|

市場調查報告書

商品編碼

2066576

加密資產:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)Cryptocurrency - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

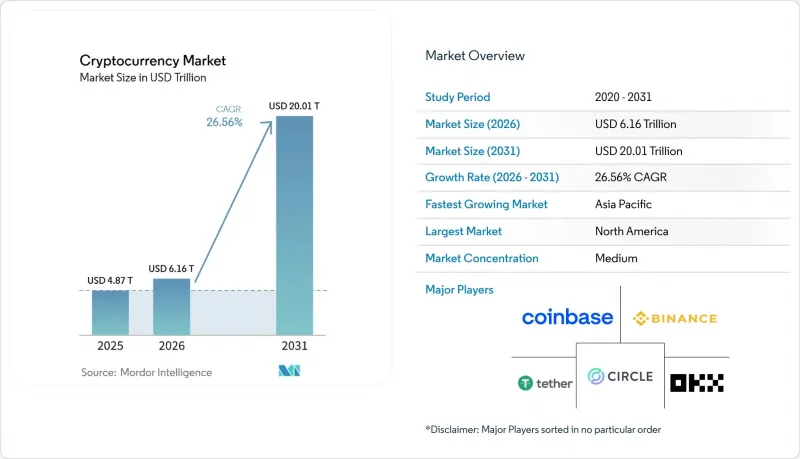

根據 Mordor Intelligence 預測,加密貨幣市場規模預計將從 2025 年的 4.87 兆美元成長到 2026 年的 6.16 兆美元,到 2031 年達到 20.1 兆美元,2026 年至 2031 年的複合年成長率為 26.56%。

本報告按交易用途(支付和匯款、交易和投資匯款、其他)、用戶類型(個人、機構)、加密貨幣(BTC、ETH、Ripple、Bitcoin Cash、Cardano、其他)以及地區(北美、南美、歐洲、亞太、中東和非洲)進行分類。市場預測以美元計價。

全球加密貨幣市場趨勢與洞察

受監管的實體比特幣 ETF 的激增正在推動機構投資者的資金流入。

2024年1月,美國批准現貨比特幣交易所交易產品(ETP),建立了一個高度透明且監管完善的框架,為退休基金、捐贈基金和諮詢平台等機構委託管理比特幣鋪平了道路。該產品結構符合審慎投資者的規則,並減少了直接託管帶來的操作摩擦,從而提升了機構需求,推動了加密資產市場的成長。美國的批准和持續的監管參與向其他司法管轄區發出了強烈的訊號,加速了產品創新進程,包括在受監管市場中推出加密資產ETP選項和多元資產基金設計。託管機構透明的儲備揭露,以及經審計的基金管理,增強了機構投資者的合規能力,並縮短了實質審查所需的時間。這些進展使比特幣投資在主流投資政策中成為常態,並擴大了參與市場的機構投資者範圍。

在整個歐元區實施MiCA將創造一個和諧的跨境基礎設施。

《加密資產市場監管條例》(MiCA)於2024年底在歐盟全面生效,以單一的發行方和仲介業者通行證制度取代了先前分散的國家法規。到2025年12月,已有超過100家加密資產服務供應商獲得MiCA授權,使其能夠憑藉單一許可證為整個歐洲經濟區(EEA)的客戶提供服務,並減少了重複的合規負擔。統一的穩定幣發行和託管規則降低了跨境摩擦,並加強了消費者保護。因此,該地區的機構投資者信心增強,服務範圍也隨之擴大。 MiCA規定的資本和風險管理要求提高了准入門檻,並促進了符合營運韌性和資訊揭露標準的營運商之間的整合。到2025年,受監管的歐元計價穩定幣已廣泛流通,顯示在不斷發展的歐洲市場中,對受監管結算資產的需求日益成長。

對電網的反對以及礦業活動的暫時中止限制了產能擴張。

政策制定者和電網營運商對高能耗的工作量證明(PoW)機制帶來的電力需求表示擔憂。這影響了與加密貨幣市場相關的大型設施的許可程序和永續性資訊揭露要求。歐洲監管發展強調在金融消費者保護之外,還需揭露氣候和營運風險,增加了尋求擴張企業的合規成本。人工智慧工作負載加劇了資料中心容量的競爭,提高了電力和土地使用的機會成本,限制了某些地區挖礦供應的擴張。 2025年的投資決策反映出部分運算基礎設施正轉向盈利更高的人工智慧應用,減少了市場增加挖礦容量的空間。這些壓力正在推動中期內向更高的效率和更最佳化的位置方向發展,同時也增強了離網可再生能源的合法性以及參與能源市場需量反應的必要性。

