|

市場調查報告書

商品編碼

2066518

印度環氧樹脂市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)India Epoxy Resins - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

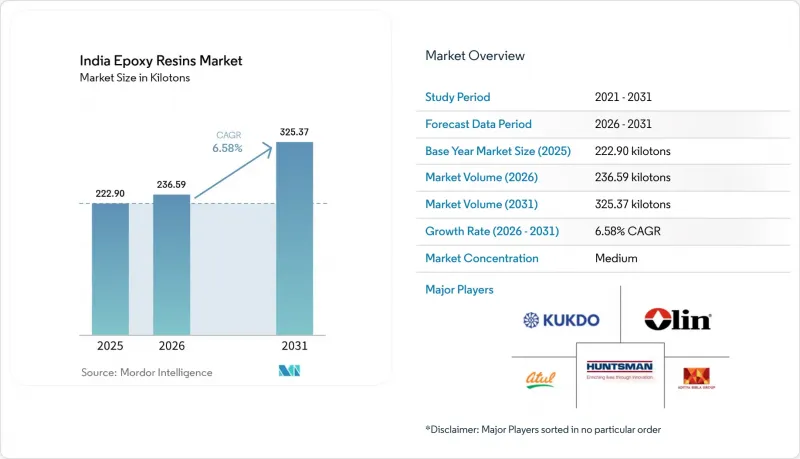

據 Mordor Intelligence 稱,2025 年印度環氧樹脂市場規模為 222.90 千噸,預計到 2031 年將達到 325.37 千噸,而 2026 年為 236.59 千噸,預測期(2026-2031 年)複合年成長率為 6.58%。

本報告按原料(DGEBA、DGEBF、酚醛清漆、脂肪族化合物、縮水甘油胺及其他原料)和應用領域(油漆和塗料、黏合劑和密封劑、複合材料、電氣和電子及其他應用領域)進行分類。市場預測以噸為單位。

印度環氧樹脂市場趨勢與洞察

二、三線城市基礎建設投資快速成長

政府為區域城市現代化所做的努力,推動了對耐用地板材料、防護塗料和結構性黏著劑的強勁需求,這些材料主要用於新建購物中心、醫院和教育設施。與大都會圈相比,這些地區擁有待開發區需求,且價格競爭較小,這使得製造商能夠維持利潤率。開發商更青睞無縫、衛生的地板材料,其性能優於陶瓷和水磨石等其他材料;而承包商則看重其縮短的工期。古吉拉突邦和馬哈拉斯特拉邦的製造地佔據了大部分樹脂供應,這得益於其鄰近的港口和完善的石化資源。隨著建設活動從沿海大都會圈向內陸擴展,供應商若能將經銷網路拓展至內陸地區,則可望進一步提升銷售量。

根據2025會計年度CAFE標準,促進車輛減重

更嚴格的企業平均燃油經濟性(CAFE)法規要求汽車製造商降低其車隊的排放氣體,從而推動車身面板、結構件和電池機殼中碳纖維和環氧複合材料的應用。一項政府資助的25938印度盧比(約31億美元)的生產關聯激勵(PLI)計劃,僅限於電動汽車、混合動力汽車和燃料電池汽車,正在加速對先進黏合劑和導熱環氧灌封化合物的中間需求。一級供應商正利用印度在大規模電子組裝的成熟能力,並實現複合材料材料子部件的在地化生產,從而增加樹脂的用量。輕量化是結構性必然要求,而非短期產量波動,確保了消費的穩定成長。

BIS 提出了關於樹脂中 BPA 殘留量的規定。

提案的品管指令對未反應的雙酚A (BPA) 含量設定了嚴格的限制,迫使製造商投資於純化、替代固化劑或不含BPA的化學物質。擁有雄厚研發資金的大型一體化製造商或許能夠迅速調整配方,並在出口市場利用其合規記錄。另一方面,如果資本需求超過流動性,小規模的區域性公司可能會面臨利潤率壓力和產業重組的風險。

細分市場分析

預計到2025年,DGEBA將佔據印度環氧樹脂市場64.02%的佔有率,並在2031年之前保持8.05%的複合年成長率。該樹脂具有優異的機械強度、耐化學性和成本效益,因此廣泛應用於塗料、電絕緣材料和複合材料領域。 DGEBF則面向電子和高溫應用,這些應用需要低黏度和高熱穩定性。酚醛樹脂滿足了對耐化學性要求極高的細分市場,例如化學處理罐的內襯。脂肪族樹脂具有優異的紫外線穩定性,適用於裝飾性塗料;而縮水甘油胺類樹脂則具有高金屬附著力和抗衝擊性,使其在船舶和航太塗料領域得到應用。其他原料還包括生物基和特種化學品,這些材料目前正因響應永續性的需求而湧現。

