4.2.4 Commercial adoption of silicon-photonics transceivers

- 4.2.5 Shift toward co-packaged optics (CPO) for switch ASICs

- 4.2.6 Emergence of thin-film lithium-niobate (LNOI) photonics for long-reach links

- 4.3 Market Restraints

- 4.3.1 Slow commercialisation of next-gen optical interconnect tech

- 4.3.2 High capex for 800G/1.6T optics and advanced packaging

- 4.3.3 Thermal-management challenges in CPO and integrated photonics

- 4.3.4 Indium-phosphide wafer and packaging supply bottlenecks

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter'ss Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product

- 5.1.1 Optical Transceivers

- 5.1.2 Active Optical Cables (AOC)

- 5.1.3 Embedded Optical Modules (EOM)

- 5.1.4 Cable Assemblies

- 5.1.5 Optical Connectors

- 5.2 By Interconnect Level

- 5.2.1 Chip-to-Chip

- 5.2.2 Board-to-Board / Rack-Level

- 5.2.3 Metro and Long-Haul DCI

- 5.3 By Fiber Mode

- 5.3.1 Single-Mode Fiber

- 5.3.2 Multi-Mode Fiber

- 5.4 By Data-Rate

- 5.4.1 less than 40 Gbps

- 5.4.2 40-100 Gbps

- 5.4.3 100-400 Gbps

- 5.4.4 above 400 Gbps

- 5.5 By Application

- 5.5.1 Telecommunication

- 5.5.2 Data Communication

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 ASEAN

- 5.6.4.6 Rest of Asia Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 UAE

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 3M Company

- 6.4.2 Amphenol Corporation

- 6.4.3 Broadcom Inc.

- 6.4.4 Ciena Corporation

- 6.4.5 Cisco Systems Inc.

- 6.4.6 Coherent Corp. (formerly II-VI)

- 6.4.7 CommScope Holding Co.

- 6.4.8 Corning Incorporated

- 6.4.9 FIT Hon Teng (Molex) Ltd.

- 6.4.10 Go!Foton Inc.

- 6.4.11 Huawei Technologies Co. Ltd.

- 6.4.12 Infinera Corporation

- 6.4.13 Intel Corporation

- 6.4.14 Lumentum Holdings Inc.

- 6.4.15 NVIDIA Corporation

- 6.4.16 Samtec Inc.

- 6.4.17 Sumitomo Electric Industries Ltd.

- 6.4.18 TE Connectivity Ltd.

- 6.4.19 ZTE Corporation

- 6.4.20 Others (additional niche photonic start-ups)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

光連接模組市場規模、佔有率、趨勢和預測:按產品類型、互連等級、光纖模式、應用、最終用戶產業和地區分類,2026-2034 年

光連接模組市場規模、佔有率、趨勢和預測:按產品類型、互連等級、光纖模式、應用、最終用戶產業和地區分類,2026-2034 年 光連接模組市場:按組件、資料傳輸速率、傳輸距離、光纖類型、外形規格和應用分類-2026-2032年全球市場預測

光連接模組市場:按組件、資料傳輸速率、傳輸距離、光纖類型、外形規格和應用分類-2026-2032年全球市場預測 全球資料中心光連接模組市場:預測(至 2034 年)-按元件、資料速率、技術、距離、最終使用者和地區分類的分析

全球資料中心光連接模組市場:預測(至 2034 年)-按元件、資料速率、技術、距離、最終使用者和地區分類的分析 共封裝光學元件 (CPO) 與光互連專利格局分析 (2026)

共封裝光學元件 (CPO) 與光互連專利格局分析 (2026) 2026年全球光連接模組市場報告2026年超短光連接模組全球市場報告全球共封裝光模組市場(按組件、資料速率、整合類型、技術、應用和最終用戶分類)預測(2026-2032年)

2026年全球光連接模組市場報告2026年超短光連接模組全球市場報告全球共封裝光模組市場(按組件、資料速率、整合類型、技術、應用和最終用戶分類)預測(2026-2032年) 光互連市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2026-2034)

光互連市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2026-2034) 光連接模組市場規模、佔有率和成長分析(按產品類型、互連等級、光纖模式和地區分類)-2026-2033年產業預測

光連接模組市場規模、佔有率和成長分析(按產品類型、互連等級、光纖模式和地區分類)-2026-2033年產業預測 超短距離光連接模組市場規模、佔有率、趨勢分析報告:按數據速率、距離、產品、技術、地區、細分市場預測,2025-2030 年

超短距離光連接模組市場規模、佔有率、趨勢分析報告:按數據速率、距離、產品、技術、地區、細分市場預測,2025-2030 年