細分市場分析

預計到2025年,交易和投資轉移將佔加密貨幣市場佔有率的49.52%,並將在2031年之前以31.24%的複合年成長率成長。這反映了市場結構向受監管衍生性商品和交易所交易的轉變。向受監管交易所的過渡加深了流動性,降低了交易對手風險,增強了機構投資者在市場中有效對沖和再平衡的能力。穩定幣結算繼續支持平台間抵押品和現金等價物的快速流動,提高了資本效率和市場響應能力。受監管產品的擴展提高了營運標準和託管保障,促進了大規模的交易和更廣泛的參與。因此,加密貨幣市場建立了更強大的交易基礎,風險管理更加清晰,並與傳統金融體系建立了更緊密的聯繫。

在支付和匯款領域,受監管的發行機構擴大了與銀行的合作,並加強了合規架構,以支持個人和企業用戶的應用場景,從而提升了穩定幣在跨境匯款中的效用,並受益於此趨勢。在「去中心化金融協議流程」類別中,金融負責人和市場創造者繼續對擔保貸款、流動性提供和代幣化抵押策略表現出濃厚的興趣,而風險管理工具也在不斷改進。 「其他」類別涵蓋跨境B2B支付、資產代幣化和NFT相關活動,隨著資產管理公司推出鏈上基金並於2025年開始與支付網路開展支付試點項目,該類別的範圍也日益多元化。總而言之,這些趨勢表明,儘管支付和交易在加密貨幣市場的短期交易量中佔據最大佔有率,但其應用範圍正在不斷擴大。因此,加密貨幣行業正在開發基礎設施和合規機制,以適應日常匯款和專業風險管理等應用情境。

區域分析

預計到2025年,北美將佔據35.38%的市場佔有率,並將繼續受益於受監管的交易所交易產品(ETP)、機構託管服務以及鼓勵專業人士參與加密貨幣市場的強勁衍生品市場。美國對穩定幣和交易所的政策監管不斷推進,提高了服務供應商和投資者的透明度,從而增強了流動性和市場深度。經審計託管機構的擴張改善了資產管理公司和企業財務部門的進入管道,促進了大規模資金進入市場。加拿大和跨境匯款管道的出現,增加了對數位美元和低成本匯款的需求,推動了該地區市場以實用性主導的成長。這些因素共同維持了北美在產品廣度、合規性和機構採用率的領先地位。

亞太地區預計將成為成長最快的地區,到2031年複合年成長率將達到29.24%,這主要得益於支付應用場景的拓展、區域監管的細化以及各國央行在加密貨幣市場相關支付模式方面的探索。監管機構已在金融中心為穩定幣和仲介業者設立了許可製度,為機構投資者的運作提供了保障。付款管道和超級應用程式擴大了消費者和商家獲取數位美元的管道,支援了匯款管道和電子商務結算。跨國試點計畫持續測試跨國即時全額支付,展現了公共和私人代幣在市場整合區域支付系統中的長期作用。這些發展共同促進了亞太地區參與度的提升和基礎設施投資的增加。

以MiCA為核心的歐洲框架在其27個成員國之間建構了統一的許可環境,並建立了通行證制度,從而減少了重複的合規負擔。這促進了該地區加密貨幣市場的業務擴大策略。獲得許可的CASP(加密貨幣資產服務提供者)在2025年擴大了跨境企業發展,受監管的歐元計價穩定幣透過與銀行的合作和支付試點計畫獲得了市場認可。隨著鏈上產品規模的擴大,監管機構正在為穩定幣和DeFi(去中心化金融)制定風險管理框架,以確保金融穩定和投資者權益。主要資產管理公司的代幣化基金擴大了銷售網路,加強了與專業投資者的互動,並強化了與資本市場的連結。這些政策和產品的變化共同表明,歐洲正繼續朝著更深入、更安全的市場參與邁進。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 受監管的實體比特幣ETF數量激增(2024-2025年)

- MiCA在歐元區的全國部署將促進跨境加密貨幣服務的擴展。

- 亞太地區和海灣合作理事會國家央行數位貨幣試點計畫的快速進展正在推動支付試驗。

- 人工智慧驅動的合規工具正在降低詐欺造成的損失率。

- 納斯達克100指數競爭對手公司財務實施狀況

- 在非洲和東南亞的行動超級應用程式中整合USDC支付路徑

- 市場限制因素

- 斯堪的納維亞和美國對能源網路和少數族裔暫停令的抵制

- 分散的KYC/AML執法超出了MiCA的範圍。

- 穩定幣脫鉤引發了儲備金要求的收緊。

- 區塊鏈工程人才流失到生成式人工智慧領域。

- 價值鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- 環境影響分析

第5章 市場規模與成長預測

- 按交易目的

- 支付和匯款

- 資金透過交易和投資進行流動

- 去中心化金融(DeFi)協議的資金流動

- 其他(跨境B2B支付、資產代幣化和結算、NFT購買)