製造商正透過分階段的技術創新來應對未來的標準,例如縮短固化時間、使用低揮發性有機化合物(VOC)混合物以及減少雙酚A(BPA)含量。隨著更嚴格的BPA殘留標準可能迫使配方設計人員轉向使用二硫化石墨烯基環氧樹脂(DGEBF)或生物環氧樹脂,預計競爭將加劇。然而,鑑於目前成本績效的優勢,在2030年之前不太可能出現大規模的替代方案。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 二、三線城市基礎建設投資快速成長

- 根據2025會計年度CAFE標準,促進車輛減重

- 根據印度500吉瓦可再生能源目標,增加風力發電機葉片。

- 政府針對先進化學電池(ACC)電池組(封裝)的產品許可計劃(PLI)

- 有組織的零售業中地板材料和裝飾層壓板的快速成長

- 市場限制因素

- 樹脂中雙酚A殘留的BIS基準值草案

- 原油價格波動導致丙烯和苯酚原料價格波動

- 生物基不飽和聚酯替代品的日益普及。

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 按成分

- DGEBA(雙酚A和ECH)

- DGEBF(雙酚F和ECH)

- 酚醛樹脂(甲醛和苯酚)

- 脂肪族(脂肪醇)

- 縮水甘油胺(芳香胺和ECH)

- 其他原料

- 透過使用

- 油漆和塗料

- 黏合劑和密封劑

- 複合材料

- 電氣和電子設備

- 其他用途

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- 3M

- Aditya Birla Group

- Atul Ltd

- BASF

- Daicel Corporation

- DuPont

- Huntsman International LLC

- Kukdo Chemical Co., Ltd.

- Macro Polymers Pvt Ltd

- Nan Ya Plastics Corporation

- Olin Corporation

- Westlake Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the india epoxy resins market size was valued at 222.90 kilotons in 2025 and is estimated to grow from 236.59 kilotons in 2026 to reach 325.37 kilotons by 2031, at a CAGR of 6.58% during the forecast period (2026-2031).

This report is Segmented by Raw Material (DGEBA, DGEBF, Novolac, Aliphatic, Glycidylamine, and Other Raw Materials), and Application (Paints and Coatings, Adhesives and Sealants, Composites, Electrical and Electronics, and Other Applications). The Market Forecasts are Provided in Terms of Volume (Tons).

India Epoxy Resins Market Trends and Insights

Surging Infrastructure Spending in Tier-2 and Tier-3 Cities

Government missions to modernize secondary cities are driving robust uptake of heavy-duty epoxy flooring, protective coatings, and structural adhesives for new malls, hospitals, and education facilities. These locations offer greenfield demand where competitive pricing pressure is lower than in metros, enabling producers to sustain margins. Developers prefer seamless, hygienic epoxy floors that outperform ceramic and terrazzo alternatives, while contractors appreciate shorter project turnaround times. Manufacturing hubs in Gujarat and Maharashtra supply most of the resin volumes, benefitting from nearby ports and integrated petrochemical feedstocks. Suppliers that expand distribution into interior districts can capture incremental volume growth as construction activity spreads beyond coastal metros.

Automotive Lightweighting Push from FY 2025 CAFE Norms

Stricter Corporate Average Fuel Economy rules oblige automakers to lower fleet emissions, spurring adoption of carbon-fiber-epoxy composites for body panels, structural parts, and battery enclosures. The government's INR 25,938 crore (USD 3.1 billion) vehicle PLI scheme, restricted to EV, hybrid, and fuel-cell platforms, accelerates intermediate demand for advanced adhesives and thermally conductive epoxy potting compounds. Tier-1 suppliers leverage India's proven capability in scaled electronics assembly to localize composite sub-component fabrication, increasing resin off-take. Lightweighting is a structural necessity rather than a short-term volume swing, ensuring consistent consumption growth.

BIS Draft Limits on BPA Residuals in Resins

Proposed Quality Control Orders impose stringent caps on unreacted bisphenol A content, compelling manufacturers to invest in purification, alternative curing agents, or BPA-free chemistries. Large integrated producers with robust research and development funding can adjust formulations swiftly and may leverage compliance credentials in export markets. Smaller regional firms risk margin compression and potential consolidation if capital requirements exceed liquidity.

Other drivers and restraints analyzed in the detailed report include:

- Wind-Turbine Blade Additions Under India's 500 GW Renewables Target

- Government PLI Scheme for Advanced Chemistry Cell Battery Packs

- Volatile Propylene and Phenol Feedstock Prices Linked to Crude Swings

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

DGEBA accounted for 64.02% of India Epoxy Resin market share in 2025 and is forecast to post an 8.05% CAGR to 2031. The composition yields excellent mechanical strength, chemical resistance, and cost efficiency, supporting wide penetration in coatings, electrical insulation, and composites. DGEBF targets electronics and high-temperature sectors that require lower viscosity and higher thermal stability. Novolac systems fill niches needing exceptional chemical resistance, such as chemical-processing tank linings. Aliphatic resins deliver superior UV stability for decorative finishes, while glycidylamine grades provide high adhesion to metals and impact resistance, serving marine and aerospace coatings. Other raw materials include bio-based and specialty chemistries now emerging in response to sustainability mandates.