- 依使用者類型

- 零售

- 機構投資者

- 透過加密貨幣

- BTC

- ETH

- Ripple

- Bitcoin Cash

- Cardano

- 其他

- 按地區

- 北美洲

- 加拿大

- 美國

- 墨西哥

- 南美洲

- 巴西

- 秘魯

- 智利

- 阿根廷

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 比荷盧經濟聯盟

- 北歐的

- 其他歐洲國家

- 亞太地區

- 印度

- 中國

- 日本

- 澳洲

- 韓國

- 東南亞

- 其他亞太國家

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Coinbase Global Inc.

- Binance Holdings Ltd.

- Tether Limited(USDT)

- Circle Internet Financial LLC(USDC)

- OKX(OK Group)

- Kraken(Payward Inc.)

- KuCoin

- Huobi(HTX)

- Bybit Fintech Ltd.

- Bitfinex

- Gate.io

- Bitstamp Ltd.

- Gemini Trust Company LLC

- Upbit Exchange(Dunamu Inc.)

- Bithumb Korea Co. Ltd.

- Bitget(Singapore)

- MEXC Global

- Coincheck Inc.

- Bitso SA de CV

- Coinone

第7章 市場機會與未來展望

According to Mordor Intelligence, the cryptocurrency market size is expected to increase from USD 4.87 trillion in 2025 to USD 6.16 trillion in 2026 and reach USD 20.01 trillion by 2031, growing at a CAGR of 26.56% over 2026-2031.

This report is Segmented by Transaction Purpose (Payments & Remittances, Trading and Investment Transfers, and More), User Type (Retail, Institutional), Cryptocurrency (BTC, ETH, Ripple, Bitcoin Cash, Cardano, Others), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Cryptocurrency Market Trends and Insights

Surge in Regulated Spot-Bitcoin ETFs Unlocking Institutional Capital

The approval of spot Bitcoin exchange-traded products in the United States in January 2024 created a transparent and regulated wrapper that opened fiduciary access for pensions, endowments, and advisory platforms. Institutional demand increased as the product structure aligned with prudent investor rules and reduced operational frictions associated with direct custody, which has reinforced the growth profile of the Cryptocurrency market. U.S. approval and continued supervisory engagement improved the signalling effect for other jurisdictions and accelerated product innovation pipelines, including options on crypto ETPs and multi-asset fund designs in regulated venues. The combination of transparent reserve disclosures at custodians and audited fund operations strengthened compliance readiness for institutional allocators and reduced due diligence cycle times. These developments helped normalize Bitcoin exposure within mainstream investment policy statements and broadened the addressable base of institutions participating in the market.

Euro-Wide MiCA Roll-Out Creating Harmonized Cross-Border Infrastructure

The Markets in Crypto-Assets Regulation became fully enforceable across the European Union in late 2024, replacing divergent national rules with a single passporting framework for issuers and intermediaries. By December 2025, over 100 Crypto-Asset Service Providers operated under MiCA authorization, which allowed a single license to serve clients across the European Economic Area and reduced duplicative compliance overhead. Unified rules for stablecoin issuance and custodial operations lowered cross-border frictions and improved consumer safeguards, which in turn increased institutional confidence to scale services in the region's Cryptocurrency market. Capital and risk management requirements under MiCA raised the threshold for entry and are supporting consolidation among providers that meet operational resilience and disclosure standards. Compliant euro-denominated stablecoins gained traction during 2025, signalling rising demand for regulated settlement assets in Europe's evolving market .

Energy-Grid Backlash and Miner Moratoria Constraining Capacity Expansion

Policymakers and grid operators raised concerns about power demand from energy-intensive proof-of-work operations, which influenced permitting processes and sustainability disclosure requirements tied to large installations interacting with the Cryptocurrency market. European rulemaking has emphasized climate and operational risk disclosures alongside financial consumer protection, which raises compliance costs for operators seeking expansion. Heightened competition for data centre capacity from AI workloads increased the opportunity cost of electricity and land use, which constrained supply growth for mining in several sites. Investment decisions in 2025 reflected pivot dynamics where some compute infrastructure migrated to higher-yield AI applications, reducing the headroom for mining capacity additions within the market. These pressures support a medium-run shift toward efficiency upgrades and location optimization while reinforcing the case for off-grid renewables and demand response participation in energy markets.

Other drivers and restraints analyzed in the detailed report include:

- Rapid CBDC Pilots in APAC and GCC Accelerating Settlement Infrastructure

- AI-Powered Compliance Tools Reducing Fraud-Loss Ratios

- Fragmented KYC and AML Enforcement Creating Compliance Arbitrage

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Trading and Investment Transfers accounted for 49.52% of the Cryptocurrency market share in 2025 and are projected to grow at a 31.24% CAGR through 2031, reflecting a structural shift toward regulated derivatives and exchange-traded access. The transition to compliant trading venues deepened liquidity and reduced counterparty risk, which strengthened the ability of institutions to hedge and rebalance efficiently in the market. Stablecoin settlement continued to support the rapid movement of collateral and cash equivalents across platforms, improving capital efficiency and market responsiveness. As regulated products scaled, operational standards and custody assurances improved, supporting larger ticket sizes and broader participation. The result is a more durable trading foundation in the crypto market, with clearer risk controls and integration points to traditional finance.

Payments and Remittances benefited from growing stablecoin utility for cross-border flows as regulated issuers expanded banking partnerships and compliance coverage that supports retail and enterprise use cases. The Decentralized Finance Protocol Flows category continued to attract treasurers and market makers to secured lending, liquidity provisioning, and tokenized collateral strategies where risk tooling is improving. The Others category, which includes cross-border B2B settlements, asset tokenization, and NFT-related activity, diversified in 2025 as asset managers launched on-chain funds and settlement pilots with payment networks. Together, these trends point to a broader utility mix, with payments and trading carrying the largest weight in near-term volumes within the Cryptocurrency market. The Cryptocurrency industry is therefore aligning infrastructure and compliance with use cases that connect to everyday money movement and professional risk management.

Geography Analysis

North America held 35.38% in 2025 and continued to benefit from regulated ETPs, institutional custody, and deep derivatives markets that attract professional participation in the Cryptocurrency market. U.S. policy advances on stablecoin oversight and exchange oversight increased clarity for service providers and investors, which supported liquidity and market depth. The scale of audited custodians improved access for asset managers and corporate treasuries, which facilitated on-ramps for large pools of capital. Canada and cross-border remittance corridors contributed incremental demand for digital dollars and low-cost transfers, which reinforced utility-driven growth in the region's market. Together, these elements sustained North America's leadership in product breadth, compliance, and institutional adoption.

Asia-Pacific is projected to be the fastest-growing region at 29.24% CAGR through 2031 on the back of payment use cases, regional regulatory clarity, and central bank experimentation that shape settlement models relevant to the crypto market. Regulators advanced licensing regimes for stablecoins and intermediaries in financial hubs, which provided guardrails for institutional operations. Payment platforms and super-apps expanded digital dollar access for consumers and merchants, which supported remittance corridors and e-commerce payments. Multi-country pilots continued to test real-time gross settlement across borders, which informs the long-run role of public and private tokens in regional payment systems that interface with the market. These trends collectively underpin rising participation and infrastructure investment in Asia-Pacific.

Europe's framework, centred on MiCA, created a harmonized licensing environment across 27 member states and enabled passporting that reduces duplicative compliance, which supports scale-up strategies in the region's Cryptocurrency market. Authorized CASPs expanded operations across borders in 2025, and compliant euro-denominated stablecoins gained adoption through banking partnerships and payment pilots. Supervisors are advancing risk frameworks for stablecoins and DeFi to ensure financial stability and investor protection as on-chain products scale. Tokenized funds from major asset managers extended distribution and engagement among professional investors, which strengthened linkages with capital markets. Together, these policy and product shifts keep Europe on a path toward deeper, safer participation in the market.

- Coinbase Global Inc.

- Binance Holdings Ltd.

- Tether Limited (USDT)

- Circle Internet Financial LLC (USDC)

- OKX (OK Group)

- Kraken (Payward Inc.)

- KuCoin

- Huobi (HTX)

- Bybit Fintech Ltd.

- Bitfinex

- Gate.io

- Bitstamp Ltd.

- Gemini Trust Company LLC

- Upbit Exchange (Dunamu Inc.)

- Bithumb Korea Co. Ltd.

- Bitget (Singapore)

- MEXC Global

- Coincheck Inc.

- Bitso S.A. de C.V.