Producers use incremental innovations-faster cure, low-VOC blends, and BPA-reduced options-to address upcoming standards. Competitive tension may intensify if BPA residual limits push formulators toward DGEBF or bio-epoxies; however, current price-performance advantages make large-scale substitution unlikely before 2030.

List of Companies Covered in this Report:

- 3M

- Aditya Birla Group

- Atul Ltd

- BASF

- Daicel Corporation

- DuPont

- Huntsman International LLC

- Kukdo Chemical Co., Ltd.

- Macro Polymers Pvt Ltd

- Nan Ya Plastics Corporation

- Olin Corporation

- Westlake Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging infrastructure spending in Tier-2 and Tier-3 cities

- 4.2.2 Automotive lightweighting push from FY 2025 CAFE norms

- 4.2.3 Wind-turbine blade additions under India's 500 GW renewables target

- 4.2.4 Government PLI scheme for advanced chemistry cell (ACC) battery packs (encapsulants)

- 4.2.5 Rapid growth of organised retail flooring and decorative laminates

- 4.3 Market Restraints

- 4.3.1 BIS draft limits on BPA residuals in resins

- 4.3.2 Volatile propylene and phenol feedstock prices linked to crude swings

- 4.3.3 Rising popularity of bio-based unsaturated polyester alternatives

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Raw Material

- 5.1.1 DGEBA (Bisphenol A and ECH)

- 5.1.2 DGEBF (Bisphenol F and ECH)

- 5.1.3 Novolac (Formaldehyde and Phenols)

- 5.1.4 Aliphatic (Aliphatic Alcohols)

- 5.1.5 Glycidylamine (Aromatic Amines and ECH)

- 5.1.6 Other Raw Materials

- 5.2 By Application

- 5.2.1 Paints and Coatings

- 5.2.2 Adhesives and Sealants

- 5.2.3 Composites

- 5.2.4 Electrical and Electronics

- 5.2.5 Other Applications

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Aditya Birla Group

- 6.4.3 Atul Ltd

- 6.4.4 BASF

- 6.4.5 Daicel Corporation

- 6.4.6 DuPont

- 6.4.7 Huntsman International LLC

- 6.4.8 Kukdo Chemical Co., Ltd.

- 6.4.9 Macro Polymers Pvt Ltd

- 6.4.10 Nan Ya Plastics Corporation

- 6.4.11 Olin Corporation

- 6.4.12 Westlake Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

風力渦輪機葉片樹脂市場預測至2034年-按樹脂類型、應用、最終用戶和地區分類的全球分析

風力渦輪機葉片樹脂市場預測至2034年-按樹脂類型、應用、最終用戶和地區分類的全球分析 歐洲環氧樹脂:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

歐洲環氧樹脂:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 水性環氧樹脂市場:依應用、產品類型、分子量、最終用途產業和地區分類。

水性環氧樹脂市場:依應用、產品類型、分子量、最終用途產業和地區分類。 環氧樹脂市場:2026-2032年全球市場預測(依樹脂類型、形態、應用、終端用戶產業及通路分類)柔軟性環氧樹脂:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

環氧樹脂市場:2026-2032年全球市場預測(依樹脂類型、形態、應用、終端用戶產業及通路分類)柔軟性環氧樹脂:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 環氧樹脂市場:市場規模、佔有率、成長率、全球產業分析、按類型、應用和地區分類的分析以及未來預測(2026-2034 年)

環氧樹脂市場:市場規模、佔有率、成長率、全球產業分析、按類型、應用和地區分類的分析以及未來預測(2026-2034 年) 生物可再生環氧樹脂市場分析及預測(至2035年):類型、產品、應用、技術、材料類型、最終用戶、形態、製程、功能、安裝類型2026-2034年雙酚A氫全球市場規模、佔有率、趨勢和成長分析報告全球生物基環氧樹脂市場規模、佔有率、趨勢和成長分析報告(2026-2034)

生物可再生環氧樹脂市場分析及預測(至2035年):類型、產品、應用、技術、材料類型、最終用戶、形態、製程、功能、安裝類型2026-2034年雙酚A氫全球市場規模、佔有率、趨勢和成長分析報告全球生物基環氧樹脂市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026年全球環氧樹脂市場報告

2026年全球環氧樹脂市場報告