- Coinone

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in regulated spot-Bitcoin ETFs (2024-25)

- 4.2.2 Euro-wide MiCA roll-out unlocking cross-border crypto services

- 4.2.3 Rapid CBDC pilots in Asia-Pacific & GCC boosting settlement trials

- 4.2.4 AI-powered compliance tools lowering fraud-loss ratios

- 4.2.5 Corporate treasury adoption by NASDAQ-100 constituents

- 4.2.6 Mobile-super-apps in Africa & SEA integrating USDC rails

- 4.3 Market Restraints

- 4.3.1 Energy-grid backlash & miner moratoria in Nordics & U.S.

- 4.3.2 Fragmented KYC / AML enforcement outside MiCA scope

- 4.3.3 Stable-coin de-pegs triggering tighter reserve mandates

- 4.3.4 Blockchain-engineering talent drain to Gen-AI sector

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Environmental Impact Analysis

5 Market Size & Growth Forecasts (Value)

- 5.1 By Transaction Purpose

- 5.1.1 Payments & Remittances

- 5.1.2 Trading and Investment Transfers

- 5.1.3 Decentralized Finance (DeFi) Protocol Flows

- 5.1.4 Others (Cross-border B2B Settlements, Asset Tokenization & Settlements, NFT Purchases)

- 5.2 By User Type

- 5.2.1 Retail

- 5.2.2 Institutional

- 5.3 By Cryptocurrency

- 5.3.1 BTC

- 5.3.2 ETH

- 5.3.3 Ripple

- 5.3.4 Bitcoin Cash

- 5.3.5 Cardano

- 5.3.6 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 Canada

- 5.4.1.2 United States

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Peru

- 5.4.2.3 Chile

- 5.4.2.4 Argentina

- 5.4.2.5 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Spain

- 5.4.3.5 Italy

- 5.4.3.6 BENELUX

- 5.4.3.7 NORDICS

- 5.4.3.8 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 India

- 5.4.4.2 China

- 5.4.4.3 Japan

- 5.4.4.4 Australia

- 5.4.4.5 South Korea

- 5.4.4.6 South East Asia

- 5.4.4.7 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Nigeria

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market-level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Coinbase Global Inc.

- 6.4.2 Binance Holdings Ltd.

- 6.4.3 Tether Limited (USDT)

- 6.4.4 Circle Internet Financial LLC (USDC)

- 6.4.5 OKX (OK Group)

- 6.4.6 Kraken (Payward Inc.)

- 6.4.7 KuCoin

- 6.4.8 Huobi (HTX)

- 6.4.9 Bybit Fintech Ltd.

- 6.4.10 Bitfinex

- 6.4.11 Gate.io

- 6.4.12 Bitstamp Ltd.

- 6.4.13 Gemini Trust Company LLC

- 6.4.14 Upbit Exchange (Dunamu Inc.)

- 6.4.15 Bithumb Korea Co. Ltd.

- 6.4.16 Bitget (Singapore)

- 6.4.17 MEXC Global

- 6.4.18 Coincheck Inc.

- 6.4.19 Bitso S.A. de C.V.

- 6.4.20 Coinone

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

加密貨幣交易平台市場-2026-2032年全球市場預測加密貨幣市場-2026年至2032年全球市場預測

加密貨幣交易平台市場-2026-2032年全球市場預測加密貨幣市場-2026年至2032年全球市場預測 加密貨幣交易所:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)穩定幣:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

加密貨幣交易所:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)穩定幣:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 全球加密貨幣交易平台市場規模、佔有率、趨勢和成長分析報告(2026-2034年)數位貨幣市場:按貨幣類型、平台、應用和最終用戶分類-2026-2032年全球市場預測

全球加密貨幣交易平台市場規模、佔有率、趨勢和成長分析報告(2026-2034年)數位貨幣市場:按貨幣類型、平台、應用和最終用戶分類-2026-2032年全球市場預測 穩定幣和數位貨幣支付基礎設施市場預測至2034年-全球分析(按組件、穩定幣類型、基礎設施層、支付類型、應用、最終用戶和地區分類)

穩定幣和數位貨幣支付基礎設施市場預測至2034年-全球分析(按組件、穩定幣類型、基礎設施層、支付類型、應用、最終用戶和地區分類) 2026年全球穩定幣合規市場報告

2026年全球穩定幣合規市場報告 加密貨幣ATM市場:按類型、按加密貨幣類型、按地區分類

加密貨幣ATM市場:按類型、按加密貨幣類型、按地區分類 加密貨幣交易平台市場規模、佔有率和成長分析:按交易所類型、交易形式、部署形式、加密貨幣類型、最終用戶和地區分類-2026-2033年產業預測

加密貨幣交易平台市場規模、佔有率和成長分析:按交易所類型、交易形式、部署形式、加密貨幣類型、最終用戶和地區分類-2026-2033年產業預測